Database Automation Market Size & Overview:

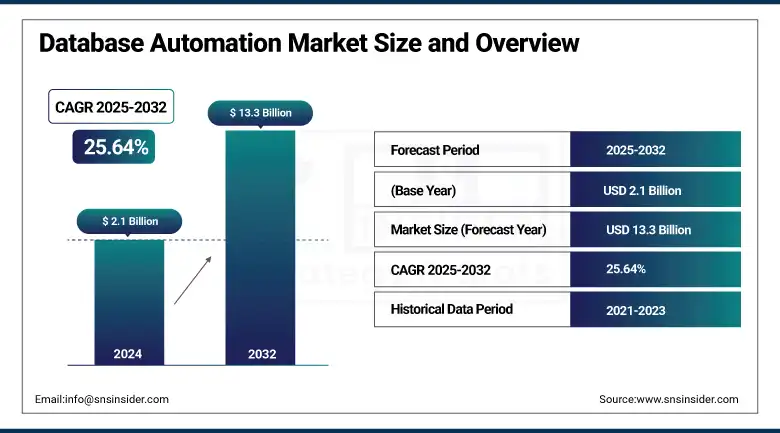

The Database Automation Market size was valued at USD 2.1 billion in 2024 and is expected to reach USD 13.3 billion by 2032, growing at a CAGR of 25.64% during 2025-2032.

The growth of the database automation market is attributed to the rising demand for scalable and efficient database management systems free from error. Automation tools reduce manual tasks by simplifying provisioning, patching, backup, and recovery operations, thereby increasing efficiency. Increasing demand for cloud-based services, growing volumes of data, and rising need for DevOps practices are some of the key growth factors. Database automation is increasingly becoming a priority among organizations in all sectors to increase performance and reduce downtime. The database automation market analysis demonstrates a strong CAGR during the forecast period, and finds North America and Asia-Pacific together as key contributors. The database automation market trend reflects the demand for AI-based automation and real-time analytics, suggesting that the future of the market is quite dynamic as economies across the globe are racing on the path of digital transformation.

To Get more information On Database Automation Market - Request Free Sample Report

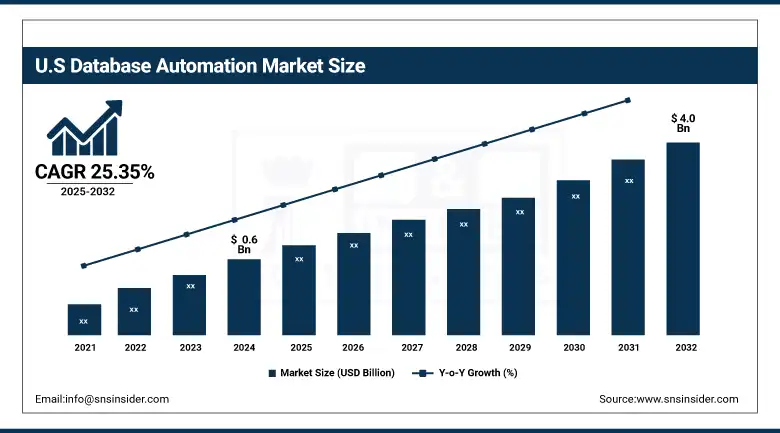

U.S. Database Automation Market is expected to grow from USD 0.6 billion in 2024 to USD 4.0 billion by 2034, at a CAGR of 25.35% . The increase in the adoption of cloud-native services, expansion of data volumes, along with machine learning and artificial intelligence technology integration, drives the growth. This is driving the need for automated solutions to manage databases in every industry

Database Automation Market Dynamics

Driver:

-

Migration to cloud environments increases complexity and scalability needs, driving demand for automated database management solutions.

One of the most significant factors driving the Database Automation Market is the increasing transition to cloud infrastructure. Due to their scalability, flexibility, and cost-effectiveness, many organizations are migrating from on-premise to cloud platforms such as AWS, Microsoft Azure, and Google Cloud. With an automation stack, they manage the complexity of cloud environments and automate deployment, performance tuning, patching, and backup tasks with fine-paced human intervention. This reduces operational overhead while making them more agile. With organizations continuing to embrace digital transformation, the need for automation in cloud database management will remain strong. Additionally, with DevOps and CI/CD pipelines integrated, it will push database automation because the data that is flowing will still need to be operated quickly, consistently, and securely across many hybrid environments.

Restraint:

-

Automation of critical database functions raises risks of data breaches and non-compliance, slowing implementation in regulated industries.

