High End Semiconductor Packaging Market Report Scope & Overview:

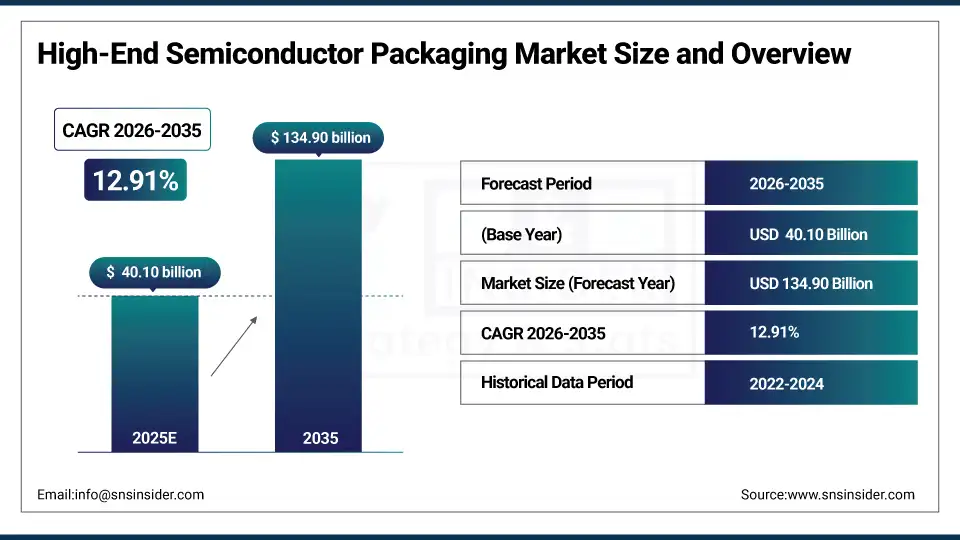

The High-End Semiconductor Packaging Market size was valued at USD 40.10 Billion in 2025 and is projected to reach USD 134.90 Billion by 2035, growing at a CAGR of 12.91% during 2026–2035.

The High-End Semiconductor Packaging Market is witnessing robust growth with the increase in demand for high-performance, miniaturized, and energy-efficient electronic devices. Advanced semiconductor packaging technologies help in the integration of more chips, performance enhancement, and thermal management, as opposed to conventional semiconductor packaging technologies. In addition, the increased demand for artificial intelligence, high-performance computing, 5G infrastructure, and high-end consumer devices is fueling the growth of the High-End Semiconductor Packaging Market. Furthermore, the ongoing innovation in semiconductor packaging materials, chiplet technologies, and heterogeneous integration is helping to increase the performance of semiconductor devices, thus paving the way for the development of the next generation of electronic systems and complex ICs.

High End Semiconductor Packaging Market Size and Forecast:

-

Market Size in 2025: USD 40.10 Billion

-

Market Size by 2035: USD 134.90 Billion

-

CAGR: 12.91% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On High-End Semiconductor Packaging Market - Request Free Sample Report

High End Semiconductor Packaging Market Key Trends:

-

Growing adoption of 3D IC and 2.5D advanced packaging technologies to support high-performance computing and AI processors.

-

Increasing use of chiplet-based architectures enabling better performance, scalability, and cost efficiency in next-generation semiconductor designs.

-

Rising demand for fan-out wafer-level packaging (FOWLP) in smartphones, wearable devices, and compact consumer electronics.

-

Expansion of advanced semiconductor packaging facilities by leading OSAT and semiconductor companies to meet growing global chip demand.

-

Increasing integration of semiconductor packaging with automotive electronics and EV technologies, driven by the growth of ADAS and autonomous driving systems.

