Satellite Internet Market Report Scope & Overview:

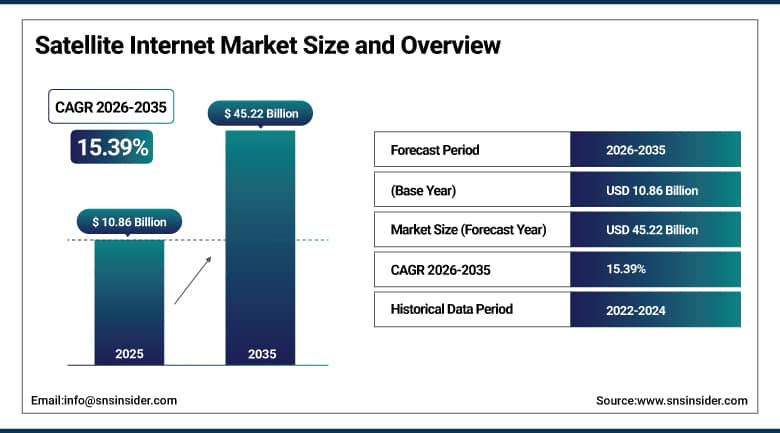

Satellite Internet Market was valued at USD 10.86 billion in 2025 and is expected to reach USD 45.22 billion by 2035, growing at a CAGR of 15.39% from 2026-2035.

The growth of Satellite Internet Market can be attributed to the rising need for high-speed internet connections in remote and underserved areas that have restricted terrestrial connectivity. The increasing uptake of satellite communications within the domains of defense, aviation, maritime, and enterprises is propelling the demand for reliable and global internet connections. The fast deployment of Low Earth Orbit satellites is resulting in faster internet connections and improved latency rates. Increased investments by major IT and aerospace firms are boosting global market growth in the industry.

SpaceX's Starlink reports that active Starlink subscribers exceeded 3 million globally in the most recently disclosed period across 100+ countries representing the fastest-growing broadband subscription service in history by subscriber acquisition rate at equivalent subscriber base.

Amazon Web Services documents that Project Kuiper's first production satellites are completing end-to-end system validation, with commercial service targeted to begin serving enterprise and government customers, creating the competitive dynamic that will sustain innovation and pricing pressure in the satellite internet market through the forecast period.

Satellite Internet Market Size and Forecast

-

Market Size in 2025: USD 10.86 Billion

-

Market Size by 2035: USD 45.22 Billion

-

CAGR: 15.39% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Satellite Internet Market - Request Free Sample Report

Satellite Internet Market Trends

-

Rising demand for high-speed connectivity in remote and underserved regions is driving the satellite internet market.

-

Growing adoption across maritime, aviation, defense, and rural broadband applications is boosting market growth.

-

Expansion of low Earth orbit (LEO) satellite constellations is fueling global coverage and lower latency services.

-

Increasing focus on bridging the digital divide and improving global internet accessibility is shaping adoption trends.

-

Advancements in satellite miniaturization, phased-array antennas, and ground station technologies are enhancing performance.

-

Rising investments from private space companies and government initiatives are supporting market expansion.

-

Collaborations between satellite operators, telecom providers, and technology firms are accelerating innovation and global adoption.

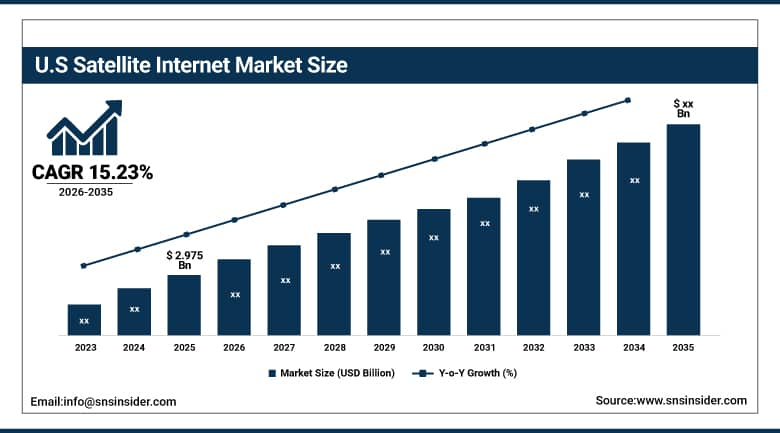

U.S. Satellite Internet Market was valued at USD 2.975 billion in 2025 and is expected to grow at a CAGR of 15.23% from 2026-2035.

