Thrust Vector Control Market Report Scope & Overview:

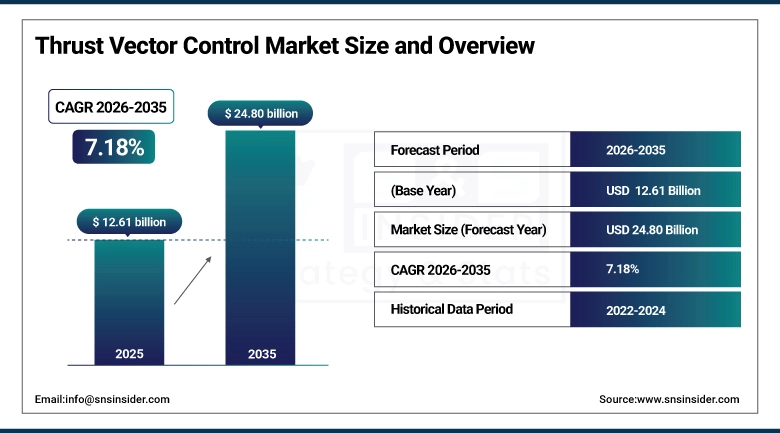

The Thrust Vector Control Market size is valued at USD 12.61 Billion in 2025 and is projected to reach USD 24.80 Billion by 2035, growing at a CAGR of 7.18% during the forecast period 2026–2035.

Insights on the Thrust Vector Control Market provide a comprehensive analysis of propulsion control technologies, aerospace innovation trends, and defense modernization programs. Increasing demand for precision-guided missile systems, hypersonic weapon development, reusable space launch vehicles, and next-generation UAV platforms, along with rapid advancements in fluidic thrust vectoring, AI-integrated flight control systems, and smart actuation technologies, are some of the major factors driving consistent market growth from 2026 to 2035.

The deployment of TVC systems is becoming mission-critical in ensuring high-accuracy trajectory correction, enhanced vehicle stability, and successful execution of complex defense and space maneuvers under extreme flight conditions.

Market Size and Forecast:

-

Market Size in 2025: USD 12.61 Billion

-

Market Size by 2035: USD 24.80 Billion

-

CAGR: 7.18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Thrust Vector Control Market - Request Free Sample Report

Thrust Vector Control Market Trends:

-

Rising deployment of precision-guided missile systems, hypersonic weapons, and next-generation space launch vehicles is significantly driving demand for advanced thrust vector control technologies to ensure superior maneuverability and trajectory accuracy.

-

Rapid expansion of global defense modernization programs and space exploration initiatives, including reusable launch vehicles and satellite mega-constellations, is accelerating integration of high-performance thrust vector control systems across platforms.

-

Increasing adoption of fluidic thrust vectoring, secondary injection systems (SITVC), and next-generation electromechanical actuators is gaining traction due to improved efficiency, reduced mechanical complexity, and higher reliability under extreme operating conditions.

-

Growing integration of AI-enabled flight control systems, real-time telemetry, and smart sensor-based feedback mechanisms is transforming thrust vector control into an intelligent propulsion management subsystem.

-

Rising investments in hypersonic defense systems and advanced missile guidance technologies are boosting demand for ultra-responsive thrust vector control solutions capable of high-speed stability correction.

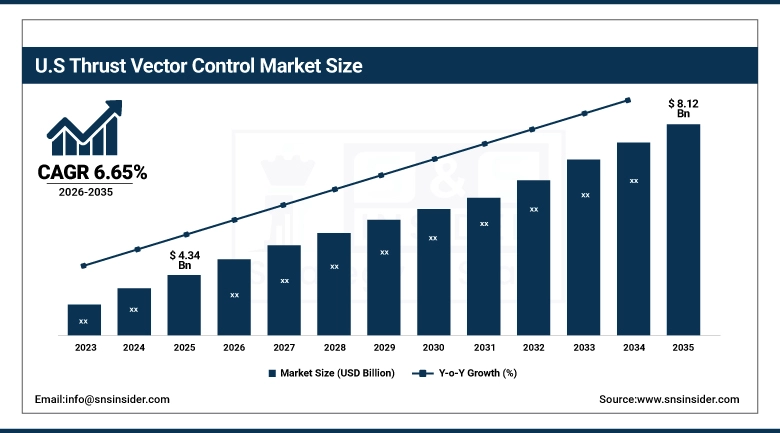

U.S. Thrust Vector Control Market Insights:

