Semiconductor Metrology and Inspection Equipment Market Size:

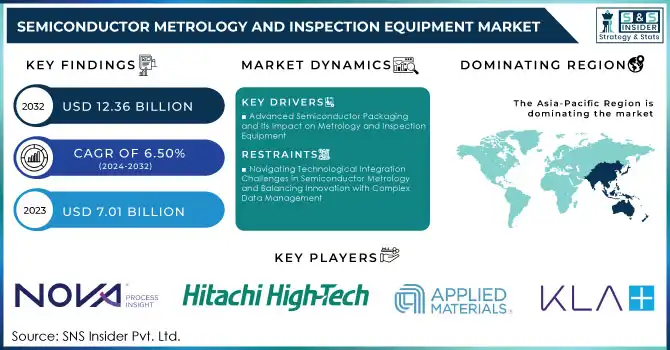

The Semiconductor Metrology and Inspection Equipment Market size was valued at USD 7.46 billion in 2024 and is expected to grow to USD 12.36 billion by 2032 and grow at a CAGR of 6.50 % over the forecast period of 2025-2032. Semiconductor metrology and inspection are integral to the semiconductor manufacturing process, which involves 400 to 600 steps and takes one to two months to complete. Any flaws detected late in the process can lead to the loss of all efforts in subsequent stages. Effective metrology and inspection are essential for ensuring a high yield and optimal quality. These procedures are implemented at critical stages of production to assess thin films, line widths, pattern defects, and other issues, minimizing costly downtime and maintaining high efficiency. The use of advanced UV light sources in semiconductor inspection is vital for reducing inspection times and improving pattern evaluation accuracy. As the semiconductor industry strives for more compact and high-performance integrated circuits, metrology becomes even more crucial.

Get More Information on Semiconductor Metrology and Inspection Equipment Market - Request Sample Report

Companies like TSMC, Infineon, Qualcomm, and Intel are increasing their chip production investments, driving up demand for metrology tools and services. The rise of smartphones, consumer electronics, automotive applications, and IoT devices, particularly with the advent of 5G networks, further fuels the demand for semiconductor materials. The GSMA projects that 5G mobile broadband connections will reach 1.1 billion by 2025, broadening the scope for semiconductor applications across industries. To stay competitive, semiconductor vendors are forming strategic partnerships to develop multifunctional inspection platforms. For example, k-Space Associates introduced the kSA XRF metrology tool, designed to measure thin film thickness with precision.

Key Semiconductor Metrology and Inspection Equipment Market Trends:

-

The adoption of 3D stacking and system-in-package (SiP) solutions is accelerating to overcome limitations of traditional chip designs.

-

Semiconductor metrology tools are evolving to deliver ultra-precise defect detection in complex multi-die packaging structures.

-

Automotive and 5G applications are driving higher demand for reliable, compact, and high-performance semiconductor devices.

-

Advanced packaging technologies like 2.5D and 3D integration are becoming critical for AI, IoT, and autonomous vehicle applications.

-

The industry is shifting toward high-resolution, high-speed inspection systems to ensure performance and reliability in advanced semiconductor packaging.

Semiconductor Metrology and Inspection Equipment Market Growth Drivers:

-

Advanced Semiconductor Packaging and Its Impact on Metrology and Inspection Equipment

The growing demand for advanced semiconductor packaging methods, such as 3D stacking and system-in-package (SiP) solutions, is driving the expansion of the semiconductor metrology and inspection equipment market. As the industry pushes to develop more compact and powerful devices, advanced packaging techniques play a crucial role in addressing the limits of traditional chip manufacturing. With increasing complexity in designs, particularly in automotive and 5G applications, packaging technologies such as 2.5D and 3D integration are becoming essential to meet the growing demand for smaller, faster, and more efficient semiconductor devices. These advanced packaging methods, which involve stacking multiple dies or chips to increase interconnect density and reduce signal paths, require highly specialized metrology tools. These tools must deliver ultra-precise measurements to detect defects in stacked chips, voids, or delamination at a micrometer level. In sectors like automotive, where semiconductor reliability is crucial for safety, the need for such high-resolution inspection is more important than ever. Advanced packaging offers a solution by combining multiple chips into a single package, thus addressing the limitations of traditional packaging. With applications in AI, IoT, and autonomous vehicles, the need for low-power, high-performance chips is escalating.