The U.S. Satellite Internet Market is experiencing significant growth owing to increasing demand for fast internet in remote locations with inadequate broadband connectivity through terrestrial networks. The increased use of satellite technology in the defense, aviation, maritime, and enterprise segments has facilitated its expansion as well. Fast development of low-earth orbit satellite systems has been contributing to better coverage, lower latency, and enhanced service performance. Significant investment by technology giants and favorable government policies related to universal broadband connectivity have also been facilitating steady market growth.

FCC Chairman testimony to Congress documents that approximately 21 million Americans lack access to broadband connectivity meeting the agency's 25/3 Mbps minimum standard representing the addressable market for satellite internet in the domestic market whose BEAD program allocation of USD 42.45 billion is expected to fund connectivity solutions including satellite internet deployment in the most remote qualifying locations.

The National Telecommunications and Information Administration's Digital Equity Program is additionally allocating USD 2.75 billion for technology adoption that complements infrastructure investment in creating functional broadband access across underserved American communities.

Satellite Internet Market Segment Analysis

-

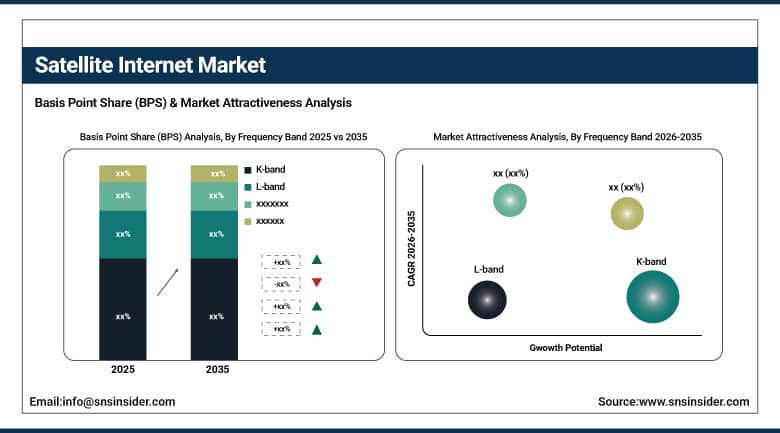

By Frequency Band, K-band segment dominated the Satellite Internet Market in 2025 with ~41% share; L-band segment is fastest growing (CAGR).

-

By Industry, Government & Public Sector segment dominated the Satellite Internet Market in 2025 with ~34% share; Transport & Cargo segment is fastest growing (CAGR).

By Frequency Band, K-band segment dominates the Satellite Internet Market, L-band segment expected to grow fastest.

K-band dominates the Satellite Internet Market due to its capabilities in enabling faster data transfer and broadband speed in satellite communications. It is extensively used in communications involving high-speed satellite systems for handling vast data and can be found in satellite communications for internet access, broadcast, and enterprise communication. The band’s efficiency in facilitating high-throughput in satellite systems and its suitability for use in fixed satellite systems make it a popular choice. Expansion of broadband satellite constellations is expected to drive its application.

L-band is the fastest growing frequency band because of its reliable signal strength, reduced sensitivity to weather interference, and good performance in remote and mobile scenarios. Its increased use in aviation, maritime, and emergency communications where reliability is of paramount importance is boosting its popularity. The band’s capability of operating with portable and mobile terminals is expected to fuel demand for L-band communications within transportation and defense sectors.

By Industry, Government & Public Sector segment dominates the Satellite Internet Market, Transport & Cargo segment expected to grow fastest.

The government and public sector have a prominent share in the Satellite Internet Market owing to its significant application in defense communications, disaster management, surveillance, and public service communications. Satellite internet provides secure, reliable, and extensive communications, particularly in difficult geographical areas. The need for extensive investment in the country's communication infrastructure and strategic defense network also contributes to this segment's leading status.

