Small Satellite Market Report Scope & Overview:

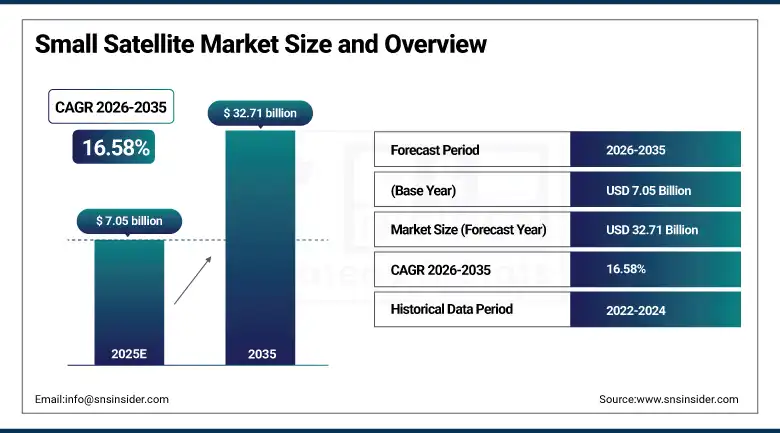

Small Satellite Market was valued at USD 7.05 billion in 2025 and is expected to reach USD 32.71 billion by 2035, growing at a CAGR of 16.58% from 2026–2035.

The global Small Satellite Market is at the epicentre of the most consequential democratisation of space access in history, as advances in miniaturisation technology, the emergence of dedicated small satellite launch vehicles and rideshare programmes, and the dramatic reduction in satellite component costs are collectively enabling a new era of space utilisation where commercial companies, government agencies, academic institutions, and even individual nations with modest space budgets can develop, launch, and operate functional satellites within compressed timelines and at costs that would have been considered impractically small for any mission a decade ago. Small satellites, typically defined as spacecraft below 500 kilograms in mass, encompass a broad spectrum from the 100 to 500-kilogram minisatellite class through microsatellites, nanosatellites in the popular CubeSat form factor, and picosatellites below 1 kilogram, each offering distinct capability profiles and market positions across a rapidly expanding range of applications.

The market is propelled by two complementary commercial forces: the development of large-scale satellite constellations encompassing thousands of small satellites in Low Earth Orbit to deliver global broadband connectivity, including SpaceX's Starlink with over 6,000 deployed satellites, Amazon's Project Kuiper targeting 3,236 satellite deployment, and OneWeb's 648 satellite connectivity network; and the parallel growth of commercial Earth observation constellations from Planet Labs, Spire Global, Satellogic, and BlackSky that provide daily global imaging and persistent monitoring capabilities previously available only to government intelligence agencies. SpaceX's October 2025 launch of its 10,000th Starlink satellite confirms the extraordinary commercial scale that LEO satellite constellation deployment has achieved, fundamentally reshaping the global telecommunications infrastructure and creating the largest commercial small satellite market in history.

Market Size and Forecast

-

Market Size in 2025: USD 7.05 Billion

-

Market Size by 2035: USD 32.71 Billion

-

CAGR: 16.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Small Satellite Market - Request Free Sample Report

Small Satellite Market Trends

-

Growing adoption of rideshare launch programmes including SpaceX's SmallSat Rideshare Program.

-

Accelerating miniaturisation of satellite payloads including high-resolution Earth observation cameras, synthetic aperture radar systems.

-

Growing integration of artificial intelligence and machine learning capabilities into small satellite onboard computing systems.

-

Rising government investment in small satellite programmes for national defence, reconnaissance, communications resilience.

