Wearable Computing Market Report Scope & Overview:

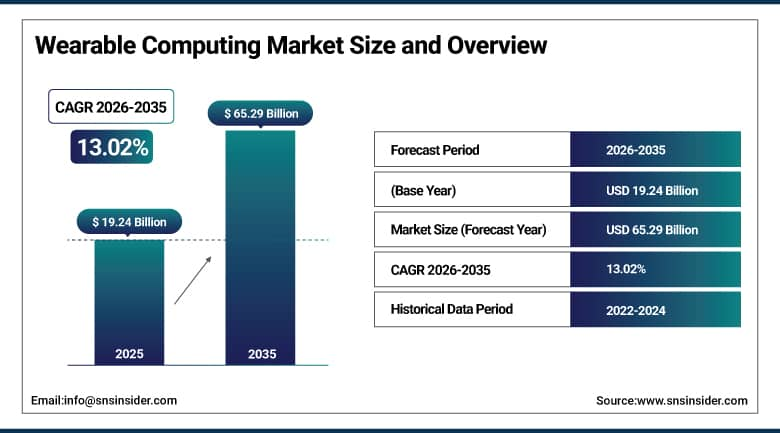

The Wearable Computing Market was valued at USD 19.24 Billion in 2025 and is expected to reach USD 65.29 Billion by 2035, growing at a CAGR of 13.02% from 2026 to 2035.

The Wearable Computing Market is experiencing rapid growth because of an increase in the demand for smart watches, fitness bands, and health monitors. An increasing level of awareness about personal health and well-being along with the evolution of AI, sensors, and low-power processing chips will result in improvements in the capabilities of wearable computing devices. The development of 5G technology and IoT networks allows real-time data transfer from one device to another with improved user experiences. The use of wearables in the field of healthcare, industry, enterprises, and AR/XR technologies will continue to drive growth in the market.

According to the International Telecommunication Union (ITU), 5.5 billion people, representing 68% of the global population, were using the Internet in 2024, while continued expansion of mobile broadband connectivity is providing the digital infrastructure required for connected wearable devices and real-time data exchange. Furthermore, the World Health Organization (WHO) estimates that approximately 1.28 billion adults aged 30–79 years worldwide are living with hypertension, significantly increasing demand for wearable devices capable of continuous monitoring of heart rate, electrocardiogram (ECG), blood pressure, and other vital health parameters.

Market Size and Forecast

-

Market Size in 2026E: USD 21.74 Billion

-

Market Size by 2035: USD 65.29 Billion

-

CAGR: 13.02% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Wearable Computing Market - Request Free Sample Report

Wearable Computing Market Trends

-

Rising adoption of smartwatches, fitness trackers, and smart glasses driving demand for advanced wearable computing technologies across consumer and enterprise applications

-

Growing integration of AI, IoT, and edge computing enabling real-time health monitoring, personalized insights, and intelligent wearable experiences

-

Increasing use of wearable devices in healthcare for remote patient monitoring, chronic disease management, and preventive wellness applications

-

Expanding adoption of augmented reality (AR) and mixed reality (MR) wearables across industrial, logistics, and field service operations to enhance workforce productivity

-

Continuous advancements in low-power processors, sensor technologies, and battery efficiency improving device performance, comfort, and extended operating life

The U.S. Wearable Computing Market Outlook

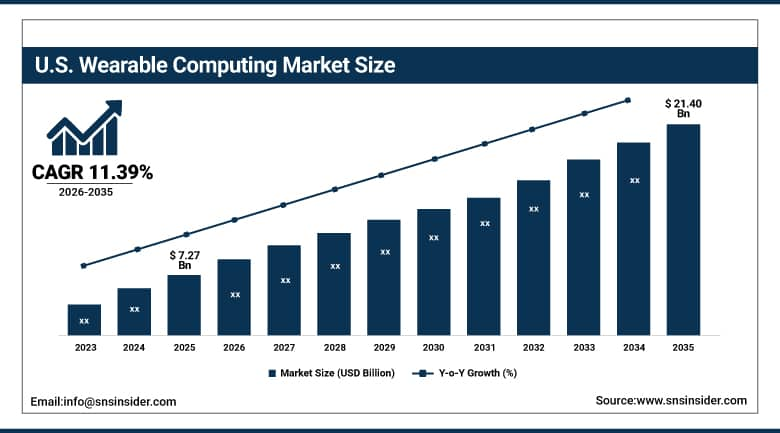

The U.S. Wearable Computing Market was valued at approximately USD 7.27 Billion in 2025 and is expected to reach approximately USD 21.40 Billion by 2035, growing at a CAGR of approximately 11.39%.