The U.S. Transcutaneous Oximetry Systems Market is projected to grow from USD 4.34 billion in 2025 to USD 8.12 Billion by 2035, at a CAGR of 6.65%. Favorable growth factors for the industry comprise the emergence of hypersonic weapons, missile defenses, and space launch vehicles with advanced capabilities; growing deployment of flight control systems that incorporate artificial intelligence, fluidic thrust vectoring technology, and state-of-the-art electromechanical actuators; and considerable expenditure on part of the U.S. Department of Defense, NASA space exploration endeavors, and commercial launches.

Thrust Vector Control Market Growth Drivers:

-

Rising deployment of hypersonic missile systems, next-generation ballistic and cruise missiles, and reusable space launch vehicles is driving strong demand for high-precision thrust vector control systems to ensure superior trajectory accuracy, stability, and maneuverability under extreme flight conditions.

Rapid advancements in the global modernization of defense systems and space exploration endeavors, especially in countries like the United States, China, and India, have led to a faster adoption of thrust vector control technology in missiles, rocket boosters, and spacecraft. Investments in the development of artificial intelligence flight controls, fluidic thrust vector controls, and intelligent electromechanical actuators have made systems more responsive and self-correcting.

Additionally, over 60% of next-generation missile and space launch programs globally are integrating advanced thrust vector control subsystems as of 2025, reflecting its growing role as a mission-critical propulsion technology.

Thrust Vector Control Market Restraints:

-

High dependence on legacy propulsion and control architectures in existing missile systems, launch vehicles, and aerospace platforms is restraining the rapid adoption of next-generation thrust vector control technologies globally.

Thrust Vector Control Market will be impacted by the use of mechanical gimbaling systems and traditional actuator mechanisms that are extensively entrenched within enduring defense and aerospace applications. The high expenses involved in developing and integrating sophisticated fluid-based thrust vectoring, artificial intelligence (AI) control systems, and high-precision electromechanical actuators make their widespread adoption difficult, especially in the cost-conscious defense acquisition sector.

Thrust Vector Control Market Opportunities:

-

Rapid advancement in next-generation defense systems and deep-space exploration programs is creating significant opportunities for advanced thrust vector control technologies globally.

The changing dynamics within the aerospace and defense ecosystem are facilitating robust adoption rates for advanced thrust vector control systems, artificial intelligence-enabled propulsion control, and precise actuator systems for hypersonic, reusable launch, and autonomous space applications. Aerospace organizations and private space enterprises are showing increasing interest in multi-dimensional maneuver systems and intelligent flight stability systems.

Also, more than 50% of hypersonic weapons and reusable launch vehicles being planned and launched after 2035 will incorporate intelligent thrust vector control systems.

Thrust Vector Control Market Segmentation Analysis:

-

By Technology Type, Gimbaled Nozzle Systems held the largest market share of 42.55% in 2025, while Fluid Injection Thrust Vectoring is expected to grow at the fastest CAGR of 9.06% during 2026–2035.

-

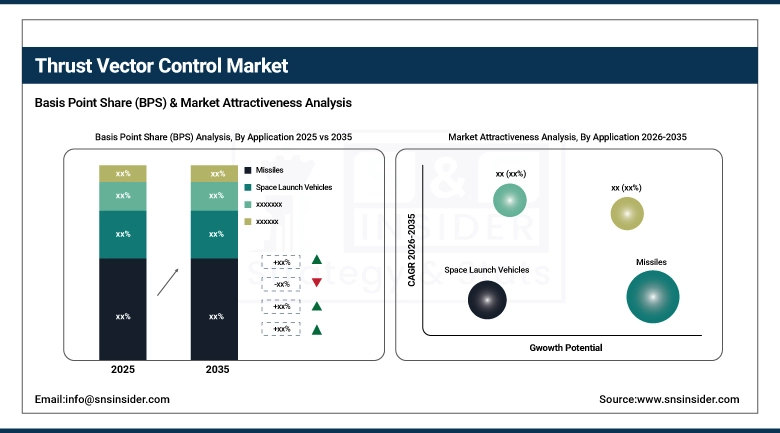

By Application, Missiles dominated with 46.45% market share in 2025, while Spacecraft & Satellites is projected to grow at the fastest CAGR of 9.17% during 2026–2035.

