UAV Payload And Subsystems Market Report Scope & Overview:

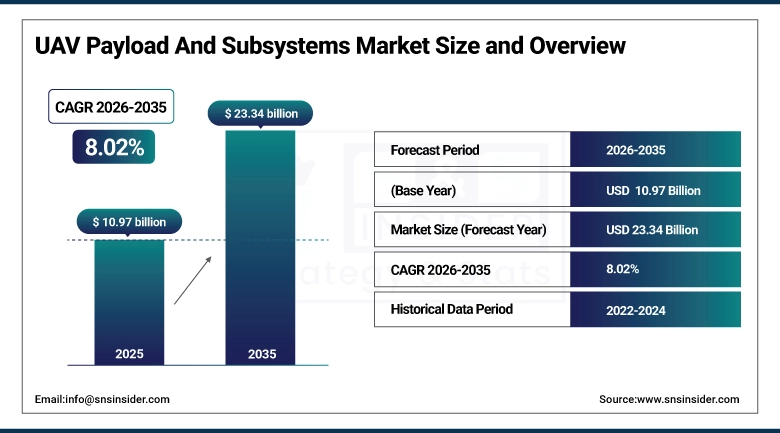

The UAV Payload and Subsystems Market size is valued at USD 10.97 Billion in 2025 and is projected to reach USD 23.34 Billion by 2035, growing at a CAGR of 8.02% during the forecast period 2026–2035.

The Insights on the UAV Payload and Subsystems Market are based on thorough research of current trends, technology advances, and increasing capabilities for UAV missions in both the defense and commercial environments. Strong drivers behind market growth include the increased use of AI-powered payload systems, increasing deployments of ISR UAVs, fast integration of sophisticated sensor technologies, including EO/IR, radar, LIDAR, and SIGINT, and the increasing demand for autonomous and BVLOS UAV flights. Moreover, increasing investments in defense upgrades, commercial drone deployments in agriculture, logistics, and infrastructure monitoring, as well as ongoing innovations in modular payloads and subsystems, are further driving market growth between 2026 and 2035.

UAV operations across thousands of active drone programs worldwide by 2025, and expanding rapidly with next-generation autonomous aerial systems by 2035.

Market Size and Forecast:

-

Market Size in 2025: USD 10.97 Billion

-

Market Size by 2035: USD 23.34 Billion

-

CAGR: 8.02% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on UAV Payload and Subsystems Market - Request Free Sample Report

UAV Payload And Subsystems Market Trends:

-

Rising adoption of AI-enabled UAV payloads and autonomous subsystems is driving enhanced mission intelligence, real-time data processing, and improved operational decision-making across defense and commercial UAV applications.

-

Increasing demand for ISR (Intelligence, Surveillance & Reconnaissance) missions is significantly boosting deployment of advanced EO/IR, radar, and SIGINT payload systems in military UAV fleets worldwide.

-

Rapid expansion of BVLOS (Beyond Visual Line of Sight) operations is accelerating integration of high-end communication systems, satellite links, and long-range data transmission subsystems.

-

Growing shift toward modular and plug-and-play payload architectures is enabling faster mission reconfiguration, improved UAV flexibility, and reduced operational downtime.

-

Increasing miniaturization of sensors and payload components is allowing lightweight UAV platforms to carry multi-mission payloads without compromising endurance or performance.

-

Rising investments in defense modernization programs and next-generation unmanned combat systems are fueling demand for advanced electronic warfare, radar, and intelligence payload technologies.

-

Expanding commercial UAV applications in agriculture, logistics, infrastructure inspection, and mapping are driving adoption of LiDAR, multispectral, and imaging payload systems.

-

Growing integration of edge computing, onboard AI, and real-time analytics in UAV subsystems is transforming raw data into actionable intelligence directly on the platform.