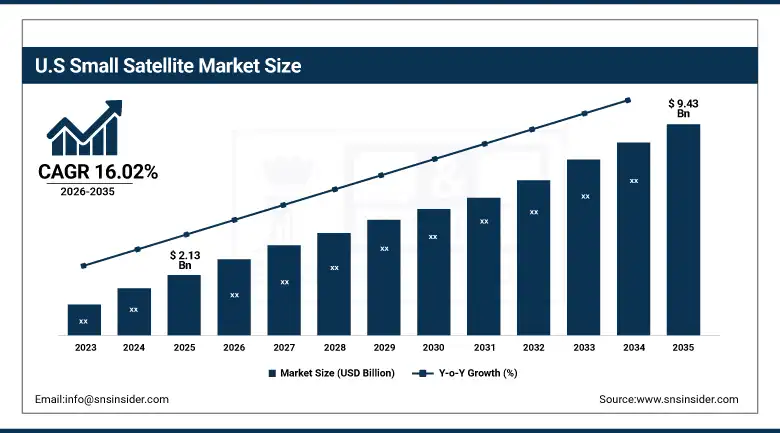

U.S. Small Satellite Market was valued at USD 2.13 billion in 2025 and is expected to reach USD 9.43 billion by 2035, growing at a CAGR of 16.02% during 2026–2035.

The United States dominates the global Small Satellite Market through the extraordinary commercial ecosystem anchored by SpaceX, Planet Labs, Rocket Lab, HawkEye 360, Spire Global, and BlackSky, combined with the most active government small satellite procurement from NASA, the Space Force, National Reconnaissance Office, and DARPA that provides the largest national funding base for small satellite technology development in the world. The U.S. government's growing recognition that small satellite constellations provide national security advantages in contested space environments, reflected in the Space Force's Proliferated Warfighter Space Architecture programme targeting hundreds of LEO small satellites for military communications and missile warning, is creating a government procurement demand channel that complements the commercial LEO constellation buildout.

SpaceX's October 2025 achievement of launching its 10,000th Starlink satellite through its 132nd Falcon 9 mission of the year, further strengthening satellite broadband coverage quality and geographic reach, represents the most commercially significant milestone in small satellite market history. This deployment scale confirms that the U.S. commercial small satellite industry has achieved an operational maturity and production economics that no other national space industry has replicated, establishing U.S. commercial leadership in the global small satellite market through the 2026 to 2035 forecast period.

Small Satellite Market Segment Insights

-

According to Satellite Mass, Minisatellite class (100 to 500 kg) retains the largest revenue contribution; Nanosatellites (1 to 10 kg) are expected to grow at the fastest CAGR driven by lower development costs, shorter build timelines, and suitability for rideshare launch programmes.

-

In terms of Application, Communication dominated with approximately 34.5% market share in 2025 and is also expected to grow at the fastest CAGR from 2026 to 2035, driven by the proliferation of satellite internet constellation deployments and global broadband connectivity demand.

-

By End-User, Commercial dominated and is growing rapidly through commercial constellation operators and Earth observation data service companies; Government and Defense is the second-largest segment through national security space programmes and Earth monitoring satellite procurement.

-

By Orbit, Low Earth Orbit dominated with the largest revenue share in 2025, reflecting the commercial constellation deployment concentration in LEO for broadband and Earth observation; LEO is simultaneously the fastest-growing orbit as constellation deployment scales.

Small Satellite Market Segment Analysis

By Satellite Mass: Minisatellite dominates by revenue, Nanosatellite grows fastest

The Minisatellite class (100 to 500 kg) retains the largest revenue contribution within the Small Satellite Market in 2025, reflecting the higher per-unit production and launch cost of larger small satellites that deliver the most sophisticated payload capabilities including high-resolution optical imaging, synthetic aperture radar, and communications transponders that generate the highest commercial and government data service revenues. Minisatellites provide the payload mass, power budget, and volume that accommodate the advanced sensors, power systems, and onboard computing required for professional-grade commercial Earth observation and communications applications. Major commercial operators including Planet Labs' SkySat platform and defence reconnaissance programmes specify minisatellite class platforms for the most performance-demanding missions requiring state-of-the-art payload capability.