The transport and cargo market segment is witnessing rapid growth driven by the rising requirement for continuous tracking and monitoring of cargo fleets and logistics networks. Satellite internet offers reliable communication services to the maritime cargo ships, air freighters, and overland transportation vehicles operating in remote locations. Increasing globalization, the widespread adoption of smart logistics management solutions, and the growing volume of global business transactions continue to boost the demand for satellite internet services in this industry.

Satellite Internet Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

India |

35% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

48% |

North America Satellite Internet Market Insights

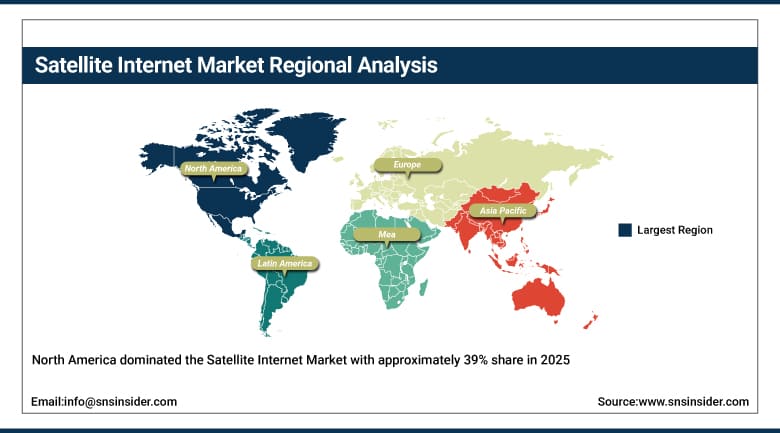

North America dominated the Satellite Internet Market with approximately 39% share in 2025 because of its dominance in having key satellite Internet providers, technological developments, and use of LEO broadband internet services. The high demand for consistent connectivity among rural areas will continue to bolster the market's growth rate in coming years. Widespread applications in fields like defense, aerospace, marine, and enterprise sectors are also contributing to its success. The region is also making significant investments in satellite networks and government efforts for broadband initiatives.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Satellite Internet Market Insights

The Asia Pacific is the fastest growing regional Satellite Internet Market because of the fast pace of digitalization, the increasing requirement for high-speed internet in rural and remote locations, and the strong efforts of governments to ensure digital inclusiveness. The increased usage of Satellite Internet in maritime applications, airlines, defense systems, and enterprises is also contributing significantly to its adoption. There have been huge investments made into LEO satellite constellations, as well as partnerships with global providers of satellite internet, ensuring better network coverage and faster speed and lower latency.

Europe Satellite Internet Market Insights

The Europe Satellite Internet Market is experiencing significant growth owing to the rising demand for internet access in far-flung areas, alongside substantial penetration into the aviation, maritime, and enterprise markets. The development of digital transformation programs and the implementation of broadband expansion schemes by the government are also boosting the market growth. The increasing deployment of LEO satellite constellations is enhancing the speed and latency capabilities of satellite internet services in the region. In addition, there is also considerable emphasis on communication security for military and commercial uses.

MEA and Latin America Satellite Internet Market Insights

MEA and Latin America Satellite Internet Market is registering steady growth due to lack of adequate broadband network on ground, higher demand for rural internet services, and increased usage in difficult terrains. There are initiatives being taken by governments towards digitalization to ensure availability of internet services in underdeveloped areas. Higher usage in shipping, oil and gas, mining, and military applications is contributing to higher demands. But the high cost involved and issues of affordability still pose a hindrance. LEO satellite constellation deployment is aiding the growth in the market.

Satellite Internet Market Growth Drivers:

-

Expanding Demand for High-Speed Connectivity in Remote and Underserved Regions Driven by Digital Inclusion and Global Internet Coverage Initiatives

The increased need for digital connectivity services in remote areas and other areas that lack such connectivity has caused the demand for satellite internet services to become extremely high on a global scale. The absence of terrestrial internet infrastructure in hard-to-reach geographies, including mountainous regions, deserts, and even oceans, is causing satellite internet to become increasingly essential for providing connectivity services. There are many government and corporate agencies investing heavily to reduce the digital divide and provide connectivity for all.