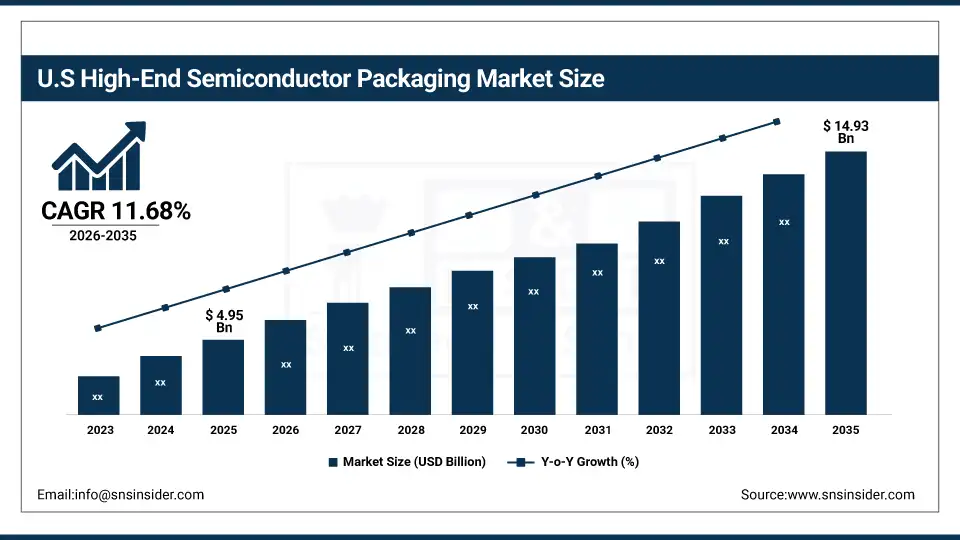

The U.S. High End Semiconductor Packaging Market is valued at USD 4.95 Billion in 2025 and is expected to reach USD 14.93 Billion in 2035, growing at a CAGR of 11.68% from 2026 to 2035. This growth is due to the increasing demand for AI processor chips, high-performance computing, data center infrastructure, high-end consumer products, along with increasing investments in domestic semiconductor manufacturing, which is backed by the US CHIPS Act.

High End Semiconductor Packaging Market Key Drivers:

-

Growing demand for AI, high-performance computing, and advanced consumer electronics

The major growth driver of the High-End Semiconductor Packaging market is the high growth rate of AI, 5G, data centers, and high-performance computing applications, which require advanced semiconductor packages for greater integration, performance, and thermal management. The semiconductor industry is increasingly using technologies such as 3D IC, fan-out wafer-level packaging, system-in-package (SiP), and others to support the miniaturization and increased chip functionality of various products in the consumer electronics, automotive, and telecom markets.

High End Semiconductor Packaging Market Key Restraints:

-

High manufacturing costs and technological complexity

One of the challenges facing the market is the high level of capital investment that is required to support the development of sophisticated packaging technologies, materials, and manufacturing tools. The level of sophistication that is involved in the development of multi-chip packages could also pose a challenge to the market. In addition, the need for highly skilled engineers could pose a challenge to the market, especially to small semiconductor companies.

High End Semiconductor Packaging Market Key Opportunities:

-

Increasing adoption of chiplet architectures and heterogeneous integration

There are tremendous opportunities available in the market with the rise of chiplet-based architecture, AI accelerators, advanced automotive, and next-generation communication solutions. With the advancements in 2.5D and 3D chip stacking, fan-out wafer-level packaging, system-in-packages, chip performance, and power efficiency, new opportunities are being created in the market. With government investments in semiconductor manufacturing, new opportunities are being created in the market for advanced semiconductor packaging solutions.