Nanosatellites (1 to 10 kg), predominantly in the standardised CubeSat form factor, are projected to grow at the fastest CAGR during the forecast period, driven by the extraordinary cost reduction that nanosatellite platforms enable for applications where scientific value, IoT data collection, technology demonstration, and atmospheric sensing do not require the larger sensor apertures and power systems of heavier small satellite classes. CubeSat technology has enabled universities, government research agencies, and commercial startups to deploy orbital platforms at costs measured in tens of thousands to low millions of dollars that provide genuine scientific and commercial utility, creating an entirely new category of space mission economics. The growing nanosatellite constellation approach, where arrays of dozens to hundreds of low-cost units collectively provide revisit rates and data coverage that single larger satellites cannot match, is expanding the nanosatellite addressable market across IoT connectivity, maritime tracking, signals intelligence, and climate monitoring applications.

By Application: Communication dominates and grows fastest

The Communication application segment dominated the Small Satellite Market in 2025 with approximately 34.5% of revenues and is simultaneously projected to grow at the fastest CAGR from 2026 to 2035, a dual leadership reflecting the extraordinary commercial and strategic importance of satellite-based global connectivity services that are the primary commercial justification for the largest small satellite constellation deployments in history. Satellite communication applications encompassing global broadband internet service, maritime and aviation connectivity, IoT device connectivity, backhaul for terrestrial 5G networks in underserved regions, and military communication resilience collectively represent the most commercially valuable and volume-intensive use cases for small satellites. The scale of communication constellation deployment, where SpaceX Starlink alone has over 6,000 satellites providing commercial broadband service to over 4 million subscribers in more than 100 countries, demonstrates the unprecedented market development potential of LEO satellite communication services.

Earth Observation is the second-largest and strongly growing application segment, driven by commercial demand for daily global satellite imagery from Planet Labs' constellation providing daily coverage of the entire Earth's landmass, government demand for continuous monitoring of agriculture, natural resource management, border surveillance, and disaster response, and the growing market for AI-analysed Earth observation data products including crop yield prediction, construction activity monitoring, deforestation tracking, and shipping lane congestion analysis. The proliferation of commercial Earth observation small satellite constellations has created a democratisation of geospatial intelligence that was previously confined to government intelligence agencies, enabling businesses, NGOs, researchers, and governments at all levels to access satellite imagery and monitoring data that is transforming decision-making across agriculture, logistics, insurance, and environmental management.

By Orbit: Low Earth Orbit dominates and grows fastest

Low Earth Orbit retained the dominant position in 2025 with the largest small satellite revenue share and is simultaneously the fastest-growing orbit segment, reflecting the profound commercial and technical advantages of LEO deployment for the most commercially significant small satellite applications including broadband communication and Earth observation. LEO orbits between 200- and 2,000-kilometres altitude provide the round-trip signal latency of 20 to 60 milliseconds that is competitive with fibre broadband for most consumer and enterprise applications, enabling satellite internet services to serve the latency-sensitive applications that earlier high-altitude geostationary satellite broadband services could not reliably support. LEO's lower altitude additionally enables satellite imaging at resolutions down to sub-meter per pixel using much smaller telescope apertures than equivalent geostationary imaging systems, making LEO the only commercially viable orbit for high-resolution commercial Earth observation constellations.

Medium Earth Orbit and specialised higher altitude orbits serve important niche application segments including navigation satellite systems such as GPS, GLONASS, and Galileo that require the global coverage geometry achievable at MEO altitudes, and highly elliptical orbits serving high-latitude communication coverage over Arctic regions that geostationary orbits cannot reach. The commercial small satellite market activity is overwhelmingly concentrated in LEO, where the combination of communication, Earth observation, IoT connectivity, and technology demonstration applications creates the broadest and most rapidly growing commercial satellite deployment programme in space history.

