Surgical Drill Market Report Scope & Overview:

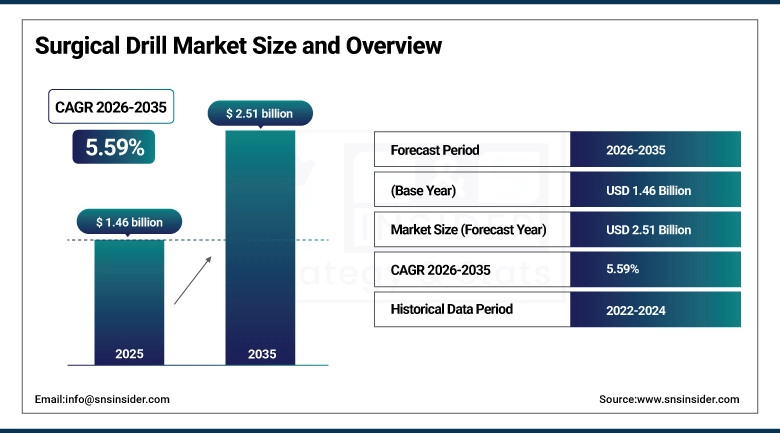

The Surgical Drill Market size was valued at USD 1.46 billion in 2025 and is expected to reach USD 2.51 billion by 2035, growing at a CAGR of 5.59% over the forecast period of 2026-2035.

Global Surgical Drill Market growth is driven by the rising number of surgeries, such as orthopedic, dental, and neurological procedures, across the globe. In addition, the rising number of chronic conditions such as arthritis and osteoporosis, which require surgical intervention, is another key driver of the global market. Moreover, the global market for surgical drills is witnessing a paradigm shift with the rising demand for minimally invasive surgeries (MIS), as these surgeries demand high-precision and ergonomic surgical drills. The growing investments of medical device companies in research and development to develop smart integrated surgical drills with advanced safety features such as auto-stop functions and sensors are providing strong opportunities for the global market to grow. In addition, the growing healthcare infrastructure in emerging markets and the rising number of ambulatory surgical centers (ASCs) are providing a robust platform for the global market to grow.

In February 2025, a leading orthopedic device manufacturer received FDA 510(k) clearance for its new line of smart, connected surgical drills featuring real-time torque monitoring and data capture capabilities, a 15% increase in cleared devices compared to the previous year, highlighting the trend towards digitized surgical tools.

Surgical Drill Market Size and Forecast:

-

Market Size in 2025: USD 1.46 Billion

-

Market Size by 2035: USD 2.51 Billion

-

CAGR: 5.59% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Surgical Drill Market - Request Free Sample Report

Surgical Drill Market Trends:

-

Development of cordless, battery-powered surgical drills offering greater freedom of movement and eliminating cumbersome tubing, enhancing surgeon ergonomics and operating room efficiency.

-

Integration of smart technologies, including IoT sensors and data analytics, into drill systems for real-time feedback on bone density and drill bit depth, improving surgical precision and patient safety.

-

Rising demand for customized and procedure-specific drill attachments and accessories, driven by the complexity of modern surgical techniques in orthopedics and neurosurgery.

-

Increasing utilization of reusable surgical drills and accessories to manage costs and reduce medical waste, particularly in price-sensitive markets, balancing with the demand for single-use, sterile components to eliminate cross-contamination risks.

-

Adoption of advanced materials, such as titanium and specialized alloys, in drill construction to provide lightweight, durable, and autoclavable instruments that withstand rigorous sterilization processes.

-

Growth in outpatient surgeries is fueling demand for compact, portable, and easy-to-use surgical drills suitable for ambulatory surgical centers and specialized dental clinics.

-

Development of robotic-assisted surgical systems that incorporate high-speed, precision drills, allowing for pre-planned, minimally invasive bone cuts in joint replacement and spinal procedures.

