Digital Security Control Market Report Scope & Overview:

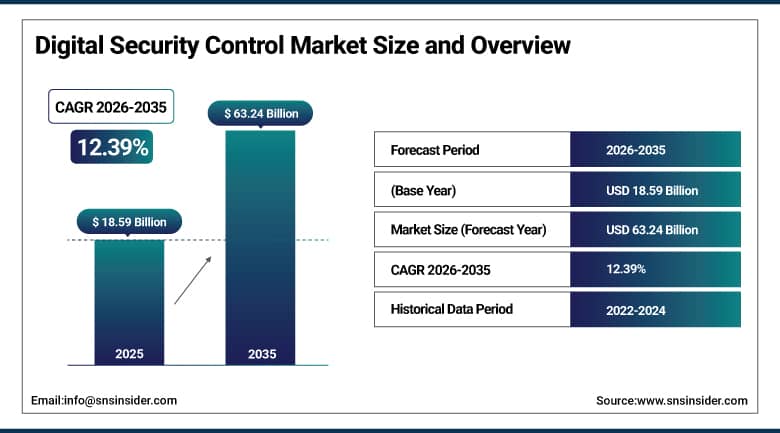

The Digital Security Control Market was valued at USD 18.59 Billion in 2025 and is expected to reach USD 63.24 Billion by 2035, growing at a CAGR of 12.39% from 2026 to 2035.

The global digital security control market is experiencing significant and accelerating growth, driven by the increasing adoption of advanced security solutions in response to rising cybersecurity threats, stringent data privacy regulations, and the expanding digital economy's demand for robust identity verification and access management. Digital security control encompasses the technologies and systems that verify identity, control access to physical and digital assets, protect data integrity, and monitor network activity across enterprise, government, and consumer environments. The market is propelled by the integration of artificial intelligence and machine learning that is revolutionising threat detection and response, the growing focus on consumer data protection under regulations including GDPR and CCPA, the rapid proliferation of connected devices creating new authentication requirements, and the global financial sector's relentless investment in fraud prevention and transaction security.

In 2024, Microsoft expanded its AI-powered cybersecurity capabilities across its enterprise cloud security platforms, integrating advanced threat intelligence from its Security Copilot platform with biometric multi-factor authentication and zero-trust identity verification across Microsoft Entra, Azure, and Microsoft 365 enterprise deployments. This integration enables enterprise customers to enforce continuous identity assurance through behavioural biometrics, device compliance attestation, and risk-based conditional access policies that adapt authentication requirements dynamically based on real-time threat signal analysis rather than static policy rules.

Market Size and Forecast

-

Market Size in 2026E: USD 20.89 Billion

-

Market Size by 2035: USD 63.24 Billion

-

CAGR: 12.39% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Digital Security Control Market - Request Free Sample Report

Digital Security Control Market Trends

-

Growing adoption of passwordless authentication based on FIDO2 and WebAuthn standards is improving security while reducing reliance on vulnerable password-based login methods

-

Behavioral biometrics are enabling continuous user authentication by analyzing typing patterns, mouse movements, and user behavior to detect account compromise in real time

-

Decentralized identity solutions based on blockchain and verifiable credentials are emerging to enhance privacy, user control, and secure digital identity management

-

Convergence of physical and logical access control is driving unified identity management platforms that secure both facility access and digital resources through a single framework

-

Rising focus on quantum-safe cryptography is accelerating the adoption of next-generation digital signature technologies designed to protect identity verification systems against future quantum computing threats

U.S. Digital Security Control Market Outlook

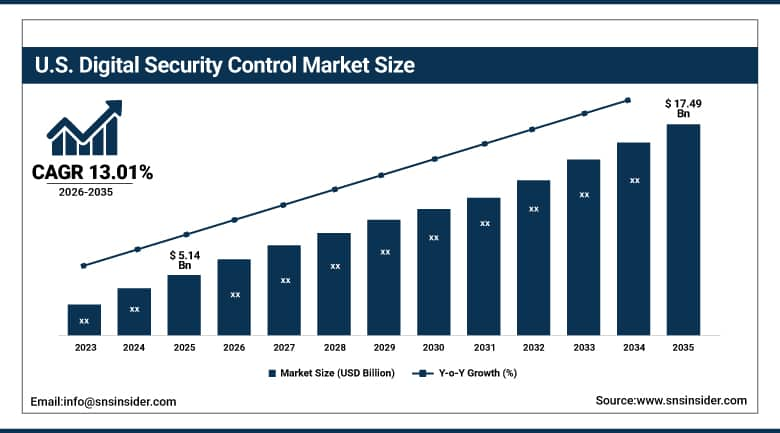

The U.S. Digital Security Control Market was valued at approximately USD 5.14 Billion in 2025 and is expected to reach approximately USD 17.49 Billion by 2035, growing at a CAGR of approximately 13.01%.

