Spring Water Market Report Scope & Overview:

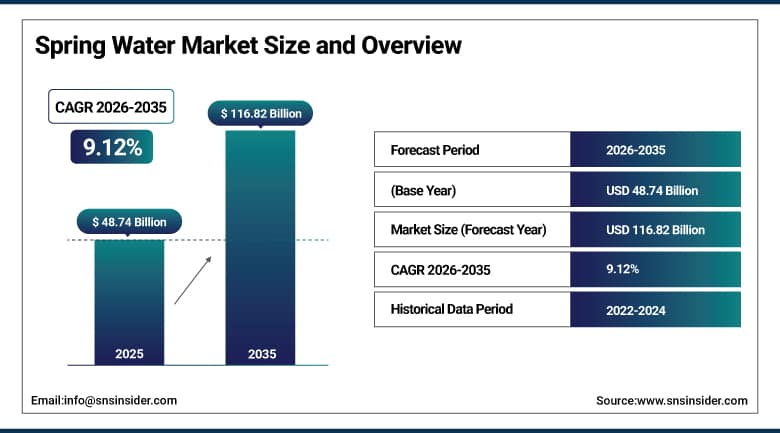

The Spring Water Market was valued at USD 48.74 Billion in 2025 and is expected to reach USD 116.82 Billion by 2035, growing at a CAGR of 9.12% from 2026 to 2035.

Spring water is a particularly commercially advantaged category within the wider world market for packaged beverages, driven by the confluence of the trends toward health and wellness consumption, source-based premiumization, and the structural shift away from sugary carbonated beverages which has caused the beverage purchasing dollars of the consumer base to move toward hydration beverages. The inherent strengths in the concept of spring water include its natural origin from groundwater wells, its composition in terms of minerals, which distinguishes it from purified bottled water, and its association with quality brands which have been built based on decades of steady investment in their branded and source storytelling. The category itself is extremely diverse, ranging from low-cost, generic brands of PET-bottled spring water available in large mass distribution channels to luxury heritage brands like Voss, Acqua Panna, and S Pellegrino, which sell in higher-end, glass-packaged formats catering to premium hotel chains, high-end restaurants, and exclusive retail markets at prices per liter which produce outstanding per unit margins.

Evian, owned by Danone, unveiled a premium line of spring water packaged in 100% recycled glass bottles in February 2025, targeting the luxury hospitality, airline business class, and premium retail segments were packaging quality signals brand prestige and environmental commitment simultaneously.

Market Size and Forecast

-

Market Size in 2026E: USD 53.18 Billion

-

Market Size by 2035: USD 116.82 Billion

-

CAGR: 9.12% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get More Information On Spring Water Market - Request Free Sample Report

Spring Water Market Trends

-

Consumers are increasingly shifting from sugary soft drinks and energy beverages toward natural spring water, driving strong global demand growth.

-

Premium and ultra-premium spring water brands are gaining popularity due to rising consumer preference for source authenticity and sustainable packaging.

-

Sustainable packaging innovations such as rPET bottles, lightweight packaging, and recyclable materials are reshaping the spring water industry.

-

Sparkling spring water demand is increasing as consumers seek healthier alternatives to carbonated soft drinks without sugar or artificial additives.

-

Direct-to-consumer subscription and home delivery models are expanding rapidly, supporting recurring revenue opportunities for spring water brands.

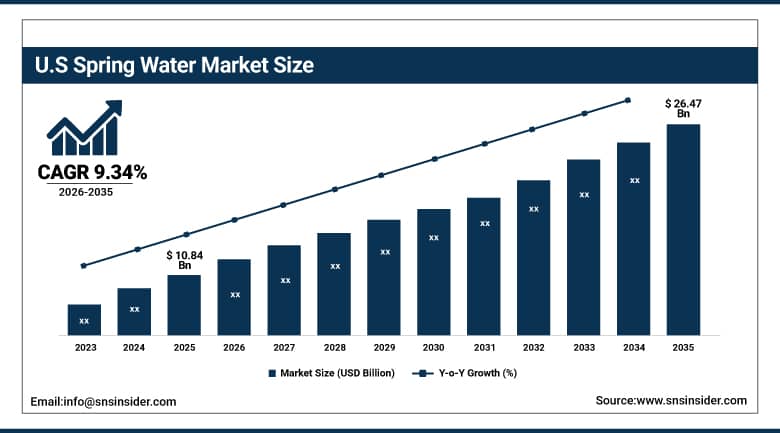

The U.S. Spring Water Market Outlook

The U.S. Spring Water Market was valued at approximately USD 10.84 Billion in 2025 and is expected to reach approximately USD 26.47 Billion by 2035, growing at a CAGR of approximately 9.34%.