Small Satellite Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~84% |

|

Europe |

United Kingdom |

~28% |

|

Asia Pacific |

China |

~43% |

|

Middle East & Africa |

UAE |

~28% |

|

Latin America |

Brazil |

~43% |

North America Small Satellite Market Insights

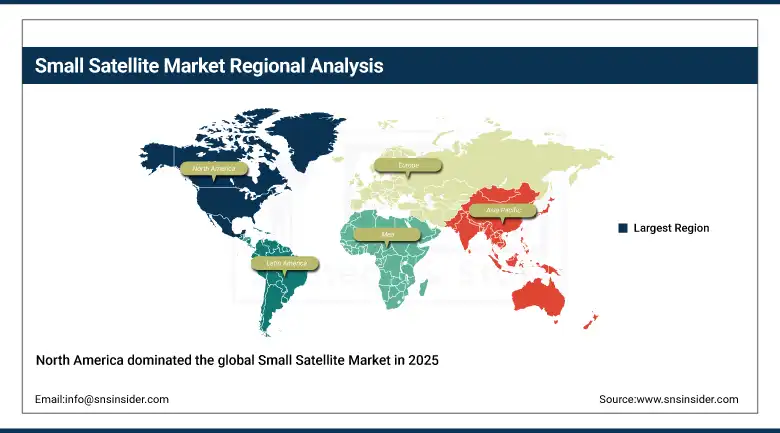

North America dominated the global Small Satellite Market in 2025, driven overwhelmingly by the United States which accounted for approximately 84% of North American revenues. U.S. market leadership is anchored by SpaceX's dominant commercial small satellite launch and constellation operation capabilities, Planet Labs' world-leading commercial Earth observation constellation, and the largest national government investment in small satellite technology development globally through NASA, Space Force, NRO, and DARPA. The U.S. commercial space ecosystem's unique combination of venture capital investment, advanced technology development capability, and the world's most active launch market creates a self-reinforcing innovation cycle that sustains American commercial and technical leadership in small satellites.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Small Satellite Market Insights

Asia Pacific is projected to grow at the fastest regional CAGR of approximately 17.48% through 2035, driven by China's aggressive government-backed satellite constellation programmes including the Guowang 12,992-satellite broadband constellation approved in 2020, India's ISRO expanding commercial small satellite launch services through its PSLV rideshare programme and new SSLV dedicated small satellite launch vehicle, Japan's advanced commercial small satellite industry anchored by Mitsubishi Electric and emerging startups, and South Korea's growing national space programme. China's dominance within the region through state-backed funding, domestic launch vehicle availability, and a large domestic satellite manufacturing ecosystem positions it as one of the world's most significant small satellite markets independent of the commercial Western constellation buildout.

Europe Small Satellite Market Insights

Europe is a technically sophisticated small satellite market, anchored by the United Kingdom's world-class commercial small satellite industry encompassing Surrey Satellite Technology Limited, Reaction Engines, and a growing ecosystem of small satellite startups supported by the UK Space Agency, combined with Luxembourg's commercial satellite sector, France's growing small satellite programmes at CNES and commercial operators, and Germany's active aerospace research community. The European Space Agency's expanding in-house small satellite programme and commercial procurements are sustaining European market development, while the continent's growing commercial Earth observation and IoT connectivity startups are deploying new small satellite constellations that expand European market presence.

Middle East & Africa and Latin America Small Satellite Market Insights

MEA and Latin America are emerging small satellite markets, driven by growing government investment in national space capabilities for communication, Earth observation, and navigation sovereignty, combined with expanding commercial demand for satellite connectivity services in regions with limited terrestrial broadband infrastructure. The UAE's Mohammed Bin Rashid Space Centre's active small satellite development programme, including Earth observation satellites providing daily national monitoring coverage, exemplifies the growing national space programme investment across the Gulf. Brazil leads Latin American small satellite market revenues through its national space programme and INPE Earth observation satellite operations.