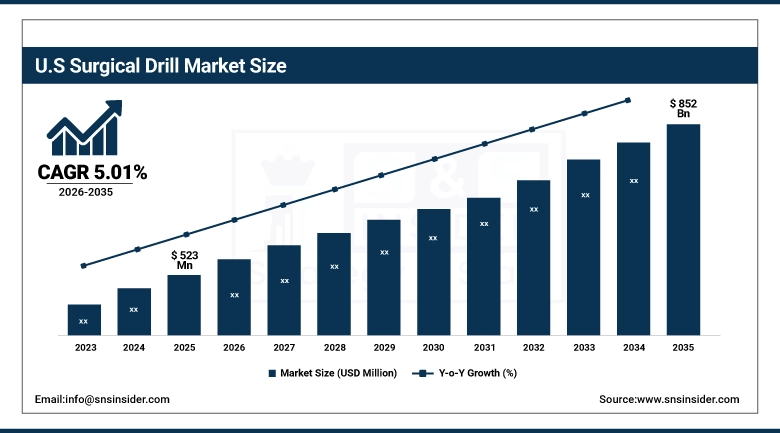

The US Surgical Drill Market is estimated at USD 523 million in 2025, and it is expected to reach USD 852 million by 2035, growing at a CAGR of 5.01% from 2026-2035. The United States has the highest share in the surgical drill market due to the large number of orthopedic and dental surgeries, advanced medical facilities, and high healthcare expenditure. The presence of key medical companies, the rate of adoption of technologically advanced surgical equipment, and favorable reimbursement policies for surgical procedures are some of the key factors for the growth of the surgical drill market in this region. The rise in sports injuries and the need for joint replacement surgeries because of the aging population are key factors for the growth of the surgical drill market.

Surgical Drill Market Growth Drivers:

-

Rising Incidence of Orthopedic and Dental Disorders Driving Market Growth

The growing global incidence of musculoskeletal disorders and dental problems is one of the main drivers behind the surgical drill market. The growing global incidence of osteoarthritis, rheumatoid arthritis, osteoporosis, especially in the aging global population, is one of the main drivers behind this market. The growing global incidence of osteoarthritis, rheumatoid arthritis, osteoporosis, especially in the aging global population, is one of the main drivers behind this market. The growing global incidence of dental caries and periodontitis is another main reason behind this market. The growing global incidence of dental caries and periodontitis is another main reason behind this market. The growing global incidence of sports-related injuries is another main reason behind this market, thereby providing a solid foundation to this market.

For example, in March 2025, data from the American Academy of Orthopaedic Surgeons indicated a 7% year-over-year increase in knee and hip replacement procedures among patients aged 55-70, directly correlating with a higher demand for precision surgical drills in U.S. hospitals.

Surgical Drill Market Restraints:

-

High Cost of Advanced Surgical Drills and Budget Constraints Restricting Market Expansion

The high-cost factor involved with technologically advanced surgical drill systems, especially electric and smart drill systems with consoles and software, acts as a major impediment to the development of the market. Budget constraints faced by small-scale hospitals, clinics, and developing nations act as major impediments to the purchase of technologically advanced surgical drill systems due to the high costs involved with them. Additionally, the high cost of maintaining and replacing the accessories also acts as a major impediment to the development of the market. The preference towards reusable systems also calls for high initial costs towards the development of the sterilization system, which acts as a major impediment to the development of the market.

Surgical Drill Market Opportunities:

-

Expansion in Emerging Markets and Development of Cost-Effective Solutions Creating Market Opportunities

The growing infrastructures in Asia Pacific, Latin America, and the Middle East & Africa provide opportunities for the surgical drill market. In addition, there is an increasing trend in medical tourism in these regions. Moreover, with an increase in disposable income and awareness of advanced surgical treatment options, the demand for surgical drills is expected to rise in these regions. There is a huge potential in the market for the development and introduction of cost-effective, durable, and user-friendly surgical drills that can cater to the requirements and budget constraints of the emerging markets. In addition, the development of dedicated surgical drills for specific surgical procedures, such as minimally invasive spinal surgery and dental implant surgery, is an opportunity in the market.

For example, in January 2025, a medical device company launched a new, affordable line of battery-powered surgical drills specifically for the Southeast Asian market, featuring simplified controls and compatibility with existing accessories to facilitate adoption in cost-conscious healthcare settings.

Surgical Drill Market Segment Analysis:

-

By product, the instruments segment accounted for the largest share of 72.4% in 2025. Within instruments, electric drills dominated, and the accessories segment is anticipated to exhibit the fastest growth, at a CAGR of 6.2%.

-

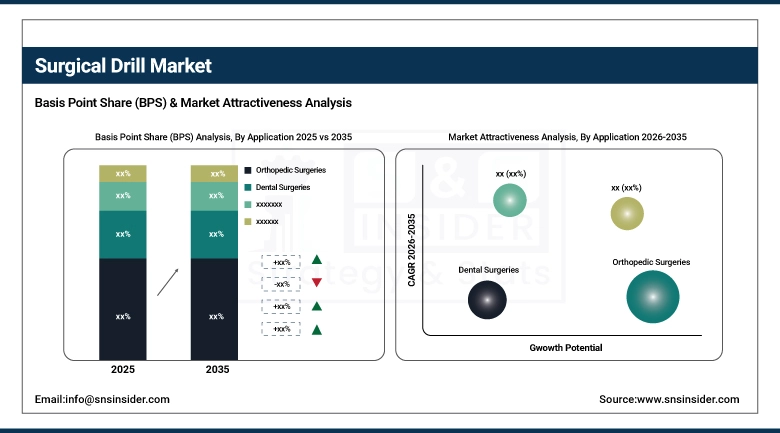

By application, the orthopedic surgeries segment registered the highest market share of about 48.5% in 2025, while the dental surgeries segment is anticipated to register the highest CAGR of 6.1%.

