Smart Transformers Market Report Scope & Overview:

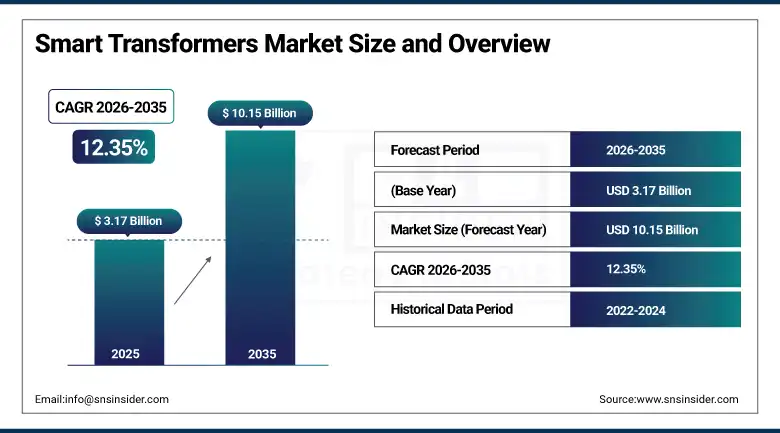

The Smart Transformers Market was valued at USD 3.17 Billion in 2025 and is expected to reach USD 10.15 Billion by 2035, growing at a CAGR of 12.35% from 2026–2035.

The global smart transformers market is growing at an exceptional pace. Smart transformers integrate advanced communication technology, real-time monitoring, and digital control capability with traditional transformer function, enabling adaptive voltage regulation, power quality management, and predictive maintenance that conventional transformers cannot deliver. Power grid technology received USD 87 billion in funding in the U.S. in 2023 alone, while global grid investments exceeded USD 300 billion. Utilities are increasingly focused on improving grid dependability and efficiency as the world shifts to more sustainable energy sources, and smart transformers are essential to this transition.

In April 2024, Hitachi Energy announced a partnership with SP Energy Networks to develop and deploy a power quality solution aimed at increasing grid stability and facilitating renewable energy movement between Scotland and England. The project leverages smart transformer technology to support renewable energy integration, demonstrating the commercial validation of smart transformer infrastructure investment for the specific challenge of accommodating variable renewable generation whose grid integration requires the dynamic voltage management and power quality control that smart transformers provide.

Market Size and Forecast

-

Market Size in 2026E: USD 3.56 Billion

-

Market Size by 2035: USD 10.15 Billion

-

CAGR: 12.35% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Smart Transformers Market - Request Free Sample Report

Smart Transformers Market Trends

-

Smart grid deployment by utilities is creating the primary commercial demand for smart transformers whose bidirectional communication, real-time monitoring.

-

Renewable energy grid integration is creating above-average smart transformer demand as variable solar and wind generation creates voltage fluctuation and power quality challenges.

-

EV charging infrastructure investment is driving smart transformer adoption as high-power charging stations create localised grid demand spikes.

-

Predictive maintenance capability integration is reducing transformer failure-related outage costs as continuous health monitoring identifies degradation patterns weeks before failure events.

-

Digital twin technology integration with smart transformer management systems is enabling virtual simulation of grid scenarios, optimisation of transformer loading.

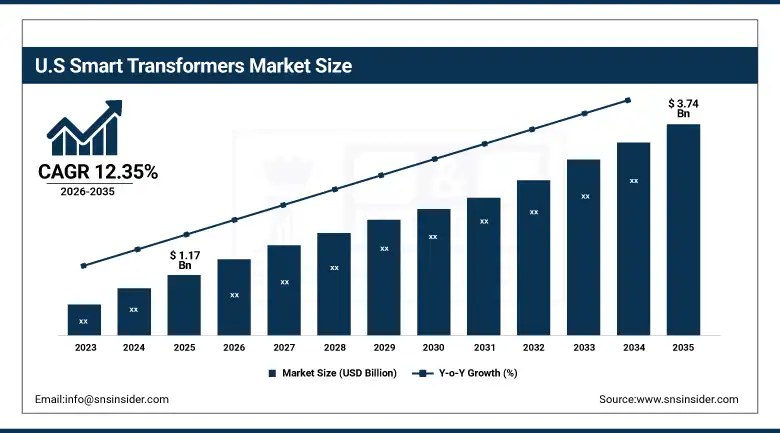

U.S. Smart Transformers Market Outlook

The U.S. Smart Transformers Market was valued at approximately USD 1.17 Billion in 2025 and is expected to reach approximately USD 3.74 Billion by 2035, growing at a CAGR of approximately 12.35%.