Small Satellite Market Growth Drivers:

-

LEO satellite constellation deployment for global broadband and Earth observation creating the largest commercial small satellite demand in history

The primary structural growth driver for the Small Satellite Market is the unprecedented commercial investment in LEO satellite constellation deployment for global broadband connectivity and Earth observation services that is simultaneously creating the largest satellite manufacturing demand in space history, the highest launch frequency ever achieved, and the most commercially significant space market that has ever existed. The global digital divide, where an estimated 2.6 billion people lack reliable internet access, represents the commercial addressable market that has motivated SpaceX, Amazon, OneWeb, and multiple national governments to commit hundreds of billions of dollars to satellite constellation infrastructure investment, sustaining small satellite market demand at a scale that will expand through the forecast period as constellation deployment, maintenance, and generational upgrade cycles continue.

SpaceX's October 2025 launch of its 10,000th Starlink satellite, achieving the milestone through its 132nd Falcon 9 mission of the year, represents the most compelling validation of the LEO satellite constellation commercial model ever achieved, with Starlink serving over 4 million customers across more than 100 countries and generating substantial annual recurring revenue that validates the commercial case for large-scale LEO satellite constellation investment. Amazon's parallel Project Kuiper beginning commercial deployment with over USD 10 billion committed confirms that LEO satellite broadband is not a single-company experiment but a structural transformation of global telecommunications infrastructure that will sustain small satellite market demand through the 2026 to 2035 forecast period.

Small Satellite Market Restraints

-

Orbital debris proliferation risks, spectrum allocation and interference management, and satellite re-entry environmental concerns limiting regulatory approval for new constellations

A significant restraint on the Small Satellite Market is the growing concern among space regulators, national space agencies, and the scientific community about orbital debris accumulation from large-scale LEO constellation deployment, where even partial collision events between constellation satellites and existing orbital objects can generate debris clouds that endanger other satellites and future orbital access. The ITU frequency coordination process, which requires satellite operators to negotiate spectrum access with existing users and file orbital filings years in advance of planned launches, creates regulatory timelines that can constrain new market entrants and slow the deployment of approved constellation programmes. Atmospheric re-entry of decommissioned satellites and launch vehicle upper stages is raising environmental concerns as large constellations create continuous re-entry events that deposit metallic particles in the stratosphere whose long-term atmospheric chemistry effects are actively being studied by climate researchers.

Small Satellite Market Opportunities

-

In-orbit servicing and satellite life extension, government proliferated LEO defence constellations, and emerging market satellite broadband subscriber base expansion

In-orbit satellite servicing, where autonomous robotic spacecraft extend the operational life of small satellites through refuelling, component replacement, and orbital repositioning services, represents an emerging market category that addresses both the commercial economics of constellation management and the regulatory pressure to reduce orbital debris through active deorbit of end-of-life satellites. Government proliferated LEO defence constellation programmes, where national militaries invest in large constellations of small satellites for resilient communications, persistent missile warning, and space situational awareness that cannot be defeated by attacks on individual high-value geostationary targets, represent a growing sovereign demand channel that supplements commercial constellation investment. The 2.6 billion globally unconnected population represents the ultimate commercial TAM for LEO satellite broadband, with each percentage point of market penetration across under-served markets in South Asia, Sub-Saharan Africa, and Latin America translating directly into millions of new satellite broadband subscribers sustaining constellation operators' commercial revenue growth.

Recent Developments:

-

October 2025: SpaceX launched its 10,000th Starlink satellite through its 132nd Falcon 9 mission of the year, further strengthening global coverage quality and service availability for over 4 million subscribers across more than 100 countries.

-

2025: Amazon began commercial deployment of Project Kuiper satellites, with the first operational broadband services targeting enterprise and government customers in priority coverage zones before expanding to consumer broadband in underserved markets.

-

2025: Planet Labs expanded its SkySat constellation with next-generation very high-resolution Earth observation satellites providing sub-50-centimetre resolution imaging capability and daily revisit coverage over major commercial imaging demand regions.

