Retail Logistics Market Report Scope & Overview:

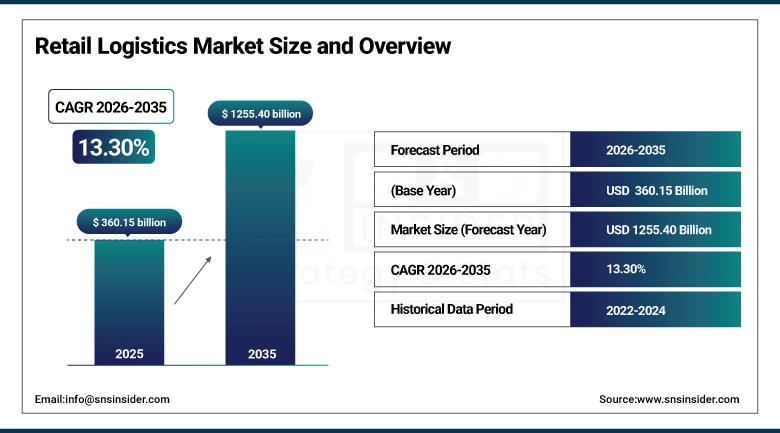

The Retail Logistics Market Size was valued at USD 360.15 billion in 2025 and is expected to reach USD 1255.40 billion by 2035, growing at a CAGR of 13.30% from 2026-2035.

Retail logistics market is growing rapidly due to the expansion of e-commerce, omnichannel retail strategies, and rising consumer expectations for faster and flexible deliveries. Increased adoption of automation, warehouse management systems, and real-time tracking technologies is improving operational efficiency. Additionally, growth in cross-border trade, urbanization, and demand for same-day and last-mile delivery services are driving investments in advanced logistics infrastructure, transportation networks, and digital supply chain solutions across global retail markets.

82% of global retailers deployed advanced logistics infrastructure leveraging automation, real-time tracking, and cross-border networks to cut delivery times by 40% and meet surging omnichannel demand.

Retail Logistics Market Size and Growth Forecast

-

Market Size in 2025: USD 360.15 Billion

-

Market Size by 2035: USD 1255.40 Billion

-

CAGR: 13.30% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Retail Logistics Market - Request Free Sample Report

Retail Logistics Market Trends

-

Rising adoption of omnichannel fulfillment models to support seamless online and offline retail logistics operations

-

Increasing investment in warehouse automation and robotics to improve order accuracy, speed, and cost efficiency

-

Growing demand for last-mile delivery optimization driven by rapid e-commerce growth and consumer expectations

-

Expansion of real-time tracking and visibility solutions to enhance supply chain transparency and customer satisfaction

-

Rising use of AI and data analytics for demand forecasting and inventory optimization across retail networks

U.S. Retail Logistics Market Size Outlook:

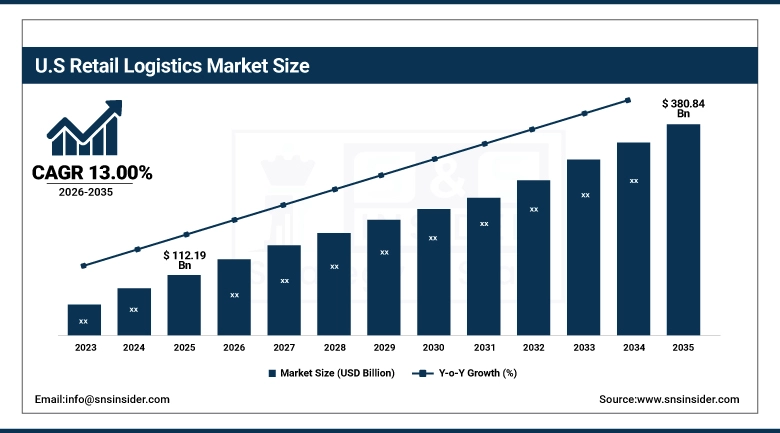

The U.S. Retail Logistics Market is valued at USD 112.19 billion in 2025 and is expected to reach USD 380.84 billion by 2035, growing at a CAGR of 13.00% from 2026-2035. U.S. retail logistics market is expanding due to strong e-commerce growth, widespread omnichannel retail adoption, and rising demand for faster delivery services. Increased investments in warehouse automation, last-mile delivery networks, advanced analytics, and real-time tracking technologies are further improving efficiency and driving sustained market growth.

