RF Semiconductor Market Size & Growth:

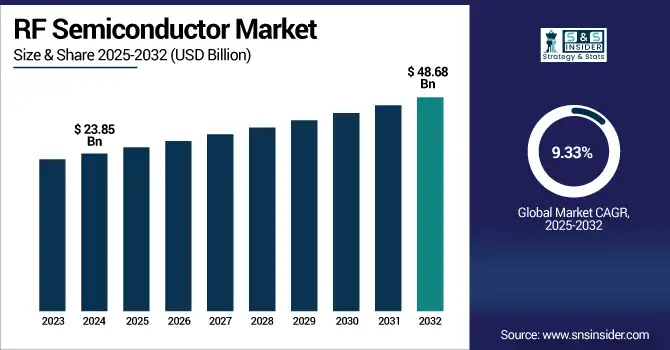

The RF Semiconductor Market size was valued at USD 23.85 Billion in 2024 and is projected to reach USD 48.68 Billion by 2032, growing at a CAGR of 9.33% during 2025-2032. The RF semiconductor market is witnessing robust and continued growth with the increasing number of high-frequency components that are required for 5G networks, IoT devices, satellite communications, and advanced driver-assistance systems (ADAS drivers). Disruptive in nature as these semiconductors are the basic building block of almost any electronic device that requires wireless transmission, including smartphones, base stations, automotive radar, and industrial automation.

To Get more information on RF Semiconductor Market - Request Free Sample Report

With the rapidly changing demand for wireless connectivity, the RF components are required to be miniaturized, high-performance, and energy-efficient and the advancement of technology would be the major driving factor for this. Moreover, growth of smart cities, electric vehicles, and next-gen wireless infrastructure is driving new use cases. Demand for RF technologies will continue to increase due investment in research and development, which along with the proliferation of RF technologies across broader sectors will lead to steady market growth until 2032 with growing commercial as well as industrial adoption of the technology.

Mitsui Fudosan To Set Up Semiconductor Research And Development Base In TokyoWants to bring together 200-300 corporations and institutions from Nihonbashi to foster chip development and talent.

The U.S RF Semiconductor Market size was valued at USD 4.26 Billion in 2024 and is projected to reach USD 9.13 Billion by 2032, growing at a CAGR of 9.97% during 2025-2032. The growth of the U.S. The demand for 5G infrastructure development, IoT devices, and advanced automotive electronics are fostering the growth of RF semiconductor market. Growing usage of high frequency communication technologies in smartphones, defence systems and connected vehicles, is accelerating growth of the market.

The U.S. RF semiconductor market trend is the rapid shift toward high-frequency and mmWave technologies to support 5G, satellite communications, and autonomous vehicle systems. Manufacturers are increasingly focusing on GaN- and GaAs-based RF components for enhanced performance, power efficiency, and miniaturization. The integration of RF front-end modules in compact devices, along with advancements in beamforming and signal filtering, is also gaining momentum, driving innovation across telecom, automotive, aerospace, and consumer electronics sectors.

RF Semiconductor Market Dynamics:

Drivers:

-

Policy Support and Supply Chain Maturity Drive RF Semiconductor Growth

The RF semiconductor market is experiencing significant growth driven by strong policy support, All of these technologies drive new performance demands and functionality in RF components providing a huge opportunity with the 5G, edge AI, and IoT applications, etc. Existing supply chains for silicon wafers, lithography tools and testing equipment are proving sturdy, allowing rapid innovation and scalable production. Industry/Academia/Manufacturing collaboration to further streamline development and deployment of RF technologies across telecom, automotive, and industrial sectors.

Japan to partner with the world on chips to become global MRAM hubRobust subsidies, edge-AI collaborations, and world-class local suppliers are fuelling for Japan's rise as a semiconductor superpower

Restraints:

-

High Production Costs and Supply Challenges Restrain RF Semiconductor Market Growth

High Cost and Complexity of Manufacturing Cutting-edge components are some of the factors that are delimiting the growth of the RF semiconductor market. High-frequency chips, especially GaN and GaAs chips, demand strict materials, fabrication and testing processes, leading to higher capital expenditure. Moreover, global supply chain disruptions and geopolitical uncertainties affect the availability of raw materials and equipment used in the manufacture of the essential components. It also slows down development as there is also a shortage of engineers who know how to design and integrate RF systems. The regulatory landscapes, from spectrum licensing and compliance requirements, bedevil market entry and expansion. Therefore, all of these elements combine to restrict scalability, delay time-to-market, and make it increasingly difficult to satisfy rapidly rising worldwide demand for RF-enabled devices.

Opportunities:

-

Wide Bandgap Materials Unlock New Opportunities in the RF Semiconductor Market

The RF semiconductor market is witnessing new growth opportunities with the emergence of wide bandgap materials, particularly gallium nitride (GaN). Capable of operating at higher frequencies and temperatures while delivering superior power efficiency, GaN is well-suited for next-generation RF applications such as 5G, radar, aerospace, and military communications. Its high thermal conductivity and performance advantages over traditional silicon open pathways for more compact and durable RF devices. Moreover, the ability to fabricate GaN on silicon wafers allows cost-effective production in existing fabs, enhancing scalability. These advancements are driving innovation across telecommunications, defense, and industrial sectors, positioning GaN-based RF semiconductors as a transformative technology for future high-frequency, high-power applications.

