Structural Steel Market Report Scope & Overview:

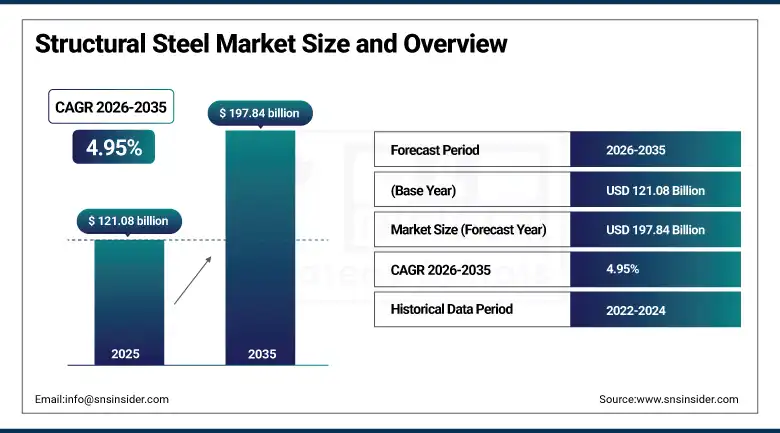

The Structural Steel Market was valued at USD 121.08 Billion in 2025 and is expected to reach USD 197.84 Billion by 2035, growing at a CAGR of 4.95% from 2026 to 2035.

Structural steel is the backbone of the modern built environment, providing the load-bearing skeletal framework upon which the world's cities, industrial facilities, transportation networks, and energy infrastructure are constructed. The material's combination of exceptional tensile and compressive strength, predictable mechanical behaviour across a wide range of loading conditions, dimensional precision from modern rolling mill production, and full recyclability at end of structural service life gives it a unique position in the construction material hierarchy that no single alternative material can match across the breadth of large-scale engineering applications. Structural steel sections including I-beams, H-piles, channels, angles, hollow structural sections, and reinforcing bar each serve specific structural engineering functions.

In June 2025, P&P Industries and Arya Engineers announced a strategic partnership to provide fully integrated end-to-end solutions for the design, manufacturing, and delivery of complete structural steel fabrication plants, targeting the growing demand for turnkey steel structure fabrication capability in emerging market economies whose rapid construction sector expansion requires domestic structural steel processing infrastructure. The partnership addressed the market gap between steel mill output and construction site delivery by providing integrated fabrication capability whose value-added processing of standard steel sections into ready-to-erect structural assemblies reduces on-site construction time and labour cost for major infrastructure and commercial building projects.

Market Size and Forecast

-

Market Size in 2026E: USD 127.08 Billion

-

Market Size by 2035: USD 197.84 Billion

-

CAGR: 4.95% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Structural Steel Market - Request Free Sample Report

Structural Steel Market Trends

-

Growing adoption of low-carbon and recycled steel is supporting demand for sustainable construction materials.

-

Prefabricated and modular steel construction systems are gaining popularity due to faster project completion and improved efficiency.

-

Increasing use of high-strength steel grades is enabling lighter structures and longer-span building designs.

-

BIM-integrated digital fabrication and automated steel processing technologies are improving manufacturing precision and productivity.

-

Rising seismic safety requirements are driving demand for high-performance structural steel in earthquake-prone regions.