-

By Platform Type, Land-Based Systems held the largest share of 38.85% in 2025, while Space-Based Platforms is expected to grow at the fastest CAGR of 10.24% during 2026–2035.

-

By Component, Actuators held the largest market share of 28.21% in 2025, while Fluid Injection Systems is expected to grow at the fastest CAGR of 10.05% during 2026–2035.

By Application, Missiles Dominates While Spacecraft & Satellites Grows Rapidly:

Missiles segment dominated the market in the global market as a result of the important application in defense mechanisms, which require highly accurate manipulation and precision under extremely difficult flight conditions. The consistent development in the global industry of ballistic missiles, cruise missiles, and hypersonic missiles further emphasizes its robust presence in the thrust vector control market.

Spacecraft & Satellites is the fastest-growing segment, driven by rising initiatives of satellite deployment projects, deep space mission, and increasing need for orbital maneuvering systems.

By Technology Type, Gimbaled Nozzle Systems Dominates While Fluid Injection Thrust Vectoring Grows Rapidly:

Gimbaled Nozzle Systems segment dominated the market due to its wide use in missile propulsion and spacecraft launches, offering dependable thrust vector control for intricate flight paths. Its widespread usage in existing military and aerospace projects guarantees its dominance in the global thrust vector control industry.

Fluid Injection Thrust Vectoring is the fastest-growing segment, as there was rising demand for more efficient propulsion, lesser mechanical intricacies, and enhanced responsiveness in future missiles and spacecraft. Increased interest in hypersonic and reusable launch vehicles has fueled the growth of this segment.

By Platform Type, Land-Based Systems Dominates While Space-Based Platforms Grows Rapidly:

The Land-Based Systems segment holds the dominant position in the market share owing to extensive use in missile launch facilities and ground-based defense systems that depend on reliable and high-precision thrust vector control technology. Existing modernization drives among militaries around the world ensure the dominance of the segment.

On the other hand, the Space-Based Platforms segment is expected to be the fastest-growing segment. Factors behind its rapid growth include more satellites in orbit, reusable rocket programs, and exploration projects in space. The need for precise maneuvering in outer space drives the market segment forward.

By Component, Actuators Dominates While Fluid Injection Systems Grows Rapidly:

Actuators segment dominated the market in the market due to its importance in facilitating mechanical motion and directing the thrust. The reliability of the actuators segment in terms of use in legacy defense platforms and ensuring the flight stability makes them dominant in the thrust vector control market.

Fluid Injection Systems is the fastest-growing segment, in the market. The growing need for efficient propulsion, minimal mechanical components, and improved response control in future missiles and spacecraft are contributing to the growth of this segment.

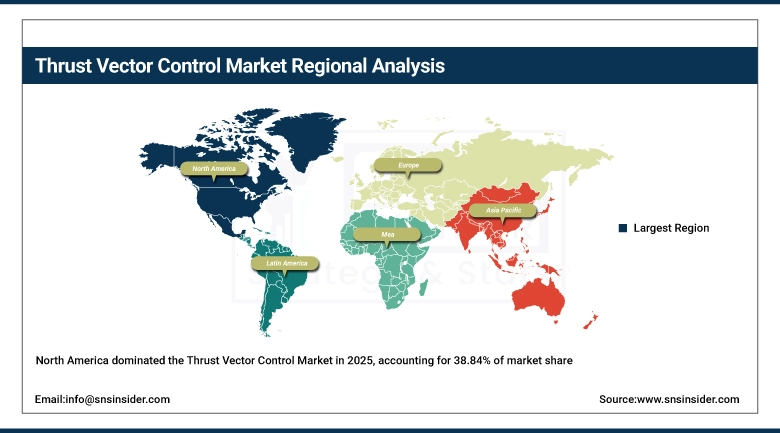

Thrust Vector Control Market Regional Analysis:

North America Thrust Vector Control Market Insights:

The North America Thrust Vector Control Market is dominated, holding a 38.84% share in 2025 because of the region’s sophisticated aerospace and defense manufacturing environment, and expertise in missile and space launch solutions. The presence of a high number of ballistic missiles featuring thrust vector control, ongoing hypersonic weapon developments, and reusable launch vehicle projects is expected to increase the market opportunities in the region. Ongoing modernization and developments in defense solutions, coupled with the presence of key aerospace original equipment manufacturers and propulsion technologies providers, have been supporting the demand in the region’s thrust vector control market.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Thrust Vector Control Market Insights:

The United States Thrust Vector Control Market features advanced defense systems, ongoing missile modernization programs, and participation in government and commercial space exploration projects. The country continues to be at the forefront of propulsion advancements, with a high adoption of thrust vector control systems in hypersonic weapons, strategic missiles, and future generation launch vehicles. Strong funding from defense and space agencies, and development of AI-driven flight control systems, is driving the advancements in thrust vector control systems.

Asia-Pacific Thrust Vector Control Market Insights:

The Asia-Pacific Thrust Vector Control Market is the fastest-growing region, projected to expand at a CAGR of 8.27% during 2026–2035. This trend is boosted by the rapid growth of defense modernization programs, space exploration programs, and indigenous development of missiles within China, India, Japan, and South Korea. Increasing use of advanced missile systems, space programs, and aerospace projects is generating high demand for thrust vector control systems in the region. There is an increased interest in developing hypersonic weapons, reusable space launch systems, and defense manufacturing, which is rapidly boosting adoption. Increased investments in R&D and focus on achieving space superiority and precision strike capability is changing the face of the regional thrust vector control market.

China Thrust Vector Control Market Insights:

China’s Thrust Vector Control Market is fueled by major investments in defense upgrades, rapid missile technology evolution, and increased space exploration. China is making significant efforts toward developing hypersonic weapons, intercontinental missiles, and space launch vehicles, all of which need thrust vector control mechanisms. The Chinese government has shown immense commitment to developing indigenous aerospace technologies, along with growing space missions and satellite launches.

Europe Thrust Vector Control Market Insights:

The Europe Thrust Vector Control market is bolstered by well-established aerospace engineering expertise, robust defense manufacturing capabilities, and growing emphasis on future propulsion technologies. Nations like France, Germany, Italy, and the United Kingdom are focusing on programs for missile improvement, reusable space launch vehicles, and satellites. The emphasis on technological sovereignty and defense capacity building in the region is leading to the growth of demand for precise thrust vector control. Moreover, growing involvement in international space exploration efforts and research into fluidic and adaptive propulsion systems is making Europe prominent in the thrust vector control arena.

Germany Thrust Vector Control Market Insights:

The Germany Thrust Vector Control Market is fueled by the country’s highly-developed aerospace engineering industry, cutting-edge precision manufacturing capability, and participation in international defense and space programs. Germany’s active involvement in the development of next-generation missile systems and propulsion systems is creating opportunities for the development of advanced thrust vector control mechanisms. Growing emphasis on engineering innovation, high-performance material usage, and system efficiency is helping the thrust vector control system development process.

Latin America Thrust Vector Control Market Insights:

The Latin America Thrust Vector Control Market is undergoing steady development due to an increase in interest in aerospace technologies, defense upgrades, and new involvement in space programs. With nations like Brazil and Argentina making advancements in rocket developments, space research, and defense upgrading, there is a steady rise in early-stage adoption of thrust vector control technologies. There are increasing collaborations between the nations in space agencies and limited yet growing aerospace infrastructures helping in transferring technology.

Middle East & Africa Thrust Vector Control Market Insights:

The Middle East & Africa Thrust Vector Control Market is witnessing emerging growth owing to increased investments in defense systems, interest in space exploration projects, and the development of sophisticated aerospace technologies. Countries such as UAE and Saudi Arabia are working towards developing themselves as space powerhouses through satellite launches and interplanetary missions. In addition to this, investments in advanced military technologies are helping in market growth.

Thrust Vector Control Market Competitive Landscape:

Honeywell International Inc. is a global leader in aerospace and defense technologies with strong capabilities in flight control systems, propulsion actuation, and advanced thrust vector control subsystems. The company plays a critical role in integrating precision control electronics, sensors, and electromechanical actuators used in missile guidance systems, space launch vehicles, and advanced aircraft platforms. Its competitive strength lies in its deep aerospace engineering expertise, large-scale defense contracts, and continuous investment in next-generation autonomous flight and propulsion control technologies.

