Smart Container Market Report Scope & Overview:

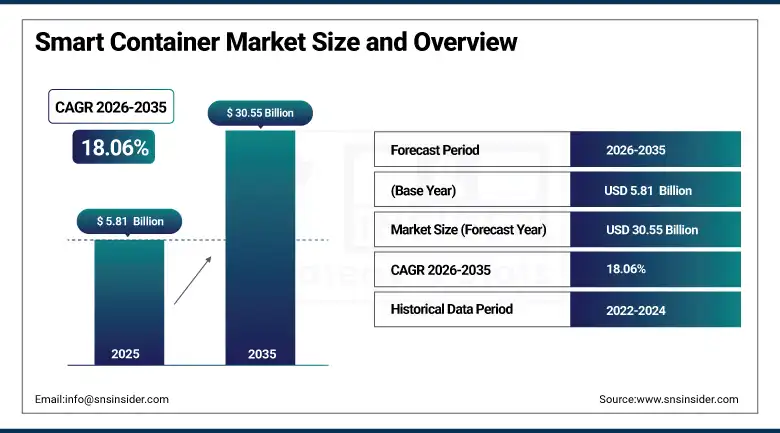

The Smart Container Market was valued at USD 5.81 Billion in 2025 and is expected to reach USD 30.55 Billion by 2035, growing at a CAGR of 18.06% from 2026–2035.

The global smart container market is advancing as shipping companies, third-party logistics providers, and cargo owners across pharmaceuticals, food and beverages, and high-value retail goods systematically retrofit conventional intermodal containers with embedded GPS tracking, environmental sensors, and cellular or satellite connectivity that provides real-time visibility into container location, temperature, humidity, shock, and tampering status throughout multi-leg international shipping journeys. Smart containers integrate IoT sensors, communication modules, and data analytics platforms whose combined capability eliminates the supply chain blind spots that conventional containers create between origin loading and destination unloading, enabling proactive intervention when environmental conditions threaten cargo integrity or security breaches occur. Growing demand for real-time monitoring and visibility in supply chains, and increasing adoption of IoT and sensor technologies escalating market growth.

In August 2024, Hapag-Lloyd and Nexxiot announced a partnership aimed at creating the largest connected fleet of smart containers, enabling real-time door-to-door monitoring set to cover over 1 million containers, while in November 2024 Hapag-Lloyd expanded its tracking deployment to over 1.5 million containers through a collaboration with HERE Tracking to improve inland estimated time of arrival accuracy across worldwide transportation networks. These large-scale fleet deployments demonstrated the shipping industry’s decisive commercial commitment to smart container technology as standard operating infrastructure rather than a premium add-on service for select high-value cargo.

Market Size and Forecast

-

Market Size in 2026E: USD 6.86 Billion

-

Market Size by 2035: USD 30.55 Billion

-

CAGR: 18.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Smart Container Market - Request Free Sample Report

Smart Container Market Trends

-

Large-scale shipping line fleet deployments are connecting millions of containers with IoT tracking devices for door-to-door visibility.

-

LoRa WAN connectivity adoption is expanding as a cost-effective, long-range alternative to cellular connectivity for smart container networks.

-

AI-powered predictive analytics is enabling automated alerts and proactive intervention for temperature and security anomalies.

-

Blockchain integration is enhancing supply chain transparency and tamper-proof documentation for high-value container shipments.

-

Cold chain pharmaceutical shipping is driving stricter GDP-compliant environmental monitoring requirements within smart container deployments.