Although database automation increases efficiency, it also poses some challenges in terms of data security and regulatory compliance. Permitting automated access, updates, and backups also raises cybersecurity vulnerability unless appropriately governed. A large number of industries, especially healthcare, finance, and governments, have to adhere to very strict regulations ( HIPAA, GDPR, SOX, etc). Such frameworks must have tight control over data privacy, storage, and access. Also, poorly configured automation scripts or tools have the potential to expose sensitive data or violate compliance mandates. Additionally, automated systems are not subject to human judgment that can assess context-sensitive risks. As a consequence, it can limit wider adoption, particularly among enterprises that handle critical or sensitive information, due to the fear of possible breaches or violations of their data.

Opportunity:

-

Incorporating AI and ML enables smarter database automation, resulting in predictive insights and reduced operational disruptions.

Artificial intelligence and machine learning incorporate a large amount of knowledge for learning; this systematic method creates big openings within the Database Automation Market. These technologies can make automation tools smarter and empower predictive maintenance, anomaly detection, and intelligent performance tuning capabilities. Automated AI software dynamically adjusts configuration, resource allocation, indexing strategies, and other variables based on usage patterns, leading to increased efficiency and reduced downtime. Machine learning algorithms can also be used to predict impending system failures or bottlenecks, affording proactive remediation. It makes database management proactive instead of reactive. There is fortune in AI/ML-powered commerce, and the vendors investing in platforms stand to gain a lion's share. The approach that requires more sophisticated enterprise AI solutions will be the area where enterprises demand more intelligent automation solutions, as the complexity of data is growing.

Challenge:

-

Outdated infrastructure lacks compatibility with modern tools, making automation integration costly and technically difficult.

However, one of the most prominent challenges of the database automation market lies in integrating automation tools with traditional systems. Various enterprises are still using outdated database technologies that general automation frameworks do not work well to serve the purpose of automation. Most of these systems might not have the APIs or standardization needed to provide seamless automation, leaving you to struggle with how to apply updates, perform backups, or efficiently manage workloads. Automating requires a lot of customizing in such environments, which is a long- and expensive-winded process. The IT teams will also be inexperienced, somewhere or the other, they will not know about amalgamating the old school method and the new, upcoming, faster method. This limits the effectiveness of automation, causing organizations to retain manual processes, resulting in delayed digital transformation and lower ROI.

Database Automation Market Segmentation Analysis:

By Component

The solution segment dominated the database automation market and accounted for 62% of revenue share in 2024, due to rising demand for automation tools to ensure optimal database performance, reduced downtime, and improved operational efficiency. Integrated solutions are the ones that organizations are choosing to manage complex, cloud-based databases. This segment will continue to dominate the market as organizations focus on automating their business processes to scale their operations, reduce manual errors, and implement digital transformation programs across verticals.

The services segment is anticipated to witness the fastest growth rate during the forecast period, primarily due to the demand for consulting, implementation, and managed services, which should support complex deployments. With in-house capabilities increasingly difficult to maintain and the integration of existing applications ever more frustrating, organizations have turned to niche service providers. Lasting Growth will ride on demand for support, training, and custom database automation frameworks.

By Application

The provisioning segment dominated the database automation market and accounted for 47% of the database automation market share in 2024, as organizations move towards automating database setup and deployment to minimize manual configuration time while ensuring consistency. Rapid application deployment is only possible because of the advancement in automated provisioning of the whole technical stack, DevOps, and cloud-native architectures. As enterprises ramp up infrastructure and demand for swifter and error-free database rollout, this segment will remain at the forefront in hybrid and multi-cloud environments.

For Instance, on April 30, 2025, the Cloud Security Alliance (CSA) launched the Compliance Automation Revolution (CAR) initiative to address the growing complexity of regulatory compliance in data security and privacy.

The security and compliance segment is expected to register the fastest CAGR during the forecast period is projected to be the result of increasing regulations regarding data privacy, as well as more malicious activities and cyber threats posing a great hazard to compliance for many organizations. They need automated tools that will provide access control, audit trails, and policy compliance. Global regulatory requirements will continue to grow stricter, spurring rapid growth in this sector, with organizations using databases without needing manual monitoring or intervention, and still providing security and compliance.

By End-Use

The BFSI segment dominated the database automation market and accounted for a significant revenue share in 2024, owing to the demand for high-performance, secure, and always-available databases. That is because operational efficiencies, compliance, and minimal human touch in transaction-heavy environments are achieved just through automation. Despite the industry economic pressures, the need for database automation will remain high as the financial services industry digitizes services, moves to cloud platforms, and needs to ensure data integrity, real-time updates, and automate periodic regulatory reporting.

