Semiconductor Etch Equipment Market Report Scope & Overview:

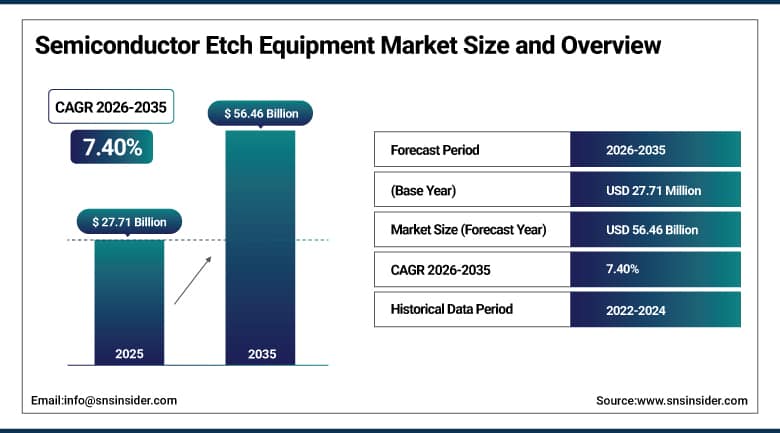

The Semiconductor Etch Equipment Market was valued at USD 27.71 billion in 2025 and is expected to reach USD 56.46 billion by 2035, growing at a CAGR of 7.40% from 2026–2035.

The semiconductor etch equipment market is witnessing substantial growth in the global market due to increasing semiconductor manufacturing investments worldwide. Rising demand for advanced logic chips and memory devices is accelerating equipment adoption across fabrication facilities. Growing deployment of AI, high-performance computing, and 5G technologies is further supporting market expansion. Continuous advancements in 3D NAND and advanced packaging technologies are significantly boosting etching requirements. Expansion of semiconductor foundries and government-backed chip production initiatives is strengthening demand for precision etch equipment globally.

According to U.S. federal semiconductor policy reporting, the U.S. now produces 12% of global semiconductor capacity, down from 37% in 1990, highlighting the strategic need for domestic equipment and etching capability expansion. U.S. legislative developments show increasing scrutiny of advanced cryogenic etch equipment exports, reinforcing the strategic importance of etching tools in national security and semiconductor sovereignty policies

Market Size and Forecast:

-

Market Size 2026E: USD 29.70 billion

-

Market Size 2035: USD 56.46 billion

-

CAGR (2026 - 2035): 7.40%

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Semiconductor Etch Equipment Market - Request Free Sample Report

Semiconductor Etch Equipment Market Trends:

-

Advanced 3D semiconductor architectures are increasing high-aspect-ratio etch demand, with leading-node production investments exceeding USD 100 billion globally.

-

Growing adoption of artificial intelligence processors is accelerating plasma etching requirements for sub-3nm fabrication and advanced packaging applications.

-

Semiconductor manufacturing capacity expansions across Asia-Pacific and North America are driving double-digit procurement growth for etch systems.

-

Sustainability initiatives are promoting energy-efficient etch chambers, reducing process gas consumption by up to 30% across fabs.

-

Increasing deployment of atomic layer etching technologies is enhancing precision, supporting complex device geometries and yield optimization.

-

Government-backed semiconductor incentive programs introduced during 2024–2026 are accelerating domestic fabrication investments and equipment localization efforts.

U.S. Semiconductor Etch Equipment Market Size Outlook:

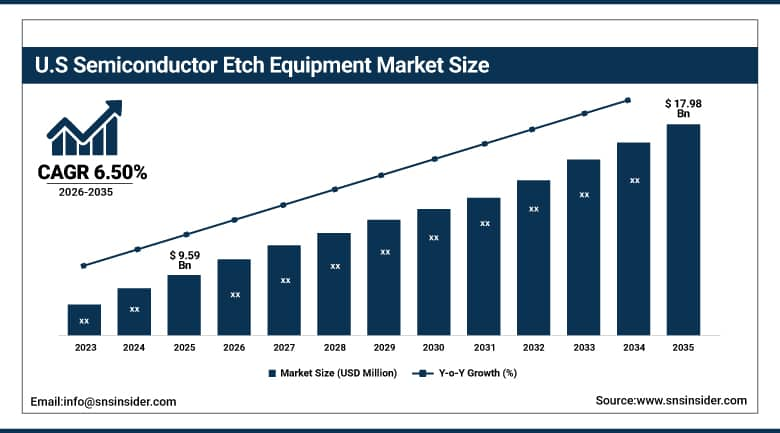

The U.S. Semiconductor Etch Equipment Market was valued at USD 9.59 Billion in 2025 and is expected to reach around USD 17.98 Billion by 2035, growing at a CAGR of 6.50% from 2026–2035.