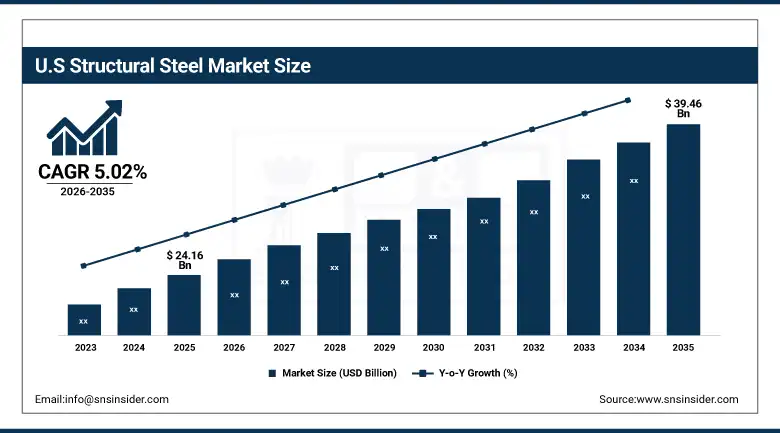

The U.S. Structural Steel Market Outlook

The U.S. Structural Steel Market was valued at approximately USD 24.16 Billion in 2025 and is expected to reach approximately USD 39.46 Billion by 2035, growing at a CAGR of approximately 5.02%. North America is expected to register the fastest CAGR over the forecast period, driven by increased construction spending and robust demand for structural steel in infrastructure modernization programmes.

The United States structural steel market benefits from the Infrastructure Investment and Jobs Act's USD 1.2 trillion commitment to highways, bridges, passenger rail, broadband, and energy grid infrastructure whose combined structural steel content requirements create sustained domestic demand that is reinforcing the commercial position of domestic producers including Nucor Corporation, Steel Dynamics, Commercial Metals Company, and SSAB Americas. The reshoring of manufacturing capacity across semiconductor fabrication, electric vehicle production, and clean energy equipment manufacturing is driving industrial building construction at unprecedented scale, with each new gigafactory and semiconductor fab representing hundreds of thousands of tonnes of structural steel demand across their building frames, mezzanine systems, and heavy equipment support structures.

In April 2023, Johnson Controls announced a steel recycling collaboration programme with Nucor Corporation through which over 70% of Johnson Controls' U.S. steel products are manufactured using recycled scrap materials processed through Nucor's Electric Arc Furnace network. The programme demonstrated the growing commercial importance of verifiable recycled content supply chains for structural steel procurement in commercial building projects whose green building certification requirements, including LEED and BREEAM, assign credit for documented recycled material content that EAF-produced structural steel can supply with greater consistency and traceability than integrated BOF production.

Structural Steel Market Segment Analysis

-

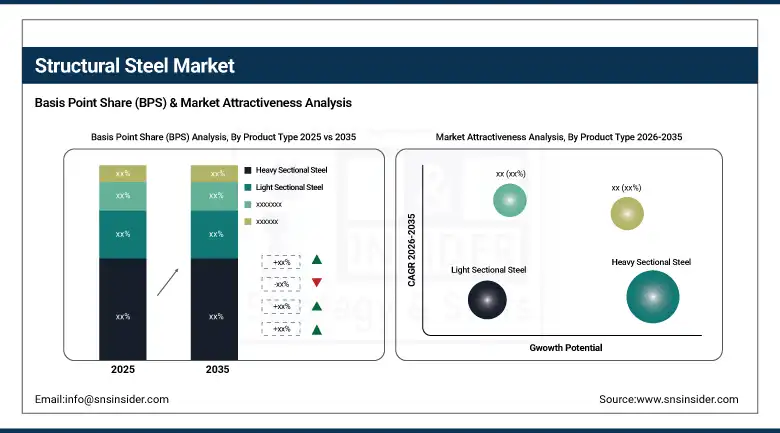

By Product Type, heavy sectional steel dominated the structural steel market in 2025, while the rebar segment is the fastest growing product type due to expanding concrete reinforcement requirements across residential and infrastructure construction.

-

By Manufacturing Process, hot-rolled steel dominated the structural steel market in 2025, while the galvanized steel segment is the fastest growing process type driven by corrosion protection requirements in coastal, industrial, and outdoor structure applications.

-

By Application, the non-residential segment dominated the structural steel market with over 54% share in 2025, while the infrastructure segment is the fastest growing application, expanding at a CAGR of approximately 6.8% during 2026–2035.

-

By End User, the construction segment dominated the Structural Steel market with the largest share in 2025, while the manufacturing & industrial segment is the fastest growing end user during the forecast period.

