Rockets and Missiles Market Report Scope & Overview:

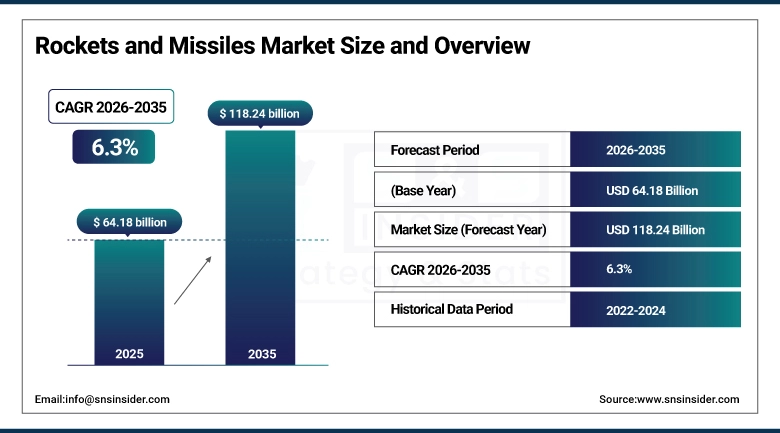

The Rockets and Missiles Market size was valued at USD 64.18 Billion in 2025 and is projected to reach USD 118.24 Billion by 2035, growing at a CAGR of 6.3% during 2026–2035.

The Rockets and Missiles market is one of the significant markets in the global defense sector, which is fueled by the rising security challenges and the growing defense modernization programs. The market is witnessing an increased demand for advanced technologies in terms of precision, range, and speed. The sector is also witnessing advancements in propulsion and guidance technologies. The governments across the globe are investing heavily in advanced technologies in the next-generation weapons. Additionally, the sector is also witnessing the benefits of the growing trend towards indigenization and the adoption of advanced digital and autonomous technologies.

Rockets and Missiles Market Size and Forecast:

-

Market Size in 2025: USD 64.18 Billion

-

Market Size by 2035: USD 118.24 Billion

-

CAGR: 6.3% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Rockets and Missiles Market - Request Free Sample Report

Rockets and Missiles Market Key Trends:

-

Rapid development and deployment of hypersonic missiles (Mach 5+) for advanced strike capabilities

-

Increasing integration of AI and advanced guidance systems for precision targeting

-

Growing demand for missile defense systems, including anti-ballistic and interceptor technologies

-

Rising focus on indigenous missile development and domestic defense manufacturing

-

Expansion of multi-platform launch capabilities across air, land, and naval forces

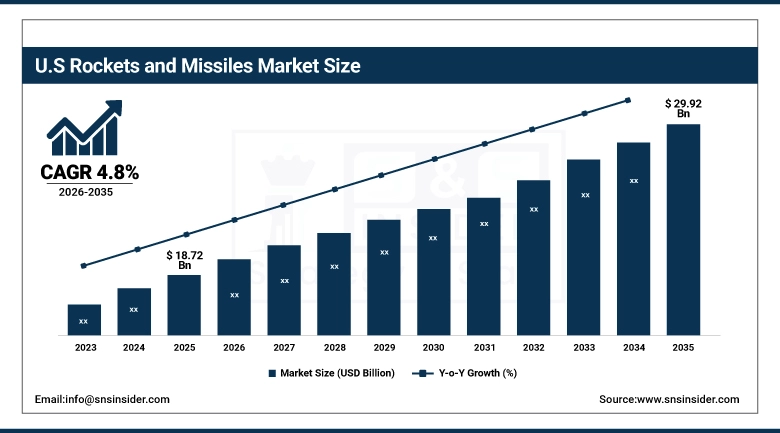

The U.S. Rockets and Missiles Market has been valued at USD 18.72 Billion in 2025 and is expected to reach USD 29.92 Billion in 2035, growing at a CAGR of 4.8% from 2026 to 2035, Growth of the U.S. Rockets and Missiles Market is driven by rising defense spending, continuous modernization of military capabilities, increasing investments in hypersonic and missile defense systems, and strong presence of leading defense contractors.

Rockets and Missiles Market Key Drivers:

-

Rising geopolitical tensions and increasing defense modernization programs drive demand for advanced missile systems.

The major driving force in the rockets and missiles market is the increased number of geopolitical conflicts, border issues, and security concerns in different parts of the world, including the Asia-Pacific region, Middle East, and Eastern Europe. Governments are investing heavily in defense systems to enhance their military capabilities in different defense domains. Technological advancements in hypersonic technology are also driving this market. Furthermore, the focus on developing indigenous defense capabilities is also increasing investments in defense technology around the world.

