Silicon IGBT Market Report Scope & Overview:

The Silicon IGBT Market was valued at USD 4.11 billion in 2025E and is expected to reach USD 9.22 billion by 2033, growing at a CAGR of 10.76% from 2026-2033.

The Silicon IGBT market is growing due to rising demand for efficient power electronics across electric vehicles, renewable energy systems, and industrial automation. Increasing EV adoption requires high-performance power switching devices, while expanding solar and wind installations rely on IGBTs for reliable energy conversion. Additionally, the shift toward smart grids and advanced motor drives boosts usage. Ongoing technological improvements in efficiency, thermal performance, and cost optimization further accelerate market expansion.

According to the U.S. Department of Energy, widespread adoption of energy-efficient technologies including silicon IGBTs could generate up to USD 2 trillion in electricity-cost savings by 2030, highlighting their strategic importance in the global energy transition.

Silicon IGBT Market Size and Forecast

-

Silicon IGBT Market Size in 2025: USD 4.11 Billion

-

Silicon IGBT Market Size by 2033: USD 9.22 Billion

-

CAGR: 10.76% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Silicon IGBT Market - Request Free Sample Report

Silicon IGBT Market Trends

-

Rising adoption in electric vehicles (EVs) to improve power efficiency and driving range.

-

Growing use in renewable energy systems, especially solar inverters and wind converters.

-

Shift toward high-voltage and high-power IGBTs for industrial and grid applications.

-

Increasing integration of IGBT modules over discrete components for better thermal and electrical performance.

-

Advancements in packaging technologies, such as silicon carbide (SiC) co-packaged modules.

-

Demand for energy-efficient motor drives in manufacturing and automation sectors.

-

Expansion of smart grids and power infrastructure requiring reliable switching devices.

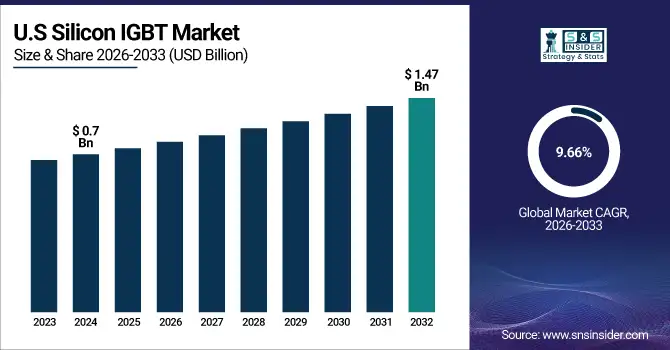

U.S. Silicon IGBT Market was valued at USD 0.7 billion in 2025E and is expected to reach USD 1.47 billion by 2033, growing at a CAGR of 9.66% from 2026-2033.

The U.S. Silicon IGBT market is growing due to rising EV production, increased investment in renewable energy, and expanding industrial automation. Demand for efficient power management solutions and upgrades to grid infrastructure further support market expansion.

Silicon IGBT Market Growth Drivers:

-

Rapid surge in electric vehicle adoption increasing the need for high-efficiency power switching solutions across traction inverters and charging systems

The rapid surge in electric vehicle adoption is significantly increasing demand for high-efficiency power switching solutions, making silicon IGBTs essential for traction inverters, onboard chargers, and power management units. As automakers expand EV production and governments strengthen emission regulations, the requirement for reliable, thermally efficient, and cost-effective semiconductor components continues to rise. Silicon IGBTs offer the ideal balance of performance and affordability, enabling smoother acceleration, optimized battery usage, and improved overall vehicle efficiency. Their ability to handle higher voltages and currents positions them as a critical component supporting the global shift toward large-scale electrified transportation systems.

More than 1 in 5 new cars sold globally in 2024 are estimated to be electric, reflecting rapid EV market expansion and rising demand for high-efficiency power devices.