The U.S. is the world's largest smart transformers market within North America's approximately 38% global revenue dominance. DOE's USD 62 billion Bipartisan Infrastructure Law grid modernisation investment, the IRA's clean energy tax credit infrastructure, and utility sector's distribution grid upgrade investment collectively create structured institutional procurement. The rapid proliferation of solar installations on distribution networks creates reverse power flow challenges that smart transformers' bidirectional power management uniquely resolves.

In 2025, Schneider Electric enhanced its EcoStruxure Grid automation suite with updated monitoring and control features tailored for modern smart transformer applications. The enhancement enables utilities to integrate smart transformer operational data directly into their distribution management system and SCADA infrastructure, creating a unified digital operational picture whose situational awareness improves grid operator response time to voltage events, transformer loading anomalies, and power quality disturbances.

Smart Transformers Market Segment Analysis

-

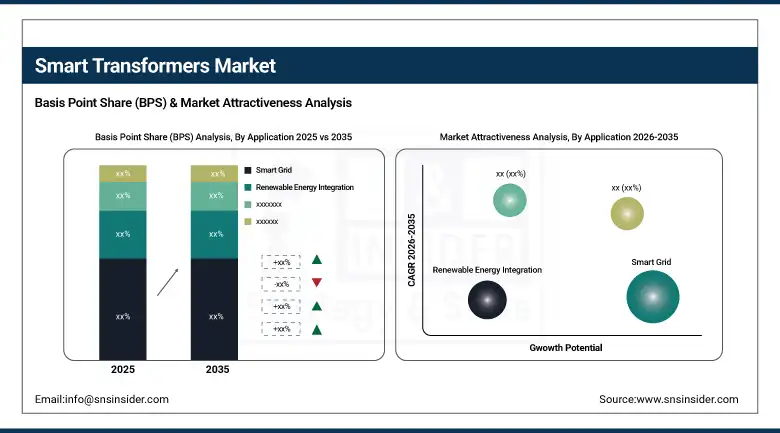

By Application, the Smart Grid segment dominated the Smart Transformers Market with approximately 59% share in 2025, while the Renewable Energy Integration segment is the fastest growing.

-

By Type, the Power/Transmission Transformer segment dominated the Smart Transformers Market in 2025, while the Distribution Transformer segment is the fastest growing with a CAGR of approximately 13.80%.

-

By End User, the Utilities segment dominated the Smart Transformers Market in 2025, while the Industrial segment is the fastest growing.

By Application, smart grid dominates, renewable energy grows fastest

Smart grid retained the dominant application position with approximately 59% of the smart transformers market in 2025. Its commercial primacy reflects the extraordinary scale of global grid modernisation investment whose smart transformer component creates the market's most commercially certain procurement category. Each utility that commits to smart grid deployment creates systematic smart transformer procurement as the foundational power quality and monitoring infrastructure whose capability enables the advanced grid management that smart grid architecture requires. The U.S. DOE's grid investment, European smart grid mandates, and Asian national grid modernisation programmes collectively define a procurement pool whose aggregate value sustains the smart transformer market's above-average growth trajectory.

Renewable energy integration is the fastest-growing application because each percentage point increase in grid-connected solar and wind capacity creates proportional new demand for the voltage regulation and power quality management that smart transformers provide at renewable energy connection points. Solar panel installations create localised reverse power flow whose magnitude overwhelms conventional distribution transformer capacity during peak generation periods, creating operational grid challenges that smart transformer's bidirectional power management and adaptive voltage regulation resolves. Each new solar farm and wind park grid connection creates a smart transformer procurement opportunity whose aggregate commercial scale compounds with renewable energy capacity growth.