By Product Type, heavy sectional steel dominates, rebar grows fastest

Heavy sectional steel generated the dominant product type revenue share in 2025, reflecting its indispensable role as the primary load-bearing structural member in commercial buildings, industrial facilities, bridges, and public infrastructure. Wide-flange H-beams, universal beams, and heavy channel sections deliver the bending moment capacity and shear strength that column, beam, and truss systems require. Heavy sectional steel's revenue leadership reflects the high value per tonne of finished structural sections versus rebar and light sections. High-rise buildings, long-span warehouse roofs, and heavy industrial equipment support structures each require heavy sections whose weight-to-span ratios cannot be served by lighter alternatives without engineering compromise.

Rebar is growing fastest, driven by its deployment as the primary reinforcing component in concrete construction whose global volume substantially exceeds structural steel frame construction across residential and infrastructure applications in emerging economies. The expanding middle-class housing construction wave across India, Southeast Asia, Africa, and Latin America predominantly employs reinforced concrete structural systems whose rebar consumption per unit of floor area creates enormous volume demand for deformed bar whose production from Electric Arc Furnace mini-mills is progressively supported by local steel-making capacity expansion in proximity to these high-growth markets.

By Application, non-residential dominates, infrastructure grows fastest

Non-residential applications generated over 54% of structural steel market revenue in 2025, driven by commercial office, retail, logistics, data centre, and industrial building construction whose structural steel frame systems deliver the clear-span interior flexibility, floor-to-floor height efficiency, and construction speed that concrete-frame alternatives cannot match in commercial developer economics. The explosive global growth of e-commerce distribution centre construction, whose vast single-storey structural steel portal frame buildings with spans of 30 to 60 metres represent ideal applications for structural steel's unmatched span-length-to-column-spacing performance, has been a particularly commercially significant non-residential demand driver whose correlation with the e-commerce adoption curve across all major economies creates structural demand growth independent of traditional construction market cycles.

Infrastructure is growing fastest as the combination of government stimulus investment in transport infrastructure, bridge replacement programmes whose backlog in North America and Europe represents trillions of dollars in identified but underfunded capital needs, renewable energy installation requiring structural steel tower bases and substation frameworks, and data centre and energy storage facility construction collectively creates an infrastructure steel demand pool whose growth rate exceeds both residential and commercial construction categories through the forecast period. Each GW of installed wind turbine capacity requires steel tower and foundation structures whose structural steel content per GW of generation capacity represents a growing contribution to infrastructure steel demand that scales with the global energy transition investment trajectory.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

46.28% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Middle East & Africa |

Saudi Arabia |

24.73% |

|

Latin America |

Brazil |

43.84% |

North America Structural Steel Market Insights

North America is the fastest-growing regional structural steel market, expected to register the highest CAGR of 6.5% from 2026 to 2035. The United States accounts for approximately 82.47% of regional revenue through its domestic steel industry's EAF production leadership and the largest single-country infrastructure bill in global history whose implementation is creating sustained structural steel demand across highway bridge, passenger rail, port, and energy grid projects through 2031 and beyond. The U.S. domestic steel industry's competitive position has been reinforced by Section 232 tariffs on imported steel whose maintenance sustains domestic producer pricing and investment economics that support new EAF capacity additions. Canada contributes supplementary demand through its resource extraction infrastructure, urban transit expansion, and commercial building construction whose volumes create a commercially significant regional structural steel market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Structural Steel Market Insights

Europe held approximately 12.84% of global structural steel revenues in 2025. Germany accounts for approximately 28.47% of European revenues through its industrial building construction, automotive manufacturing plant investment, and the structural steel requirements of its extensive Mittelstand manufacturing sector whose factory and warehouse construction creates consistent domestic demand. European structural steel producers are investing heavily in low-carbon production technology under the EU's Green Deal industrial policy framework, with ArcelorMittal, Thyssenkrupp, SSAB, and Voestalpine each operating demonstration or commercial hydrogen-based direct reduction programmes whose low-carbon steel output commands price premiums in construction procurement programmes with embodied carbon specifications.

