Smart Badge Market Report Scope & Overview:

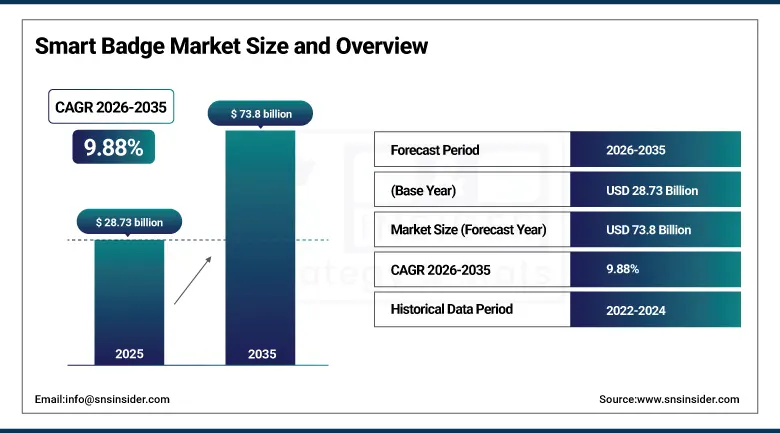

The Smart Badge Market size was valued at USD 28.73 billion in 2025 and is expected to reach USD 73.8 billion by 2035, growing at a CAGR of 9.88% from 2026-2035.

Smart badges are credential devices that go far beyond the laminated photo ID cards they are progressively replacing embedding microprocessors, wireless communication radios, cryptographic security chips, biometric sensors, and in premium versions digital display screens within badge-form-factor hardware that provides identity verification, physical access control, logical system authentication, real-time location tracking, and wireless payment within a single wearable credential that employees carry as their primary organizational interface. The market's commercial logic is compelling security incidents caused by lost, shared, or duplicated physical access credentials create liability, regulatory exposure, and operational disruption that smart badge authentication prevents through cryptographic challenge-response protocols that cannot be replicated without the physical smart badge hardware. Its reflects both the ongoing replacement of legacy proximity card and magnetic stripe badge systems with contactless NFC and RFID smart badge alternatives and the expansion of smart badge functionality into real-time workforce analytics, contact tracing, social distancing monitoring, and productivity measurement that organizations are discovering as valuable operational intelligence beyond the security compliance use case that originally justified smart badge investment.

The Global Security Industry Association documents that the installed base of physical access control systems in the United States exceeds 4 billion credential transactions annually, with smart card and NFC credential formats representing 42% of new system installations in the past three years demonstrating the replacement market's scale as legacy proximity card systems are upgraded. The U.S. Department of Homeland Security's REAL ID Act compliance requirements mandating verifiable digital identity credentials for federal facility access are sustaining government procurement of smart badge infrastructure across federal civilian and military installations.

Market Size and Forecast

-

Market Size in 2025: USD 28.73 Billion

-

Market Size by 2035: USD 73.8 Billion

-

CAGR: 9.88% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Smart Badge Market - Request Free Sample Report

Smart Badge Market Trends

-

AI-powered behavioral analytics integration with smart badge location tracking — generating workforce flow heat maps, meeting room utilization rates, and cross-departmental interaction patterns from badge scan data is enabling workplace optimization insights that justify smart badge investment beyond security compliance alone.

-

Biometric-integrated smart badges combining card-embedded fingerprint sensors with contactless NFC communication are enabling true two-factor authentication without PIN entry simultaneously improving security and user convenience for high-security government and healthcare access control scenarios.

-

Digital identity convergence where smart badge credentials bridge physical access control with cloud-based single sign-on, VPN authentication, and digital signature authorization is positioning smart badges as the physical anchor of enterprise zero-trust identity architectures.

-

Battery-powered digital display smart badges enabling dynamic QR codes, meeting schedules, and visitor management workflows are growing in large corporate campuses where static printed badges cannot communicate real-time information to employees and visitors.

-

Contactless payment integration with smart badges enabling food court, parking, and vending machine purchases through the same credential used for building access is creating convenience value that sustains employee badge adoption without the friction of mandatory security policies.

-

Visitor management smart badge programs where temporary visitor badges are digitally provisioned with time-limited access credentials from a reception kiosk and deactivated at departure are replacing paper visitor logs with documented, auditable access records that comply with ISO 27001 and SOC 2 security audit requirements.

-

Healthcare wearable badge integration where smart badges on clinical staff simultaneously manage access control, real-time location for emergency response coordination, and time-temperature exposure logging in pharmaceutical storage areas — is creating healthcare-specific badge functionality that general enterprise badges do not address.