-

In August 2025, Honeywell expanded its aerospace control systems portfolio by enhancing its next-generation electromechanical actuator platforms designed for advanced missile and space launch applications, strengthening its position in high-precision thrust control systems.

Moog Inc. is a leading global provider of precision motion control systems and is widely recognized as one of the most critical suppliers of thrust vector control actuators and flight control systems for defense and space applications. The company specializes in high-performance electrohydraulic and electromechanical actuation technologies used in missile systems, launch vehicles, and spacecraft maneuvering systems. Moog’s competitive advantage lies in its deep specialization in motion control engineering, long-standing defense partnerships, and strong presence in both reusable space launch and hypersonic weapon programs.

-

In September 2025, Moog Inc. advanced its space and defense actuation portfolio through upgraded flight control and thrust vector actuation systems deployed in next-generation launch vehicle programs and hypersonic defense platforms.

RTX Corporation (Raytheon Technologies) is a leading aerospace and defense organization engaged in numerous research and development efforts in the areas of missile propulsion systems, missile guidance technologies, and thrust vector control solutions. This company supplies essential propulsion control systems for tactical missiles, ballistic missile defense solutions, and next-generation hypersonic systems through its divisions in aerospace and defense, space. RTX Corporation is highly competitive due to an extensive number of defense programs, advanced R&D capabilities, and a high degree of integration in missile guidance, propulsion, and avionics systems.

-

In July 2025, RTX strengthened its missile systems portfolio by advancing integrated propulsion control and thrust vectoring technologies for next-generation hypersonic defense programs, improving maneuverability and target precision in high-speed engagement systems.

Thrust Vector Control Market Key Players:

Some of the Thrust Vector Control Market Companies are:

-

Honeywell International Inc.

-

Moog Inc.

-

RTX Corporation (Raytheon Technologies)

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

Woodward Inc.

-

BAE Systems plc

-

Safran S.A.

-

Aerojet Rocketdyne (L3Harris Technologies)

-

Parker Hannifin Corporation

-

MBDA

-

IHI Corporation

-

Nammo AS

-

Leonardo S.p.A.

-

Thales Group

-

Israel Aerospace Industries (IAI)

-

Saab AB

-

Rolls-Royce plc

-

SpaceX

-

Blue Origin

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.61 Billion |

| Market Size by 2035 | USD 24.80 Billion |

| CAGR | CAGR of 7.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology Type (Gimbaled Nozzle Systems, Jet Vanes, Fluid Injection Thrust Vectoring, Secondary Injection Thrust Vector Control (SITVC), Others) • By Application (Missiles, Space Launch Vehicles, Spacecraft & Satellites, Fighter Aircraft & UAVs, Others) • By Platform Type (Land-Based Systems,Airborne Platforms, Naval Platforms, Space-Based Platforms, Others) • By Component (Actuators, Nozzles, Control Systems, Sensors, Fluid Injection Systems, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Moog Inc., RTX Corporation (Raytheon Technologies), Northrop Grumman Corporation, Lockheed Martin Corporation, Woodward Inc., BAE Systems plc, Safran S.A., Aerojet Rocketdyne (L3Harris Technologies), Parker Hannifin Corporation, MBDA, IHI Corporation, Nammo AS, Leonardo S.p.A., Thales Group, Israel Aerospace Industries (IAI), Saab AB, Rolls-Royce plc, SpaceX, Blue Origin |

Frequently Asked Questions

North America dominated with a 38.84% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 8.27% during 2026–2035.

Land-Based Systems dominated with a 38.85% share in 2025, while Space-Based Platforms are projected to grow at the fastest CAGR of 10.24% during 2026–2035.

Growth is driven by rising demand for hypersonic missiles, advanced space launch vehicles, and precision-guided defense systems, along with increasing integration of AI-enabled flight control and advanced propulsion technologies.

The market is valued at USD 12.61 Billion in 2025 and is projected to reach USD 24.80 Billion by 2035.

The Thrust Vector Control Markets projected to grow at a CAGR of 7.18% during 2026–2035.

Get in Touch