The U.S. Spring Water Market is expanding owing to the growing consumer inclination towards healthful and natural beverages as against sugar-laden soft and energy drinks. Increased health consciousness and hydration demand, along with a growing preference for products with clean labels, are driving up the consumption of spring water products in the U.S. Premium and flavored sparkling spring water products have started gaining popularity with health-conscious consumers looking for healthy and calorie-free beverage options. Sustainability practices involving use of recyclable packages and environmentally friendly bottles are also playing a role in purchase decisions. Furthermore, growing retail presence and online delivery of beverages and increased demands in office, gymnasiums, and hospitality sectors are aiding the U.S. spring water market growth.

Primo Water Corporation, which operates one of North America's largest direct-to-consumer bottled spring and purified water delivery networks, completed strategic route optimization investments in 2025 that improved delivery efficiency and expanded its customer base across suburban U.S. markets by 14% year over year.

Spring Water Market Segment Analysis

-

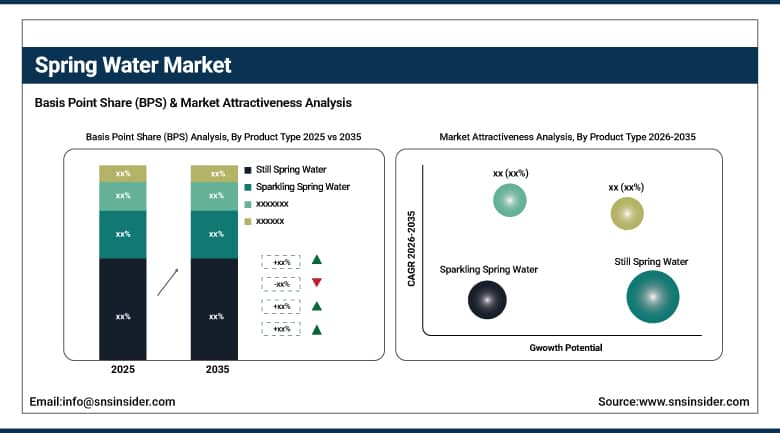

By Product Type, the still spring water segment dominated the spring water market with 72.48% share in 2025, while the sparkling spring water segment is the fastest growing product type during 2026 to 2035.

-

By Packaging Type, the pet bottles segment dominated the spring water market with 64.82% share in 2025, while the aluminium cans segment is the fastest growing packaging type during 2026 to 2035.

-

By Distribution Channel, the hypermarkets & supermarkets segment dominated the spring water market with 48.74% share in 2025, while online retail is the fastest growing distribution channel during 2026 to 2035.

-

By End User, the household/retail consumers segment dominated the spring water market with 62.36% share in 2025, while the food service & hospitality segment is the fastest growing end user during 2026 to 2035.

By Product Type, still spring water dominates, sparkling spring water grows fastest

Still spring water retained the dominant product position with 72.48% of market revenue in 2025. Its commercial dominance reflects universal hydration applicability across all consumption occasions, demographic segments, and geographic markets that positions plain still spring water as the broadest accessible category in the global packaged beverages market.

Sparkling spring water is growing fastest as the structural decline of sugary carbonated soft drinks has expanded the addressable market for carbonated alternatives that deliver the sensory experience of fizz without sugar, artificial sweeteners, or synthetic flavourings. San Pellegrino, Perrier, Gerolsteiner, and LaCroix have successfully positioned sparkling spring water as a premium everyday beverage.

By Packaging Type, PET bottles dominate, aluminium cans grow fastest

PET bottles retained the dominant packaging position with 64.82% of spring water revenue in 2025. PET's combination of transparency that communicates product clarity, lightweight shatter-resistance for portable consumption occasions, and cost-competitive production economics make it the commercially preferred spring water packaging format across mass market and premium mainstream positioning tiers globally.

Aluminium cans are the fastest-growing packaging format, driven by their superior recyclability credentials, premium aesthetic presentation, and growing adoption by spring water brands targeting environmentally conscious younger adult consumers who associate aluminium cans with sustainability and contemporaneous brand positioning. The rapidly growing single-serve sparkling spring water segment is driving aluminium can volume growth disproportionately as the format's carbonation retention properties and premium shelf presence make it the preferred packaging choice for retail and food service sparkling water positioning.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Europe |