Retail Logistics Market Growth Drivers:

-

Rapid growth of e-commerce and omnichannel retailing is driving demand for efficient retail logistics solutions supporting fast fulfillment, inventory visibility, and last-mile delivery operations

The rapid expansion of e-commerce and omnichannel retail has significantly increased complexity in retail supply chains. Consumers expect seamless shopping experiences across online and offline channels, requiring retailers to manage inventory efficiently and fulfill orders quickly. Retail logistics providers are increasingly adopting integrated warehousing, real-time inventory tracking, and advanced last-mile delivery solutions to meet these demands. High order volumes, seasonal peaks, and returns management further drive reliance on specialized logistics services. As digital retail continues to grow globally, efficient retail logistics remains critical for maintaining customer satisfaction, operational efficiency, and competitive advantage.

80% of retailers prioritized integrated logistics solutions achieving 95% inventory visibility and cutting last-mile delivery times by 35% to meet booming e-commerce and omnichannel demands.

-

Rising consumer expectations for same-day and next-day delivery are pushing retailers to invest in advanced logistics networks and outsourced retail logistics services

Modern consumers increasingly demand faster delivery times, making speed a key competitive differentiator for retailers. Same-day and next-day delivery expectations are driving investments in localized fulfillment centers, micro-warehousing, and optimized transportation networks. Retailers are also partnering with third-party logistics providers to enhance delivery speed, flexibility, and scalability. Advanced route optimization, real-time tracking, and last-mile innovations are being implemented to reduce delivery times. This growing demand for rapid fulfillment is accelerating the evolution of retail logistics models, strengthening the role of technology-enabled logistics partners in meeting customer expectations.

74% of retailers invested in advanced logistics networks or outsourced fulfillment enabling 65% of orders to meet same-day or next-day delivery demands and raising customer satisfaction by 28%.

Retail Logistics Market Restraints:

-

High transportation costs, fuel price volatility, and rising labor expenses increase operational complexity and reduce profit margins for retail logistics providers globally

Retail logistics providers face increasing cost pressures from fluctuating fuel prices, higher wages, and rising vehicle maintenance expenses. These factors significantly impact transportation and last-mile delivery costs, which represent a major portion of logistics spending. Labor shortages further increase reliance on temporary or premium workforce solutions, raising operational expenses. Cost volatility makes long-term pricing strategies difficult and compresses profit margins. Smaller logistics providers are particularly affected, limiting their ability to scale operations or invest in advanced technologies, thereby constraining overall market growth.

72% of retail logistics providers reported margin pressures driven by 30% higher fuel costs, volatile transport pricing, and rising labor expenses eroding profitability amid thin retail supply chain margins.

-

Infrastructure limitations, warehouse capacity constraints, and traffic congestion in urban areas hinder efficient retail logistics operations and timely order fulfillment

In many regions, inadequate infrastructure and limited warehouse availability restrict the efficiency of retail logistics operations. Urban congestion leads to delivery delays, increased fuel consumption, and higher operating costs. Limited space for large fulfillment centers in city areas complicates last-mile distribution strategies. Additionally, aging transportation networks in developing markets further affect reliability and speed. These infrastructure challenges reduce service quality, increase operational risks, and limit the ability of logistics providers to meet tight delivery timelines, negatively impacting customer satisfaction and market expansion.

68% of urban retailers faced fulfillment delays due to aging infrastructure, overcrowded warehouses, and traffic congestion increasing average delivery times by up to 22%.

Retail Logistics Market Opportunities:

-

Adoption of automation, robotics, AI, and warehouse management systems offers opportunities to improve efficiency, accuracy, and scalability in retail logistics operations

Advanced technologies are transforming retail logistics by improving operational efficiency and reducing human error. Automation and robotics streamline order picking, sorting, and packaging, while AI enhances demand forecasting and route optimization. Warehouse management systems enable real-time inventory visibility and faster fulfillment. These technologies reduce labor dependency, lower operational costs, and improve accuracy. Retail logistics providers adopting digital solutions can scale operations more effectively and handle high order volumes. Technology-driven logistics capabilities offer significant opportunities to enhance service quality and gain a competitive advantage.

75% of retail logistics operations integrated automation, AI, and WMS boosting order accuracy by 35% and throughput by 50% while enabling scalable fulfillment for e-commerce growth.

