Specialty paper Market Report Scope & Overview:

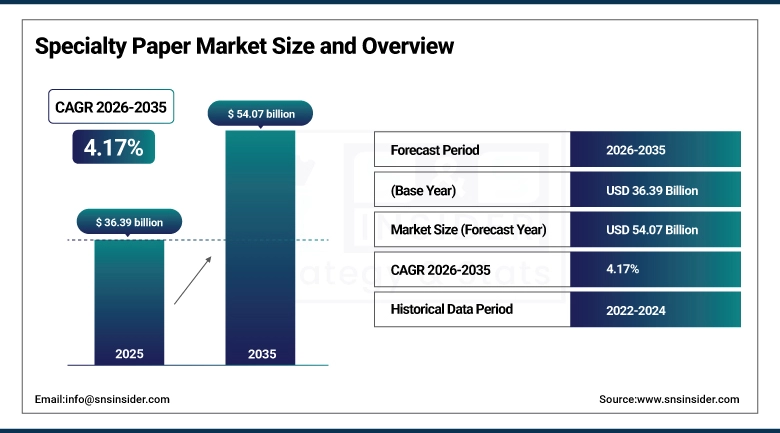

The Specialty Paper Market was valued at USD 36.39 billion in 2025 and is expected to reach USD 54.07 billion by 2035, growing at a CAGR of 4.17% from 2026–2035.

The Specialty Paper Market is experiencing a continuous rise due to the growing demands for sustainable packaging solutions, increased adoption of environmentally friendly label options, and growing uses in various segments like the food service industry, healthcare industry, electronic sector, and consumer packaging industry. The growing regulatory restrictions on single-use plastics, along with the rising consumer inclination towards the adoption of recyclable and biodegradable paper products, is considerably contributing to the faster adoption of specialty paper products worldwide.

Recent developments include strategic investments by leading paper manufacturers in recyclable barrier-coated papers, fiber-based flexible packaging, and low-carbon specialty paper production technologies. Companies such as Mondi plc, Stora Enso Oyj, and UPM-Kymmene Corporation are expanding sustainable packaging paper capacities and introducing advanced specialty grades for food-contact and industrial applications.

Specialty paper Market Size and Forecast

-

Market Size in 2025: USD 36.39 Billion

-

Market Size by 2035: USD 54.07 Billion

-

CAGR: 4.17% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Specialty Paper Market - Request Free Sample Report

Specialty paper Market Trends

-

Rising adoption of sustainable and recyclable specialty paper solutions is accelerating replacement of plastic-based packaging materials globally.

-

Increasing demand for barrier-coated and food-grade specialty papers is driving innovation in eco-friendly packaging applications.

-

Rapid expansion of e-commerce and premium consumer packaging is boosting demand for high-performance labeling and packaging papers.

-

Growing adoption of digital printing-compatible specialty papers is enhancing print quality, customization, and branding capabilities.

-

Increasing investments in recycled fiber processing and low-carbon paper manufacturing technologies are strengthening sustainable production capacity.

-

Rising utilization of lightweight and high-durability specialty papers is expanding applications across healthcare, electronics, and industrial sectors.

-

Expanding integration of automation and smart mill technologies is improving operational efficiency and product consistency in specialty paper manufacturing.

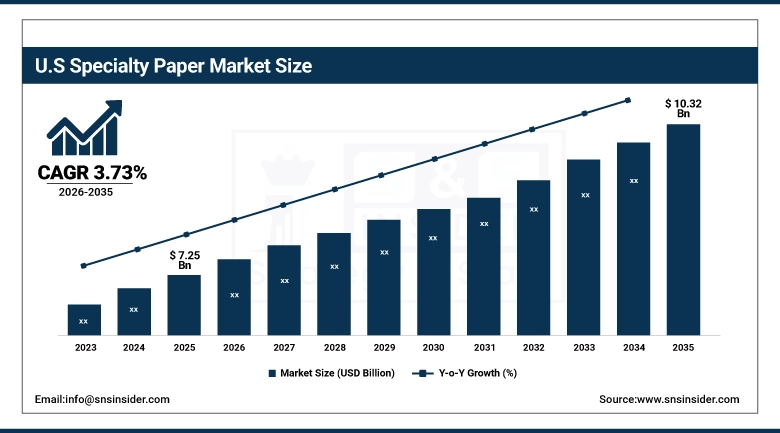

The U.S. Specialty Paper Market was valued at USD 7.25 billion in 2025 and is expected to reach around USD 10.32 billion by 2035, growing at a CAGR of 3.73% from 2026–2035.