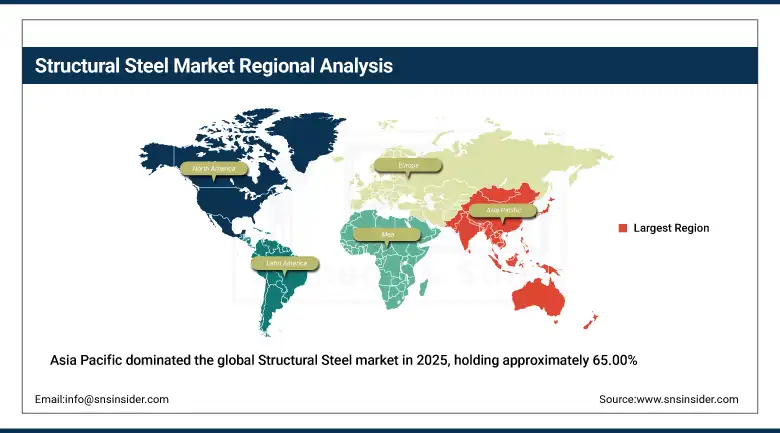

Asia Pacific Structural Steel Market Insights

Asia Pacific dominated the global Structural Steel market in 2025, holding approximately 65.00% of global revenues, a dominance reflecting the region's role as both the world's largest structural steel producer and its largest consumer. China accounts for approximately 46.28% of Asia Pacific revenues as the world's largest steel producer and construction market, whose annual crude steel output of approximately 1 billion tonnes and construction sector's continuing urbanization investment creates a structural steel consumption base that dwarfs all other national markets combined. India is growing fastest within the region as the world's most rapidly expanding major steel market, where government investment in National Highway Authority programmes, Pradhan Mantri Awas Yojana housing, and industrial corridor development is creating above-average structural steel demand growth.

MEA & Latin America Structural Steel Market Insights

Middle East and Latin America are growing Structural Steel markets where infrastructure investment under national development programmes, manufacturing sector expansion, and commercial construction activity are creating expanding demand. Saudi Arabia leads MEA revenues at approximately 24.73% of the regional total through the extraordinary capital investment of Vision 2030 mega-projects including NEOM, the Red Sea Project, and Diriyah Gate whose structural steel requirements for urban infrastructure, industrial facilities, and large-scale public buildings represent some of the largest individual structural steel procurement programmes globally. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large residential construction market.

Market Dynamics

Growth Drivers: Global infrastructure investment surge and the green building movement favoring recyclable structural steel over higher-embodied-carbon alternatives

The structural steel market's growth is driven by the alignment between a global infrastructure investment imperative, whose USD 94 trillion estimated global infrastructure gap documented by the McKinsey Global Institute creates politically popular investment programmes in virtually every major economy, and the unique performance and sustainability characteristics that structural steel delivers in the construction projects receiving this investment. Government infrastructure programmes in the United States, European Union, India, Saudi Arabia, and Southeast Asian economies are each creating multi-year, non-cyclical demand waves whose project pipelines provide structural steel producers and fabricators with sustained order books that smooth the demand volatility that historically characterized construction materials markets.

Restraints: Volatile raw material costs and trade policy uncertainty create pricing instability that complicates structural steel procurement planning for large construction projects

Structural steel pricing is exposed to the volatility of iron ore, coking coal, and scrap steel commodity markets whose price movements can alter finished section costs by 20 to 40% over periods of months, creating budget risk for fixed-price construction contracts whose structural steel procurement is typically locked at the project bidding stage. Trade policy instruments including Section 232 tariffs in the United States, EU safeguard measures, and anti-dumping duties in various national markets create artificial price differentials between domestic and import supply whose fluctuation with political cycle changes generates procurement uncertainty for contractors operating across multiple national markets. The energy intensity of structural steel production makes producer margins highly sensitive to natural gas and electricity price movements, particularly in Europe where energy cost escalation has periodically made European structural steel production economically uncompetitive against import alternatives.