The U.S. semiconductor etch equipment market is witnessing steady growth because of increasing investments in domestic semiconductor manufacturing facilities. Semiconductor etch equipment adoption across advanced logic, memory, and specialty device production has been responsible for strong market expansion. Increasing funding under semiconductor capacity expansion programs has led to rising demand for precision fabrication equipment. Growing development of AI processors, high-performance computing chips, and advanced packaging technologies is further supporting equipment adoption. Continuous focus on supply chain resilience and next generation semiconductor production is strengthening market growth.

According to the U.S. Department of Commerce, the GAO reports that 40 semiconductor projects across 19 companies were funded as of July 2025, boosting domestic equipment demand. U.S. production capacity is projected to support rising AI, automotive, and defense chip needs through 2030s growth initiatives.

Semiconductor Etch Equipment Market Segment Analysis:

-

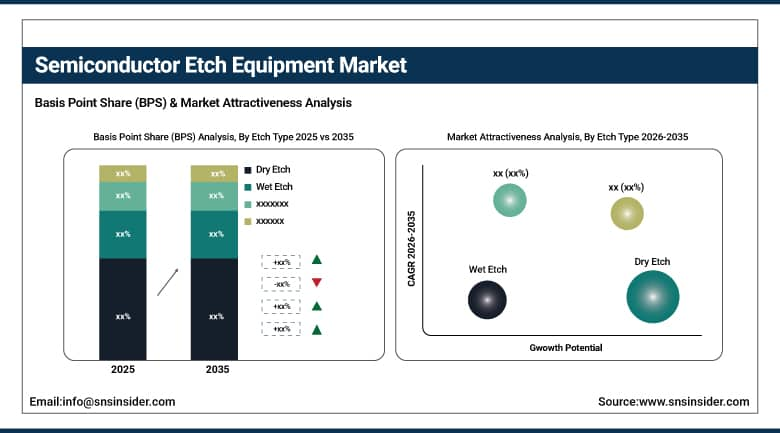

By Etch Type, dry etch dominated the semiconductor etch equipment market with 78.45% share in 2025; while wet etch are the fastest growing segment with CAGR of 8.46% during 2026 to 2035.

-

By Dimension, 2D dominated the semiconductor etch equipment market with 58.35% share in 2025; while 3D is the fastest growing segment with CAGR of 11.03% during 2026 to 2035.

-

By Application, semiconductor fabrication plant/foundry dominated the semiconductor etch equipment market with 62.40% share in 2025; while semiconductor electronics are the fastest growing segment with CAGR of 9.86% during 2026 to 2035.

-

By Wafer Size Compatibility, 300 mm dominated the semiconductor etch equipment market with 64.85% share in 2025; while ≥450 mm is the fastest growing segment with CAGR of 24.75% during 2026 to 2035.

By Etch Type, dry etch dominated the semiconductor etch equipment market, while wet etch is the fastest growing segment.

Dry Etch emerged as the major segment in the Semiconductor Etch Equipment Market, dominated maximum revenue share in 2025. The segment retained its supremacy owing to better precision and significance in the manufacture of semiconductors. Dry etching ensures precise pattern formation in nanotechnology-based semiconductor manufacturing applications. An upsurge in 3D NAND manufacturing and advanced node semiconductors is expected to augment the use of dry etching process further. Compatibility with high volume manufacturing is driving adoption around the world in semiconductor fabs.

The Wet Etch segment is likely to exhibit the fastest growth during 2026-2035. The segment is poised to benefit from increasing usage in specialty semiconductor products and advanced packaging technology. Wet etching is less expensive and provides better selectivity than dry etching. Investments made towards heterogeneous integration and next generation packaging technology are driving growth within the segment. Increasing semiconductor manufacturing capacity and technological advancements offer ample growth prospects for the segment.