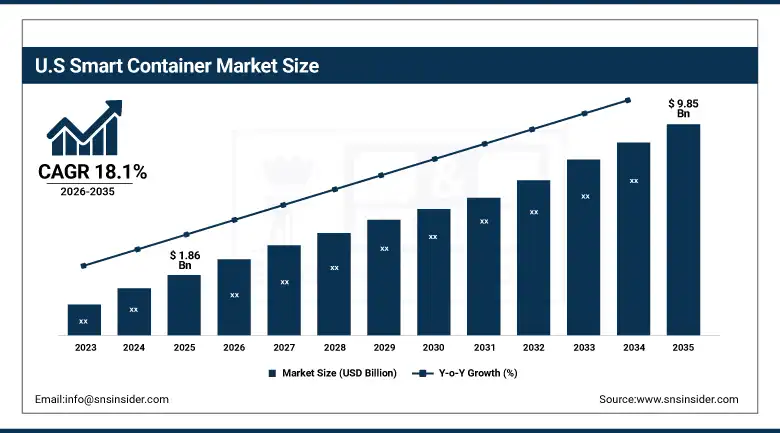

The U.S. Smart Container Market Outlook

The U.S. Smart Container Market was valued at approximately USD 1.86 Billion in 2025 and is projected to reach approximately USD 9.85 Billion by 2035, expanding at a CAGR of around 18.1% during 2026–2035.

The United States leads North American smart container revenues through its position as the world’s largest import and export market whose container volume creates the largest single national addressable market for tracking technology deployment, the advanced cold chain pharmaceutical and food distribution infrastructure requiring stringent environmental monitoring, and the early adoption of IoT-enabled logistics among major shipping lines and third-party logistics providers. Orbcomm, Traxens, and Phillips Connect Technologies sustain U.S. market leadership through their comprehensive hardware and platform offerings.

In June 2024, SAVVY secured third place at the 2024 Swiss Logistics Award Night for its innovative Smart Bogie technology, which collects real-time data from freight wagons through measuring sensors whose advanced algorithms process the data and alert stakeholders to anomalies requiring immediate action. The recognition highlighted the broadening application of smart tracking technology beyond ocean containers into rail freight, demonstrating the cross-modal expansion potential of sensor-based cargo monitoring across the complete intermodal supply chain.

Smart Container Market Segment Analysis

-

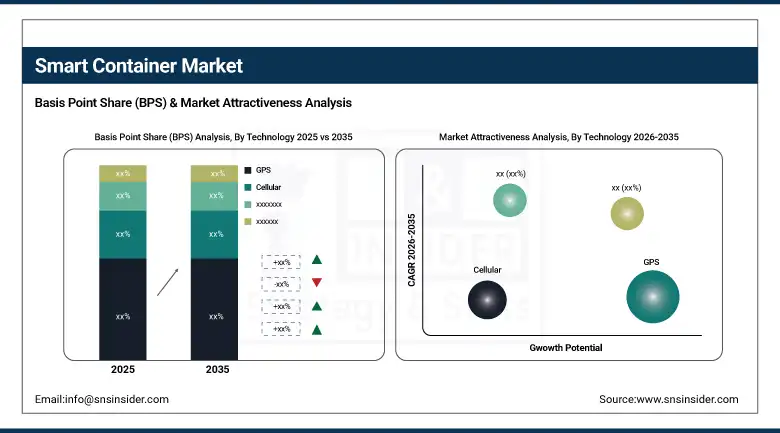

By Technology, the GPS segment dominated the smart container market with approximately 78% share in 2025 through its accuracy in real-time location monitoring, while LoRa WAN is the fastest-growing technology offering cost-effective long-range connectivity.

-

By Application, the asset tracking & management segment dominated the smart container market with approximately 68% share in 2025, while supply chain optimization is the fastest-growing application driven by demand for automated, transparent logistics processes.

-

By Industry Vertical, the food & beverages segment dominated the smart container market with the largest share in 2025 through temperature-controlled shipment requirements, while pharmaceuticals is the fastest-growing vertical driven by GDP-compliant vaccine and biologics shipping.

By Technology, GPS dominates, LoRa WAN grows fastest

GPS retained the dominant technology position with approximately 78% of the smart container market in 2025. Due to the importance of GPS technology in providing the most accurate and real-time monitoring related to container location, speed, and route, GPS integrated with IoT remains the foundational technology enabling the basic visibility function that defines smart container value. With the booming logistics and e-commerce sectors, the need for real-time asset tracking solutions to ensure on-time deliveries, lower operational expenditure, and gain insights on asset utilization continues to add to GPS’s persistent dominance, as virtually every smart container deployment incorporates GPS as its core positioning technology regardless of which supplementary sensor or connectivity technologies accompany it.