Opportunities: Low-carbon green steel development and prefabricated modular steel construction represent transformative commercial frontiers that can substantially expand structural steel's market

The development of commercially available low-carbon structural steel produced through hydrogen direct reduction or electric arc furnace technology whose carbon footprint is 70 to 90% below conventional blast furnace production represents the most commercially significant product innovation opportunity in the structural steel industry since the introduction of high-strength microalloyed steel grades in the 1970s. Each national government and major private developer that establishes embodied carbon procurement thresholds for construction materials creates a market pull for green steel certification that early-mover producers including SSAB's Hybrit initiative and ArcelorMittal's XCarb programme are positioned to capture at significant price premium. Prefabricated modular steel construction whose factory-built volumetric modules and panelised floor, wall, and roof systems dramatically reduce on-site construction time and labour requirements is creating growing demand for precision-fabricated structural steel that commands higher margins than commodity section supply.

Recent Developments:

-

2025: P&P Industries and Arya Engineers formed a strategic partnership to offer fully integrated end-to-end solutions for structural steel fabrication plant design, manufacturing, and delivery, targeting the growing demand for turnkey steel fabrication capability in rapidly developing construction markets across South Asia and the Middle East.

-

2024: ArcelorMittal began commercial sales of XCarb recycled and renewably produced steel in Europe, providing construction procurement teams with verified low-carbon structural sections whose documented carbon footprint of under 400 kg CO2 per tonne supports green building certification credit and corporate net-zero supply chain commitments.

-

2023: Johnson Controls and Nucor Corporation formalised their steel recycling programme through which over 70% of U.S. Johnson Controls steel products use recycled scrap processed through Nucor's EAF network, demonstrating the growing commercial importance of verifiable recycled content documentation in structural steel supply chains.

Structural Steel Market Key Players are:

-

ArcelorMittal SA

-

Nippon Steel Corporation

-

China Baowu Steel Group Corporation Ltd.

-

POSCO Holdings Inc.

-

Tata Steel Ltd.

-

Nucor Corporation

-

Steel Dynamics Inc.

-

Gerdau SA

-

Commercial Metals Company

-

Hyundai Steel Co. Ltd.

-

SSAB AB

-

Thyssenkrupp AG

-

Voestalpine AG

-

Jiangsu Shagang Group Co. Ltd.

-

Baogang Group

-

Anyang Iron & Steel Group Co. Ltd.

-

Essar Steel India Ltd.

-

JSW Steel Ltd.

-

Evraz PLC

-

BlueScope Steel Ltd.

Structural Steel Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 121.08 Billion |

| Market Size by 2035 | USD 197.84 Billion |

| CAGR | CAGR of 4.95% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Heavy Sectional Steel, Light Sectional Steel, Rebar) • By Manufacturing Process (Hot-Rolled Steel, Cold-Rolled Steel, Galvanized Steel) • By Application (Residential, Non-Residential, Infrastructure) • By End User (Construction, Manufacturing & Industrial, Oil & Gas, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ArcelorMittal SA, Nippon Steel Corporation, China Baowu Steel Group Corporation Ltd., POSCO Holdings Inc., Tata Steel Ltd., Nucor Corporation, Steel Dynamics Inc., Gerdau SA, Commercial Metals Company, Hyundai Steel Co. Ltd., SSAB AB, Thyssenkrupp AG, Voestalpine AG, Jiangsu Shagang Group Co. Ltd., Baogang Group, Anyang Iron & Steel Group Co. Ltd., Essar Steel India Ltd., JSW Steel Ltd., Evraz PLC, and BlueScope Steel Ltd. |

Frequently Asked Questions

The Structural Steel Market was valued at USD 121.08 Billion in 2025.

The Structural Steel Market is expected to grow at a CAGR of 4.95% from 2026 to 2035.

Rising infrastructure investments, rapid urbanization, increasing industrial construction, growing adoption of sustainable building materials, and government-funded transportation and bridge development projects are driving structural steel market growth.

The heavy sectional steel segment dominated the Structural Steel Market in 2025 due to its exceptional strength, load-bearing capacity, and indispensable role in commercial, industrial, and infrastructure construction.

Asia Pacific dominated the Structural Steel Market in 2025, holding approximately 65.00% of global revenues, with China accounting for approximately 46.28% of Asia Pacific revenues as both the world's largest steel producer and construction market.

Get in Touch