GaN Positioned to Disrupt RF Semiconductors with Wide Bandgap AdvantagesGaN chips ideal next-gen RF semiconductor building blocks bring unrivaled frequency, power and heat performance to military, telecom and aerospace applications.

Challenges:

-

Material Limitations and Integration Complexities Challenge RF Semiconductor Market Expansion

The growth of the RF semiconductor market is challenged by material limitations, thermal management issues, and integration complexities. State of the art RF devices are also dependent on advanced RF components, while GaN and SiC based wide bandgap RF devices suffer issues such as lattice mismatches, thermal expansion differences and expensive fabrication cost. Such complications in the manufacturing process result in higher defect risk. Moreover, fully integrated RF semis with CMOS technology has proven to be challenging: these technologies often operate at different processing temperatures and have different chipset structures. Engineering challenges are also found in packaging and miniaturization for high-frequency applications, especially when it comes to signal loss and heat management. These technical barriers create longer development cycles and higher costs of production, thereby restricting the outreach and adoption of RF solutions into large array of use cases associated with commercial, industrial and defense applications.

RF Semiconductor Market Segmentation Analysis:

By Product Type

In 2024, the RF Power Amplifier segment accounted for approximately 38% of the RF semiconductor market share, due to a rapid demand for high-efficiency signal amplification for 5G infrastructure, satellite communication, and defense systems in 2024. As such, it has proven to be an essential – if not somewhat of a cornerstone – buildingblock across telecom, aerospace and automotive RF applications because ofits pivotal role enabling high-frequency, high-power transmission.

The RF Low Noise Amplifier segment is expected to experience the fastest growth in RF semiconductor market over 2025-2032 with a CAGR of 10.76%, owing to its increasing usage in 5G smartphones, IoT devices, and satellite communication systems. And that would help in weak signal reception with very little added noise, making it a key component in next-gen wireless networks, as well as in radar and high-frequency automotive applications.

By Material

In 2024, the Gallium Arsenide (GaAS) segment accounted for approximately 34% of the RF semiconductor market share, due to its high-frequency performance and high electron mobility. RF front-end modules for smartphones, satellite communication devices and radar systems all utilize GaAs due to its utility in high-frequency systems. The material is also fairly useful for high performance wireless applications because of its power amplification efficiency and signal integrity.

The Gallium Nitride (GaN)segment is expected to experience the fastest growth in RF semiconductor market over 2025-2032 with a CAGR of 11.63%, propelled by high-power and high-frequency applications like 5G infrastructure, military radar, and satellite communications. This characteristic, along with good breakdown voltage, efficiency, and thermal stability makes it a perfect candidate for next-generation RF power devices in almost all aerospace, defense and telecom sectors.

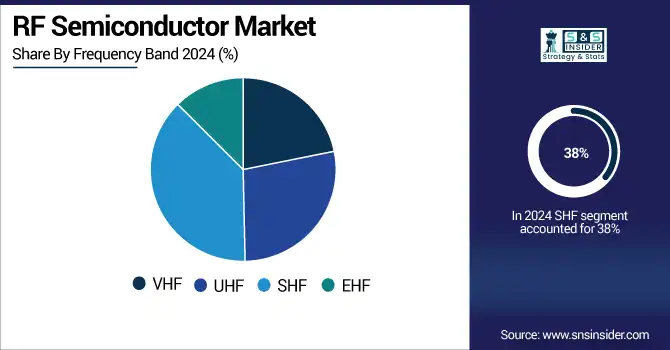

By Frequency Band

In 2024, the SHF segment accounted for approximately 38% of the RF semiconductor market share, owing to increasing adoption in satellite communications, high-resolution radar systems, and 5G base stations. SHF components have the advantages in transmission of high-data-rates and low-latency communication, where they are important not only for the commercial but also for the defense market. Growing wireless backhaul networks, erupting necessity for real-time information transfer among the aerospace and telecom zones, also prods the segment to strengthen its hold in the market.

The EHF segment is expected to experience the fastest growth in RF semiconductor market over 2025-2032 with a CAGR of 12.34%, driven by higher power demands in the advanced military communication systems, next-gen satellite networks, and the emerging 6G technologies. Broadly speaking, EHF semiconductors will facilitate data transmission at very high speeds, low-latency connectivity, and secure long-range communication.

By Application

In 2024, the Consumer Electronics segment accounted for approximately 34% of the RF semiconductor market share, driven by the proliferation of smartphones, smart TVs, wearables, and wireless audio devices. The segment accounted for the majority of the revenue share owing to rising implementation of RF chips for 5G, Wi-Fi 6/6E and Bluetooth connectivity in increasingly smaller consumer devices across established and new digital economies.