Rockets and Missiles Market Key Restraints:

-

High development costs and strict international regulations limit market expansion.

There are some challenges facing the rockets and missiles industry, which may affect the growth of the industry in the future. The first challenge is the cost factor, which is quite high in the case of missile technology, making it difficult for smaller countries to afford this technology. The next challenge is the international regulations and treaties related to the sale and trade of missiles, which may affect the growth of this industry. The testing and maintenance cost is another factor, which may affect the growth of this industry.

Rockets and Missiles Market Key Opportunities:

-

Advancements in hypersonic technology and missile defense systems create strong growth opportunities.

The growing interest in next-gen warfare technologies is creating opportunities for growth in the rockets & missiles market. Development of hypersonic missiles that can travel at speeds above Mach 5 is gaining momentum among the prominent defense forces of the world. Furthermore, the increasing need for advanced missile defense technologies is also creating opportunities for growth in the market. Emerging technologies such as artificial intelligence, sensors, and autonomous targeting are also improving missile capabilities. Increasing investments in local defense manufacturing capabilities and international defense projects are also expected to contribute to the growth of the market.

Rockets and Missiles Market Segments:

-

By Speed: In 2025, Supersonic dominated with 47% share; Hypersonic fastest growing segment during 2026-2035

-

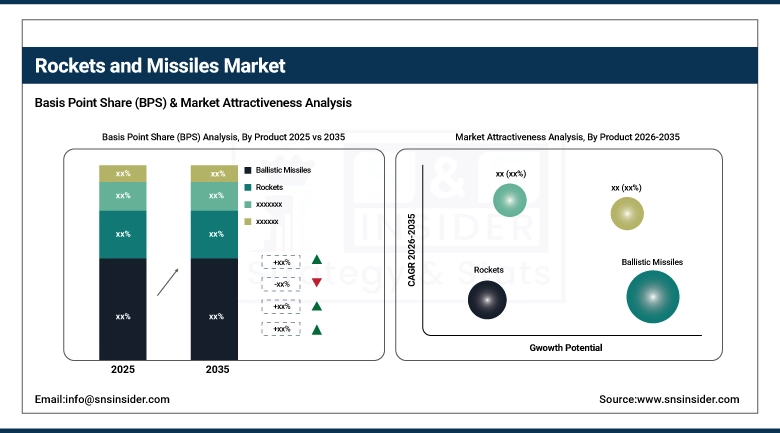

By Product: In 2025, Ballistic Missiles dominated with 38% share; Cruise Missiles fastest growing segment during 2026-2035

-

By Propulsion Type: In 2025, Solid dominated with 52% share; Scramjet fastest growing segment during 2026-2035

-

By Guidance Mechanism: In 2025, Guided dominated with 73% share; Guided fastest growing segment during 2026–2035

-

By Launch Mode: In 2025, Surface to Surface dominated with 33% share; Subsea to Surface fastest growing segment during 2026–2035

Rockets and Missiles Market Segment Analysis:

By Product: Ballistic Missiles Dominate, Cruise Missiles Fastest-Growing

Ballistic missiles hold the largest share in the product segment, largely because of their importance in strategic deterrence. Ballistic missiles are an important part of a country’s defense system, especially with respect to nuclear deterrence. They have been largely employed by different countries for their military purposes.

Cruise missiles hold the largest share in the growth segment, largely because of their accuracy, low-flying abilities, and versatility with different platforms. They have become an important part of modern warfare, especially with their ability to inflict surgical strikes with minimal collateral damage.

By Speed: Supersonic Dominates, Hypersonic Fastest-Growing

Supersonic missiles have the highest market share in the speed segment, owing to their widespread use in air, land, and sea warfare. Supersonic missiles provide the best trade-off in terms of speed, cost-effectiveness, and reliability, making them highly suitable for warfare operations. The existing infrastructure and compatibility with existing defense systems have added to the dominance of supersonic missiles in the global defense industry.

Hypersonic missiles have the highest growth rate, mainly due to the increase in investments in next-generation missiles, which have the capability to operate at speeds higher than Mach 5. The missiles possess better penetration capabilities against advanced enemy air defense systems and reduce the reaction time for the enemy. The U.S., China, and Russia are investing heavily in hypersonic missiles, which is causing this market to grow rapidly.

By Propulsion Type: Solid Propellant Dominates, Scramjet Fastest-Growing

The market is dominated by solid propulsion systems due to their reliability, easy storage capabilities, and fast readiness for launch. They are also widely used for both tactical and strategic missiles because of their easy maintenance capabilities and simplicity of operation. Their reliability in varied combat situations is another factor that puts these systems at the forefront of the market.