The United States is the world's most commercially advanced wearable computing market, due to its global market leadership in consumer wearable hardware provided by companies like Apple, Fitbit, and Garmin; integration of wearables into its healthcare system, where wearable remote patient monitoring technologies have become part of cardiac rehabilitation, diabetes, and postoperative monitoring; and corporate technology adoption culture, which sees investments in worker productivity through deployment of smart glasses and wearable worker assistance technology in industries such as manufacturing and logistics. US wearables market revenue from the global leader, Apple, including Apple Watch, AirPods, and Apple Vision Pro devices, makes it the top-valued individual country market for high-end wearables.

According to the Centers for Disease Control and Prevention (CDC), approximately 38.4 million people in the United States are living with diabetes, driving increased adoption of wearable glucose monitoring systems, continuous health tracking devices, and connected digital health technologies.

Wearable Computing Market Segment Analysis

-

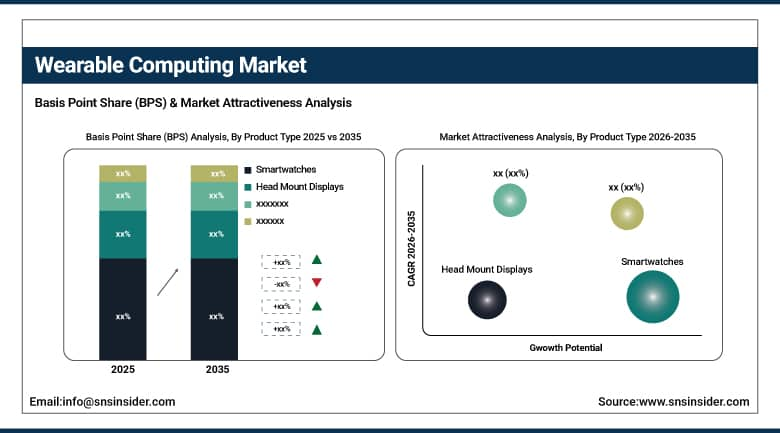

By Product Type, smartwatches segment dominated the Wearable Computing Market in 2025 with 46% share; head mount displays segment is the fastest growing segment.

-

By Connectivity, Bluetooth segment dominated the market in 2025 with 64% share; 4G/5G segment is the fastest growing segment.

-

By Application, consumer segment dominated the market in 2025 with 79% share; non-consumer segment is the fastest growing segment.

By Product Type, Smartwatches segment dominates the Wearable Computing Market, Head Mount Displays segment expected to grow fastest

The smartwatches segment dominated the Wearable Computing Market owing to extensive usage by consumers for health monitoring, fitness tracking, communication, and mobility applications. Features like heart rate tracking, sleep tracking, GPS tracking, contactless payments, and smartphone connectivity have resulted in high product demand. Constant developments in sensors, batteries, appealing designs, and awareness about preventive healthcare have bolstered the dominance of the segment in the market.

The head mount displays segment is the fastest growing in the Wearable Computing Market owing to increased adoption of augmented reality and virtual reality solutions in industrial, healthcare, defense, educational, and entertainment industries. Such devices provide advanced visualization capabilities, remote collaboration, workforce training, and immersive experience for users. Innovations in display technology, lighter designs, AI integration, and digital transformation of enterprises have fueled the demand for head mount display products across the globe.

By Connectivity, Bluetooth segment dominates the Wearable Computing Market, 4G/5G segment expected to grow fastest

The Bluetooth segment dominated the Wearable Computing Market as it offers effective, low power and affordable wireless communication between wearable devices and smartphones, tablets and other connected products. High level of compatibility, simplicity of use and effective data transferring are the reasons why it is preferable for use in smartwatches, fitness trackers and wireless monitoring devices. Improvement of Bluetooth technologies standards and development of consumer electronics industry contribute to the leadership of this segment on the market.

The 4G/5G segment is the fastest growing in the Wearable Computing Market owing to the rise in demand for standalone wearable devices that can provide high-speed connection without using smartphones. Thanks to the fast data transfer, low latency and network reliability, new advanced applications like real-time health monitoring, remote communication and cloud services can be implemented in the device. Expansion of 5G networks, popularity of connected healthcare and always-connected wearables increase the growth rate of the segment.

By Application, Consumer segment dominates the Wearable Computing Market, Non-consumer segment expected to grow fastest

The consumer segment dominated the Wearable Computing Market owing to high demand for smartwatches and fitness bands and other wearables that help in health monitoring, communication, entertainment, and lifestyle management. High health consciousness, higher smartphone adoption, and increased inclination towards connected technologies have contributed to high usage by consumers. Constant innovations in products and ecosystem expansion, as well as addition of artificial intelligence features in the wearable computing market, have further solidified the dominance of this segment.