U.S. Smart Badge Market Size Outlook:

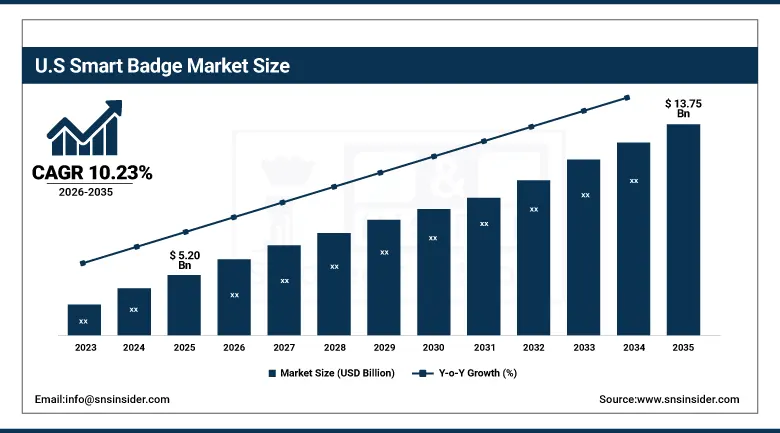

The U.S. Smart Badge Market was valued at USD 5.20 billion in 2025 and is expected to reach USD 13.75 billion by 2035, growing at a CAGR of 10.23%. North America leads the global Smart Badge Market, driven by the United States' combination of the largest corporate enterprise market for physical security infrastructure, the most comprehensive government identity credential mandates through HSPD-12 and REAL ID requirements, and the most commercially active smart badge technology ecosystem. U.S. government smart badge adoption where the federal government has mandated PIV (Personal Identity Verification) smart card credentials for all federal employees since 2008 has created a large and technically sophisticated government smart badge industry that drives technology development benefiting the commercial sector. U.S. healthcare organizations whose HIPAA privacy requirements for controlled access to patient records and pharmaceutical storage areas create security compliance motivation are among the most active adopters of biometric-enhanced smart badge systems in the enterprise sector.

The U.S. Office of Personnel Management documents that over 4.2 million federal employees and contractors hold active PIV smart card credentials representing the world's largest single-organization smart badge deployment by credentialed population. HID Global's 2025 State of Physical Access Control report documents that 62% of U.S. organizations with more than 1,000 employees have completed or are actively deploying smart card migration from legacy proximity card access control.

Smart Badge Market Segment Analysis

-

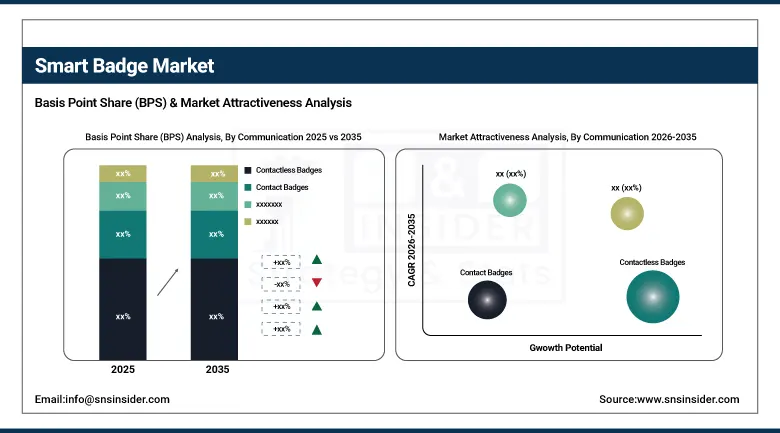

By Communication Type, Contactless Badges dominated with the largest share in 2025; Contact Badges growing at the fastest CAGR.

-

By Type, Smart Badges without Display dominated with the largest share in 2025; Smart Badges with Display growing at the fastest CAGR.

-

By Application, Government and Healthcare dominated with the largest share in 2025; Retail and Hospitality growing at the fastest CAGR.

By Communication Type: Contactless Dominates at Scale, Contact Badges Drive Next-Gen Growth

Contactless Badges held the dominant position in the Smart Badge Market in 2025, driven by the widespread adoption of NFC and RFID-based credentials across corporate, government, healthcare, and retail environments where secure, fast, and seamless authentication is the primary requirement. These badges are preferred due to their passive operation, low cost, long lifecycle, and strong compatibility with global access control infrastructures, making them the standard for large-scale identity and access management deployments. Their ability to enable frictionless entry, improve operational efficiency, and support scalable security systems continues to reinforce their dominance across multiple end-use industries.

The Contact Badges segment is growing at the fastest CAGR, supported by increasing demand for multi-functional smart identification solutions that integrate enhanced data exchange, higher security controls, and evolving workplace authentication requirements. Growing digital transformation initiatives, expansion of smart workplace ecosystems, and rising need for secure yet interactive identification systems in high-security environments are accelerating the adoption of advanced contact-based smart badge technologies globally.