-

Expansion of cross-border e-commerce and emerging retail markets creates opportunities for logistics providers to offer integrated international warehousing and fulfillment services

The growth of cross-border e-commerce and rising retail activity in emerging markets present strong opportunities for retail logistics providers. Retailers expanding internationally require reliable logistics partners to manage customs clearance, international transportation, and regional warehousing. Integrated fulfillment solutions help reduce delivery times and operational complexity. As global online shopping increases, logistics providers can establish regional hubs and offer value-added services such as returns management and localized distribution. This expansion enables providers to tap into new revenue streams and strengthen their global footprint.

70% of logistics providers expanded integrated international warehousing and fulfillment solutions capturing a 40% increase in cross-border e-commerce demand from emerging retail markets.

Retail Logistics Market Segment Analysis

-

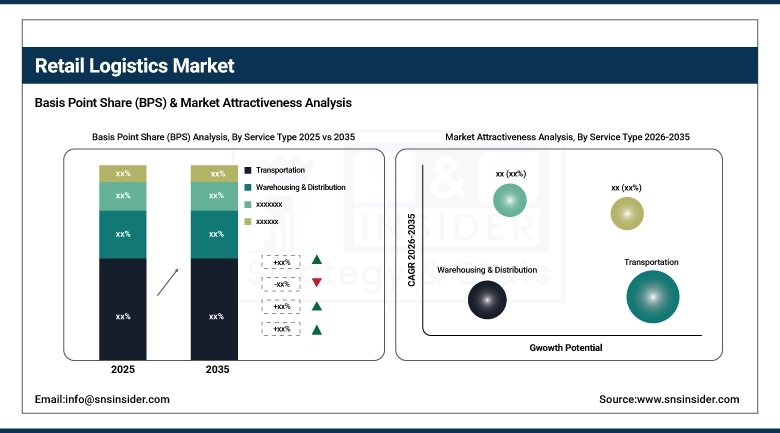

By Service Type: Transportation led with 38.6% share, while Reverse Logistics is the fastest-growing segment with CAGR of 18.4%.

-

By Mode of Transportation: Roadways led with 57.2% share, while Airways is the fastest-growing segment with CAGR of 19.1%.

-

By Retail Type: Online / E-commerce Retail led with 49.8% share, while Omnichannel Retail is the fastest-growing segment with CAGR of 17.6%.

-

By End-User: Grocery & Food Retail led with 34.5% share, while Pharmaceuticals & Healthcare is the fastest-growing segment with CAGR of 18.9%.

By Service Type: Transportation led, while Reverse Logistics is the fastest-growing segment.

Transportation dominates the retail logistics market as it forms the backbone of retail supply chains, enabling large-scale movement of goods from manufacturers to distribution centers and retail outlets. High demand from grocery, e-commerce, and consumer electronics retailers drives continuous freight movement, particularly for time-sensitive deliveries. Advancements in route optimization, fleet management systems, and last-mile delivery networks further strengthen this segment’s leadership. Its indispensability across all retail formats ensures steady volumes and recurring revenue, making transportation the most critical and dominant service type.

Reverse Logistics is the fastest-growing service type due to the rapid expansion of e-commerce and omnichannel retail models, which significantly increase product returns. Rising consumer expectations for hassle-free returns, refunds, and exchanges are forcing retailers to strengthen reverse supply chains. Sustainability initiatives, refurbishment, recycling, and resale of returned goods are also accelerating demand. The integration of digital tracking, AI-driven inspection, and automated sorting systems is enhancing efficiency, making reverse logistics a key growth driver in modern retail logistics.

By Mode of Transportation: Roadways led, while Airways is the fastest-growing segment.

Roadways dominate retail logistics because they provide unmatched flexibility, door-to-door connectivity, and cost efficiency for short- and medium-distance freight movement. Retailers heavily rely on road transport for last-mile and regional distribution, particularly in urban and semi-urban areas. The growth of organized retail, expansion of warehouse networks, and rising demand for same-day or next-day delivery further reinforce roadways’ dominance. Continuous investments in trucking fleets, cold-chain vehicles, and digital fleet management systems sustain this segment’s leading position.

Airways represent the fastest-growing transportation mode due to increasing demand for rapid delivery of high-value, time-sensitive, and perishable retail goods. Growth in cross-border e-commerce, pharmaceuticals, and premium consumer electronics is driving air freight adoption. Retailers increasingly use air logistics to meet tight delivery timelines and customer expectations. Improvements in air cargo infrastructure, expansion of dedicated cargo flights, and integration with express logistics providers are accelerating growth, positioning airways as a critical enabler of fast retail fulfillment.

By Retail Type: Online / E-commerce Retail led, while Omnichannel Retail is the fastest-growing segment.