-

2025: Rocket Lab expanded its Electron small satellite launch vehicle programme with increased launch cadence, achieving monthly dedicated small satellite launch frequency from its New Zealand and planned U.S. Virginia launch facilities.

-

2025: The Space Force awarded multiple contracts under its Proliferated Warfighter Space Architecture programme for LEO military communications and missile warning small satellites, confirming the U.S. government's commitment to resilient distributed LEO space architecture.

Small Satellite Market Key Players

-

SpaceX Inc.

-

Planet Labs PBC

-

Rocket Lab USA Inc.

-

Airbus Defence and Space SAS

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Thales Alenia Space

-

Surrey Satellite Technology Ltd. (SSTL)

-

Blue Canyon Technologies LLC

-

Spire Global Inc.

-

BlackSky Technology Inc.

-

HawkEye 360 Inc.

-

Satellogic Inc.

-

OneWeb Ltd.

-

Amazon.com Inc. (Project Kuiper)

-

GomSpace Group AB

-

Tyvak Nano-Satellite Systems Inc. (Terran Orbital)

-

NanoAvionics UAB

-

Exolaunch GmbH

-

Orbital Micro Systems Inc.

Small Satellite Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.05 Billion |

| Market Size by 2035 | USD 32.71 Billion |

| CAGR | CAGR of 16.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Satellite Mass (Minisatellite 100–500 kg, Microsatellite 10–100 kg, Nanosatellite 1–10 kg, Picosatellite Below 1 kg, Others) • By Application (Communication, Earth Observation, Navigation, Scientific Research, Technology Demonstration, Others) • By End-User (Commercial, Government and Defense, Academic and Research) • By Orbit (Low Earth Orbit, Medium Earth Orbit, Geostationary Orbit, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | SpaceX Inc., Planet Labs PBC, Rocket Lab USA Inc., Airbus Defence and Space SAS, Lockheed Martin Corporation, Northrop Grumman Corporation, Thales Alenia Space, Surrey Satellite Technology Ltd. (SSTL), Blue Canyon Technologies LLC, Spire Global Inc., BlackSky Technology Inc., HawkEye 360 Inc., Satellogic Inc., OneWeb Ltd., Amazon.com Inc. (Project Kuiper), GomSpace Group AB, Tyvak Nano-Satellite Systems Inc. (Terran Orbital), NanoAvionics UAB, Exolaunch GmbH, Orbital Micro Systems Inc. |

Frequently Asked Questions

Ans: The unprecedented commercial investment in LEO satellite constellation deployment for global broadband connectivity and Earth observation services, exemplified by SpaceX Starlink's 10,000th satellite launch milestone in October 2025 serving over 4 million global subscribers and Amazon Project Kuiper's USD 10 billion deployment commitment, creating the largest commercial small satellite manufacturing and launch demand in space history.

Ans: The Small Satellite Market was valued at USD 7.053 billion in 2025.

Ans: North America dominated with the largest revenue share in 2025, led by the United States which accounted for approximately 84% of North American revenues through SpaceX's dominant commercial constellation operations, Planet Labs' world-leading Earth observation constellation, and the largest national government investment in small satellite technology development globally through NASA, Space Force, and defense intelligence agencies.

Ans: Nanosatellites (1 to 10 kg) are expected to grow at the fastest CAGR through 2035, driven by their lower development costs, shorter build timelines, and suitability for rideshare launch programmes that are enabling universities, startups, and commercial enterprises to access orbit for IoT connectivity, technology demonstration, scientific research, and atmospheric monitoring applications at costs previously impractical for these organisations.

Ans: Communication dominated with approximately 34.5% of market revenues in 2025 and is simultaneously the fastest-growing application through 2035, driven by the proliferation of LEO satellite internet constellations including Starlink and Project Kuiper targeting global broadband connectivity for the estimated 2.6 billion people currently without reliable internet access.

Ans: The Small Satellite Market is expected to grow at a CAGR of 16.58% from 2026 to 2035.

Get in Touch