U.S. UAV Payload And Subsystems Market Insights:

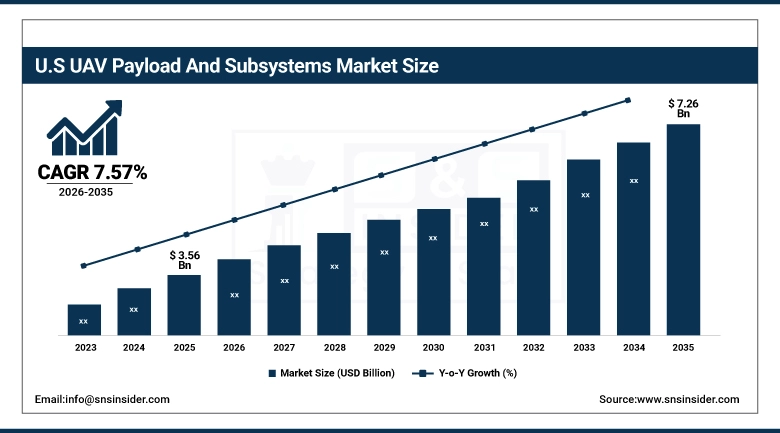

The UAV Payload and Subsystems Market is projected to grow from USD 3.56 Billion in 2025 to USD 7.26 Billion by 2035, at a CAGR of 7.57%. The positive growth drivers in this industry are the accelerated growth of defense and commercial UAV operations, greater use of sophisticated ISR payloads like EO/IR sensors, radars, LIDARs, and SIGINT technology, and the growing prevalence of AI-based autonomous data processing and edge computing in UAVs. The growing trend towards BVLOS missions, modular payload systems, and high-bandwidth communication subsystems is helping make UAV operations more efficient and versatile, both militarily and commercially, between 2026 and 2035.

UAV Payload And Subsystems Market Growth Drivers:

-

Rising deployment of multi-mission UAV platforms across defense, homeland security, and commercial sectors is driving strong demand for advanced payload and subsystem integration to enhance surveillance accuracy, situational awareness, and mission endurance.

Significant developments in UAV automation, AI-powered on-board computing, and compact sensors are fueling the rapid deployment of the latest payload technologies, including electro-optical/infrared (EO/IR), radar, LIDAR, and signal intelligence (SIGINT), to achieve immediate intelligence gathering and analysis at the edge level. With the ongoing modernization of military ISR systems, deployment of drone-based weapons systems, and increased investment in UCAVs, the need for advanced communication, navigation, and electronic warfare sub-systems is set to rise sharply.

More than 55% of advanced military UAV platforms globally are now integrated with AI-assisted payload management and modular subsystem architectures as of 2025.

UAV Payload And Subsystems Market Restraints:

-

High integration complexity and cost associated with advanced UAV payload systems and next-generation subsystems is restraining rapid large-scale deployment across commercial and budget-constrained defense UAV programs globally.

The UAV Payload and Subsystems Market is influenced by the persistent use of traditional one-sensor payload systems and legacy UAV avionics designs which are firmly entrenched within current drone inventories. The expensive R&D and integration requirements for more sophisticated EO/IR, radar, LiDAR, and SIGINT sensors, in addition to AI-driven onboard processing, secure communication channels, and modular subsystem design approaches, are acting as barriers to widespread adoption, especially amongst smaller UAV platforms and commercial users.

UAV Payload And Subsystems Market Opportunities:

-

Rapid evolution of network-centric warfare and intelligent battlefield systems is creating significant opportunities for advanced UAV payload and subsystem technologies globally.

UAV Payload and Sub-systems Market Growth is getting fuelled by the fast-moving trend towards multi-domain operations, in which UAVs are being increasingly used for synchronized ISR missions, electronic warfare, and immediate communication relay within the defense network. Increased focus on autonomous swarm UAV technology, advanced AI-based mission planning capabilities, and edge computing sensor fusion solutions is leading to better coordination and increased flexibility in missions. Defense organizations and businesses are increasingly leaning towards modular payload solutions for easy switching between different mission types involving imaging, targeting, communication, and sensing payloads.

Over 50% of next-generation UAV procurement programs globally are expected to prioritize modular, AI-integrated payload architectures and interoperable subsystem frameworks by 2035.

UAV Payload And Subsystems Market Segmentation Analysis:

• By Payload Type, EO/IR Payloads held the largest market share of 34.55% in 2025, while LiDAR Payloads are expected to grow at the fastest CAGR of 9.57% during 2026–2035.