The scramjet propulsion system is the fastest-growing segment of the market due to the development of hypersonic missiles. Scramjet propulsion is capable of achieving hypersonic speeds using the oxygen present in the atmosphere for combustion.

By Guidance Mechanism: Guided Systems Dominate and Fastest-Growing

Guided missiles are at the forefront in this segment, considering the need to increase accuracy in targeting. The missiles employ various technologies, like GPS, inertial guidance, radar, and infrared guidance, to accurately target their enemies. The effectiveness of these missiles in reducing damage to properties during attacks has made them popular.

The guided segment is growing at the fastest rate due to the constant improvements being made to artificial intelligence, sensor technology, and real-time data processing. Precision engagement is becoming an essential part of modern warfare, thus promoting the growth of this segment.

By Launch Mode: Surface-to-Surface Dominates, Subsea-to-Surface Fastest-Growing

The launch mode segment is dominated by surface-to-surface missiles owing to their widespread use in ground-based military operations. These types of missiles are increasingly used in ground-based military operations. Their incorporation in the defense strategies of various nations also contributes to their popularity.

The subsea-to-surface missile segment is growing at a high rate owing to the expansion in naval defense strategies. Second-strike capability is considered essential in naval defense strategies. This capability is offered by submarine-launched ballistic missiles. These types of missiles ensure the stealth and survival of submarines. The rising investment in submarine defense strategies across the globe is also boosting this segment.

Rockets and Missiles Market Regional Analysis:

North America Rockets and Missiles Market Insights:

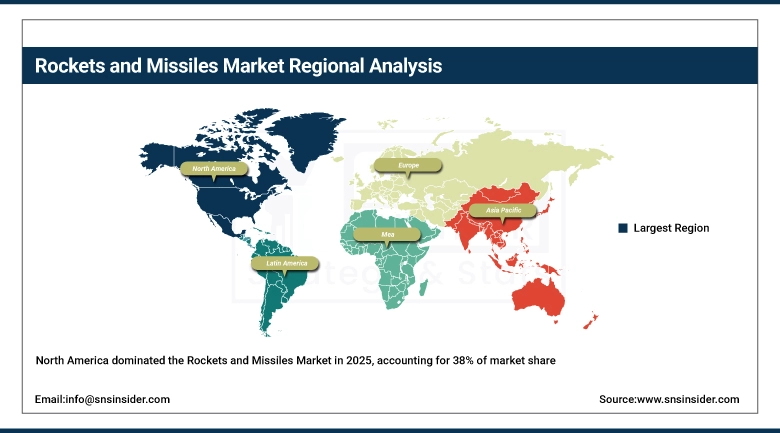

North America holds the largest share in the market in terms of rockets and missiles. It accounts for about 38% of the market share in 2025. This is mainly because of the high defense expenditure and technological advancements in the country. The presence of major defense companies such as Lockheed Martin, RTX, and Northrop Grumman also contributes to the high market share in the region. The investments in advanced missile technologies such as hypersonic and missile defense also add to the high market share.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Rockets and Missiles Market Insights:

Europe also plays an important role in the market for rockets and missiles. This is mainly because of the rising defense cooperation and modernization efforts in all the NATO countries. Many European countries, such as the UK, France, and Germany, are developing advanced missile defense systems to ensure the security of the region. Many collaborative efforts are being undertaken by organizations such as MBDA to ensure the development of enhanced missile defense capabilities in European countries. Furthermore, there is a rising focus on developing air and missile defense systems in the region.

Asia-Pacific Rockets and Missiles Market Insights:

The rockets and missiles market is growing at a fast pace in the Asia-Pacific region. The growth is mainly due to the rise in geopolitical situations, border disputes, and increased defense spending in countries such as China, India, Japan, and South Korea. The governments are investing heavily in indigenous missile development projects to enhance their military capabilities. Apart from that, rapid modernization of their defense forces is also contributing to the growth of the rockets and missiles market in the Asia-Pacific region.

Latin America Rockets and Missiles Market Insights:

Latin America is a smaller but growing market for rockets and missiles, as countries such as Brazil, Mexico, and Chile are modernizing their defense capabilities at a slow pace. Countries are trying to boost their national security, borders, and counter-narcotics capabilities. This has created a need for tactical missiles/rockets. Brazil is investing heavily in indigenous defense manufacturing capabilities. Countries are trying to boost their national security, borders, and counter-narcotics capabilities. This has created a need for tactical missiles/rockets. Brazil is investing heavily in indigenous defense manufacturing capabilities.