The U.S. is the most commercially significant digital security control market, driven by the growing focus on consumer data protection under CCPA and sector-specific privacy legislation, strong enterprise cybersecurity investment culture, and the large-scale presence of Thales, HID Global, NXP Semiconductors, Broadcom, Ping Identity, and Microsoft Security whose combined product and platform revenues define the domestic commercial standard. The financial services sector's above-average investment in biometric authentication and digital signature platforms, the federal government's identity credential and access management programme investment, and the healthcare sector's HIPAA-driven access control compliance create three independently motivated institutional demand streams that sustain consistent growth. The rollout of REAL ID compliant digital identity credentials across U.S. state governments creates structured government-initiated biometric and smart card procurement at state and federal agency scale.

In 2023, Thales Group launched an enhanced version of its SafeNet Trusted Access cloud authentication platform with expanded biometric authentication support, adaptive risk-based access policies, and passwordless MFA options for enterprise workforce identity management. The platform enhancement directly addresses the enterprise market's transition from conventional password-based authentication toward biometric and hardware security key-based zero-trust identity architectures that eliminate the credential theft vulnerability that passwords inherently create.

Digital Security Control Market Segment Analysis

-

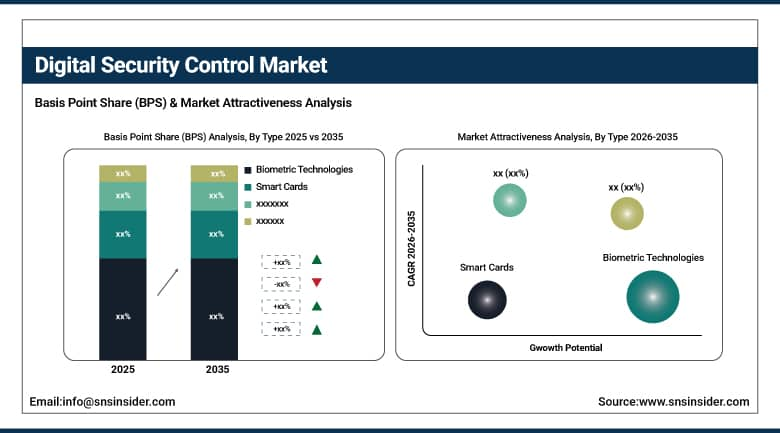

By Type, the Biometric Technologies segment dominated the Digital Security Control Market with approximately 56% share in 2025, while the Smart Cards segment is the fastest growing.

-

By Application, the User Authentication segment dominated the Digital Security Control Market with approximately 54% share in 2025, while the Network Monitoring segment is the fastest growing.

-

By End User, the BFSI segment dominated the Digital Security Control Market with approximately 32% share in 2025, while the Healthcare segment is the fastest growing.

By Type, biometric technologies dominate, smart cards grow fastest

Biometric technologies retained the dominant type position with approximately 56% of the digital security control market in 2025. The segment's commercial primacy reflects the fundamental shift in enterprise and consumer security architecture from knowledge-based credentials that adversaries can steal, replicate, or compromise toward inherent physical identity characteristics that uniquely identify individuals without shared secret vulnerability. Fingerprint scanning's deployment across enterprise access control, financial services customer verification, and government identity programmes creates the highest-volume single biometric modality. Facial recognition's adoption in banking digital onboarding, border control biometric identity verification, and retail loss prevention collectively creates above-average revenue from high-value commercial deployment. Iris recognition's deployment in maximum-security government and defence environments sustains premium pricing for the modality's unmatched distinctiveness and permanence characteristics.

Smart cards are the fastest-growing type because the convergence of digital payment adoption, government digital identity programme investment, and healthcare patient identification system modernisation creates structured above-average procurement growth across multiple independent end-user demand streams. Each national digital identity card programme that issues contactless smart card credentials to millions of citizens creates procurement at national scale. The financial services industry's contactless payment card issuance, whose EMV chip technology creates a smart card technology specification that sustains consistent global issuance volumes, and the healthcare sector's patient identification card programmes together create the commercial foundation for smart card's fastest-growing type designation.