The United States leads as the major market for specialty paper in the region, attributed to the growing need for sustainable packaging materials, increased utilization of high-quality label printing options, and the availability of highly developed paper production facilities. The growth of the market is further fueled by the increasing demands for e-commerce packaging, the growing use of recyclable food service papers, and increased investment in sustainable packaging options.

Additionally, recent developments such as International Paper Company expanding sustainable packaging solutions and Mondi plc increasing investments in high-performance recyclable specialty paper products are reinforcing long-term market expansion and accelerating innovation in the U.S. specialty paper industry.

Specialty paper Market Segment Highlights

-

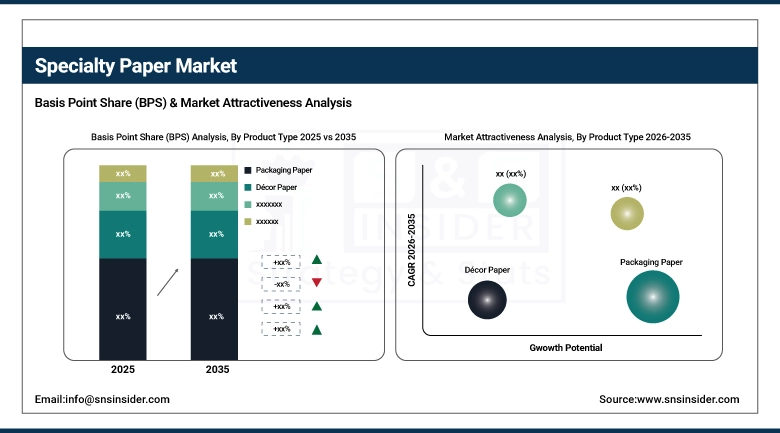

By Product Type, Packaging Paper dominated the Specialty Paper Market with 28.36% share in 2025; Packaging Paper fastest growing CAGR.

-

By Raw Material, Pulp-Based Specialty Paper dominated the Specialty Paper Market with 42.35% share in 2025; Recycled Fiber-Based Paper fastest growing at CAGR.

-

By Application, Packaging & Labeling dominated the Specialty Paper Market with 36.45% share in 2025; Food Service fastest growing CAGR.

-

By End-Use Industry, Packaging Industry dominated the Specialty Paper Market with 34.24% share in 2025; Retail & E-Commerce fastest growing CAGR.

-

By Distribution Channel, Direct Sales dominated the Specialty Paper Market with 37.51% share in 2025; Online Sales Channels fastest growing CAGR.

By Product Type, Packaging Paper segment dominates the Specialty Paper Market, Décor Paper expected to grow fastest

In 2025, the Packaging Paper segment maintained its dominant position in the Specialty Paper Market, accounting for 28.36% of total revenue. This leadership is primarily driven by rising demand for sustainable flexible packaging solutions, increasing replacement of plastic-based packaging materials, and strong adoption of recyclable specialty papers across food, beverage, retail, and e-commerce industries.

From 2026 to 2035, the Décor Paper segment is projected to record the highest CAGR. This rapid growth is driven by increasing demand for premium interior furnishing materials, rising residential and commercial construction activities, and expanding applications in laminates, furniture surfaces, and decorative panelling solutions.

By Raw Material, Pulp-Based Specialty Paper segment dominates the Specialty Paper Market, Recycled Fiber-Based Paper expected to grow fastest

The Pulp-Based Specialty Paper segment held the largest share of 42.35% in 2025, as a result of its extensive usage for high-end packaging, labeling, printing, and industrial purposes within the paper industry. High levels of raw material availability, printability, and durability attributes have played an important role in this regard.

The Recycled Fiber-Based Paper segment is expected to register the highest CAGR of during the 2026–2035 forecast period. Factors fueling growth include increased sustainable practices, tighter regulations surrounding the use of plastic, and investments in technology associated with the production of paper using circular economy principles. Other growth factors include greater demand for recyclable packaging solutions and the ability to process recycled fibers better.