To align with the IEA’s Net Zero Emissions by 2050 pathway, electric car sales must grow around 23% annually from 2024–2030, signaling sustained long-term demand for advanced power electronics such as silicon IGBTs.

-

Accelerating deployment of renewable energy infrastructure driving the need for stable and efficient power conversion technologies

The accelerating deployment of renewable energy infrastructure, particularly solar and wind installations, is boosting demand for stable and efficient power conversion technologies, making silicon IGBTs crucial for inverter and converter systems. Their capability to deliver high reliability, low switching losses, and effective thermal management ensures uninterrupted power flow in fluctuating energy environments. As nations target aggressive clean-energy goals, the integration of large-scale renewable plants requires advanced semiconductor devices that can handle high voltages and harsh operating conditions. Silicon IGBTs provide the performance foundation needed to maximize energy conversion efficiency and support grid-level stability across expanding renewable networks.

|

Region |

Renewable Capacity Additions 2025 |

Key Details |

Share/Targets |

|

United States |

63 GW new utility-scale capacity |

Solar + battery storage = 81% of additions; Solar alone 32.5 GW (half from Texas & California) |

Renewables ~26% electricity now; >40% by 2030 |

|

Europe (EU) |

89 GW new renewable capacity |

70 GW solar, 19 GW wind; record addition aiming to cut gas imports & meet 2030 goals |

65.5 GW solar + 12.9 GW wind added in 2024 |

|

China |

~400 GW total planned renewable additions in 2025 |

210 GW solar added in 1H 2025; 290 GW new capacity early 2025 (solar + wind) |

Total 3.9 TW installed capacity by end 2025 |

|

Japan |

3.1 GW renewable capacity additions in 2023 |

Solar now ~10% electricity; needs 25-38 GW more solar by 2030; renewable curtailments rising |

Plans fivefold solar increase by 2050 |

Silicon IGBT Market Restraints:

-

Increasing competition from wide-bandgap technologies reducing the long-term growth potential for traditional silicon-based power devices

Increasing competition from wide-bandgap technologies such as silicon carbide and gallium nitride is reducing the long-term growth potential for traditional silicon-based power devices. These next-generation materials offer superior switching speeds, higher temperature tolerance, and better overall efficiency, making them attractive for advanced EVs, fast chargers, and high-power renewable systems. As prices gradually decline and manufacturing scales up, industries may transition from silicon IGBTs to SiC or GaN solutions. This technological shift creates a competitive restraint, limiting the adoption of silicon IGBTs in high-performance applications and challenging manufacturers to justify their relevance in evolving power-electronics markets.

Despite current higher manufacturing costs impacting mass adoption for about 37% of companies, declining costs and scaling production are rapidly narrowing the gap, making WBG devices increasingly accessible and competitive versus traditional silicon IGBTs.

SiC and GaN adoption in EV inverters, fast chargers, and solar systems reduces demand for silicon IGBTs, pressuring manufacturers to upgrade efficiency and shift toward WBG technologies to stay competitive.

Silicon IGBT Market Opportunities:

-

Growing demand for smart grids and energy-efficient industrial systems creating significant scope for advanced power semiconductor integration

Growing demand for smart grids and energy-efficient industrial systems is creating significant scope for advanced power semiconductor integration, positioning silicon IGBTs as vital components for future infrastructure upgrades. As utilities modernize transmission networks and industries adopt intelligent motor drives and automation technologies, the need for reliable, high-capacity power switching devices increases. Silicon IGBTs support improved system stability, reduced energy losses, and enhanced operational efficiency. Furthermore, the transition toward digitalized grid management and predictive maintenance opens new pathways for the incorporation of optimized IGBT modules, enabling smarter, more resilient energy ecosystems capable of supporting rising electrical loads.

Technological improvements such as triple-gate drive IGBTs lower turn-on losses by 66% and turn-off losses by 35% compared to conventional devices, significantly reducing energy dissipation and boosting operational efficiency.