High End Semiconductor Packaging Market Segments Analysis:

-

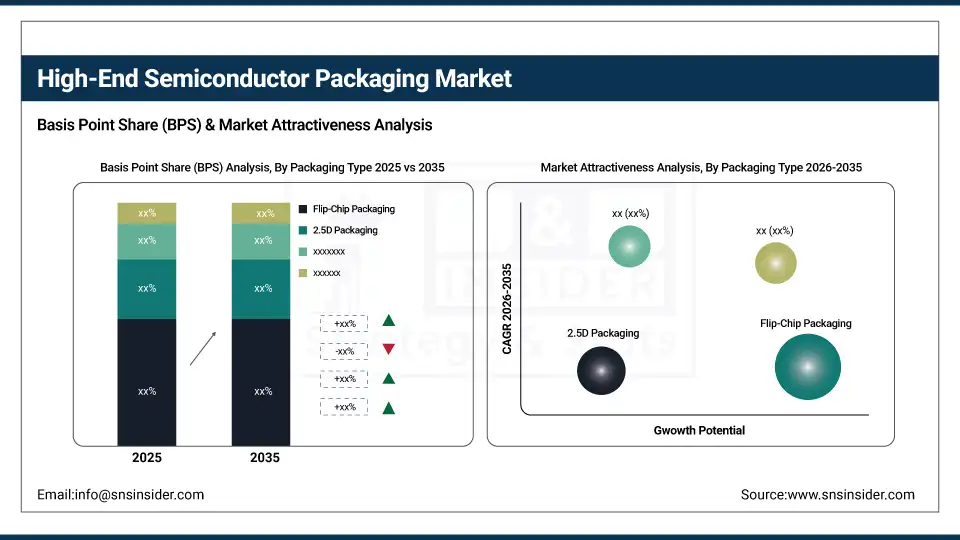

By Packaging Type: In 2025, Flip-Chip Packaging dominated with 32% share; 3D Packaging fastest growing segment during 2026-2035

-

By Material: In 2025, Organic Substrates dominated with 39% share; Die-Attach Materials fastest growing segment during 2026-2035

-

By Application: In 2025, Consumer Electronics dominated with 41% share; Automotive Electronics fastest growing segment during 2026-2035

-

By End-User: In 2025, Outsourced Semiconductor Assembly and Test (OSAT) Companies dominated with 55% share; Foundries fastest growing segment during 2026-2035

By Packaging Type: Flip-Chip Packaging Dominates, 3D Packaging Fastest-Growing

Flip-chip packaging leads the packaging type segment, holding a share of approximately 32%, owing to its high I/O density, better electrical performance, and thermal management capabilities.

The 3D packaging segment is increasing at the highest rate due to the increasing demand for AI processors, high-performance computing, and advanced data center chips.

By Material: Organic Substrates Dominate, Die-Attach Materials Fastest-Growing

Organic substrates are the largest segment in the material segment, accounting for approximately 39%. This is because organic substrates offer excellent electrical connectivity, thermal stability, and support for complex semiconductor package structures.

Die attach materials are the fastest-growing segment because of the increasing need for improved thermal conductivity, reliability, and performance in advanced semiconductor package structures.

By Application: Consumer Electronics Dominate, Automotive Electronics Fastest-Growing

Consumer electronics segment is the largest in the application segment, with a market share of approximately 41%, driven by the increased demand for smartphones, tablets, and other portable electronic devices, which have high demands for semiconductor packaging technologies.

Automotive electronics is the fastest-growing application segment, driven by the growing demand for electric vehicles, advanced driver assistance systems, and autonomous driving technologies.

By End-User: OSAT Companies Dominate, Foundries Fastest-Growing

Outsourced Semiconductor Assembly and Test (OSAT) companies dominate the end-user segment, accounting for about 55% of the market share. They specialize in semiconductor packaging and testing services and are a vital ally for semiconductor manufacturers worldwide.

Foundries are the fastest-growing segment as semiconductor manufacturers increasingly integrate advanced packaging technologies with wafer fabrication processes to improve chip performance and reduce production complexity

High End Semiconductor Packaging Market Regional Analysis:

Asia-Pacific High End Semiconductor Packaging Market Insights:

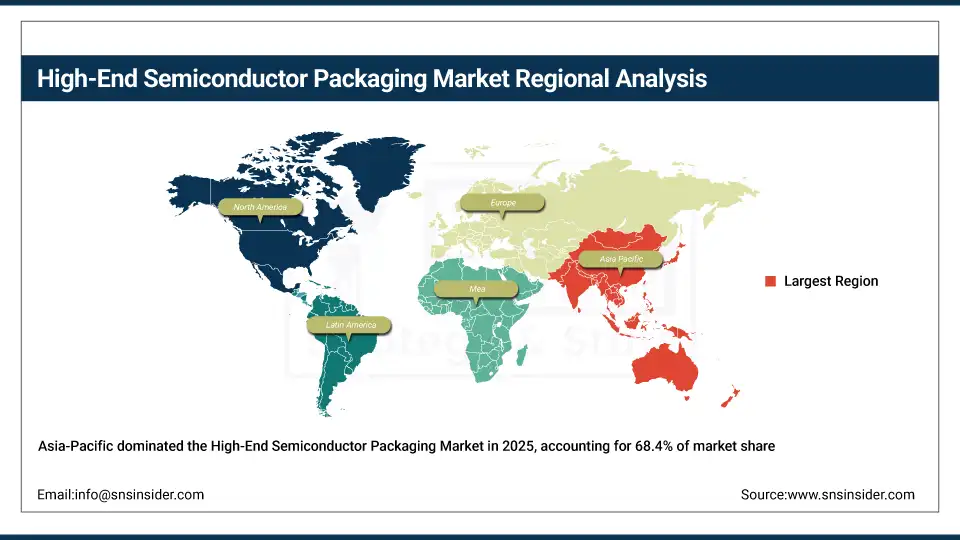

Asia-Pacific leads the High-End Semiconductor Packaging Market in terms of market share, which accounts for about 68.4% of the overall market in 2025. This region is also expected to grow the fastest in the High-End Semiconductor Packaging Market, with a CAGR of 13.77% during the forecast period. This is because of the presence of strong semiconductor manufacturing infrastructure in Taiwan, South Korea, China, and Japan, along with the presence of key OSAT players and the growing need for AI chip-based solutions, 5G devices, high-end computing solutions, and automotive electronics. The investments in advanced semiconductor packaging technologies like 2.5D/3D IC, FOWLP, and SiP are also fueling the Asia-Pacific High-End Semiconductor Packaging Market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America High End Semiconductor Packaging Market Insights:

North American region also presents another major market opportunity for high-end semiconductor packaging, considering the high demand for high-end semiconductor devices for various applications, including AI, high-performance computing, data centers, 5G infrastructure, automotive, etc. Moreover, the region also hosts several semiconductor companies, including Intel, AMD, Texas Instruments, etc. In addition, the region also invests heavily in the development of advanced semiconductor packaging technologies, semiconductor manufacturing facilities, etc. Government initiatives for the domestic semiconductor industry have also helped the growth of high-end semiconductor packaging, including advanced semiconductor packaging technologies such as 2.5D/3D integration, chiplets, system-in-package, etc.

Europe High End Semiconductor Packaging Insights:

Europe is a significant contributor to the High-End Semiconductor Packaging Market due to the demand for semiconductor devices in the automotive, industrial automation, telecommunications, and aerospace sectors. In addition, the region is driven by the presence of major semiconductor players, such as Infineon Technologies, STMicroelectronics, and NXP Semiconductors, which are investing heavily in the development of semiconductor devices in order to improve the overall performance of the devices while maintaining the energy efficiency of the chips. In addition, the presence of electric vehicles, ADAS, and smart manufacturing is creating a high demand for high-end semiconductor devices in the region.

Latin America High End Semiconductor Packaging Market Insights:

Latin America is an emerging market driven by expanding electronics manufacturing, automotive production, and telecommunications infrastructure. Countries such as Brazil and Mexico are increasing semiconductor adoption, while partnerships with global companies and growing digitalization are supporting gradual demand for advanced semiconductor packaging solutions.