By Application, Packaging & Labeling segment dominates the Specialty Paper Market, Food Service expected to grow fastest

The Packaging & Labeling segment accounted for the largest market share of 36.45% in 2025, backed by healthy growth in demand for premium label stock, sustainable retail packagings, and high-quality paper-based brand marketing products. Growth in the use of e-commerce, packaged consumer goods, and food delivery systems has greatly boosted the consumption of high-barrier, printable, and durable paper packaging products.

The Food Service segment is projected to witness the fastest CAGR from 2026 to 2035. The major factors driving this growth include the rising demand for eco-friendly food packaging solutions, biodegradable food wrapping paper, and sustainable packaging solutions among quick-service food chains. There is also an increase in regulatory initiatives to minimize plastic consumption coupled with consumers’ preference towards eco-friendly food contact materials.

By End-Use Industry, Packaging Industry segment dominates the Specialty Paper Market, Retail & E-Commerce segment expected to grow fastest

In 2025, the Packaging Industry segment maintained its dominant position in the Specialty Paper Market, accounting for 34.24% of total revenue. This market dominance is backed by a growing need for sustainable packaging products, replacing plastic-based packaging products, and a rise in the use of advanced papers for packaging applications. Companies are turning toward utilizing advanced paper solutions that are lightweight and durable, thereby providing better packaging options and adhering to environmental requirements, thus supporting their dominance in the market segment.

From 2026 to 2035, the Retail & E-Commerce segment is projected to record the highest CAGR.

By Distribution Channel, Direct Sales segment dominates the Specialty Paper Market, Online Sales Channels segment expected to grow fastest

The Direct Sales segment maintained the highest share of 37.51% in 2025. Such domination is characterized by long-term contracts entered into between specialty paper producers and high-volume purchasers of the latter's products who need special requirements fulfilled. Big purchasers have a tendency to buy directly from the suppliers since such companies are capable of offering customizing options associated with their products’ barrier properties, printability, durability, and eco-friendliness.

The Online Sales Channels segment is projected to achieve the highest growth rate during 2026–2035.

Specialty paper Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

34.39% |

|

Europe |

Germany |

26.69% |

|

Asia Pacific |

China |

41.19% |

|

Middle East & Africa |

UAE |

21.34% |

|

Latin America |

Brazil |

39.64% |

Europe Specialty Paper Market Insights

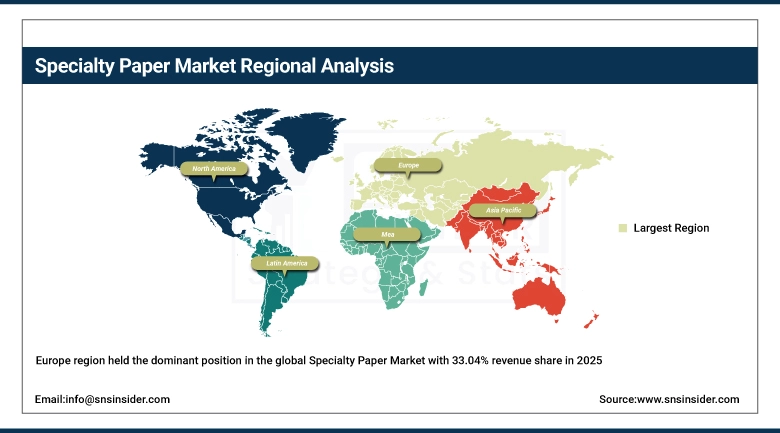

Europe region held the dominant position in the global Specialty Paper Market with 33.04% revenue share in 2025 because of its robust sustainability policies, effective recycling framework, and extensive use of green packaging materials. Nations including Germany, France, Italy, United Kingdom, and Nordic countries have taken the lead in adopting sustainable specialty papers, especially for food packaging, labels, and industries.

Stora Enso Oyj strengthened investments in renewable fiber-based materials and high-performance specialty paper innovation for premium packaging applications.