Predictive maintenance for IGBT systems cuts unplanned downtime by up to 30% and maintenance costs by about 15%, enabling condition-based actions that improve operational efficiency and extend equipment life in grids and renewables.

-

Expansion of electric mobility infrastructure and fast-charging networks offering new avenues for high-performance power conversion solutions

Expansion of electric mobility infrastructure and fast-charging networks is offering new avenues for high-performance power conversion solutions that rely on silicon IGBTs. As cities deploy rapid-charging stations and commercial fleets electrify, the demand for robust semiconductor devices capable of handling high voltages and continuous operation grows. Silicon IGBTs ensure stable current flow, reduced heat generation, and efficient power management, making them ideal for demanding charging environments. The proliferation of e-buses, delivery EVs, and long-range passenger vehicles further increases the need for scalable, efficient, and cost-effective power electronics, opening substantial opportunity for IGBT-based technologies.

Silicon IGBT Market Segment Highlights

-

By End-Use Industry: In 2025, Industrial Equipment led the market with share 36%, while Automotive is the fastest-growing segment with the highest CAGR (2026–2033).

-

By Application: In 2025, Motor Drives led the market with share 32%, while Electric Vehicles is the fastest-growing segment with the highest CAGR (2026–2033).

-

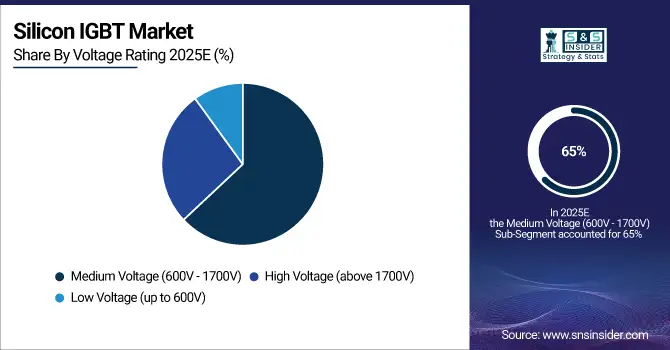

By Voltage Rating: In 2025, Medium Voltage (600V–1700V) led the market with share 65%, while High Voltage (above 1700V) is the fastest-growing segment with the highest CAGR (2026–2033).

-

By Technology: In 2025, Standard IGBT Technology led the market with share 50%, while High-Speed IGBT Technology is the fastest-growing segment with the highest CAGR (2026–2033).

-

By Packaging Type: In 2025, IGBT Modules led the market with share 55%, while IGBT Modules is the fastest-growing segment with the highest CAGR (2026–2033).

Silicon IGBT Market Segment Analysis

By Voltage Rating

The Medium Voltage segment dominated the market in 2025 because most industrial machinery, renewable inverters, and motor drives operate in the 600V to 1700V range, creating strong demand for IGBTs optimized for these voltage levels. Their balance of cost, efficiency, and performance supports widespread adoption across established power-electronics applications.

The High Voltage segment is expected to grow fastest from 2026 to 2033 due to increasing deployment of high-capacity renewable plants, HVDC systems, and grid-level power infrastructure requiring devices capable of managing extreme voltages. Growing electrification of transportation and heavy industrial systems further boosts adoption of high-voltage IGBTs.

By End-Use Industry

The Industrial Equipment segment dominated the market in 2025 because industries rely heavily on IGBT-based power modules for motor control, automation, and heavy machinery operations. High durability, efficiency, and scalability make IGBTs indispensable in manufacturing systems, enabling stable performance under harsh conditions and continuous operation, driving the segment’s leading revenue position in 2025.

The Automotive segment is expected to grow fastest from 2026 to 2033 due to rising adoption of electric and hybrid vehicles, which require IGBTs for power control, battery management, and traction inverters. Government incentives, strict emission norms, and rapid EV production expansion further accelerate demand for high-efficiency power semiconductor solutions.