By Application, user authentication dominates, network monitoring grows fastest

User authentication retained the dominant application position with approximately 54% of the digital security control market in 2025. As the foundational security function that establishes verified identity before any system access, transaction authorisation, or data access is permitted, user authentication represents the most universally deployed digital security control application across enterprise, government, and consumer digital environments. Each enterprise workstation, cloud application, and mobile device that requires identity verification before access creates user authentication procurement whose commercial aggregate across the global digital infrastructure creates the application's dominant revenue position. The progressive evolution of authentication from single-factor password to multi-factor authentication combining biometrics, hardware tokens, and behavioural analytics creates above-average per-user authentication platform investment that sustains revenue growth beyond mere user count expansion.

Network monitoring is the fastest-growing application because zero-trust security architecture's elimination of implicit network trust creates the requirement for continuous traffic analysis, user behaviour monitoring, and anomaly detection that conventional perimeter-only network security cannot provide. Each enterprise that adopts zero-trust principles must implement network monitoring solutions that inspect all traffic, log all access events, and detect behavioural deviations that indicate compromised accounts or insider threat activity. The AI-powered network monitoring platform's ability to process telemetry at scale that human analysts cannot manually review creates commercial motivation for automated monitoring investment that sustains the application segment's fastest-growing designation.

By End User, BFSI dominates, healthcare grows fastest

The BFSI segment retained the dominant end-user position with approximately 32% of the digital security control market in 2025. The financial services industry's position as the primary target of financially motivated cybercriminal operations, whose fraud, ransomware, and account takeover attacks create direct financial loss exposure that motivates above-average security investment, combined with the extraordinary volume of daily financial transactions requiring fraud-prevention authentication, creates the most commercially concentrated digital security control demand of any industry vertical. The payment card industry's PCI DSS compliance requirements, the EU's PSD2 strong customer authentication mandate, and equivalent bank regulator requirements in every major market create compliance-driven authentication investment independent of commercial ROI calculation. Each bank, insurer, asset manager, and payment processor whose customer-facing and internal system security must satisfy regulatory and commercial fraud prevention objectives creates above-average per-organisation digital security control investment.

Healthcare is the fastest-growing end user because the combination of HIPAA-mandated electronic health record access control, the growing telehealth platform's identity verification requirements, and the healthcare sector's progressive adoption of biometric patient identification at care delivery points creates structured above-average digital security control procurement. Each electronic health record access event that requires clinician authentication, each telemedicine consultation that requires patient identity verification, and each pharmacy dispense event that requires patient identification creates healthcare digital security control demand whose aggregate across the global healthcare system grows proportionally with digital health adoption. The healthcare sector's above-average data breach cost, consistently the highest of any industry in IBM's annual breach cost survey at over USD 10 million per incident, creates commercial motivation for premium security investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Digital Security Control Market Insights

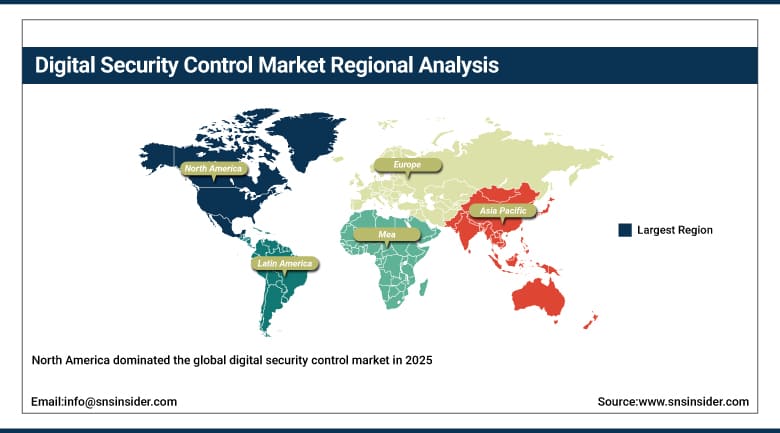

North America dominated the global digital security control market in 2025, driven by strong enterprise cybersecurity investment, advanced digital infrastructure, stringent data privacy regulation, and the commercial presence of Thales, HID Global, Broadcom, Microsoft Security, and NXP Semiconductors whose combined product revenues define the domestic commercial standard. The United States accounts for approximately 87.4% of North American revenues through the financial services sector's authentication investment, the federal government's ICAM programme, and the healthcare sector's HIPAA compliance procurement.