Middle East & Africa (MEA) Rockets and Missiles Market Insights:

Middle East & Africa is an important region in terms of rockets and missiles, considering the conflicts and geopolitical situations in this region, which has led to higher defense spending in countries like Saudi Arabia, Israel, and the UAE. The region has shown high demand for missile defense systems, which are highly sophisticated in nature. Apart from this, countries in this region are showing higher spending on precision-guided munitions, which is helping the rockets and missiles industry grow in this region. In the African region, the industry is growing gradually.

Rockets and Missiles Market Competitive Landscape:

Lockheed Martin Corporation is a company that was formed in 1995 and is one of the world's leading aerospace and defense companies. The company specializes in the development of advanced missile systems, tactical missiles, and defense solutions. The company is involved in the development of critical missile systems such as the PAC-3 missile defense system, THAAD missile defense system, and other air-to-surface and surface-to-surface missile defense systems. The company has operations across the globe with main offices in the US.

-

In 2024, Lockheed Martin announced advancements in its hypersonic missile programs, focusing on enhancing long-range strike capabilities and accelerating the development of next-generation precision-guided systems to support evolving military requirements.

RTX Corporation (Raytheon Technologies) was established in 2020 following the merger of Raytheon Company and United Technologies Corporation and is a major player in defense technologies, particularly in missile systems and air defense solutions. The company manufactures widely used systems such as the Tomahawk cruise missile, Standard Missile series, and NASAMS air defense system. RTX operates across multiple countries, supplying advanced missile technologies to allied defense forces worldwide.

-

In 2024, RTX announced upgrades to its missile defense portfolio, including enhancements to the Patriot air and missile defense system, aimed at improving interception capabilities against advanced aerial and ballistic threats.

Rockets and Missiles Market Key Players:

-

Lockheed Martin Corporation

-

RTX Corporation (Raytheon Technologies)

-

Northrop Grumman Corporation

-

Boeing Defense, Space & Security

-

BAE Systems plc

-

MBDA Inc.

-

Thales Group

-

Saab AB

-

Rafael Advanced Defense Systems Ltd.

-

Israel Aerospace Industries (IAI)

-

General Dynamics Corporation

-

L3Harris Technologies, Inc.

-

Kongsberg Gruppen ASA

-

Bharat Dynamics Limited (BDL)

-

Defence Research and Development Organisation (DRDO)

-

China Aerospace Science and Technology Corporation (CASC)

-

China Aerospace Science and Industry Corporation (CASIC)

-

Rostec State Corporation

-

Tactical Missiles Corporation (KTRV)

-

Mitsubishi Heavy Industries Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 64.18 Billion |

| Market Size by 2035 | USD 118.24 Billion |

| CAGR | CAGR of 6.3% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Speed: (Subsonic, Supersonic, Hypersonic) • By Product: (Cruise, Ballistic Missiles, Rockets, Torpedo) • By Propulsion Type: (Solid, Liquid, Hybrid, Ramjet, Turbojet, Scramjet) • By Guidance Mechanism: (Guided, Un-Guided) • By Launch Mode: (Surface to Surface, Surface to Air, Air to Air, Air to Surface, Subsea to Surface) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, RTX Corporation (Raytheon Technologies), Northrop Grumman Corporation, Boeing Defense, Space & Security, BAE Systems plc, MBDA Inc., Thales Group, Saab AB, Rafael Advanced Defense Systems Ltd., Israel Aerospace Industries (IAI), General Dynamics Corporation, L3Harris Technologies, Inc., Kongsberg Gruppen ASA, Bharat Dynamics Limited (BDL), Defence Research and Development Organisation (DRDO), China Aerospace Science and Technology Corporation (CASC), China Aerospace Science and Industry Corporation (CASIC), Rostec State Corporation, Tactical Missiles Corporation (KTRV), Mitsubishi Heavy Industries Ltd. |

Frequently Asked Questions

Ans: The Rockets and Missiles Market is expected to grow at a CAGR of 6.3% during 2026–2035.

Ans: The market was valued at USD 64.18 Billion in 2025 and is projected to reach USD 118.24 Billion by 2035.

Ans: The key drivers of the Rockets and Missiles Market include rising geopolitical tensions, increasing defense budgets, demand for precision strike systems, hypersonic advancements, and modernization of military capabilities globally drive market growth.

Ans: The Ballistic Missiles segment dominated during the projected period.

Ans: North America dominated the Rockets and Missiles Market in 2025.

Get in Touch