The non-consumer segment is the fastest growing in the Wearable Computing Market owing to the growing adoption in the healthcare, manufacturing, logistics, defense, and enterprise sectors. Companies are increasingly adopting wearable computing technology for workforce safety, remote assistance, asset management, and improving productivity. Growing initiatives related to digital transformation and adoption of augmented reality, artificial intelligence, and IoT technologies in the industries, as well as investments in smart workplace solutions, are driving demand for wearables.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Wearable Computing Market Insights

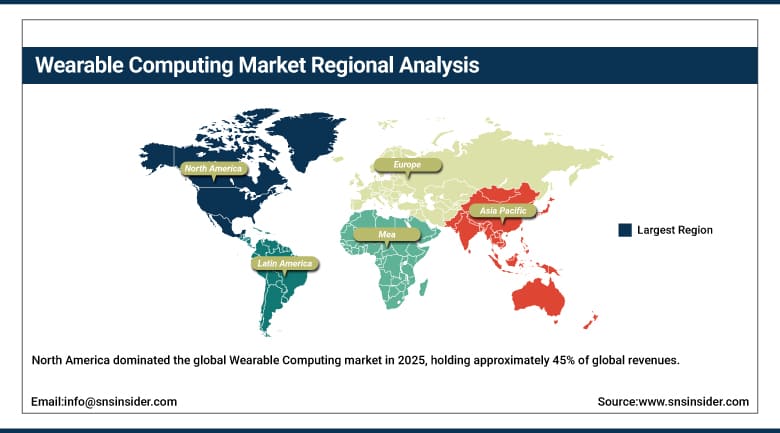

North America dominated the global Wearable Computing market in 2025, holding approximately 45% of global revenues. The United States accounts for approximately 84.73% of regional revenue through the global commercial dominance of Apple, Fitbit, and Garmin in premium consumer wearables, the progressive integration of wearable remote patient monitoring into U.S. clinical care pathways, and growing enterprise deployment of smart glasses and wearable worker assistance technology across manufacturing, logistics, and healthcare provider organisations.

he United States also hosts the most commercially advanced wearable computing startup ecosystem, with companies including WHOOP, Oura, Whoop, and Vuzix developing specialised products for high-performance athletic monitoring, discrete consumer health sensing, and enterprise AR respectively, whose collective innovation sustains the market's competitive dynamism.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Wearable Computing Market Insights

Europe held approximately 25.47% of global Wearable Computing revenues in 2025. Germany accounts for approximately 27.84% of European revenues through its industrial enterprise adoption of smart glasses and wearable worker assistance technology at automotive and manufacturing facilities, its medical device regulatory framework that is progressively enabling clinical wearable application development, and its strong consumer market for smartwatches and fitness devices.

The United Kingdom contributes secondary European demand through NHS wearable remote patient monitoring programme development and strong consumer smartwatch adoption. France, Netherlands, and Scandinavia each contribute meaningful European demand through their healthcare innovation programmes and enterprise technology adoption in manufacturing and logistics.

According to the European Commission, the Digital Europe Programme allocates more than €7.5 billion to accelerate investments in artificial intelligence (AI), advanced digital technologies, cybersecurity, cloud infrastructure, and high-performance computing.

Asia Pacific Wearable Computing Market Insights

Asia Pacific is the fastest-growing regional Wearable Computing market, projected to expand at a CAGR of approximately 15.84% through 2035, driven by China's dominant consumer electronics manufacturing and large domestic consumer market for smartwatches and fitness devices from Huawei, Xiaomi, and Oppo at highly competitive price points, Japan and South Korea's advanced electronics industry and consumer technology adoption, and the rapidly growing middle-income consumer markets in India, Southeast Asia, and Australia where rising disposable incomes and smartphone penetration are driving first-time wearable adoption.

China accounts for approximately 38.47% of Asia Pacific revenues through its dual role as the world's largest consumer electronics manufacturing hub and a large domestic wearable computing consumer market whose brand diversity and price range breadth creates the highest market access flexibility globally.

MEA & Latin America Wearable Computing Market Insights

Middle East and Latin America are growing Wearable Computing markets where rising consumer technology adoption, expanding healthcare digital transformation programmes, and growing enterprise technology deployment are creating increasing demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its high-income consumer base, early adoption culture for premium technology products, and smart city and digital health programme development that includes wearable remote patient monitoring components.

Saudi Arabia's Vision 2030 digital transformation agenda and growing tech-savvy urban population contribute secondary MEA demand. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large urban consumer population, growing smartphone ecosystem, and expanding healthcare digital transformation investment.

Market Dynamics

Growth Drivers: Clinical health monitoring and enterprise AR wearables drive growing demand across consumer and commercial markets.

Continuous blood pressure monitoring, sleep apnea screening, and ECG monitoring features in Apple Watch Series 10 are the cutting edge examples of an emerging industry trend where consumer smartwatch platforms are increasingly integrating health sensing technologies that can claim healthcare professional endorsement and regulatory clearance necessary to be reimbursable and included in clinical pathways.