Semiconductor Metrology and Inspection Equipment Market Restraints:

-

Navigating Technological Integration Challenges in Semiconductor Metrology and Balancing Innovation with Complex Data Management

A major restraint in the semiconductor metrology and inspection equipment market stems from the challenges associated with integrating a range of advanced metrology tools—optical, X-ray, and electron microscopes—each with distinct calibration and data output requirements. These tools must be synchronized to ensure accurate and consistent defect detection across varying scales, but achieving this integration is complicated by the complexity of aligning different hardware, software, and operator processes. Additionally, the vast amount of data generated by these systems often overwhelms traditional processing pipelines, necessitating advanced, real-time software solutions to effectively manage and analyze the data. Without seamless integration, the risk of delays, errors, and inefficiencies increases, ultimately driving up costs and slowing down market innovation.

Semiconductor Metrology and Inspection Equipment Market Segment Analysis:

By Type

In 2024, the lithography metrology segment dominates the semiconductor metrology and inspection equipment market, of around 41% of total revenue. This leadership is due to its crucial role in supporting advanced manufacturing processes like node miniaturization and producing larger wafer sizes. Lithography metrology tools, such as Critical Dimension Scanning Electron Microscopes (CD-SEMs), ensure the precision and accuracy required for wafer patterning, essential for ultra-large-scale integrated circuits. The segment’s growth is fueled by increasing demand for high-performance semiconductor devices, particularly in AI, 5G, and consumer electronics. Major companies like ASML and KLA continue to lead the segment, pushing advancements in defect detection and mask optimization to strengthen their market position further.

Semiconductor Metrology and Inspection Equipment Market Regional Analysis:

Asia Pacific Semiconductor Metrology and Inspection Equipment Market Insights

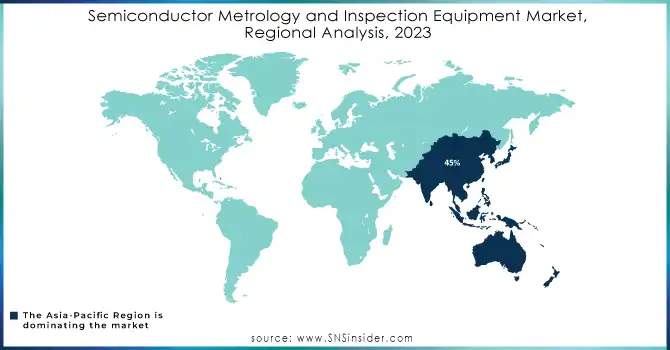

In 2024, the Asia-Pacific region held a dominant share of around 45% in the semiconductor metrology and inspection equipment market, driven by the robust growth of semiconductor manufacturing in Taiwan, South Korea, China, and Japan. Taiwan, with TSMC as a key player, has driven demand for advanced metrology tools due to investments in EUV lithography and 3D packaging. South Korea's semiconductor giants, Samsung and SK Hynix, continue to invest in next-gen technologies like DRAM and NAND flash, fueling the demand for wafer inspection and defect detection. China's push for self-reliance in semiconductor production further accelerates the need for advanced metrology systems. Japan remains a leader in precision equipment, with companies like Tokyo Electron and Nikon at the forefront.

North America Semiconductor Metrology and Inspection Equipment Market Insights

In 2024, North America emerged as the fastest-growing region in the semiconductor metrology and inspection equipment market, driven by significant advancements in semiconductor manufacturing and technological innovation. The United States, with key players like Intel, Micron, and GlobalFoundries, has been at the forefront of expanding semiconductor operations. Intel’s investments in next-gen technologies, including advanced process nodes and 3D packaging, have boosted demand for precise metrology tools. Additionally, the U.S. government's CHIPS Act, which supports domestic semiconductor manufacturing, further accelerates growth. Micron’s advancements in memory chips and the rise of AI and 5G technologies also contribute to the region's robust demand for inspection systems. These factors position North America as a leader in semiconductor metrology, sustaining rapid growth.

Europe Semiconductor Metrology and Inspection Equipment Market Insights

The Europe semiconductor metrology and inspection equipment market is growing steadily, driven by rising demand for advanced chips in automotive, industrial automation, and 5G infrastructure. With Europe’s strong semiconductor ecosystem and focus on precision manufacturing, adoption of advanced inspection tools is increasing. Investments in R&D, particularly in Germany and the Netherlands, further accelerate technological advancements and market expansion.

Latin America (LATAM) and Middle East & Africa (MEA) Semiconductor Metrology and Inspection Equipment Market Insights

The Latin America and Middle East & Africa semiconductor metrology and inspection equipment market is emerging, supported by growing demand for electronics, automotive, and telecom applications. While semiconductor manufacturing capacity is limited, rising adoption of IoT, AI, and 5G technologies fuels equipment demand. Government initiatives and foreign investments are gradually enhancing regional capabilities, creating opportunities for metrology and inspection solutions.