By Dimension, 2D dominated the semiconductor etch equipment market, while 3D is the fastest growing segment.

2D etch process accounted for a dominated revenue share in 2025, owing to the large-scale usage of conventional planar semiconductor fabrication technologies in logic and analog semiconductor devices. Many semiconductor fabs used the traditional 2D technology as it had low production complexity and high efficiency. High demand for semiconductor chips for consumer electronics, vehicles, and industrial applications boosted the use of 2D etching equipment.

3D etch process is anticipated to exhibit the fastest CAGR during the forecast period due to the growing usage of 3D NAND memory devices, packaging technologies, and heterogeneous integration. Several semiconductor companies have been making massive investments in high-aspect-ratio etching equipment to develop next-gen semiconductor chips. Growing demand for artificial intelligence, high-performance computing, and data center applications will boost the demand for 3D semiconductor processes.

By Application, semiconductor fabrication plant/foundry dominated the semiconductor etch equipment market, while semiconductor electronics is the fastest growing segment.

Semiconductor Fabrication Plant/Foundry dominated the semiconductor etch equipment market in terms of high revenue share in 2025. The leadership position was largely attributed to the significant installations of etch equipment in large-scale production of semiconductors worldwide. Fabrication plants and foundries utilize the latest technology in etching to produce logic, memory, and specialty semiconductors. Increasing investments in production facilities for fabrication of wafer semiconductors and advanced nodes were also contributing to equipment sales.

Semiconductor Electronics segment is anticipated to register the fastest CAGR during the period from 2026 to 2035. The rapid growth will be driven by increasing demand for consumer electronics, AI-driven devices, and high-performance computing systems worldwide. The advanced semiconductor parts are required in smartphones, data centers, automobiles, and industrial machinery. Increasing usage of 5G-enabled technologies and smart electronic devices will boost the demand for semiconductor chips.

By Wafer Size Compatibility, 300 mm dominated the semiconductor etch equipment market, while ≥450 mm is the fastest growing segment.

The segment of 300 mm held dominated revenue share in the semiconductor etch equipment market in 2025 owing to the popularity of this format in most of the advanced semiconductor manufacturing plants globally. Majority of the leading foundry companies and integrated device manufacturers use 300 mm format for bulk production. The segment offers advantages such as better throughput, low costs of manufacture per chip, and process efficiency along with growing demand for advanced electronics such as AI devices, 5G, and other high-performance computers.

The segment ≥450 mm is likely to witness the fastest CAGR during the forecast period owing to growing interest in large wafer size for advanced semiconductor production in the future. Large wafers help in enhancing output efficiency and lowering the costs of manufacture per chip. Growing research initiatives in next generation fabrication technologies are expected to further drive growth in the segment. Increasing investments towards semiconductor production infrastructure are also contributing positively to the market growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

87.45% |

|

Europe |

Germany |

28.36% |

|

Asia Pacific |

China |

43.78% |

|

Middle East & Africa |

UAE |

17.24% |

|

Latin America |

Brazil |

46.15% |

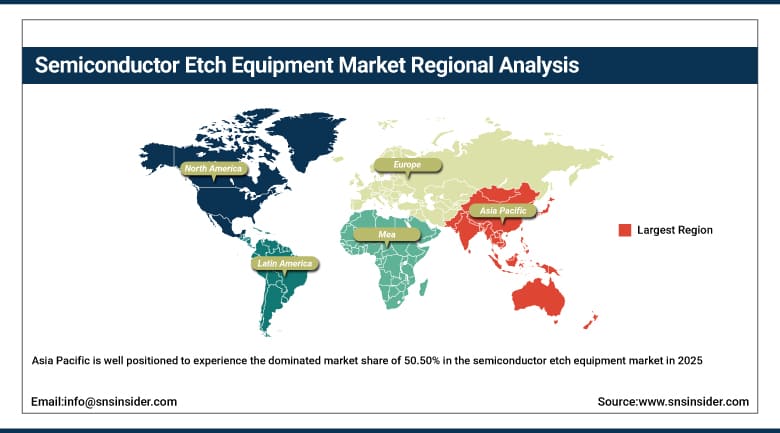

Asia Pacific Semiconductor Etch Equipment Market Insights.