Canada contributes approximately 12.6% of North American revenues through its banking sector's digital security investment, the federal government's digital identity programme, and the growing healthcare sector's patient identification system modernisation across provincial health systems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Digital Security Control Market Insights

Europe is the world's most regulation-driven digital security control market where GDPR's data protection requirements, eIDAS's electronic identity and trust services framework, the EU's NIS2 Directive, and PSD2's strong customer authentication mandate create a layered compliance environment that sustains non-discretionary digital security investment across financial services, healthcare, and government sectors. Germany accounts for approximately 22.3% of European revenues through its financial sector's authentication investment, the Bundesdruckerei's government digital identity operations, and the strong enterprise biometrics adoption across manufacturing and critical infrastructure.

The United Kingdom, France, and the Netherlands are significant secondary markets where the UK's digital identity and attributes trust framework, BNP Paribas' authentication investment, and ING's digital banking security procurement create consistent demand. Thales Group's French headquarters and Giesecke+Devrient's German operations sustain regional market supply.

Asia Pacific Digital Security Control Market Insights

Asia Pacific is the fastest-growing regional digital security control market, driven by China's digital payment ecosystem's authentication scale, India's Aadhaar biometric identity infrastructure, Japan's My Number digital identity programme, South Korea's advanced banking authentication standards, and Southeast Asia's rapidly expanding digital financial services sector. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary digital payment authentication volume, the national electronic identity card programme, and the government's digital governance investment in biometric identity systems.

India represents the most commercially dynamic emerging market within Asia Pacific where the Aadhaar biometric identity system's 1.4 billion enrolments create the world's largest single biometric identity infrastructure, the Unified Payments Interface's transaction authentication requirements create structured commercial demand, and the growing financial inclusion programme creates first-time digital identity and authentication procurement across hundreds of millions of previously unserved individuals.

MEA & Latin America Digital Security Control Market Insights

The UAE leads MEA revenues at approximately 31.2% through its smart city digital identity investment, DIFC financial sector authentication compliance, and the Emirates ID Authority's biometric identity infrastructure creating structured government-driven procurement. Saudi Arabia's National Cybersecurity Authority mandates and Vision 2030's digital government investment add complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its Pix instant payment system's authentication requirements, the banking sector's biometric verification investment, and the government's digital identity programme. Mexico's financial sector and Colombia's digital banking growth collectively sustain regional expansion through 2035.

Market Dynamics

Growth Drivers: Escalating data breach costs and regulatory authentication mandates creating non-discretionary security investment

The escalating financial and reputational cost of data breaches is the digital security control market's most commercially compelling structural growth driver. IBM's 2024 Cost of a Data Breach Report documented the average global breach cost at USD 4.88 million, with financial services averaging over USD 6 million per incident, creating financial loss exposure that substantially exceeds the annual cost of comprehensive digital security control investment for most organisations. Each publicised breach that exposes inadequate authentication controls at a peer organisation creates market awareness and procurement urgency among security decision makers whose risk avoidance motivation sustains digital security investment through economic cycles where purely cost-based procurement rationalisation would moderate spending.

Regulatory authentication mandates create additional non-discretionary procurement motivation that sustains digital security control investment independently of commercial risk-benefit analysis. The EU's eIDAS 2.0 regulation requiring qualified electronic signature and digital identity wallet compliance, the banking sector's PSD2 strong customer authentication requirement, HIPAA's access control and audit logging mandate, and equivalent national regulations create defined technical implementation requirements whose compliance timeline creates structured procurement cycles.

Restraints: Privacy concerns limiting biometric data collection and implementation complexity of enterprise-scale identity systems

Privacy concerns surrounding biometric data collection, storage, and potential misuse create regulatory and reputational barriers that limit biometric authentication adoption in jurisdictions with strict biometric privacy legislation. Each Illinois Biometric Information Privacy Act litigation outcome, each GDPR enforcement action for biometric data processing without valid legal basis, and each corporate data breach exposing biometric templates creates market awareness of biometric liability that moderates enterprise biometric deployment decisions in privacy-sensitive jurisdictions.

Enterprise-scale identity and access management implementation complexity creates project delivery risk whose cost overrun and timeline delay exposure moderates the pace of large-scale digital security control deployment. Each enterprise identity system migration whose integration with hundreds of applications, legacy system compatibility, and user migration logistics creates multi-year implementation programmes requires sustained organisational commitment and budget allocation that competes with other digital transformation priorities.

Opportunities: Decentralised identity and passkey authentication creating next-generation platform investment

Decentralised identity using blockchain-based verifiable credentials and self-sovereign identity architectures represents the most commercially transformative emerging market opportunity whose elimination of centralised identity database breach risk and user privacy-preserving design creates enterprise and government adoption motivation. Each jurisdiction that adopts verifiable credential standards for digital identity document issuance creates government-initiated procurement that sustains platform investment beyond enterprise commercial demand cycles.