• By Subsystems Type, Navigation & Guidance Systems held the largest share of 26.45% in 2025, while Data Processing & AI Systems are expected to grow at the fastest CAGR of 9.65% during 2026–2035.

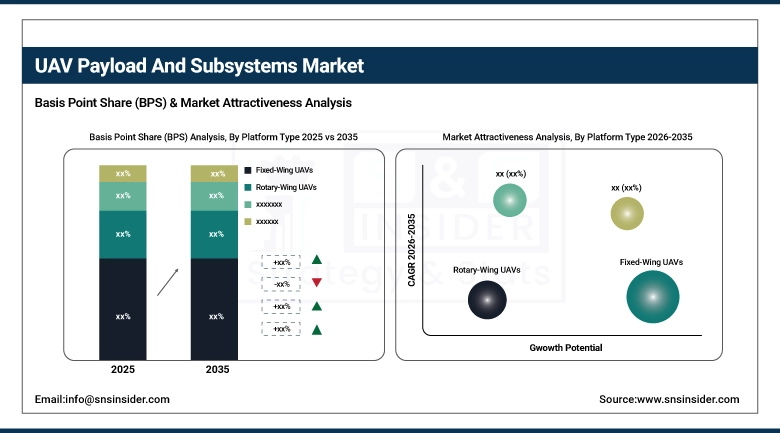

• By Platform Type, Fixed-Wing UAVs held the largest market share of 32.85% in 2025, while Hybrid VTOL UAVs are expected to grow at the fastest CAGR of 10.38% during 2026–2035.

• By Application, Defense & Military ISR dominated with 48.21% market share in 2025, while Logistics & Delivery Services is expected to grow at the fastest CAGR of 11.54% during 2026–2035.

• By End-User, Defense Forces held the largest share of 52.51% in 2025, while Commercial Enterprises are expected to grow at the fastest CAGR of 9.81% during 2026–2035.

By Payload Type, EO/IR Payloads Dominates While LiDAR Payloads Grows Rapidly:

EO/IR Payloads segment dominated in the UAV payload market because of the extensive application of the payload in the fields of defense surveillance, reconnaissance activities, and imaging. Its wide application range along with its upgrading in technologies such as thermal imaging and electro-optical sensors guarantees its position on top in the global UAV payloads market.

LiDAR Payloads is the fastest-growing segment, one owing to the increased demand for high-quality mapping, terrain modeling, and creation of 3D spatial maps using UAV payloads.

By Subsystems Type, Navigation & Guidance Systems Dominates While Data Processing & AI Systems Grows Rapidly:

Navigation & Guidance Systems segment dominated the market since this constitutes the main backbone of UAV stability, precision, and successful completion of tasks. The dominance of this segment results from the already existing UAV fleets where this segment is installed. Moreover, the importance of such systems in making sure that the UAVs navigate safely through their missions explains its dominance.

Data Processing & AI Systems is the fastest-growing segment one since this serves the growing need for real time analysis and autonomous mission success.

By Platform Type, Fixed-Wing UAVs Dominates While Hybrid VTOL UAVs Grows Rapidly:

Fixed-Wing UAVs segment dominated the market due to its high endurance flights, high operational range, and applicability in wide area surveillance and mapping applications in defense and commercial sectors. Efficiency in long term ISR missions coupled with the fact that the segment finds ample usage in military reconnaissance missions makes it one of the leading segments in the UAV platform market.

Hybrid VTOL UAVs is the fastest-growing segment in terms of market share due to the rising requirement for hybrid UAVs combining the virtues of VTOL and Fixed-wing capabilities in unmanned aircraft.

By Application, Defense & Military ISR Dominates While Logistics & Delivery Services Grows Rapidly:

Defense & Military ISR was the most dominating segment owing to the high utilization of UAV payload technologies and subsystems for intelligence, surveillance, and reconnaissance purposes. Modern military warfare has become dependent on the deployment of sophisticated EO/IR, radar, and SIGINT payload system. Therefore, the segment enjoys dominance in the UAV application domain.