By Type: Smart Badges without Display dominate, With Display growing fastest

Smart Badges without Display held the dominant position in the Smart Badge Industry in 2025, driven by their widespread deployment in corporate, government, and healthcare environments where secure authentication, low cost, long lifecycle, and seamless integration with existing RFID/NFC access control systems remain the core requirements. Their passive design, high durability, and compatibility with established global access infrastructure make them the preferred choice for large-scale identity management programs.

Smart Badges with Display are growing at the fastest CAGR, supported by rising demand for interactive identity solutions that enable dynamic information display, visitor management, and enhanced user engagement in smart workplaces and enterprise campuses.

By Application: Government & Healthcare dominate, Retail & Hospitality growing fastest

Government and Healthcare held the dominant application position in the Smart Badge Market in 2025, supported by strong adoption of secure identity verification systems, controlled access environments, and strict regulatory compliance requirements across public sector facilities and medical institutions. These sectors rely heavily on smart badges for workforce authentication, patient identification, and secure facility management.

Retail and Hospitality are growing at the fastest CAGR, driven by increasing adoption of smart employee identification systems, personalized customer engagement solutions, and digital access control technologies that enhance operational efficiency, service quality, and visitor experience.

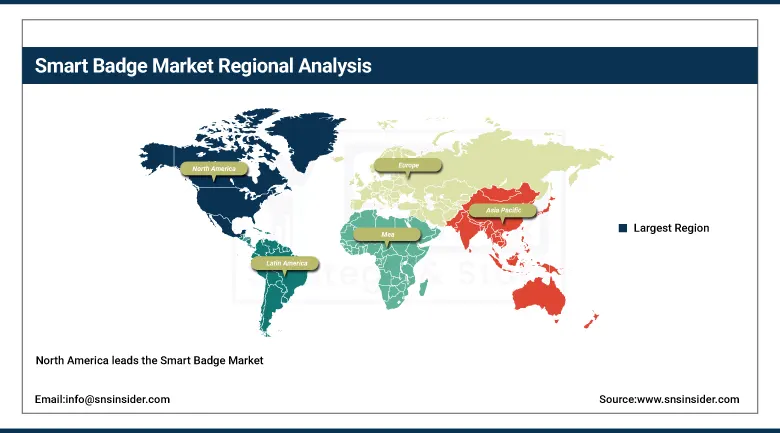

Smart Badge Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

48% |

North America Smart Badge Market Insights

North America leads the Smart Badge Market driven by U.S. government PIV mandate scale, the world's most active corporate enterprise security upgrade market, and the commercial concentration of leading smart badge technology companies including HID Global (ASSA ABLOY), Identiv, Allegion, and Entrust. The U.S. defense contractor market where cleared defense facility access requires DoD-compliant smart credential systems creates a specialized high-security smart badge procurement channel whose stringent specifications sustain premium technology investment by major defense contractors and their personnel security officers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Smart Badge Market Insights

Asia Pacific is the fastest-growing regional Smart Badge Market, driven by China's government and corporate digital identity infrastructure investment where national digital ID programs and corporate smart building initiatives are creating large-scale smart badge deployments India's expanding IT services sector whose large corporate campuses require sophisticated access control, and South Korea and Japan's technology-forward enterprise security culture. Government-initiated smart badge programs across ASEAN where digital national ID infrastructure is enabling interoperable citizen credential ecosystems are creating public sector smart badge procurement at scales that government programs in more mature economies already completed in earlier implementation cycles.

Europe Smart Badge Market Insights

Europe's Smart Badge Market is growing with the EU's eIDAS 2.0 digital identity framework whose interoperable digital credential standard enables cross-border digital identity recognition that sustains national smart ID infrastructure investment and corporate enterprise security upgrade cycles replacing aging proximity card systems with NFC smart badge alternatives. Germany's industrial corporate campuses, the UK's financial services sector access control requirements, and France's government facility security mandates collectively sustain European smart badge demand growth.

MEA and Latin America Smart Badge Market Insights

The Middle East's Smart Badge Industry is growing with the Gulf states' smart city and smart government initiatives where UAE's Emirates ID smart card program, Saudi Arabia's ABSHER digital identity ecosystem, and Qatar's national ID infrastructure create government-driven smart credential adoption at scale. Latin America's market concentrates in Brazil and Mexico's growing corporate enterprise sector and financial services access control requirements.

Growth Drivers: Workplace security mandates and zero-trust identity architecture adoption driving sustained smart badge market growth globally

The Smart Badge Market is driven by the progressive adoption of zero-trust security architecture in enterprise and government IT environments where the principle of 'never trust, always verify' requires multi-factor authentication for every access request that smart badge hardware authentication satisfies at the physical credential layer. The pandemic's acceleration of hybrid work created new physical security challenges where employees accessing offices on irregular schedules and contractors entering unmanned facilities require credentialing systems whose smart badge-based audit trails provide the access event documentation that compliance requirements mandate. As workplace experience becomes a competitive talent attraction factor, smart badge-enabled amenity services seamless access, contactless payment, meeting room reservation through badge tap add employee convenience value above the compliance motivation.