Asia Pacific is well positioned to experience the dominated market share of 50.50% in the semiconductor etch equipment market in 2025 with a highest CAGR due to rapid semiconductor manufacturing expansion and technology investments. China, India, Japan, South Korea, and Taiwan are key contributors. Rising demand for consumer electronics, AI chips, and memory devices is boosting adoption. Expanding foundry capacity and advanced packaging development are further strengthening market growth across the region.

According to Korea’s Ministry of Trade, Industry and Energy, South Korea accounts for about 24.4% of global semiconductor equipment investment. Taiwan’s Ministry of Economic Affairs reports over $100 billion chip manufacturing expansion by 2025, strengthening advanced etch demand for sub-3nm nodes, driven by leading foundries and rapid fab capacity expansion across the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Semiconductor Etch Equipment Market Insights.

North America in semiconductor etch equipment market has seen its fastest growing CAGR of 8.99% in 2025 due to strong semiconductor manufacturing investments and advanced fabrication capabilities. The region benefits from leading chipmakers, cutting edge research activities, and extensive semiconductor equipment deployment. Increasing demand for AI processors, high performance computing chips, and advanced memory devices is driving steady growth across the United States and Canada. Expanding government support and domestic semiconductor production initiatives are further supporting market expansion.

U.S. government data highlights strong expansion in semiconductor manufacturing capacity under the CHIPS and Science Act, which allocates about $50 billion to strengthen domestic semiconductor ecosystems, including fabrication and equipment supply chains. The U.S. hosts over 200,000 semiconductor manufacturing jobs and rising fab investments, reinforcing demand for advanced etch equipment across domestic fabs.

Europe Semiconductor Etch Equipment Market Insights.

The Europe semiconductor etch equipment market makes an important mark in the year 2025 owing to strong semiconductor sovereignty initiatives and technology investments. Countries like Germany, France, United Kingdom, and Italy are leading contributors to regional demand. High focus on automotive semiconductors, industrial electronics, and advanced manufacturing is supporting consistent market expansion. Increasing investments in wafer fabrication facilities and semiconductor research programs are strengthening adoption across industrial and technology sectors.

The European semiconductor etch equipment ecosystem is expanding under the EU Chips Act, which targets raising Europe’s semiconductor share from 10% to 20% by 2030.

According to the European Commission, EU suppliers already contribute about 28% of global semiconductor manufacturing equipment output. These government-backed initiatives strengthen demand for advanced etch tools across European fabs, especially in logic and automotive chip manufacturing.

Middle East & Africa and Latin America Semiconductor Etch Equipment Market Insights.

The Middle East & Africa region along with Latin America will exhibit consistent growth in the semiconductor etch equipment market up till 2025 due to investments in technology infrastructure development. The UAE, Saudi Arabia, South Africa, Brazil, and Mexico will join the list as countries with an emerging market for semiconductor etch equipment. Given that the growing electronics demand, manufacturing sector expansion, and digitalization efforts will increase the use of semiconductor equipment in these regions.

The Ministry of Communications and Information Technology through the National Semiconductor Hub is working to build a full semiconductor value chain by attracting large-scale investments exceeding SAR 1 billion to strengthen domestic chip design and manufacturing capabilities.

According to Brazil’s Ministry of Science, Technology and Innovation, the Brasil Semicon program along with the expansion of CEITEC is enhancing local semiconductor R&D and production capacity, thereby increasing the need for advanced wafer etching technologies across Latin America.

Market Dynamics:

Growth Drivers: Increasing demand for AI processors and advanced semiconductor devices requiring highly precise etching technologies across modern fabrication facilities

Due to the increased use of artificial intelligence, high-performance computing, and improved memory technologies, there is increased manufacture of semiconductors all around the world. There is a growing need for advanced semiconductor device manufacturing because the process of etching needs to be very accurate for making complex devices in small dimensions. There is a growing adoption of AI servers, data centers, and 5G networks that have driven the growth in advanced logic semiconductors. Increased investment by companies in manufacturing plants has resulted in increased manufacture of semiconductors.

According to the European Commission’s European Chips Act framework, Europe targets doubling its global semiconductor production share to 20% by 2030, accelerating investment in cutting-edge fabrication technologies such as advanced etching systems required for sub-5 nm and AI processor manufacturing.