Online / E-commerce Retail dominates retail logistics as digital shopping platforms generate high order volumes, frequent deliveries, and complex fulfillment requirements. The need for fast shipping, efficient inventory placement, and last-mile optimization drives extensive logistics demand. Growth in mobile commerce, subscription services, and direct-to-consumer brands further fuels logistics activity. Retailers’ investments in automated warehouses, fulfillment centers, and advanced order management systems strengthen e-commerce’s leadership, making it the largest contributor to retail logistics revenue.

Omnichannel Retail is the fastest-growing retail type as businesses integrate online and offline channels to deliver seamless customer experiences. Services such as buy-online-pickup-in-store, ship-from-store, and curbside pickup significantly increase logistics complexity and demand. Retailers require real-time inventory visibility, flexible distribution networks, and faster order orchestration. As consumer expectations shift toward convenience and channel flexibility, logistics providers are expanding omnichannel capabilities, driving rapid growth in this segment across global retail markets.

By End-User: Grocery & Food Retail led, while Pharmaceuticals & Healthcare is the fastest-growing segment.

Grocery & Food Retail dominates the end-user segment due to constant demand, high order frequency, and the essential nature of food products. This segment requires robust logistics support, including cold chain transportation, temperature-controlled warehousing, and rapid replenishment cycles. Growth in organized grocery retail, online grocery delivery, and quick-commerce platforms further intensifies logistics activity. The need for reliability, freshness, and speed ensures sustained logistics spending, reinforcing grocery and food retail’s dominant market position.

Pharmaceuticals & Healthcare is the fastest-growing end-user segment due to rising demand for temperature-sensitive drugs, medical supplies, and healthcare products. Expansion of online pharmacy platforms, direct-to-patient delivery models, and healthcare infrastructure development is driving logistics growth. Strict regulatory requirements, cold chain dependency, and real-time tracking needs are pushing retailers to partner with specialized logistics providers. Increasing healthcare consumption and aging populations worldwide further accelerate logistics demand in this segment.

Retail Logistics Market Regional Analysis

North America Retail Logistics Market Insights:

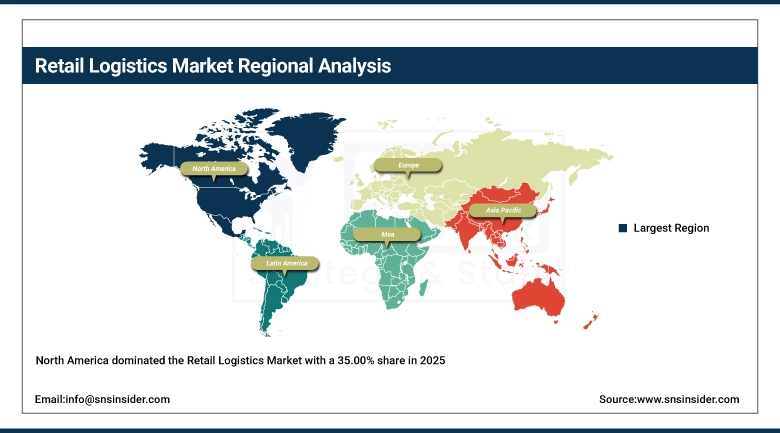

North America dominated the Retail Logistics Market with a 35.00% share in 2025 due to its highly developed supply chain infrastructure, strong presence of major retail and e-commerce players, and advanced adoption of automation and warehouse management technologies. Efficient last-mile delivery networks, high consumer demand, and widespread omnichannel retail models further reinforced regional market leadership.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Retail Logistics Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 15.02% from 2026–2035, driven by rapid e-commerce expansion, rising urbanization, and increasing consumer spending. Significant investments in logistics infrastructure, growth of cross-border trade, and adoption of digital logistics platforms are accelerating demand for modern retail logistics solutions across the region.

Europe Retail Logistics Market Insights

Europe held a significant share in the Retail Logistics Market in 2025, supported by well-established transportation networks, high penetration of organized retail, and strong growth in e-commerce across major economies. Increasing adoption of sustainable logistics practices, advanced warehouse automation, and cross-border trade within the region further strengthened Europe’s market position.

Middle East & Africa and Latin America Retail Logistics Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Retail Logistics Market in 2025, driven by expanding retail sectors, rising e-commerce adoption, and improving logistics infrastructure. Growing investments in warehousing, last-mile delivery capabilities, and digital supply chain technologies supported the regions’ gradual market expansion.