By Type, power transformers dominate, distribution grows fastest

Power and transmission transformers retained the dominant type position in the smart transformers market in 2025. Transmission grid smart transformer investment creates the highest per-unit commercial value of any smart transformer category whose large MVA ratings, high voltage operation, and complex grid interconnection functions create procurement relationships whose individual contract values substantially exceed distribution transformer alternatives. Each transmission grid upgrade project creates smart transformer procurement whose engineering specification, factory acceptance testing, and installation commissioning requirements create long-duration commercial relationships between transformer manufacturers and utility customers.

Distribution transformers are the fastest-growing type at approximately 13.80% CAGR because distribution grid modernisation is creating the broadest and most geographically distributed smart transformer procurement opportunity. Each electricity distribution network's progressive smart transformer upgrade programme creates sequential procurement across hundreds or thousands of distribution points whose combined volume creates commercial scale that transmission grid applications cannot match in unit count. The distributed energy resources' integration challenge at the distribution network level creates the most commercially urgent smart transformer requirement whose resolution requires distribution-level voltage management that conventional distribution transformers cannot provide.

By End User, utilities dominate, industrial grows fastest

Utilities retained the dominant end user position in the smart transformers market in 2025. The electricity distribution and transmission system's comprehensive dependence on transformer infrastructure creates utilities as the most commercially certain and largest-volume smart transformer customer segment. Each utility's grid modernisation programme creates systematic smart transformer procurement whose multi-year project timeline creates visible forward order books that sustain transformer manufacturer production planning. Regulatory rate-base treatment of smart grid infrastructure investment in most regulatory jurisdictions creates investment certainty that utility procurement decisions benefit from.

Industrial is the fastest-growing end user because manufacturing facilities, data centres, and process plants are adopting smart transformers for power quality management and predictive maintenance whose operational benefit is measurable in reduced downtime cost and energy efficiency improvement. Data centre operators whose entire revenue depends on continuous power availability are particularly motivated to adopt smart transformer monitoring capability whose early warning of thermal degradation, insulation resistance decline, and dissolved gas anomalies enables planned maintenance that prevents unplanned outages whose financial impact substantially exceeds transformer replacement cost.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Smart Transformers Market Insights

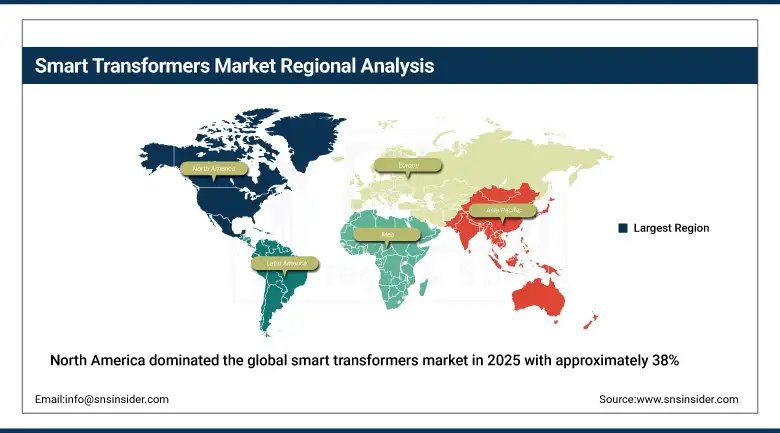

North America dominated the global smart transformers market in 2025 with approximately 38% of global revenues. The United States accounts for approximately 87.4% of North American revenues through its combination of the world's most advanced smart grid investment programme, the highest utility investment in distribution grid modernisation, and the commercial presence of ABB, Siemens, Eaton, and Schneider Electric's operations. The DOE's USD 87 billion grid investment in 2023 alone creates the commercial certainty that sustains smart transformer procurement planning across the U.S. utility sector.