Restraints: Complex process integration challenges and stringent technological requirements increasing operational difficulties across semiconductor manufacturing environments

Semiconductor manufacture with sophisticated technology necessitates complex production processes that require precise control capabilities. The operation of etch equipment needs to be carried out strictly within set specifications in order to attain the required device properties. Installation of new equipment in an existing production line can demand rigorous testing and optimization. Increased complexity of devices is posing further challenges to semiconductor manufacturers throughout the world. Any deviation from the process can pose a serious problem for the entire production process.

Opportunities: Rising development of next generation semiconductor nodes enabling broader deployment of advanced etching equipment worldwide

The shift towards smaller semiconductor process nodes is opening up huge prospects for the adoption of advanced etch equipment. The attention of manufacturers is currently being paid towards making highly advanced chips that have superior performances and energy efficiency. In order to meet the requirements of advanced processes, there needs to be high accuracy in etching technology for meeting complex device structures. Research and development initiatives are gaining pace due to increased investment in semiconductors. Increased demand for advanced semiconductor production technologies is being witnessed among consumers.

According to India’s Ministry of Electronics and IT, the India Semiconductor Mission has approved around $10 billion incentives to strengthen fabrication and packaging ecosystems, supporting advanced manufacturing growth.

Recent Developments:

-

2026: Oxford Instruments plc expanded plasma processing and materials characterization capabilities, supporting compound semiconductors, advanced packaging, quantum technologies, and manufacturing innovation.

-

2025: Tokyo Electron Limited extended its strategic partnership with iMac through a new five-year agreement targeting beyond-2nm semiconductor technologies and advanced patterning.

-

2025: Hitachi High-Tech Corporation strengthened semiconductor equipment capabilities by expanding advanced process control and metrology solutions supporting AI-driven chip production.

-

2024: Corial SAS expanded international engagement for its plasma etching systems supporting research laboratories and specialized semiconductor manufacturers.

Semiconductor Etch Equipment Market Key Players are:

-

Lam Research Corporation

-

Tokyo Electron Limited

-

Applied Materials, Inc.

-

ASM International N.V.

-

Hitachi High-Tech Corporation

-

SCREEN Holdings Co., Ltd.

-

Oxford Instruments plc

-

Plasma-Therm LLC

-

SPTS Technologies Ltd.

-

Advanced Energy Industries, Inc.

-

ULVAC, Inc.

-

Veeco Instruments Inc.

-

NAURA Technology Group Co., Ltd.

-

AMEC

-

Kokusai Electric Corporation

-

Mattson Technology, Inc.

-

Samco Inc.

-

Corial SAS

-

GigaLane Co., Ltd.

-

Jusung Engineering Co., Ltd.

Semiconductor Etch Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.71 Billion |

| Market Size by 2035 | USD 56.46 Billion |

| CAGR | CAGR of 7.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Etch Type (Dry Etch, Wet Etch) • By Dimension (2D, 2.5D, 3D) • By Application (Semiconductor Fabrication Plant/Foundry, Semiconductor Electronics, Test Home) • By Wafer Size Compatibility (≤150 mm, 200 mm, 300 mm, ≥450 mm) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lam Research Corporation, Tokyo Electron Limited, Applied Materials, Inc., ASM International N.V., Hitachi High-Tech Corporation, SCREEN Holdings Co., Ltd., Oxford Instruments plc, Plasma-Therm LLC, SPTS Technologies Ltd., Advanced Energy Industries, Inc., ULVAC, Inc., Veeco Instruments Inc., NAURA Technology Group Co., Ltd., AMEC, Kokusai Electric Corporation, Mattson Technology, Inc., Samco Inc., Corial SAS, GigaLane Co., Ltd., Jusung Engineering Co., Ltd. |

Frequently Asked Questions

The semiconductor etch equipment market is expected to grow at a CAGR of 7.40% from 2026 to 2035.

The semiconductor etch equipment market was valued at USD 27.71 billion in 2025.

Rising demand for AI processors, advanced memory devices, and semiconductor fabrication expansion is driving etch equipment adoption globally.

Dry Etch dominated the market in 2025 due to superior precision, advanced node compatibility, and high-volume manufacturing efficiency.

North America dominated the market in 2025 due to strong semiconductor investments, advanced fabs, and government support.

Get in Touch