-

By end use, hospitals & clinics had the highest market share of about 60.3% in 2025, and the ambulatory surgical centers (ASCs) segment is projected to be the fastest-growing, with a CAGR of 6.8%.

By Application, Orthopedic Surgeries Dominate, While Dental Surgeries Show Rapid Growth

The orthopedic surgeries segment has the highest revenue share of around 48.5% in 2025, owing to the large number of surgeries such as knee and hip replacement, bone fracture fixation, and spinal fusion. This growth is mainly attributed to the rise in the geriatric population, which is prone to diseases such as osteoarthritis and osteoporosis, as well as sports injuries. Surgical drills are the basic tools used in orthopedic surgeries for bone preparation, screw placement, and reaming.

The dental surgeries segment is expected to witness the highest growth rate in the range of 6.1% from 2026 to 2035, specifically attributed to the increased global interest in cosmetic dentistry, the rise in dental disorders, and the increased popularity of dental implants as a tooth replacement option. This is mainly attributed to the increased demand for precise, quiet, and vibration-free dental drills.

By Product, Instruments Lead the Market, While Accessories Register Fastest Growth

In 2025, the instruments segment contributed over 72.4% of the revenue share, with electric drills holding the largest sub-segment share due to their consistent power, variable speed control, and suitability for a wide range of heavy-duty orthopedic and neurosurgical applications. The reliability and precision of electric drills make them a staple in hospital operating rooms.

On the other hand, the accessories segment, which includes drill bits, reamers, saw blades, and batteries, is expected to record the highest CAGR of about 6.2% between 2026 and 2035. The expansion is driven by the recurring need for replacement of consumable and wear-and-tear items, the development of specialized, procedure-specific accessories, and the increasing adoption of battery-powered drills that require replacement batteries and chargers.

By End Use, Hospitals & Clinics Lead, While Ambulatory Surgical Centers Grow the Fastest

The segment of hospitals & clinics dominated the surgical drill market with the largest revenue share of 60.3% in the year 2025 due to the high volume of intricate surgical procedures conducted within the sector, such as joint replacement surgeries, intricate spinal surgeries, and trauma surgeries. The sector also has the resources to purchase high-end and multifunctional surgical drill systems due to the availability of capital budgets within the sector.

However, the ambulatory surgical centers segment is expected to witness the highest CAGR of 6.8% during the forecasted period of 2026-2035. This is due to the rising trend of moving surgical procedures from the inpatient sector to the ambulatory sector due to the cost-effectiveness, convenience, and technological capabilities of the ambulatory sector to conduct less invasive surgical procedures using compact, portable, and easy-to-use surgical drill systems.

Surgical Drill Market Regional Highlights:

North America Surgical Drill Market Insights:

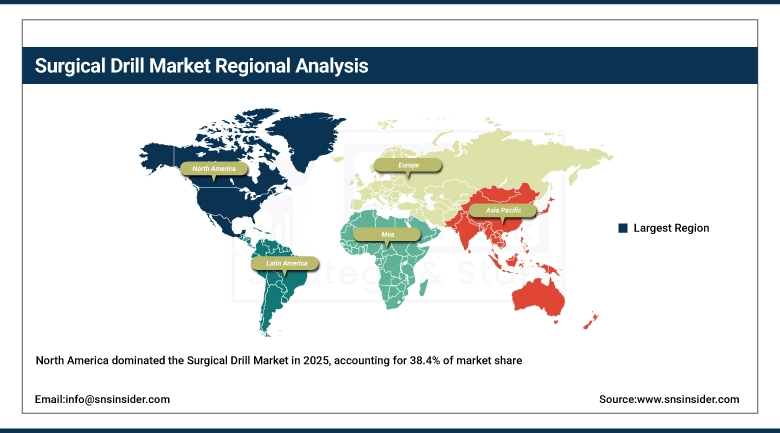

North America dominated the surgical drill market in terms of revenue share at 38.4% in 2025 due to its established healthcare infrastructure, high healthcare expenditure per capita, and adoption of technologically advanced surgical devices at the outset. The key enablers are the presence of major medical device manufacturers, high volume of orthopedic and dental surgeries, and high reimbursement rates for surgeries.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Surgical Drill Market Insights:

The Asia Pacific market is the fastest-growing regional market, with a CAGR of 6.7%, due to a rapidly aging population, increasing healthcare expenditure, and a rising prevalence of chronic diseases. The major factors that contribute to the growth of the surgical procedures market in the region include the high patient pool in China and India, which in turn increases the volume of surgical procedures in the region, as well as the rise in medical tourism, government initiatives, and the growth in the number of medical schools.