Retail Logistics Market Competitive Landscape:

DHL Supply Chain

DHL Supply Chain, a division of Deutsche Post DHL Group, is a global leader in contract logistics and supply chain management. The company provides end-to-end logistics solutions, including warehousing, transportation, and value-added services for retail, e-commerce, and industrial sectors. Known for its innovation and technology-driven operations, DHL focuses on optimizing efficiency, reducing costs, and enhancing customer satisfaction. With a presence in over 50 countries, DHL Supply Chain serves multinational corporations with scalable and sustainable logistics solutions worldwide.

-

May 2024, DHL Supply Chain launched Retail Pulse, an end-to-end AI-powered retail logistics platform designed to unify e-commerce, store replenishment, and returns management.

Kuehne + Nagel

Kuehne + Nagel, headquartered in Switzerland, is one of the world’s leading logistics providers specializing in sea freight, air freight, contract logistics, and integrated supply chain solutions. The company serves industries including retail, automotive, and pharmaceuticals, emphasizing efficiency, transparency, and reliability. Kuehne + Nagel leverages advanced IT systems, data analytics, and innovative technologies to optimize operations. With a strong global network of offices and warehouses, it provides flexible, sustainable, and cost-effective logistics solutions to multinational clients.

-

February 2025, Kuehne + Nagel launched KN Retail Chain, a green urban logistics solution for fast-moving consumer goods (FMCG) and fashion retailers, featuring electric last-mile delivery and dark store integration.

DB Schenker

DB Schenker, a division of Deutsche Bahn AG, is a top global logistics provider offering comprehensive supply chain solutions including land transport, air and ocean freight, and contract logistics. The company focuses on integrating technology, sustainability, and process efficiency to meet customer demands across retail, automotive, and healthcare sectors. DB Schenker operates an extensive network of warehouses and transport services worldwide, ensuring reliable and flexible logistics solutions, while emphasizing innovation, digitalization, and environmentally responsible supply chain practices.

-

October 2023, DB Schenker introduced Retail Flow, a unified logistics platform connecting brick-and-mortar stores with direct-to-consumer (DTC) channels.

Retail Logistics Companies are:

-

DHL Supply Chain

-

Kuehne + Nagel

-

DSV A/S

-

XPO Logistics

-

CEVA Logistics

-

UPS Supply Chain Solutions

-

FedEx Logistics

-

C.H. Robinson

-

Nippon Express

-

Geodis

-

Ryder System

-

Toll Group

-

Kerry Logistics

-

GXO Logistics

-

Sinotrans

-

Penske Logistics

-

Yusen Logistics

-

Schneider Logistics

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 360.15 Billion |

| Market Size by 2035 | USD 1255.40 Billion |

| CAGR | CAGR of 13.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Transportation, Warehousing & Distribution, Inventory Management, Order Fulfillment, Reverse Logistics) • By Mode of Transportation (Roadways, Railways, Airways, Waterways) • By Retail Type (Online / E-commerce Retail, Offline / Brick-and-Mortar Retail, Omnichannel Retail) • By End-User (Grocery & Food Retail, Apparel & Fashion, Consumer Electronics, Pharmaceuticals & Healthcare, Home & Furniture) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DHL Supply Chain, Kuehne + Nagel, DB Schenker, DSV A/S, XPO Logistics, CEVA Logistics, UPS Supply Chain Solutions, FedEx Logistics, C.H. Robinson, Nippon Express, Geodis, Ryder System, Expeditors International, Toll Group, Kerry Logistics, GXO Logistics, Sinotrans, Penske Logistics, Yusen Logistics, Schneider Logistics. |

Frequently Asked Questions

The Retail Logistics Market is expected to grow at a CAGR of 13.30% from 2026 to 2035, driven by e-commerce expansion and omnichannel retail adoption.

In 2025, the Retail Logistics Market is valued at USD 360.15 billion, supported by rising demand for faster deliveries, automation, and advanced supply chain solutions globally.

Key growth drivers include e-commerce growth, omnichannel retail strategies, last-mile delivery optimization, adoption of automation, AI, warehouse management systems, and real-time tracking technologies.

Transportation service type, Roadways transportation mode, Online/E-commerce retail type, and Grocery & Food Retail end users dominated the Retail Logistics Market.

North America dominated in 2025 with a 35.00% share, due to advanced supply chain infrastructure, widespread e-commerce adoption, and robust last-mile and warehouse capabilities.

Get in Touch