Passkey and FIDO2 passwordless authentication represents the most commercially accessible near-term market development whose industry-wide adoption by Apple, Google, and Microsoft creates consumer-scale deployment precedent that sustains enterprise procurement for compatible authentication infrastructure. Each enterprise that deploys FIDO2 passkeys across its workforce creates hardware security key, platform authenticator, and identity platform investment that compounds with the enterprise's security architecture maturity progression.

Recent Developments:

-

2024: Microsoft expanded its AI-powered cybersecurity capabilities in 2024 across enterprise cloud platforms, integrating Security Copilot's threat intelligence with biometric multi-factor authentication and zero-trust identity verification across Microsoft Entra and Azure, enabling risk-based conditional access policies that adapt dynamically to real-time threat signals.

-

2024: Thales Group launched its CipherTrust Data Security Platform update in 2024 with enhanced post-quantum cryptography readiness features and expanded hardware security module integration, enabling enterprise customers to begin migrating encryption key management infrastructure toward quantum-safe algorithms in preparation for NIST post-quantum cryptography standard compliance.

-

2025: Fingerprint Cards AB collaborated with jNet Secure in January 2025 to develop a turnkey biometric System-in-Package module for secure digital authentication targeting enterprise access control, financial services, and government identification programmes with a passwordless cryptography-based authentication solution.

-

2023: Thales Group launched an enhanced SafeNet Trusted Access cloud authentication platform in 2023 with expanded biometric authentication support, adaptive risk-based access policies, and passwordless MFA options for enterprise workforce identity management, addressing the enterprise transition toward zero-trust identity architectures.

-

2023: Cisco Systems enhanced its Duo Security multi-factor authentication platform in 2023 with expanded biometric authentication support, continuous identity trust monitoring, and Device Trust capabilities for zero-trust network access, enabling enterprises to enforce least-privilege access across hybrid and multi-cloud environments.

Digital Security Control Market Key Players

-

Thales Group SA

-

HID Global Corporation (ASSA ABLOY)

-

NXP Semiconductors NV

-

Infineon Technologies AG

-

Broadcom Inc. (Symantec)

-

Microsoft Corporation

-

Cisco Systems Inc. (Duo Security)

-

Ping Identity Corporation

-

CyberArk Software Ltd.

-

ForgeRock Inc. (Ping Identity)

-

Giesecke+Devrient GmbH

-

IDEMIA Group

-

Entrust Corporation

-

OneSpan Inc.

-

RSA Security LLC

-

Fingerprint Cards AB

-

Aware Inc.

-

Okta Inc.

-

SailPoint Technologies Inc.

-

BeyondTrust Corporation

Digital Security Control Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.59 Billion |

| Market Size by 2035 | USD 63.24 Billion |

| CAGR | CAGR of 12.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Biometric Technologies, Smart Cards, Digital Signatures, Hardware Security Modules, Others) • by Application (User Authentication, Access Control, Data Encryption, Network Monitoring, Identity Management, Others) • by End User (BFSI, Government and Defence, Healthcare, IT and Telecom, Retail and E-commerce, Energy and Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thales Group SA, HID Global Corporation (ASSA ABLOY), NXP Semiconductors NV, Infineon Technologies AG, Broadcom Inc. (Symantec), Microsoft Corporation, Cisco Systems Inc. (Duo Security), Ping Identity Corporation, CyberArk Software Ltd., ForgeRock Inc. (Ping Identity), Giesecke+Devrient GmbH, IDEMIA Group, Entrust Corporation, OneSpan Inc., RSA Security LLC, Fingerprint Cards AB, Aware Inc., Okta Inc., SailPoint Technologies Inc., BeyondTrust Corporation |

Frequently Asked Questions

The Digital Security Control Market is expected to grow at a CAGR of 12.39% from 2026 to 2035.

The Digital Security Control Market was valued at USD 18.59 Billion in 2025.

Escalating data breach costs creating financial loss exposure that motivates above-average digital security investment, and regulatory authentication mandates including GDPR, eIDAS 2.0, PSD2 strong customer authentication, and HIPAA access control requirements creating non-discretionary compliance-driven procurement across financial services, government, and healthcare end-user sectors.

Biometric Technologies dominated with approximately 56% share in 2025, while Smart Cards is the fastest growing segment driven by digital transaction growth and government identity programme investment.

North America dominated the Digital Security Control Market in 2025, while Asia Pacific is the fastest-growing region driven by China's digital payment authentication scale and India's Aadhaar biometric identity infrastructure.

Get in Touch