By Application

The Motor Drives segment dominated the market in 2025 because motor-driven systems across industries depend on IGBTs for precise speed control, reduced power losses, and enhanced operational efficiency. Their ability to handle high voltages and currents makes them essential in compressors, pumps, fans, and industrial automation equipment, ensuring sustained demand across manufacturing applications.

The Electric Vehicles segment is expected to grow fastest from 2026 to 2033 as EV powertrains rely on IGBTs for efficient conversion and control of high-power electrical energy. Growing infrastructure development, declining battery costs, and automaker investments in electrification significantly increase the need for advanced power modules, boosting rapid segment expansion.

By Technology

The Standard IGBT Technology segment dominated the market in 2025 because it offers a proven, cost-effective, and highly reliable solution widely used in motor drives, industrial equipment, and power supply systems. Its mature manufacturing ecosystem and broad compatibility ensure strong demand across conventional, high-volume applications.

The High-Speed IGBT Technology segment is expected to grow fastest from 2026 to 2033 as advanced EVs, fast chargers, and renewable systems require faster switching capabilities to improve efficiency and reduce energy losses. Technological shifts toward high-performance power electronics drive adoption of next-generation, high-speed semiconductor solutions.

By Packaging Type

The IGBT Modules segment dominated the market in 2025 and is expected to grow fastest from 2026 to 2033 because modules offer superior thermal performance, higher power density, and greater reliability compared to discrete devices. Their ability to integrate multiple chips into compact, efficient packages makes them essential for electric vehicles, renewable energy systems, motor drives, and industrial machinery. As demand for high-efficiency, high-voltage power conversion increases across advanced applications, IGBT modules continue to gain preference, driving both dominance and accelerated future growth.

Silicon IGBT Market Regional Analysis

Asia Pacific Silicon IGBT Market Insights

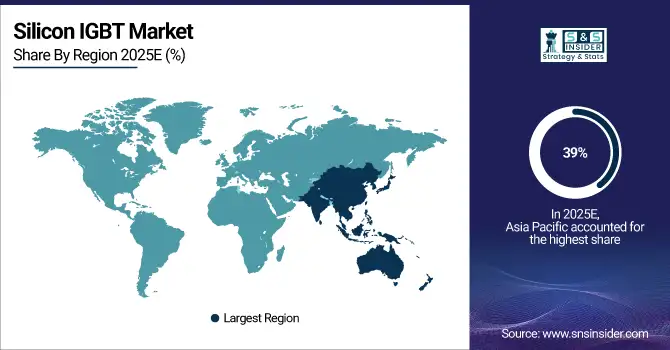

Asia Pacific dominated the Silicon IGBT Market with about 39% revenue share in 2025 due to its strong manufacturing base, expanding electronics production, and large-scale industrial automation.

In 2023, China accounted for nearly 60% of global new electric car registrations, with EVs surpassing 35% of its domestic car sales, reinforcing the region’s rapid EV adoption.

Significant renewable energy investments, favorable government initiatives, and the presence of major semiconductor manufacturers combined with cost-efficient production capabilities further strengthened Asia Pacific’s leading market position during 2025.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Silicon IGBT Market Insights

North America’s Silicon IGBT Market is driven by strong adoption of electric vehicles, increasing investments in renewable energy, and the expansion of industrial automation. The region benefits from advanced technological infrastructure, supportive government policies, and growing deployment of power-efficient systems across transportation, manufacturing, and energy sectors. Rising demand for high-voltage power electronics in grid modernization projects further strengthens the market, positioning North America as a steadily expanding region with significant long-term growth potential.

The United States leads North America’s silicon IGBT market, driven by major EV production, strong renewable-energy investments, and advanced industrial automation adoption.

Europe Silicon IGBT Market Insights

Europe is expected to grow at the fastest CAGR of about 12.18 from 2026 to 2033 because of its aggressive electrification targets, strong push toward carbon neutrality, and rapid adoption of electric vehicles. Increasing investments in renewable energy projects, advancements in power grid modernization, and stringent energy-efficiency regulations further accelerate demand for high-performance IGBT solutions. The region’s focus on sustainable transportation and industrial decarbonization drives accelerated growth.