Germany |

28.47% |

|

North America |

United States |

84.73% |

|

Asia Pacific |

China |

34.82% |

|

Middle East & Africa |

UAE |

26.48% |

|

Latin America |

Brazil |

42.73% |

Europe Spring Water Market Insights

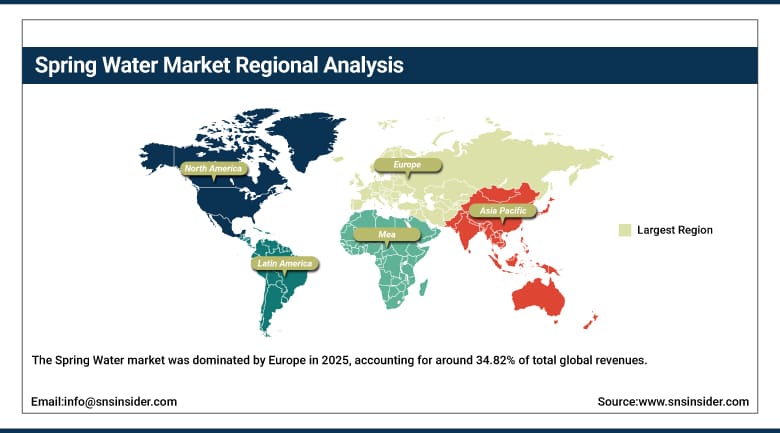

The Spring Water market was dominated by Europe in 2025, accounting for around 34.82% of total global revenues. Thanks to its strong traditional history and established heritage brands such as Evian, Volvic, Perrier, S Pellegrino, Spa, and Gerolsteiner, Europe boasts high per capita volumes of spring/mineral water consumption and consumer expertise in the mineral composition of springs that allows premium price positioning across both mass and luxury segments. Germany provides close to 28.47% of European revenues on account of its global per capita leadership in consumption of sparkling mineral water, premium water retailing sector development, and its export-oriented premium spring water brands into other markets. France, Italy, UK, and Benelux also generate significant regional revenues due to their home-grown premium spring water brands as well as growing imports of premium foreign brands.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Spring Water Market Insights

North America was estimated to represent around 22.47% of worldwide sales of Spring Water in 2025, where the United States accounted for around 84.73% of regional sales. The spring water market of North America is structurally aided by the continued fall in the consumption of carbonated soft drinks among US consumers, where the expenditure on beverages by individuals was channeled into the natural water category at levels which ensure growth above average in terms of volumes and revenues. Around 15.27% of regional sales is made up by Canada, due to its strong spring water consumption culture in the domestic market, with the help of ample infrastructure of natural springs found in British Columbia, Quebec, and Ontario, which are the source of water for the spring water brands of international repute.

Asia Pacific Spring Water Market Insights

The Asia Pacific region stands out as the most rapidly growing spring water market in terms of CAGR at 11.24%, primarily due to increased health awareness among urban populations in China, India, Japan, South Korea, and Southeast Asian countries, as well as the increasing worries over the poor quality of water available through taps in major Asian cities and the high profile and prestige attached to imported premium spring water brands. China constitutes approximately 34.82% of total revenue generation in the Asia Pacific region, courtesy of the dominant domestic market share held by the Nongfu Spring brand of water, whose unique marketing strategy based on source origin and premium glass-bottle product line has enabled them to build credibility when it comes to quality of spring water among consumers making the switch from purified to natural spring water.

MEA & Latin America Spring Water Market Insights

The Middle East & Latin America represent some of the rapidly emerging spring water market due to the growth in urbanization, increase in disposable income, and health awareness amongst the consumers which is contributing to the growth in both the consumer base and the commercial framework that is required for the distribution of premium spring water products. The UAE represents the largest share of revenues in MEA at around 26.48% by virtue of the cosmopolitan hospitality network in place, affluent expatriate community that has been consuming spring water for years now, and luxury hotels and restaurants that include international premium brands of spring water in their beverage’s menu. Saudi Arabia’s Vision 2030 campaign that aims at making the population of the country healthier through various health and wellness programs is contributing to the growth in the consumption of spring water. The country of Brazil leads Latin American revenues with around 42.73%.

Market Dynamics

Growth Drivers: Rising health consciousness and declining consumption of sugary beverages are driving strong demand growth in the spring water market across premium and mainstream segments.

The structural foundation for spring water market growth lies in the established trend of behavioral change from sugary drinks towards healthier options for hydration that has been noted in all major developed countries and that is steadily becoming a reality in developing nations due to increased awareness of health issues and greater spending power. The trend translates into an expanding addressable market for the industry, which is happening through three channels of commercial success at once. They are the upgrading of regular water users to premium spring water, the switching of soft drink users to spring water products and new markets developing in emerging economies, where spring water becomes their first exposure to premium water. The digital health movement, which impacts consumer behavior disproportionately strongly amongst younger consumers, accelerates this trend towards natural hydration solutions.

Restraints: Environmental concerns over plastic bottle waste and water source sustainability are creating regulatory and reputational challenges for the spring water market.

Environmental issues associated with PET packaging of single-use bottles are arguably the greatest source of reputation risk confronting the spring water industry. The growing concern with plastics in the oceans and microplastics contaminating water sources, alongside increasing awareness of the greenhouse gas emissions associated with long-distance transport of heavy water products, has resulted in a consumer and regulatory landscape in which spring water brands will need to prove genuine sustainability credentials to maintain consumer trust amongst increasingly eco-conscious buying groups. Direct economic and formulation implications arise from increased taxation of plastic packaging, extended producer responsibility regulations, and legislation around recycled plastic content for spring water bottles throughout Europe. Another issue of reputation is associated with the ecological sustainability of spring water sourcing, particularly issues such as over-extraction from aquifers, and this is managed by certification, reporting, and investment.