Canada contributes approximately 12.6% of North American revenues through its utility sector's grid modernisation investment, renewable energy integration requirements, and the federal government's clean electricity infrastructure investment that creates structured smart transformer procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Smart Transformers Market Insights

Europe is a technically sophisticated smart transformers market where the EU's clean energy transition, ENTSO-E's transmission grid investment requirements, and national distribution network operators' smart grid deployment programmes create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its energy transition's (Energiewende) extraordinary renewable energy integration challenge whose distribution grid voltage management requirements create above-average smart transformer demand.

The United Kingdom and France are significant secondary European markets where National Grid's transmission investment, SP Energy Networks' smart transformer partnership with Hitachi Energy, and the distribution network operators' smart grid programmes create consistent procurement. The UK's electricity system operator's smart grid investment and France's RTE transmission modernisation programme create complementary procurement environments whose combined scale sustains European market growth.

Asia Pacific Smart Transformers Market Insights

Asia Pacific is the fastest-growing regional smart transformers market at approximately 14.54% CAGR, driven by China's extraordinary grid investment, India's RDSS smart grid programme, and Southeast Asia's urbanisation and power infrastructure development. China accounts for approximately 44.8% of Asia Pacific revenues through State Grid Corporation and China Southern Grid's systematic smart transformer deployment as part of China's ultra-high voltage transmission and smart distribution grid investment programme.

India represents the most commercially dynamic emerging market within Asia Pacific, where the RDSS (Revamped Distribution Sector Scheme) programme's USD 26 billion investment in distribution network modernisation creates structured smart transformer procurement whose scale reflects India's 300 million electricity consumer infrastructure upgrade ambition.

MEA & Latin America Smart Transformers Market Insights

The Middle East and Africa and Latin America are growing smart transformers markets where renewable energy investment, grid modernisation, and industrial development create structured demand. UAE leads MEA revenues at approximately 38.4% through its smart city grid infrastructure, the Emirates's renewable energy programme whose solar park grid connections require smart transformer voltage management, and DEWA's grid modernisation investment.

Brazil leads Latin American revenues at approximately 44.2% through its power utility sector's grid modernisation investment, the renewable energy sector's wind and solar grid integration requirements, and ANEEL's distribution network modernisation regulation creating compliance-driven smart transformer procurement.

Market Dynamics

Growth Drivers: Smart grid modernisation investment and renewable energy grid integration creating structured demand

Smart grid modernisation investment is the smart transformers market's most commercially certain structural growth driver. Global grid investments exceeding USD 300 billion annually create the procurement environment within which smart transformers represent the foundational intelligent grid infrastructure whose deployment enables the advanced grid management that smart grid architecture requires. Each utility that commits to a smart grid roadmap creates systematic smart transformer procurement whose multi-year project pipeline provides commercial predictability that sustains manufacturer investment in smart transformer product development and production capacity.

Renewable energy grid integration is simultaneously creating the most operationally urgent application for smart transformer capability. Solar and wind energy's variable generation creates voltage fluctuations, frequency deviations, and reverse power flows that conventional grid infrastructure was not designed to manage. Smart transformers' real-time voltage regulation, reactive power compensation, and bidirectional power management create grid stability at renewable energy connection points that conventional transformers cannot achieve, creating a technically non-discretionary requirement for smart transformer deployment wherever high renewable energy penetration creates grid management challenges.

Restraints: High initial cost versus conventional transformers and cybersecurity vulnerability of connected smart transformers

Smart transformers' 30-50% premium over conventional transformer alternatives creates procurement resistance in utility and industrial environments whose capital budget cycles extend from 5-10 years and whose return on investment analysis must demonstrate economic benefit within regulatory rate-base and internal hurdle rate constraints. Emerging market utilities whose tariff revenue structures cannot fully fund smart infrastructure investment face the most significant smart transformer capital cost barrier whose resolution requires government funding support or concessional financing.

Cybersecurity vulnerability of IIoT-connected smart transformers creates infrastructure risk concerns that slow adoption in critical grid environments. Each smart transformer connected to the utility's communication network creates a potential attack surface for grid disruption whose consequences include regional blackouts. National grid operators' zero tolerance for critical infrastructure cyber risk creates extensive cybersecurity validation requirements that extend smart transformer procurement timelines and add engineering cost beyond the transformer hardware itself.