Logistics & Delivery Services is the fastest-growing segment owing to fast-paced developments in drone delivery systems, e-commerce logistics, and last-mile logistics services. Investments in autonomous UAV-based deliveries along with favorable regulations for commercial drones will fuel growth in the segment.

By End-User, Defense Forces Dominates While Commercial Enterprises Grows Rapidly:

Defense Forces remained the dominating market segment due to huge investments in the procurement of cutting-edge UAV technology platforms, coupled with payloads and subsystems for use in reconnaissance, intelligence, and combat operations. The constant upgrading of military UAVs and geopolitical unrest contribute to the dominance of this segment in the market.

Commercial Enterprises remained the fastest growing segment on account of increasing usage of UAVs for various agricultural, infrastructure inspections, power generation, and logistic operations. An increase in the use of UAV technology in terms of analytics and automation has led to increased investment in UAV payloads and subsystems.

UAV Payload And Subsystems Market Regional Analysis:

North America UAV Payload and Subsystems Market Insights:

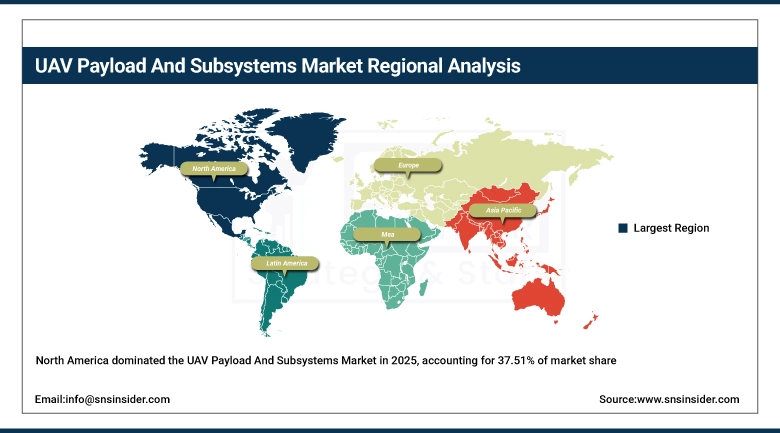

The North America UAV Payload and Subsystems Market is dominated, holding a 37.51% share in 2025 owing to its highly advanced and developed ecosystem of aerospace, defense and unmanned systems. The robust presence of UAV manufacturers, defense contractors and providers of sensors is facilitating the integration of advanced payload systems comprising EO/IR, radar and SIGINT technologies among others. Ongoing investments in AI-based autonomous UAV systems, network-centric warfare and intelligence solutions are reinforcing the market dominance. The increased adoption of UAVs for purposes of border surveillance, defense reconnaissance missions, infrastructure monitoring as well as commercial uses like logistics management and inspections will drive demand over the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States UAV Payload and Subsystems Market Insights:

The United States UAV Payload and Subsystems Market occupies the dominant position in the regional landscape owing to its advanced and state-of-the-art UAV fleet modernization programs, well-established research and development ecosystem and adoption of advanced payloads and subsystems. The country is making significant investments in artificial intelligence-based autonomous UAV systems, EW payloads and advanced multi-sensor intelligent UAVs. High involvement of defense bodies, aerospace OEMs and technology firms in this industry is fostering innovation.

Asia-Pacific UAV Payload and Subsystems Market Insights:

The Asia-Pacific UAV Payload and Subsystems Market is the fastest-growing region, projected to expand at a CAGR of 9.81% during 2026–2035. The factors contributing to the growth in the region include the fast-paced development of UAV systems for defense, the rising importance placed on surveillance systems by geographies, and the increased adoption of commercial drones. The countries in the region including China, India, Japan, and South Korea are making substantial efforts towards building UAVs, advanced sensors, and autonomous flight technologies enabled by artificial intelligence. Growing use cases for border security, disaster relief, precision farming, and logistical applications are helping drive demand for enhanced payload and subsystem technologies. Increased investment in smart defense solutions, combined with the growing uptake of multi-role UAV platforms, is rapidly changing the UAV landscape in the region.