The United Kingdom leads Europe’s silicon IGBT market, supported by strong EV adoption, major renewable-energy investments, and accelerated power-grid modernization initiatives.

Middle East & Africa and Latin America Silicon IGBT Market Insights

The Middle East & Africa Silicon IGBT Market is supported by rising investments in renewable energy, particularly solar power, alongside expanding industrial automation and infrastructure development that drive demand for efficient power electronics. In Latin America, market growth is fueled by increasing renewable energy installations, expanding automotive manufacturing, and modernization of industrial equipment. Both regions benefit from growing adoption of energy-efficient technologies and supportive government initiatives, contributing to steady overall market expansion.

Silicon IGBT Market Competitive Landscape:

Infineon Technologies AG

Infineon Technologies AG is a global leader in power semiconductors, offering advanced IGBT, silicon carbide (SiC), and hybrid power-module technologies for electric vehicles, renewable energy systems, and industrial drives. Known for its innovation in efficiency, thermal robustness, and reliability, Infineon continues to expand its e-mobility and industrial-power portfolios with cutting-edge Si, SiC, and hybrid architectures. Its strong manufacturing footprint and technology roadmap reinforce its role as a key supplier in next-generation power electronics.

-

October 15, 2024: Introduced the HybridPACK Drive G2 Fusion, the first plug-and-play automotive power module combining silicon + silicon carbide devices for enhanced EV efficiency and performance.

-

April 16, 2025: Launched a new generation of IGBT and RC-IGBT devices optimized for electric vehicles, offering improved switching losses and higher operating temperatures.

-

May 6, 2022: Released the TRENCHSTOP 1700 V IGBT7, expanding high-voltage capability for industrial converters and renewable systems.

Mitsubishi Electric Corporation

Mitsubishi Electric Corporation is a major power-semiconductor manufacturer with a strong presence in industrial drives, renewable energy, and traction applications. The company is recognized for its robust, high-voltage IGBT modules and SiC-based power-device families, enabling increased system efficiency and durability across industrial and mobility markets.

-

December 23, 2024: Announced shipment of samples for the S1-Series 1.7 kV IGBT modules, targeting large industrial equipment requiring high power density.

-

January 14, 2025: Began sample shipments of the LV100-type 1.2 kV IGBT module designed for solar inverters and renewable-energy power-supply systems.

-

January 23, 2024: Industry coverage highlighted six new J3-Series power modules featuring a mix of SiC MOSFET and RC-IGBT technologies for electric-vehicle applications.

ON Semiconductor Corporation (onsemi)

onsemi is a leading supplier of high-performance power semiconductors, focusing on energy-efficient IGBT platforms and SiC devices for industrial automation, renewable energy, heating/cooling, and solar-inverter markets. Its FS7 (Field-Stop 7th Gen) IGBT technology underpins multiple product families that reduce switching losses and simplify system design.

-

March 20, 2023: Introduced the IGBT FS7 switch platform, delivering ultra-efficient 1200 V performance for industrial markets.

-

June 11, 2024: Announced new 7th-Gen IGBT modules (QDual3, 1200 V) offering +10% more power and easier integration for renewable-energy systems.

-

February 26, 2024: Released 7th-Gen IGBT-based Intelligent Power Modules (SPM31) using FS7 technology to cut energy use in HVAC applications.

-

August 27, 2024: Rolled out upgraded solar-focused power modules integrating FS7 IGBTs with EliteSiC diodes, improving inverter efficiency.

STMicroelectronics NV

STMicroelectronics is a prominent provider of power devices for automotive, industrial, and energy applications. The company emphasizes ruggedness, switching efficiency, and thermal performance in its IGBT portfolio while supporting the broader ecosystem with advanced gate-driver solutions for both IGBT and SiC devices.