Opportunities: EV charging infrastructure and emerging market grid electrification creating new commercial categories

EV charging infrastructure investment represents the most commercially dynamic near-term growth opportunity for smart transformers. High-power DC fast charging stations consuming 150-350 kW per charger create localised grid loading whose management requires smart transformer voltage regulation at the distribution connection point. Each new EV charging hub creates smart transformer procurement that compounds with the extraordinary pace of EV infrastructure investment. Grid operators and charging network operators are progressively recognising smart transformer specification as essential infrastructure for charging network grid integration whose reliability standards justify intelligent transformer specification.

Emerging market grid electrification represents the most commercially significant long-term growth opportunity whose scale reflects the hundreds of millions of people in Africa, South Asia, and Southeast Asia whose grid connection requires distribution infrastructure investment. Each new grid electrification project represents a greenfield opportunity where smart transformer specification from initial deployment captures the operational benefits of intelligent monitoring without the retrofit complexity that upgrading existing infrastructure imposes.

Recent Developments:

-

2024: Hitachi Energy announced a partnership with SP Energy Networks in April 2024 to develop and deploy a power quality solution using smart transformer technology for grid stability and renewable energy movement between Scotland and England, targeting the specific voltage management challenge of high renewable energy penetration in regional transmission networks.

-

2025: Schneider Electric enhanced its EcoStruxure Grid automation suite in 2025 with updated monitoring and control features for smart transformer applications, enabling utilities to integrate smart transformer operational data directly into distribution management systems and SCADA infrastructure.

-

2024: ABB launched its advanced smart transformer monitoring platform in 2024 featuring dissolved gas analysis, bushing monitoring, and load tap changer diagnostics integrated with ABB Ability PGIM cloud software, enabling utilities to manage transformer fleet health from a centralised digital platform and predict maintenance requirements weeks before failure events.

Smart Transformers Market Key Players

-

ABB Ltd.

-

Siemens AG

-

Schneider Electric

-

Eaton Corporation

-

General Electric

-

Mitsubishi Electric Corporation

-

Hitachi Energy

-

Toshiba Corporation

-

TBEA Co., Ltd.

-

Baoding Tianwei Group

-

Sieyuan Electric

-

CHINT Group

-

S&C Electric Company

-

Weidmann Electrical Technology

-

Wilson Transformer Company

-

Voltamp Transformers

-

Howard Industries

-

Efacec

-

SPX Transformer Solutions

-

Grid Solutions

Smart Transformers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.17 Billion |

| Market Size by 2035 | USD 10.15 Billion |

| CAGR | CAGR of 12.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Power/Transmission Transformer, Distribution Transformer, Traction Transformer) • by Application (Smart Grid, Renewable Energy Integration, EV Charging Infrastructure, Industrial Power Management, Others) • by End User (Utilities, Industrial, Commercial, Residential) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Siemens AG, Schneider Electric, Eaton Corporation, General Electric, Mitsubishi Electric Corporation, Hitachi Energy, Toshiba Corporation, TBEA Co., Ltd., Baoding Tianwei Group, Sieyuan Electric, CHINT Group, S&C Electric Company, Weidmann, Electrical Technology, Wilson Transformer Company, Voltamp Transformers, Howard Industries, Efacec, SPX Transformer Solutions, Grid Solutions |

Frequently Asked Questions

The Smart Transformers Market is expected to grow at a CAGR of 12.35% from 2026 to 2035.

The Smart Transformers Market was valued at USD 3.17 Billion in 2025.

Smart grid modernisation investment by utilities globally creating systematic intelligent transformer procurement, and renewable energy grid integration creating technically non-discretionary smart transformer requirements at solar and wind energy connection points whose variable generation creates voltage management challenges that conventional transformers cannot resolve.

Smart Grid dominated the Smart Transformers Market with approximately 59% share in 2025, while the Distribution Transformer type is the fastest growing with a CAGR of approximately 13.80%.

North America dominated the Smart Transformers Market in 2025 with approximately 38% of global revenues, while Asia Pacific is the fastest-growing region with a CAGR of approximately 14.54%.

Get in Touch