Europe Surgical Drill Market Insights:

The European region accounts for the second most dominant market for surgical drills after North America. Strong government support for healthcare innovation, the presence of a large geriatric population, and world-leading research in surgical techniques are driving market growth. The growth of the surgical drill market in Europe is supported by a high standard of care, increasing demand for minimally invasive surgeries, and a well-regulated medical device market.

Latin America (LATAM) and Middle East & Africa (MEA) Surgical Drill Market Insights:

The Surgical Drill Market in Latin America & Middle East & Africa is steadily growing, driven by increasing investments in healthcare infrastructure, a rising prevalence of chronic and orthopedic conditions, and growing government initiatives to expand access to surgical care. The major factors for growth include the development of specialized orthopedic and dental centers, particularly in urban areas, and collaborations with international medical device companies to supply essential surgical equipment.

Surgical Drill Market Competitive Landscape:

Stryker Corporation (founded in 1941) is a global leader in medical technology, offering a comprehensive portfolio of surgical drills and power tools under its Instruments division. Their products are widely used in orthopedics, neurosurgery, and ENT, known for their reliability, ergonomic design, and integration with advanced surgical navigation systems.

-

In April 2025, Stryker launched its next-generation System 9 Smart Drill platform, featuring integrated sensor technology that provides real-time feedback on bone quality and drill depth, enhancing safety and precision in complex spinal procedures.

Medtronic plc (founded in 1949) is a massive player in medical technology, providing advanced surgical power tools and drills primarily for neurosurgical, orthopedic, and ENT applications. Their solutions are often integrated within broader surgical ecosystems, including navigation and robotic-assisted surgery platforms.

-

In September 2024, Medtronic expanded its Midas Rex neurosurgical instrument line with new high-speed, precision drills designed specifically for minimally invasive cranial and spinal procedures, featuring enhanced ergonomics and reduced acoustic noise.

Zimmer Biomet Holdings, Inc. (founded in 1927) is a leading orthopedic device company that offers a wide range of surgical products, including power tools and drills essential for joint replacement and trauma surgeries. Their drills are designed for durability, precision, and seamless integration with their implant systems.

-

In January 2025, Zimmer Biomet received FDA clearance for its new line of lithium-ion battery-powered drills for total knee and hip arthroplasty, boasting a 30% longer runtime and a universal console that powers multiple instrument types to improve OR efficiency.

Surgical Drill Market Key Players:

-

Stryker Corporation

-

Medtronic plc

-

Zimmer Biomet Holdings, Inc.

-

Johnson & Johnson (DePuy Synthes)

-

B. Braun Melsungen AG (Aesculap)

-

Smith & Nephew plc

-

CONMED Corporation

-

Brasseler USA

-

Nouvag AG

-

Saeyang Microtech

-

W&H Dentalwerk Bürmoos GmbH

-

Dentsply Sirona

-

NSK-Nakanishi Inc.

-

Osada Electric Co., Ltd.

-

Aygun Surgical

-

De Soutter Medical

-

Pro-Dex, Inc.

-

Misonix, Inc. (Bioventus)

-

MicroAire Surgical Instruments

-

AlloTech

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.46 Billion |

| Market Size by 2035 | USD 2.51 Billion |

| CAGR | CAGR of 5.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Instrument (Pneumatic Drill, Electric Drill, Battery-Powered Drill), Accessories) • By Application (Orthopedic Surgeries, Dental Surgeries, ENT Surgeries, Others) • By End Use (Hospitals & Clinics, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Stryker Corporation, Medtronic plc, Zimmer Biomet Holdings Inc., Johnson & Johnson (DePuy Synthes), B. Braun Melsungen AG (Aesculap), Smith & Nephew plc, CONMED Corporation, Brasseler USA, Nouvag AG, Saeyang Microtech, W&H Dentalwerk Bürmoos GmbH, Dentsply Sirona, NSK-Nakanishi Inc., Osada Electric Co. Ltd., Aygun Surgical, De Soutter Medical, Pro-Dex Inc., Misonix Inc. (Bioventus), MicroAire Surgical Instruments, AlloTech |

Frequently Asked Questions

Growth is driven by increasing orthopedic, dental, and neurological procedures, rising chronic diseases, and the shift toward minimally invasive surgeries (MIS).

The market is expected to grow from USD 1.46 billion in 2025 to USD 2.51 billion by 2035, at a CAGR of 5.59%.

Orthopedic surgeries hold the largest share (~48.5% in 2025), while dental surgeries are the fastest-growing segment.

Key trends include battery-powered cordless drills, smart sensor integration, robotic-assisted surgery, and demand for customized accessories.

North America leads in market share, while Asia Pacific is the fastest-growing region due to expanding healthcare infrastructure and patient volume.

Get in Touch