Restraints: Implementation complexity and interoperability challenges creating smart badge industry adoption barriers globally

Smart badge system implementation involving badge reader infrastructure installation, badge management system deployment, credential provisioning workflows, and integration with existing HR, IT, and physical security systems creates project complexity and cost that represents a meaningful barrier for smaller organizations. The lack of universal interoperability between smart badge credentials from different vendors where HID iCLASS credentials work only with HID readers, LEGIC credentials require LEGIC infrastructure creates migration friction for organizations replacing incumbent systems with competing technology platforms.

Opportunities: Digital display badge proliferation and healthcare biometric integration creating significant smart badge market growth opportunities globally

Digital display smart badges whose E-Ink or low-power OLED screens can display dynamic QR codes, employee names, roles, access levels, and real-time calendar information represent the smart badge market's most commercially differentiated product innovation opportunity. As corporate campuses adopt dynamic space management where seating assignments, meeting room bookings, and visitor management are real-time rather than fixed the display badge's ability to communicate current authorization status and employee availability creates workflow value that static badges cannot provide. Healthcare biometric integration creates a growing premium segment where fingerprint-reading smart badges eliminate shared credential vulnerability in clinical environments.

Recent Developments:

-

2026: HID Global launched the HID Signo Digital Display Smart Badge — an E-Ink display badge with embedded NFC/RFID contactless smart card, fingerprint biometric reader, and Bluetooth Low Energy connectivity — enabling dynamic QR code generation for visitor management, employee photo and role display, and two-factor biometric-plus-badge authentication in a single wearable credential whose 30-day battery life on a single charge eliminates the daily charging requirement that previous battery-powered display badges imposed on enterprise deployment programs.

-

2025: Identiv received GSA Schedule approval for its KDIS uTrust Smart Badge system meeting FIPS 201-3 Level 3 assurance requirements — the first commercially available smart badge meeting the highest assurance level in the U.S. federal PIV framework — enabling government agencies to deploy single-credential authentication for physical access, logical system access, and digital signature without separate smart card readers, enabling agencies to eliminate USD 45-120 per seat in dedicated PIV card reader hardware from their endpoint computing costs.

-

2025: Samsung launched its Galaxy Badge Enterprise Edition — integrating NFC Type 4 Tag smart card functionality into a wearable badge format compatible with Galaxy Watch 7 pairing — enabling employees to use their wearable smartwatch as a physical access control credential, logical authentication token, and contactless payment device simultaneously, removing the dedicated badge hardware requirement for Samsung ecosystem enterprise deployments at companies including Samsung Electronics' own global facilities and partner organizations in the Samsung enterprise ecosystem.

Smart Badge Companies are:

-

HID Global Corporation (ASSA ABLOY)

-

Identiv Inc.

-

Allegion plc

-

Entrust Corporation

-

Gallagher Security

-

Bosch Building Technologies

-

Honeywell Commercial Security

-

Johnson Controls (Tyco Security)

-

LEGIC Identsystems AG

-

STid Security

-

Imprivata Inc.

-

Wavelink Inc.

-

Idemia Group

-

ISCS Inc.

-

Assa Abloy AB

-

NXP Semiconductors NV

-

Samsung Electronics Co. Ltd.

-

BioConnect Inc.

-

Suprema Inc.

-

Genetec Inc.

Smart Badge Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.73 Billion |

| Market Size by 2035 | USD 73.8 Billion |

| CAGR | CAGR of 9.88% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Communication (Contact Badges, Contactless Badges) • By Type (Smart Badges with Display, Smart Badges without Display) • By Application (Government and Healthcare, Corporate, Event and Entertainment, Retail and Hospitality, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | HID Global Corporation, Identiv Inc., Allegion plc, Entrust Corporation, Gallagher Security, Bosch Building Technologies, Honeywell Commercial Security, Johnson Controls, LEGIC Identsystems AG, STid Security, Imprivata Inc., Wavelink Inc., Idemia Group, ISCS Inc., ASSA ABLOY AB, NXP Semiconductors NV, Samsung Electronics Co. Ltd., BioConnect Inc., Suprema Inc., and Genetec Inc. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Smart Badge Market in 2023

Ans: The “Contact Badges” segment dominated the Smart Badge Market.

Ans: The key drivers of the Smart Badge Market include rising security concerns, increasing adoption in government and healthcare, growing demand for contactless solutions, and advancements in IoT and wireless technology.

Ans: Without Display dominated with approximately 69% share; With Display is growing at the fastest CAGR.

Ans: The Smart Badge Market is expected to grow at a CAGR of 9.88% from 2026 to 2035.

Get in Touch