The addition of each new health monitoring feature cleared by the FDA increases the potential consumer base from fitness enthusiasts to clinically oriented consumers who make purchase decisions based on health risk management rather than fitness tracking, thus enabling premium demand generation among a wider customer base. Enterprise adoption of smart glasses is growing rapidly due to productivity improvements that have been proven in manufacturing operations through reduced errors, field service by improving first visit resolution rate, and logistics through improved picking accuracy.

Restraints: Battery limitations, comfort concerns, and biometric data privacy issues restrict wider wearable device adoption.

The amount of energy consumed by continuous biometric monitoring, GPS location services, LTE connections, and display operation in the case of smartwatches and smart glasses imposes certain limitations on battery performance, making certain tradeoffs inevitable between the capabilities of such devices and the experience of using them. The frequency of the need to charge smartwatches is determined by the type of the device and usage scenario of its owner. Users of smartwatches for health monitoring who prefer to have their full sleep analyzed are especially sensitive to the problem of limited battery performance since they cannot be charged in the middle of the day.

Consumers' concerns about the continuous monitoring of their health, location, and behavior are creating regulatory problems and reluctance from consumers that should be addressed by the platforms by providing the necessary information about the management of the data collected.

Opportunities: AI-powered AR glasses and clinical reimbursement pathways create significant wearable computing market growth opportunities.

Healthcare reimbursement integration is the biggest structural play in the wearable computing growth opportunity. The Centers for Medicare and Medicaid Services have been gradually adding codes for reimbursement for remote physiologic monitoring where healthcare practitioners can charge their patients for providing care services through wearable monitoring technology.

Every condition added for reimbursement results in a pool of buyers within the clinical segment that is bigger than any revenue from consumer purchasing. Edge computing advances lowering the time lag in AI inference for ambient intelligence assistance in next-gen AR smart glasses powered by contextual AI would be of much more commercial benefit than today’s smart glasses.

Recent Developments:

-

2025: Google LLC introduced its Pixel Vision smart glasses platform targeting enterprise applications including remote assistance, manufacturing workflow guidance, and real-time data visualisation, integrating the Gemini AI model for contextual natural language interaction with the visual field to enable voice-commanded procedural guidance and expert remote assistance at frontline worker level.

-

2025: Samsung Electronics announced a strategic partnership with leading healthcare providers to co-develop certified medical wearable devices focused on chronic disease management, integrating advanced sensor technology with clinical validation to expand Samsung's wearable platform from consumer health monitoring into clinically approved patient management applications.

-

2024: Apple launched Apple Watch Series 10 incorporating continuous blood pressure trend monitoring, improved sleep apnea detection, and enhanced cardiac monitoring through a redesigned sensor architecture, demonstrating the progressive migration of clinical-grade health monitoring capability into mainstream consumer wearable computing platforms.

Wearable Computing Market Key Players are:

-

Apple Inc.

-

Samsung Electronics

-

Google LLC

-

Garmin Ltd.

-

Huawei Technologies Co., Ltd.

-

Xiaomi Corporation

-

Fitbit (Google)

-

Sony Group Corporation

-

Amazfit (Zepp Health)

-

Fossil Group, Inc.

-

Lenovo Group Limited

-

Microsoft Corporation

-

Meta Platforms, Inc.

-

HTC Corporation

-

Vuzix Corporation

-

RealWear, Inc.

-

Magic Leap, Inc.

-

Seiko Epson Corporation

-

Qualcomm Incorporated

-

Oura Health Ltd.

Wearable Computing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.24 Billion |

| Market Size by 2035 | USD 65.29 Billion |

| CAGR | CAGR of 13.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Smartwatches, Smart Jewelry, Fitness Trackers, Body-worn Cameras, Head Mount Displays, Others) • By Connectivity (Bluetooth, Wi-Fi, 4G/5G, Others) • By Application (Consumer, Non-consumer) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Apple Inc., Samsung Electronics, Google LLC, Garmin Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Fitbit (Google), Sony Group Corporation, Amazfit (Zepp Health), Fossil Group, Inc., Lenovo Group Limited, Microsoft Corporation, Meta Platforms, Inc., HTC Corporation, Vuzix Corporation, RealWear, Inc., Magic Leap, Inc., Seiko Epson Corporation, Qualcomm Incorporated, Oura Health Ltd. |

Frequently Asked Questions

Clinical health monitoring, remote patient care, AR smart glasses, AI health analytics, and growing health awareness drive wearable computing market growth.

The Wearable Computing Market was valued at USD 19.24 Billion in 2025.

The Wearable Computing Market is expected to grow at a CAGR of 13.02% from 2026 to 2035.

The smartwatches segment dominated the Wearable Computing Market in 2025.

North America dominated the Wearable Computing Market in 2025.

Get in Touch