Middle East & Africa (MEA) High End Semiconductor Packaging Market Insights:

The Middle East & Africa market is gradually emerging, supported by growing investments in electronics manufacturing, telecommunications infrastructure, and digital transformation initiatives. Increasing demand for consumer electronics, smart devices, and industrial automation technologies is encouraging the adoption of advanced semiconductor components and packaging solutions across the region. Expanding technology hubs in countries such as the UAE, Saudi Arabia, and South Africa are further contributing to market development and strengthening regional participation in the global semiconductor ecosystem.

High End Semiconductor Packaging Market Competitive Landscape:

ASE Technology Holding Co., Ltd. is a Taiwanese company that was established in 1984. It is engaged in the business of semiconductor assembly, testing, and packaging. ASE Technology provides system-in-package, fan-out wafer-level packaging, and advanced IC packaging services for the global market, including the automotive, telecommunications, high-performance computing, and consumer sectors.

-

In May 2024, ASE expanded its advanced packaging capacity for AI and high-performance computing chips, strengthening support for next-generation processors used in data centers, 5G infrastructure, and automotive electronics.

Amkor Technology, Inc. is a US-based company founded in 1968, specializing in semiconductor packaging and test services. The company offers flip-chip, wafer-level packaging, system-in-package (SiP), and advanced packaging solutions for mobile devices, automotive electronics, AI processors, and networking applications globally.

-

In April 2024, Amkor announced expansion of its advanced packaging facility to support increasing demand for AI, high-performance computing, and automotive semiconductor applications, enhancing production capacity and technological capabilities.

High End Semiconductor Packaging Companies are:

-

ASE Technology Holding Co., Ltd

-

Amkor Technology

-

JCET Group Co., Ltd.

-

Siliconware Precision Industries Co., Ltd. (SPIL)

-

Powertech Technology Inc (PTI)

-

Tongfu Microelectronics Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Texas Instruments Incorporated

-

STMicroelectronics N.V.

-

Infineon Technologies AG

-

UTAC Holdings Ltd.

-

ChipMOS Technologies Inc.

-

Hana Micron Inc.

-

Nepes Corporation

-

Unisem Group

-

Signetics Corporation

-

Advanced Micro Devices, Inc. (AMD)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 40.10 Billion |

| Market Size by 2035 | USD 134.90 Billion |

| CAGR | CAGR of 12.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Packaging Type: (Flip-Chip Packaging, 2.5D Packaging, 3D Packaging, Fan-Out Wafer-Level Packaging (FOWLP), System-in-Package (SiP)) • By Material: (Organic Substrates, Bonding Wires, Leadframes, Encapsulation Resins, Die-Attach Materials) • By Application: (Consumer Electronics, Automotive Electronics, Telecommunications & Networking, Healthcare & Medical Devices, Industrial Electronics) • By End User: (Outsourced Semiconductor Assembly and Test (OSAT) Companies, Integrated Device Manufacturers (IDMs), Foundries) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ASE Technology Holding Co., Ltd., Amkor Technology, Inc., Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, JCET Group Co., Ltd., Siliconware Precision Industries Co., Ltd. (SPIL), Powertech Technology Inc. (PTI), Tongfu Microelectronics Co., Ltd., Samsung Electronics Co., Ltd., SK Hynix Inc., Texas Instruments Incorporated, STMicroelectronics N.V., Infineon Technologies AG, UTAC Holdings Ltd., ChipMOS Technologies Inc., Hana Micron Inc., Nepes Corporation, Unisem Group, Signetics Corporation, Advanced Micro Devices, Inc. (AMD) |

Frequently Asked Questions

The High End Semiconductor Packaging Market is expected to grow at a CAGR of 12.91% during 2026–2035.

The market was valued at USD 40.10 Billion in 2025 and is projected to reach USD 134.90 Billion by 2035.

The key drivers of the High End Semiconductor Packaging Market include rising demand for AI and high-performance computing, 5G expansion, miniaturization of electronics, increasing semiconductor complexity, growth in automotive electronics, and adoption of heterogeneous integration technologies.

The Flip-Chip Packaging segment dominated during the projected period.

Asia-Pacific dominated the High End Semiconductor Packaging Market in 2025.

Get in Touch