Opportunities: Growth in premium sparkling spring water, sustainable packaging innovations, and direct-to-consumer subscription models is creating strong revenue opportunities in the spring water market.

The premiumization trend of sparkling spring water presents the most immediate commercial opportunity within the segment. The ability and desire to pay a premium of up to 30% to 70% more on sparkling spring water that differentiates from still spring water on a sensory level through its carbonation is driving growth within the segment through higher profits and investments in new product flavors, minerals, and premium cans targeted at today’s lifestyle-oriented consumers. The direct-to-consumer subscription service business model of home/office water deliveries has emerged very quickly based on consumer demands for consistent supply, premium source water, and reduced use of plastic bottles compared to conventional grocery store purchasing patterns. Direct-to-consumer models present much greater lifetime value to brands due to the relationship-building opportunities inherent within the business model.

Recent Developments:

-

2025: Danone's Evian launched its premium spring water line packaged in 100% recycled glass bottles targeting luxury hospitality and premium retail channels globally, directly addressing growing operator and consumer demand for premium water whose packaging credentials match its source quality positioning and contribute to circular economy commitments.

-

2024: Nongfu Spring expanded its glass-bottled premium spring water distribution into international markets including Singapore, Malaysia, and Australia, leveraging the brand's established domestic premium quality credentials to compete directly with established European heritage brands in Asian premium retail and food service channel segments.

-

2024: Primo Water Corporation completed its home and office delivery route network expansion across 12 new U.S. metropolitan markets, adding over 80,000 new household and commercial delivery customers and reinforcing its strategy of building the most geographically comprehensive premium water delivery infrastructure in the North American market.

Spring Water Market Key Players are:

-

Nestle Waters (Nestle SA)

-

Danone SA (Evian, Volvic)

-

The Coca-Cola Company (Smartwater, Glaceau)

-

PepsiCo Inc. (Aquafina)

-

Primo Water Corporation

-

Nongfu Spring Co. Ltd.

-

S Pellegrino and Acqua Panna (Nestle)

-

Gerolsteiner Brunnen GmbH

-

VOSS Water AS

-

Fiji Water Company LLC

-

Mountain Valley Spring Water (BlueTriton)

-

Perrier (Nestle Waters)

-

Spa Monopole (Spadel Group)

-

Poland Spring (BlueTriton Brands)

-

Ferrarelle SpA

-

Lurisia SpA

-

Radenska (Atlantic Grupa)

-

Orient Beverages Pvt. Ltd.

-

Bisleri International Pvt. Ltd.

-

TDS Health and Wellness (Hildon)

Spring Water Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 48.74 Billion |

| Market Size by 2035 | USD 116.82 Billion |

| CAGR | CAGR of 9.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Still Spring Water, Sparkling Spring Water, Flavored Spring Water) • By Packaging Type (PET Bottles, Glass Bottles, Aluminium Cans, Others) • By Distribution Channel (Hypermarkets & Supermarkets, Specialty & Health Stores, Online Retail, Food Service) • By End User (Household/Retail Consumers, Food Service & Hospitality, Commercial & Office) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nestlé Waters (Nestlé SA), Danone SA (Evian, Volvic), The Coca-Cola Company (Smartwater, Glaceau), PepsiCo Inc. (Aquafina), Primo Water Corporation, Nongfu Spring Co. Ltd., S.Pellegrino and Acqua Panna (Nestlé), Gerolsteiner Brunnen GmbH, VOSS Water AS, Fiji Water Company LLC, Mountain Valley Spring Water (BlueTriton), Perrier (Nestlé Waters), Spa Monopole (Spadel Group), Poland Spring (BlueTriton Brands), Ferrarelle SpA, Lurisia SpA, Radenska (Atlantic Grupa), Orient Beverages Pvt. Ltd., Bisleri International Pvt. Ltd., TDS Health and Wellness (Hildon) |

Frequently Asked Questions

Europe dominated the Spring Water Market in 2025, holding approximately 34.82% of global revenues.

The still spring water segment dominated the Spring Water Market with 72.48% share in 2025.

The primary growth factors are the structural global consumer shift from sugary carbonated beverages to natural spring water driven by health consciousness, growing concern about tap water quality in urban markets globally, the premiumization of the spring water category through source differentiation and packaging innovation.

The Spring Water Market was valued at USD 48.74 Billion in 2025.

The Spring Water Market is expected to grow at a CAGR of 9.12% from 2026 to 2035.

Get in Touch