The Telecommunication segment is expected to experience the fastest growth in RF semiconductor market over 2025-2032 with a CAGR of 11.06%, ueled by rising 5G infrastructure deployments, increasing mobile data consumption, and expanding IoT connectivity. Demand for high-frequency, high-power RF components is surging as operators upgrade networks to support faster speeds, lower latency, and massive device integration.

RF Semiconductor Market Regional Insights

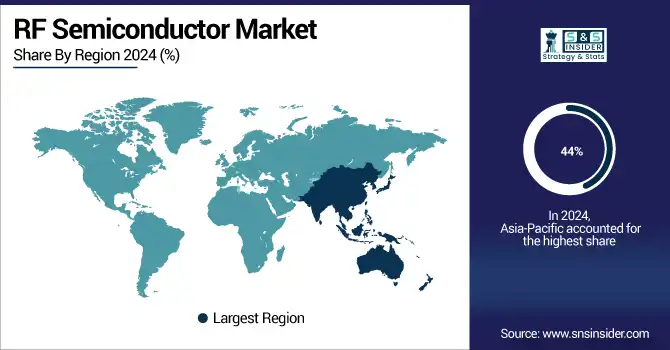

In 2024 Asia-Pacific dominated the RF semiconductor market and accounted for 44% of revenue share. propelled due to manufacturing hubs in regions such as China, South Korea, and Taiwan. High demand among consumer electronics, 5G infrastructure, and automotive sectors is propelling the region. Coupled with government support, local supply chains in Taiwan, and growing investment in R&D, this also strengthens Taiwan's position as a leader in RF semiconductor production and innovation.

North America is expected to witness the fastest growth in the RF semiconductor market over 2025-2032, with a projected CAGR of 11.04% owing to accelerating adoption of 5G networks, escalating defense and aerospace spending, along with high proliferation of advanced RF components & technologies in IoT and connected devices. Regional markets are driven by robust innovation ecosystems and supportive government initiatives.

In 2024, Europe emerged as a promising region in the RF semiconductor market, driven by strong investments in automotive electronics, 5G infrastructure, and industrial IoT. Countries like Germany and France are advancing smart manufacturing and connected vehicle technologies, fueling RF component demand. Additionally, supportive EU policies and R&D funding are fostering innovation and strengthening regional supply chains.

LATAM and MEA are experiencing steady growth in the RF semiconductor market, driven by rising urbanization, driven by rising urbanization, increasing smartphone penetration, and expanding telecom infrastructure. Governments in these regions are investing in digital transformation and 5G deployment, creating demand for RF components. Though market share remains smaller compared to other regions, growth potential is significant over the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

RF Semiconductor Companies are:

The Key Players in RF semiconductor market are Qorvo, Skyworks, Analog Devices, NXP Semiconductors, Texas Instruments, Cree, Microchip Technology, Murata Manufacturing, ON Semiconductor, MACOM, Broadcom, Infineon Technologies, STMicroelectronics, Renesas Electronics, Qualcomm, Toshiba, Samsung Electronics, Maxim Integrated, RF Micro Devices, Avago Technologies, and Others.

Recent Developments:

-

In June 2024, Qorvo Expands Radar Capabilities with Compact, High-Performance RF Multi-Chip ModulesNew X-, S-, and L-band modules offer reduced size, power consumption, and streamlined integration for advanced radar systems.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 23.85 Billion |

| Market Size by 2032 | USD 48.68 Billion |

| CAGR | CAGR of 9.33% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type(RF Power Amplifier(RF Filter, RF Switch, RF Low Noise Amplifier and Others (RF Phase Shifters, Oscillator, Couplers, Attenuator, and others)) • By Material(Silicon (Si), Silicon - Germanium (SiGe), Gallium Arsenide (GaAS), Gallium Nitride (GaN) and Indium Phosphite (InP)) • By Frequency Band(VHF, UHF, SHF and EHF) • By Application(Telecommunication, Consumer Electronics, Automotive, Aerospace & Defense, Healthcare and Others (Industrial Automation)), |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The RF semiconductor market Companies are Qorvo, Skyworks, Analog Devices, NXP Semiconductors, Texas Instruments, Cree, Microchip Technology, Murata Manufacturing, ON Semiconductor, MACOM, Broadcom, Infineon Technologies, STMicroelectronics, Renesas Electronics, Qualcomm, Toshiba, Samsung Electronics, Maxim Integrated, RF Micro Devices, Avago Technologies, and Others. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the RF Semiconductor Market in 2024.

Ans: The “RF Power Amplifier “segment dominated the RF Semiconductor Market

Ans: Rising demand for high-speed wireless communication, 5G deployment, and advanced radar systems are key drivers of the RF Semiconductor Market.

Ans: The RF Semiconductor Market size was valued at USD 23.85 Billion in 2024 and is projected to reach USD 48.68 Billion by 2032

Ans: The RF Semiconductor Market is expected to grow at a CAGR of 9.33% during 2025-2032.

Get in Touch