-

September 4, 2023: Announced a new class of IGBTs offering 1350 V breakdown voltage and 175 °C maximum junction temperature, enhancing reliability under harsh conditions.

-

November 7, 2024: Introduced the STGAP3S galvanically isolated gate drivers with flexible protection features for IGBTs and SiC MOSFETs, strengthening integration options for power-converter designers.

Toshiba Corporation (Toshiba Electronic Devices & Storage)

Toshiba is a key supplier of industrial semiconductor devices, offering discrete IGBTs, press-pack IEGTs, and high-voltage modules that support heavy-duty applications such as air-conditioning, renewable-energy systems, and high-voltage converters. The company is recognized for robust, efficiency-focused designs and continuous enhancement of high-power switching components.

-

March 8, 2023: Launched a new 650 V discrete IGBT aimed at increasing efficiency in air-conditioners and industrial equipment.

-

February 14, 2024: Released the ST3000GXH35A press-pack IEGT rated at 4500 V / 3000 A, designed for high-voltage converters and large-scale industrial power-systems.

Silicon IGBT Market Key Players

Some of the Silicon IGBT Market Companies are:

-

Infineon Technologies AG

-

Mitsubishi Electric Corporation

-

ON Semiconductor

-

STMicroelectronics

-

Fuji Electric Co., Ltd.

-

ROHM Co., Ltd.

-

Hitachi, Ltd.

-

Toshiba Corporation

-

Danfoss Group

-

ABB Ltd

-

Littelfuse, Inc.

-

Silan Microelectronics Co., Ltd.

-

Advanced Power Electronics Corp.

-

Sensitron Semiconductor

-

Power Integrations, Inc.

-

SEMIKRON International GmbH

-

Vishay Intertechnology, Inc.

-

Microsemi Corporation

-

StarPower Semiconductor Ltd.

-

Renesas Electronics Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 4.11 Billion |

| Market Size by 2033 | USD 9.22 Billion |

| CAGR | CAGR of 10.76% From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By End-Use Industry (Automotive, Consumer Electronics, Renewable Energy, Industrial Equipment, Telecommunications) • By Voltage Rating (Low Voltage (up to 600V), Medium Voltage (600V – 1700V), High Voltage (above 1700V)) • By Packaging Type (Discrete IGBTs, IGBT Modules, Integrated Circuit IGBTs) • By Application (Motor Drives, Power Supplies, HVAC Systems, Electric Vehicles, UPS Systems) • By Technology (Standard IGBT Technology, Fast Recovery IGBT Technology, High-Speed IGBT Technology) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Infineon Technologies AG, Mitsubishi Electric Corporation, ON Semiconductor, STMicroelectronics, Fuji Electric Co., Ltd., ROHM Co., Ltd., Hitachi, Ltd., Toshiba Corporation, Danfoss Group, ABB Ltd, Littelfuse, Inc., Silan Microelectronics Co., Ltd., Advanced Power Electronics Corp., Sensitron Semiconductor, Power Integrations, Inc., SEMIKRON International GmbH, Vishay Intertechnology, Inc., Microsemi Corporation, StarPower Semiconductor Ltd., Renesas Electronics Corporation |

Frequently Asked Questions

Asia Pacific dominated in 2025 owing to strong manufacturing capacity, rapid EV adoption, large electronics production, and significant renewable energy investments.

The Industrial Equipment segment dominated due to extensive use of IGBTs in automation, motor control, and heavy machinery across global manufacturing sectors.

The major growth factor is rising adoption of electric vehicles and renewable energy systems, increasing demand for efficient, high-performance power semiconductor devices.

The Silicon IGBT Market size in 2025 was valued at USD 4.11 billion, supported by strong adoption across industrial, automotive, and renewable applications.

The Silicon IGBT Market is expected to grow at a CAGR of 10.76 from 2026 to 2033, driven by expanding power-electronics demand.

Get in Touch