Additionally, increasing investments in plastic-free packaging innovation, growth in premium consumer packaging demand, and advancements in high-barrier specialty paper technologies are reinforcing Europe’s role as a major innovation-driven specialty paper market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Specialty Paper Market Insights

The continent of North America adopts a model of operations that facilitates innovations in sustainable packaging solutions, sophisticated paper processing technology, and stringent regulations to reduce plastic waste generation in both industrial and domestic operations. In North America, the market has access to some of the biggest players in the specialty paper industry, high adoption of sustainable packaging products, and increasing consumer demand for quality label and foodservice paper products. In the market for high-quality specialty papers, North America enjoys significant dominance from the USA owing to increasing investments in sustainable packaging initiatives and e-commerce logistics services.

International Paper Company announced expansion of its sustainable packaging and specialty paper conversion operations to strengthen recyclable packaging supply across North America.

Domtar Corporation increased investments in fiber optimization and low-emission paper manufacturing technologies to improve production efficiency and sustainability performance.

Asia Pacific Specialty Paper Market Insights

The Asia Pacific region is projected to register the highest CAGR of 5.80% from 2026–2035, Driven by quick industrialization, increased consumption of packaged foods, and strong development in e-commerce and consumer goods industries. Countries like China, India, Japan, South Korea, and Indonesia are fast emerging as key contributors to specialty papers' demand, with China and India emerging as leading countries in green packing material, food-grade papers, and paper converting facilities.

Oji Holdings Corporation expanded specialty packaging paper production capacities across Asia to support rising demand from food delivery and e-commerce industries.

Asia Pulp & Paper (APP) Sinar Mas accelerated investments in recyclable barrier paper solutions and advanced recycled fiber processing facilities in Southeast Asia.

Latin America, Middle East & Africa (LAMEA) Specialty Paper Market Insights

The LAMEA region is seeing a consistent increase in the demand for specialty paper as a result of increased consumption of packaged foods, development of retail sector facilities, and usage of eco-friendly packaging materials. Among some of the important economies making contributions to the increasing demand include Brazil, Mexico, the UAE, Saudi Arabia, and South Africa.

JK Paper Ltd. increased exports of specialty packaging and food-grade paper products to Middle Eastern and African packaging converters to strengthen regional supply capabilities.

In addition, increasing partnerships between global specialty paper manufacturers and regional packaging converters are improving supply chain accessibility, strengthening local production capabilities, and expanding adoption of specialty paper solutions across emerging consumer and industrial markets.

Specialty paper Market Growth Drivers:

-

Rising demand for sustainable packaging, e-commerce expansion, and regulatory shift toward plastic-free materials is driving strong growth in the global Specialty Paper Market

The major structural force impacting the Specialty Paper Market is the fast-changing trend towards the adoption of high-quality and sustainable paper-based products within the areas of packaging, labeling, foodservice, and industry use. As governments and companies are adopting stringent policies regarding the use of single-use plastics, they are moving to specialty papers that comply with environmental requirements while providing high quality.

Additionally, strategic innovation initiatives by leading manufacturers such as International Paper Company, Mondi plc, and Stora Enso Oyj are accelerating the development of lightweight recyclable packaging papers, plastic-free flexible packaging alternatives, and high-performance functional papers with improved strength, printability, and barrier properties—strengthening long-term adoption across global industrial and consumer packaging ecosystems.

Specialty paper Market Restraints:

-

Fluctuating raw material prices, supply chain inefficiencies, and high production complexity are constraining margin expansion in the global Specialty Paper Market

The first limitation in the Specialty Paper Market is the rising variability in major raw material inputs like pulp, recycled fibers, chemicals, and coating substances, affecting production and cost dynamics. The latter is augmented by disruption in global logistics, fluctuating energy prices, and inconsistent availability of quality fibers, posing challenges to long-term sourcing strategies for companies. On the other hand, specialty papers need extensive customization in applications like packaging, labeling, food-grade use, and industry sectors, thus complicating processes and limiting efficiencies.