LoRa WAN is the fastest-growing technology because its long-range, low-power wide-area network characteristics offer cost-effective connectivity for smart containers operating in remote port, rail yard, and warehouse environments where continuous cellular coverage is unavailable or prohibitively expensive at scale. Each container fleet operator that adopts LoRa WAN gateway infrastructure at major port and terminal facilities creates a connectivity backbone whose lower per-device data transmission cost compared to cellular subscriptions enables economically viable tracking deployment across larger container fleets than cellular-only architectures would support.

By Application, asset tracking dominates, supply chain optimization grows fastest

Asset tracking and management retained the dominant application position with approximately 68% of the smart container market in 2025, driven by the need for real-time visibility and control over in-transit assets. Technologies like GPS, RFID, and IoT sensors enhance tracking, ensuring security, minimizing losses, and improving efficiency. With the rise of logistics and e-commerce, demand for real-time tracking continues to grow, as shipping companies and cargo owners require continuous confirmation of container location and condition status to manage customer service level agreements, customs documentation, and insurance liability throughout the shipment lifecycle.

Supply chain optimization is the fastest-growing application from 2024 to 2032, fueled by the need for efficiency, automation, and transparency. Data from smart containers integrated with IoT sensors, GPS, and live tracking systems yield insights that help businesses streamline logistics and inventory management. Improving visibility throughout the supply chain helps reduce delays, minimize errors, and positively impact overall delivery performance, while AI and predictive analytics enable improved demand forecasting, inventory control, and route optimisation that extends smart container value beyond simple tracking into active logistics decision support.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Smart Container Market Insights

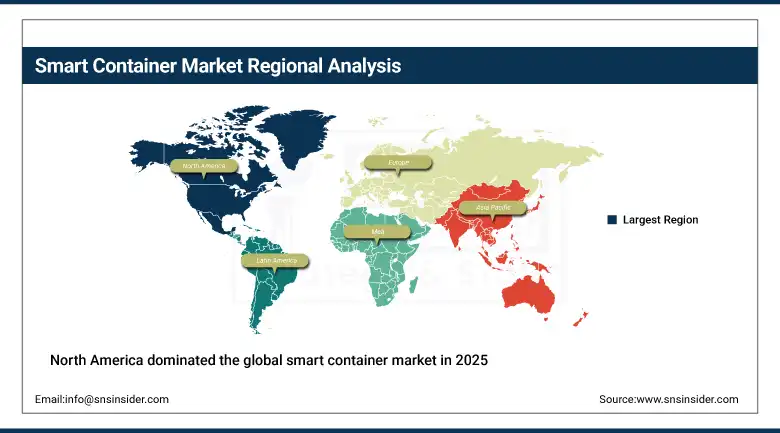

North America dominated the global smart container market in 2025, accounting for around 40% of total revenue, supported by its position as a major global trade hub with extensive import and export activity, advanced logistics infrastructure, and early adoption of IoT-enabled tracking technology among major shipping lines. The United States accounts for approximately 82.5% of North American revenues through Orbcomm, Traxens, and Phillips Connect Technologies’ comprehensive smart container hardware and platform leadership.

Canada contributes supplementary North American revenues through its growing cold chain pharmaceutical distribution sector’s tracking requirements, the cross-border trucking and rail freight sector’s adoption of intermodal tracking solutions, and the agricultural export sector’s growing need for temperature-monitored container shipments serving international markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Smart Container Market Insights

Europe is a significant smart container market where the EU’s Good Distribution Practice requirements for pharmaceutical cold chain shipping, the major port hubs at Rotterdam, Hamburg, and Antwerp’s container throughput, and the region’s advanced logistics technology adoption collectively create substantial smart container demand. Germany accounts for approximately 22.4% of European revenues through its large logistics sector and Hapag-Lloyd’s commercial fleet tracking leadership.