China UAV Payload and Subsystems Market Insights:

The Chinese UAV Payload and Subsystems Market is fueled by massive investments in unmanned aerial vehicles, the rapid expansion of the domestic UAV industry, and the ongoing modernization of the defense sector. The country is focusing heavily on the development of ISR payload systems, artificial intelligence-based surveillance UAVs, and superior radar and imaging systems for both defense and civilian purposes. The significant involvement of the Chinese government in the development of indigenous UAV technology, alongside its widespread application in border security, maritime surveillance, and infrastructure surveillance, is propelling the market ahead.

Europe UAV Payload and Subsystems Market Insights:

The Europe UAV Payload and Subsystems Market is boosted by its superior aerospace engineering industry, cutting-edge defense electronics manufacturing industry, and increased investments in autonomous unmanned aircraft. The countries like France, Germany, United Kingdom, and Italy have invested in the development of futuristic UAV platforms incorporating advanced EO/IR sensors, radar, and AI-driven payloads for military and surveillance applications. The countries have witnessed growing usage of unmanned aircraft platforms in environmental monitoring, industrial inspection, and management of critical infrastructure networks. Stringent regulations and increased demand for secure and interoperable UAV communication systems will drive the market towards advanced subsystems in the coming years.

Germany UAV Payload and Subsystems Market Insights:

The Germany UAV Payload and Subsystems Market is fuelled by the highly advanced aerospace engineering industry, advanced precision manufacturing industry, and its active participation in European defense UAV program. Germany is increasingly investing in the development of autonomous UAV platforms which incorporate imaging payloads, communication subsystems, and navigation systems for defense and industrial use. Growing investment in AI-driven mission systems and sensor fusion technology will support the country's capabilities in payload integration.

Latin America UAV Payload and Subsystems Market Insights:

The Latin America UAV Payload and Subsystems Market is experiencing steady growth on account of increased deployment of UAVs in agriculture, mining, environmental monitoring, and public safety operations. Latin American countries such as Brazil, Mexico, and Argentina are increasingly adopting UAVs with imaging/mapping payloads to increase the effectiveness of operations involving extensive agricultural and infrastructure projects. Defense modernization efforts are contributing to increased adoption of UAV payload systems designed for surveillance and reconnaissance purposes. Increasing collaboration with global UAV providers and growing awareness about drones data analytics are boosting market development within the region.

Middle East & Africa UAV Payload and Subsystems Market Insights:

The Middle East & Africa UAV Payload and Subsystems Market is exhibiting nascent growth on account of increased defense spending, border surveillance needs, and UAV-based intelligence gathering capabilities. Countries such as UAE, Saudi Arabia, Israel, and South Africa are deploying cutting-edge UAVs that are equipped with EO/IR, radar, and communication payload systems used for security and monitoring purposes, including oil & gas infrastructure and strategic surveillance. Increased efforts related to indigenization of UAV development and collaborations with foreign UAV technology providers are driving UAV payload adoption in the region.

UAV Payload And Subsystems Market Competitive Landscape:

Lockheed Martin Corporation

The Lockheed Martin Corporation stands out among other defense aerospace organizations as one of the leading players in UAV technology, autonomous mission platforms, and ISR payloads. The organization concentrates its efforts on producing state-of-the-art UAVs for applications in intelligence gathering, surveillance, and reconnaissance missions, along with developing new autonomous battle systems equipped with artificial intelligence swarm technology. The competitive edge of this company consists of extensive integration of its products into major defense programs and advanced research into autonomous systems.

-

In February 2025, Lockheed Martin enhanced its unmanned systems portfolio by advancing AI-driven autonomous mission technologies and improving integration of multi-sensor ISR payload systems across defense UAV platforms, supporting real-time battlefield intelligence and mission autonomy.

Northrop Grumman Corporation

The Northrop Grumman Corporation is an American defense company and one of the pioneers in high-altitude UAV platforms, autonomous aircraft technology, and advanced mission payload design and integration. The company has a stronghold in strategic surveillance drones, stealth technology drones, and long endurance ISR UAVs with advanced radars, imaging technologies, and electronic warfare mission payload capability. Northrop Grumman excels in autonomous next-gen drone design, classified defense UAV technology, and AI-based mission payload integration.