Satellite Internet Market Restraints:

-

Signal Latency Limitations and Weather Related Disruptions Impacting Service Reliability and Performance in Certain Operational Environments

The difficulties with latency in sending a signal through a satellite connection are one of the issues with satellite internet services. For geosynchronous satellites, the issue with latency involves sending a signal from an extremely long distance away. Issues with bad weather such as heavy rain or storms might interfere and disrupt the signal. The previously mentioned issues are obstacles to implementing applications that need minimum latency without any interruption, such as games or stock market transactions. In addition, there is a problem with line of sight and crowded space orbit.

Satellite Internet Market Opportunities:

-

Rising Integration of Satellite Internet with IoT 5G Networks and Smart Mobility Systems Driving Next Generation Connectivity Solutions Worldwide

Integration of satellite internet with IoT devices, 5G network systems, and smart mobility solutions has been resulting in groundbreaking innovations in the existing global connectivity structure. Satellites can be integrated with terrestrial communication systems to provide uninterrupted connectivity anywhere in cities, rural areas, or remote places. The combined solution of connectivity serves purposes of autonomous vehicles, smart city initiatives, precision agriculture, and industrial IoT. Increasing demand for instant data transfer and connectivity of devices on a global scale is encouraging innovations in convergent networking technologies. Such advancements are likely to transform the entire framework of global communication technology in the future to come.

Recent Developments:

-

Amazon launched Project Kuiper in 2026, deploying 578 satellites in its LEO constellation, delivering 400 Mbps speeds and 20–40 ms latency, positioning itself as a major competitor to Starlink and reshaping global satellite broadband pricing dynamics.

-

SpaceX’s Starlink received FCC approval in 2025 for V3 satellites at 340 km altitude, enabling 10x capacity growth per satellite and supporting over 3 million users with 200+ Mbps speeds while reducing subscription pricing to USD 80/month.

-

OneWeb (Eutelsat) completed LEO-GEO integration in 2025 with Intelsat, forming a hybrid satellite network combining LEO speed and GEO coverage, creating enterprise-grade connectivity solutions for aviation, maritime, and government users with premium managed service offerings globally.

Satellite Internet Market Key Players

Some of the Satellite Internet Market Companies

-

Singtel Group

-

Freedomsat

-

EchoStar Corporation

-

Thuraya Telecommunications Company

-

Eutelsat Communications SA

-

OneWeb

-

SpaceX

-

Viasat Inc.

-

Axess

-

DSL Telecom

-

Hughes Network Systems LLC

-

Telesat

-

Embratel

-

Speedcast

-

SES S.A

-

Intelsat

-

L3 Technologies Inc.

-

SKY Perfect JSAT Group

-

Gilat Satellite Networks

-

Cobham Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.86 Billion |

| Market Size by 2035 | USD 45.22 Billion |

| CAGR | CAGR of 15.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Frequency Band (L-band, C-band, K-band, X-band) • By Industry (Energy & Utility, Government & Public Sector, Transport & Cargo, Maritime, Military, Corporates/Enterprises, Media & Broadcasting, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Singtel Group, Freedomsat, EchoStar Corporation, Thuraya Telecommunications Company, Eutelsat Communications SA, OneWeb, SpaceX, Viasat Inc., Axess, DSL Telecom, Hughes Network Systems LLC, Telesat, Embratel, Speedcast, SES S.A, Intelsat, L3 Technologies Inc., SKY Perfect JSAT Group, Gilat Satellite Networks, Cobham Limited |

Frequently Asked Questions

Ans: North America dominated with approximately 39% share; Asia Pacific is the fastest growing.

Ans: Government & Public Sector dominated the Satellite Internet Market with ~34% share; Transport & Cargo is the fastest growing segment (CAGR).

Ans: K-band dominated the Satellite Internet Market with ~41% share; L-band is the fastest growing segment (CAGR).

Ans: The Satellite Internet Market is expected to grow at a CAGR of 15.39% from 2026 to 2035.

Ans: The Satellite Internet Market was valued at USD 10.86 billion in 2025.

Get in Touch