The Netherlands’ Rotterdam port hub’s container throughput volume, France’s pharmaceutical export sector’s cold chain monitoring requirements, and the Nordics’ advanced digital logistics infrastructure collectively sustain European smart container market development. European shipping lines’ progressive fleet-wide tracking deployment commitments create structured technology adoption across the continent’s major maritime trade routes.

Asia Pacific Smart Container Market Insights

Asia Pacific is the fastest-growing regional smart container market, driven by China’s position as the world’s largest container manufacturing and export hub, the expanding e-commerce sector’s growing need for shipment visibility, and increasing regional investment in supply chain digitalisation. China accounts for approximately 44.8% of Asia Pacific revenues through its dominant global container manufacturing base and the world’s busiest container ports.

Japan and South Korea’s advanced electronics manufacturing exports requiring secure tracked shipping, India’s rapidly growing pharmaceutical export sector’s cold chain monitoring needs, and Southeast Asia’s expanding manufacturing and export infrastructure collectively sustain Asia Pacific’s fastest-growing regional trajectory. Government digitalisation initiatives across major Asian ports are accelerating smart container technology integration into national logistics infrastructure.

MEA & Latin America Smart Container Market Insights

The UAE leads MEA revenues through its position as a major global re-export and transshipment hub at Jebel Ali port, the region’s growing pharmaceutical and food import sector’s cold chain requirements, and increasing investment in port digitalization infrastructure. Saudi Arabia’s growing logistics sector under Vision 2030 creates expanding regional demand.

Brazil leads Latin American revenues through its large agricultural and food export sector’s temperature-monitored container requirements, the growing pharmaceutical import market’s cold chain compliance needs, and the expanding port infrastructure investment at Santos and other major Brazilian terminals. Mexico’s cross-border trade with the United States creates substantial secondary regional demand.

Market Dynamics

Growth Drivers: Cold chain pharmaceutical shipping requirements and e-commerce-driven supply chain visibility demand creating structured smart container adoption

The smart container market’s most commercially significant growth driver is the pharmaceutical industry’s structural requirement for Good Distribution Practice-compliant temperature monitoring throughout vaccine, biologics, and other temperature-sensitive medication shipments. IoT and sensor equipment inside smart containers can monitor environmental conditions, optimizing them according to regulatory frameworks in real time and preventing spoilage, creating non-discretionary smart container adoption for the highest-value pharmaceutical cargo categories. Each new biologics or vaccine shipment programme that requires documented continuous temperature monitoring creates smart container procurement whose regulatory compliance value substantially exceeds conventional container economics.

The accelerating growth of global e-commerce and the increasing complexity of multi-leg international supply chains create structural demand for the end-to-end visibility that smart containers provide, where customer expectations for shipment tracking transparency that originated in parcel delivery are progressively extending to ocean freight and bulk cargo shipping. Each major retailer and brand owner whose supply chain transparency commitment requires real-time shipment visibility creates smart container procurement whose adoption rate tracks the broader e-commerce-driven supply chain digitalization trend.

Restraints: High upfront hardware and connectivity costs and cybersecurity vulnerability concerns limiting smart container adoption among smaller logistics operators

Smart container technology’s hardware, sensor, and ongoing cellular or satellite connectivity subscription costs create a substantial per-container cost premium that smaller logistics operators and cargo owners managing lower-margin commodity shipments may find difficult to justify relative to conventional container economics. Each container fleet operator whose capital budget review process applies simple acquisition cost comparison without capturing the full insurance, spoilage prevention, and customer service value of tracking technology creates an adoption decision that favors lower upfront cost over comprehensive lifecycle value.

The cybersecurity vulnerability inherent in connected container systems, whose IoT sensors and cellular gateways create network access points susceptible to data interception, location spoofing, or unauthorized system access, creates security risk management challenges for shipping companies whose container fleets represent valuable cargo and critical infrastructure data. Each cybersecurity incident involving compromised container tracking systems creates industry-wide caution that may delay broader technology adoption among security-conscious logistics operators.