-

In December 2025, Northrop Grumman advanced its unmanned aerial systems portfolio through continued development of next-generation autonomous UAV platforms under U.S. defense programs, enhancing multi-sensor payload integration and expanding capabilities for long-endurance surveillance and collaborative combat UAV systems.

RTX Corporation (Raytheon Technologies)

RTX Corporation is an industry leader in aerospace and defense systems, including state-of-the-art avionics, missiles, and electronic warfare capabilities that contribute directly to the design of UAV payloads and subsystems. RTX is heavily involved in the development of sensor fusion, secure communication solutions, and navigation solutions employed on UAVs in defense applications. The competitive advantage of RTX is its robust integration capability in missile defense, aerospace electronics, and autonomous technologies.

-

In March 2025, RTX strengthened its aerospace and defense electronics portfolio by enhancing integrated sensor and communication subsystem technologies used in advanced unmanned aerial systems, improving real-time data transmission and mission-level situational awareness.

UAV Payload And Subsystems Market Key Players:

Some of the UAV Payload And Subsystems Market Companies are:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

RTX (Raytheon Technologies)

-

L3Harris Technologies

-

Boeing

-

General Atomics Aeronautical Systems (GA-ASI)

-

Elbit Systems

-

Israel Aerospace Industries (IAI)

-

Teledyne FLIR

-

Thales Group

-

Leonardo S.p.A.

-

BAE Systems

-

AeroVironment

-

Textron Systems

-

Saab AB

-

Kratos Defense & Security Solutions

-

Anduril Industries

-

Shield AI

-

Insitu (Boeing subsidiary)

-

DJI

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.97 Billion |

| Market Size by 2035 | USD 23.34 Billion |

| CAGR | CAGR of 8.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Payload Type (EO/IR (Electro-Optical / Infrared) Payloads, Radar Payloads (SAR / Mini-AESA), SIGINT / COMINT Payloads, LiDAR Payloads, Multi / Hyperspectral Imaging Payloads) • By Subsystems Type (Navigation & Guidance Systems (GPS / INS), Communication Systems (Data Links / SATCOM), Flight Control Systems (Autopilot / FCS), Power & Energy Systems (Batteries / Fuel Cells), Data Processing & AI Systems) • By Platform Type (Fixed-Wing UAVs, Rotary-Wing UAVs, Hybrid VTOL UAVs, Nano / Micro UAVs, Tactical / MALE UAVs) • By Application (Defense & Military ISR, Homeland Security & Surveillance, Agriculture & Precision Farming, Industrial Inspection (Oil & Gas, Energy, Utilities), Logistics & Delivery Services, Others) • By End-User (Defense Forces, Government & Homeland Security Agencies, Commercial Enterprises, UAV OEMs / Integrators, Research & Academic Institutions) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, RTX (Raytheon Technologies), L3Harris Technologies, Boeing, General Atomics Aeronautical Systems (GA-ASI), Elbit Systems, Israel Aerospace Industries (IAI), Teledyne FLIR, Thales Group, Leonardo S.p.A., BAE Systems, AeroVironment, Textron Systems, Saab AB, Kratos Defense & Security Solutions, Anduril Industries, Shield AI, Insitu (Boeing subsidiary), DJI |

Frequently Asked Questions

Ans: North America dominated with a 37.51% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 8.96% during 2026–2035.

Defense & Military ISR dominated with a 48.21% share in 2025, while Logistics & Delivery Services are projected to grow at the fastest CAGR of 11.54% during 2026–2035.

Growth is driven by rising adoption of AI-enabled autonomous UAV systems, increasing demand for advanced ISR payloads, and expanding use of UAVs across defense, surveillance, logistics, and industrial inspection applications.

The market is valued at USD 10.97 Billion in 2025 and is projected to reach USD 23.34 Billion by 2035.

The UAV Payload And Subsystems Markets projected to grow at a CAGR of 8.02% during 2026–2035.

Get in Touch