Specialty paper Market Opportunities:

-

Rapid expansion of sustainable packaging ecosystems, premium branding requirements, and high-performance functional paper applications is creating strong opportunities for innovation-led growth in the global Specialty Paper Market

Among the major opportunities in the Specialty Paper Market is the rapid trend towards advanced value-added and application-oriented paper products that move beyond standard packaging to offer greater functionality, including moisture resistance, grease resistance, heat resistance, and superior printing performance. With an increasing focus by various industries on brand positioning and customer experience, specialty papers are gaining traction as an important component in premium packaging, labeling, and visual marketing efforts. The rising influence of e-commerce, direct consumer sales, and organized retailing channels is further boosting the demand for custom packaging, wherein specialty paper becomes a vital element in the process of improving product presentation.

Recent Developments:

-

2026: International Paper Company expanded its North American specialty packaging and functional paper production capacity with enhanced fiber-recycling and coating technology integration, aimed at scaling demand for recyclable barrier papers used in e-commerce and food packaging applications.

-

2026: Mondi plc strengthened its sustainable packaging portfolio by advancing water-based barrier coating technologies for flexible and specialty paper-based packaging solutions, reducing dependency on plastic laminates across food and consumer goods applications in Europe.

-

2025: Stora Enso Oyj enhanced its renewable fiber-based material portfolio by launching upgraded high-strength specialty paper grades designed for premium packaging, labeling, and industrial applications, improving recyclability and performance efficiency.

-

2025: Nippon Paper Industries Co., Ltd. expanded its advanced functional paper production capabilities in Asia, focusing on heat-resistant, grease-resistant, and biodegradable specialty paper solutions to support growing demand from food service and retail packaging sectors.

Specialty paper Market Key Players

Some of the Specialty paper Market Companies

-

International Paper Company

-

Mondi plc

-

Stora Enso Oyj

-

Nippon Paper Industries Co. Ltd.

-

Oji Holdings Corporation

-

UPM-Kymmene Corporation

-

SAPPI Limited

-

Domtar Corporation

-

Ahlstrom Corporation

-

Fedrigoni S.p.A.

-

Smurfit WestRock Corporation

-

ITC Limited (Paperboards & Specialty Papers Division)

-

Koehler Paper SE

-

LINTEC Corporation

-

Billerud AB

-

Asia Pulp & Paper (APP) Sinar Mas

-

Twin Rivers Paper Company LLC

-

Nordic Paper Holding AB

-

Delfort Group AG

-

JK Paper Ltd.

Specialty paper Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 36.39 Billion |

| Market Size by 2035 | USD 54.07 Billion |

| CAGR | CAGR of 4.17 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Décor Paper, Release Liner Paper, Packaging Paper, Label Paper, Thermal Paper, Others) • By Raw Material (Pulp-Based Specialty Paper, Recycled Fiber-Based Paper, Synthetic Fiber-Based Paper, Mineral/Filler-Based Paper, Composite Specialty Paper) • By Application (Packaging & Labeling, Printing & Publishing, Food Service, Electrical & Electronics, Healthcare & Hygiene) • By End-Use Industry (Packaging Industry, Food & Beverage, Healthcare & Pharmaceuticals, Retail & E-Commerce, Electronics Industry) • By Distribution Channel (Direct Sales, Distributors & Wholesalers, Specialty Retailers, Online Sales Channels, Institutional Procurement) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | International Paper Company, Mondi plc, Stora Enso Oyj, Nippon Paper Industries Co. Ltd., Oji Holdings Corporation, UPM-Kymmene Corporation, SAPPI Limited, Domtar Corporation, Ahlstrom Corporation, Fedrigoni S.p.A., Smurfit WestRock Corporation, ITC Limited (Paperboards & Specialty Papers Division), Koehler Paper SE, LINTEC Corporation, Billerud AB, Asia Pulp & Paper (APP) Sinar Mas, Twin Rivers Paper Company LLC, Nordic Paper Holding AB, Delfort Group AG, JK Paper Ltd. |

Frequently Asked Questions

Europe dominated the Specialty paper Market in 2025.

The Packaging Paper segment dominated the Specialty paper Market in 2025.

The market is primarily driven by rising demand for sustainable packaging solutions, increasing e-commerce activities, and growing adoption of biodegradable and recyclable paper materials across packaging and labeling applications.

The Specialty paper Market was valued at USD 36.39 billion in 2025.

The Specialty paper Market is expected to grow at a CAGR of 4.17% from 2026 to 2035.

Get in Touch