Opportunities: AI-powered predictive analytics integration and blockchain-based supply chain transparency creating premium smart container service categories

The integration of AI-powered predictive analytics with smart container sensor data, enabling automated anomaly alerts, predictive maintenance scheduling, and demand forecasting that extends smart container value beyond passive tracking into active logistics decision support, creates a premium service category whose data analytics value proposition justifies above-commodity pricing for technology-forward shipping lines and logistics providers. Each predictive analytics capability that demonstrably reduces spoilage incidents or improves delivery time accuracy creates measurable ROI that accelerates broader fleet-wide technology adoption.

Blockchain integration for tamper-proof supply chain documentation, whose immutable record of container location, condition, and custody transfer creates verifiable provenance documentation increasingly demanded by regulators and brand owners managing high-value or regulated cargo categories, creates commercial opportunity for smart container providers whose platform capabilities extend into comprehensive supply chain transparency infrastructure beyond basic tracking functionality.

Recent Developments:

-

2024: Hapag-Lloyd and Nexxiot partnered to create the largest connected fleet of smart containers, enabling real-time door-to-door monitoring across over 1 million containers, establishing new industry benchmarks for fleet-wide IoT tracking deployment scale.

-

2024: Hapag-Lloyd expanded its tracking technology deployment to over 1.5 million containers through a collaboration with HERE Tracking, improving inland estimated time of arrival accuracy across worldwide transportation networks for enhanced supply chain visibility.

-

2024: SAVVY secured recognition at the 2024 Swiss Logistics Award Night for its Smart Bogie technology collecting real-time freight wagon sensor data, demonstrating expansion of smart tracking technology beyond ocean containers into rail freight applications.

Smart Container Market Key Players are:

-

Orbcomm Inc.

-

Traxens SA

-

Globe Tracker ApS

-

Phillips Connect Technologies LLC

-

Nexxiot AG

-

Robert Bosch GmbH

-

Ambrosus Technologies GmbH

-

Smart Containers Group AG

-

ZillionSource Technologies LLC

-

SeaLand (CMA CGM)

-

CMA CGM SA

-

A.P. Moller-Maersk A/S

-

Hapag-Lloyd AG

-

Sensitech Inc. (Carrier Global)

-

Emerson Electric Co.

-

ORBCOMM Logistics Solutions

-

Berlinger & Co. AG

-

Controlant ehf.

-

Klinge Corporation

-

Cold Chain Technologies LLC

Smart Container Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.81Billion |

| Market Size by 2035 | USD 30.55 Billion |

| CAGR | CAGR of 18.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (GPS, Cellular, Bluetooth Low Energy, LoRa WAN, Others) • By Component (Hardware, Software, Services) • By Application (Asset Tracking & Management, Supply Chain Optimization, Others) • By Industry Vertical (Food & Beverages, Pharmaceuticals & Healthcare, Logistics & Transportation, Retail & E-commerce, Oil & Gas, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Orbcomm Inc., Traxens SA, Globe Tracker ApS, Phillips Connect Technologies LLC, Nexxiot AG, Robert Bosch GmbH, Ambrosus Technologies GmbH, Smart Containers Group AG, ZillionSource Technologies LLC, SeaLand (CMA CGM), CMA CGM SA, A.P. Moller-Maersk A/S, Hapag-Lloyd AG, Sensitech Inc. (Carrier Global), Emerson Electric Co., ORBCOMM Logistics Solutions, Berlinger & Co. AG, Controlant ehf., Klinge Corporation, and Cold Chain Technologies LLC |

Frequently Asked Questions

The Smart Container Market is expected to grow at a CAGR of 18.06% from 2026 to 2035.

The Smart Container Market was valued at USD 5.81 Billion in 2025.

Cold chain pharmaceutical shipping requirements for GDP-compliant temperature monitoring, e-commerce-driven supply chain visibility demand, growing IoT and sensor technology adoption, and the need for cost-efficient logistics solutions are the primary growth factors.

The Asset Tracking & Management segment dominated the Smart Container Market with approximately 68% share in 2025.

North America dominated the Smart Container Market in 2025, accounting for around 40% of total revenue, supported by its position as a major global trade hub with advanced logistics infrastructure.

Get in Touch