IT and telecom sector is projected to register the highest CAGR during the forecast period, Due to the explosive growth of data, expanding networks, and the deployment of 5G. These industries demand automated database solutions that are scalable to handle large volume of real-time data. With the increase of cloud-native development, DevOps and AI adoption, automation is key for performance, speed, and reliability in hyper-demanding environments.

Database Automation Market Regional Outlook:

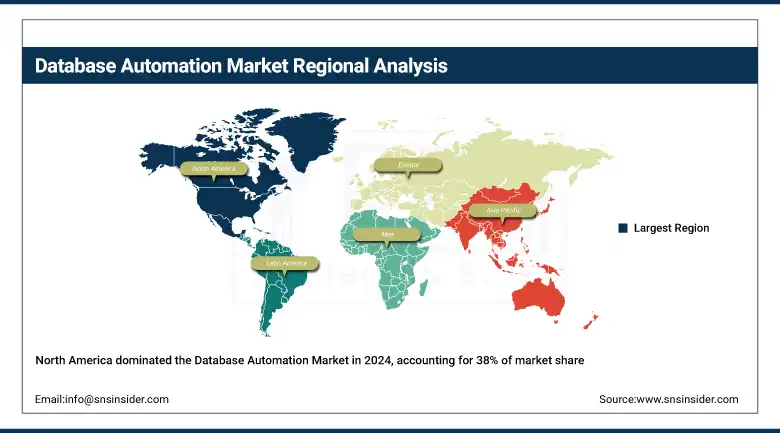

The North American region dominated the market and accounted for 38% of revenue share, owing to the presence of cloud service providers, early adoption of automation technologies, and high investment in IT infrastructure. Mature strategies of digital transformation across the BFSI, healthcare, and telecom sectors in the region. This trend will keep North America the leader as emphasis stays on AI-powered database tools and enterprise cloud migration.

Get Customized Report as per Your Business Requirement - Enquiry Now

The fastest-growing regional market is expected to be Asia Pacific, due to the rapid growth of digitalization and cloud adoption and the expanding startup ecosystem in China, India, and Southeast Asia in general. However, the need for scalable and automated database management solutions across all workloads and applications is set to rise due to increasing investments in IT modernization, coupled with supportive government initiatives for smart infrastructure and data governance across the region.

The growing need for regulatory compliance, particularly with data protection regulations such as GDPR, along with rising cloud adoption and the booming digital transformation market in sectors including BFSI, government, and healthcare, among others, has led to the growth of Europe’s database automation market. With a focus on data governance and efficiency driven by automation, the adoption will be steadily rising across enterprises looking for scalable and secure data management solutions.

With a well-developed industrial base, good IT infrastructure, and a high emphasis on Industry 4.0, Germany is Leading the European Market. For operational efficiency and compliance, German enterprises are prioritizing automation. The continued cloud computing and smart technology investment will also further drive the demand for the database automation solutions.

Key Players

The major database automation market companies are Oracle Corporation, Microsoft Corporation, IBM Corporation, BMC Software Inc., CA Technologies, Amazon Web Services (AWS), Datavail Corporation, Redgate Software, Micro Focus, Quest Software and others

Recent Developments

-

On May 5, 2025, IBM introduced the Db2 Intelligence Center, an AI-powered platform designed to streamline database management for Db2 administrators. This unified console offers advanced monitoring, AI-driven troubleshooting, and intelligent query optimization, enabling DBAs to proactively manage databases and reduce manual interventions.

-

November 7, 2024, Redgate announced the integration of AI and machine learning capabilities into its database DevOps portfolio. The enhancements include synthetic data generation in Redgate Test Data Manager and intelligent alerting in Redgate Monitor, aiming to improve efficiency, reduce manual errors, and maintain data security across database management processes.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.1 Billion |

| Market Size by 2032 | USD 13.3 Billion |

| CAGR | CAGR of 25.64 % From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2024-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Solution, Services) •By Application (Provisioning, Backup, Security and Compliance) •By End-Use (Government, BFSI, Healthcare, IT and Telecom, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Oracle Corporation, Microsoft Corporation, IBM Corporation, BMC Software Inc., CA Technologies, Amazon Web Services (AWS), Datavail Corporation, Redgate Software, Micro Focus, Quest Software and others in report |

Frequently Asked Questions

Ans- North America region dominated the Database Automation Market with 39% of revenue share in 2024.

Ans- The provisioning segment dominated the database automation market and accounted for 47% of the database automation market share in 2024.

Ans- Migration to cloud environments increases complexity and scalability needs, driving demand for automated database management solutions.

Ans- The Database Automation Market size was valued at USD 2.1 billion in 2024 and is expected to reach USD 13.3 billion by 2032.

Ans- The CAGR of the Database Automation Market during the forecast period is 25.64% during 2025-2032.

Get in Touch