Need Any Customization Research On Semiconductor Metrology and Inspection Equipment Market - Inquiry Now

Semiconductor Metrology and Inspection Equipment Companies are:

-

Applied Materials, Inc.

-

Hitachi High-Tech Corporation

-

Nova Measuring Instruments Ltd.

-

Rudolph Technologies, Inc.

-

Thermo Fisher Scientific Inc.

-

Carl Zeiss AG

-

Nikon Corporation

-

Onto Innovation Inc.

-

Bruker Corporation

-

Advantest Corporation

-

SCREEN Holdings Co., Ltd.

-

Camtek Ltd.

-

Tokyo Electron Limited

-

Lam Research Corporation

-

ASM International N.V.

-

Fujifilm Holdings Corporation

-

Keysight Technologies, Inc.

-

Qualcomm

-

TSMC

-

Infineon Technologies

Competitive Landscape for Semiconductor Metrology and Inspection Equipment Market:

Hitachi High-Tech Corporation plays a vital role in the semiconductor metrology and inspection equipment market, offering advanced solutions such as scanning electron microscope (SEM)-based systems and defect review tools. The company focuses on enabling precise measurement and defect detection at nanometer scales, supporting next-generation semiconductor manufacturing. With strong R&D capabilities and global presence, Hitachi High-Tech drives innovation in process control, helping manufacturers meet the demands of miniaturization, 5G, automotive, and AI-driven applications.

-

March 14-Hitachi High-Tech launches the LS9300AD wafer surface inspection system, offering high-sensitivity detection of low-aspect microscopic defects on both front and backside wafer surfaces. Equipped with a new Differential Interference Contrast (DIC) optical system, it improves yield and reduces inspection costs by enabling high-throughput detection of shallow, irregular defects.

KLA Corporation is a global leader in semiconductor metrology and inspection equipment, providing advanced process control, yield management, and defect detection solutions. Its comprehensive portfolio includes wafer inspection, metrology, and data analytics tools that enable manufacturers to optimize production efficiency and ensure device reliability. KLA’s innovations support critical applications in advanced packaging, 5G, AI, and automotive semiconductors, making it a key player in addressing scaling challenges in next-generation chip manufacturing.

-

Nov 8, 2023, KLA Instruments expands its metrology portfolio with new systems including the Filmetrics® R54-300 for 300mm wafer sheet resistance mapping and the F54-XYT-300 and F60-c film thickness mapping systems, offering enhanced process optimization and automated, high-speed wafer measurement.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.46 Billion |

| Market Size by 2032 | USD 12.36 Billion |

| CAGR | CAGR of 6.50% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Lithography Metrology, Wafer Inspection, Thin Film Metrology, Other Process Control Systems) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | KLA Corporation, Applied Materials, Inc., Hitachi High-Tech Corporation, ASML Holding N.V., Nova Measuring Instruments Ltd., Nanometrics Incorporated, Rudolph Technologies, Inc., Thermo Fisher Scientific Inc., Carl Zeiss AG, Nikon Corporation, Onto Innovation Inc., Bruker Corporation, Advantest Corporation, SCREEN Holdings Co., Ltd., Camtek Ltd., Tokyo Electron Limited, Lam Research Corporation, ASM International N.V., Fujifilm Holdings Corporation, Keysight Technologies, Inc. |

Frequently Asked Questions

KLA Corporation, Applied Materials, Hitachi High-Tech, ASML Holding, Nova Measuring Instruments, Nanometrics, Rudolph Technologies, Thermo Fisher Scientific, Carl Zeiss, Nikon, Onto Innovation, Bruker Corporation, Advantest, SCREEN Holdings, Camtek, Tokyo Electron, Lam Research, ASM International, Fujifilm Holdings, Keysight Technologies, Qualcomm, TSMC, and Infineon Technologies.

Lithography Metrology is dominating in Semiconductor Metrology and Inspection Equipment Market in 2023.

Asia-Pacific is dominating in Semiconductor Metrology and Inspection Equipment Market in 2023.

The Semiconductor Metrology and Inspection Equipment Market size was valued at USD 7.46 billion in 2024 and is expected to grow to USD 12.36 billion by 2032.

The Compound Annual Growth rate for Semiconductor Metrology and Inspection Equipment Market over the forecast period is 6.50%.

Get in Touch