Surgical Staplers Market Report Scope & Overview:

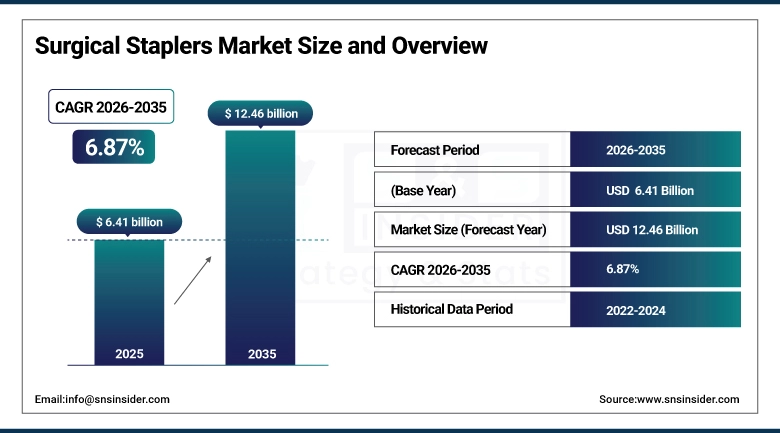

The Surgical Staplers Market was valued at USD 6.41 Billion in 2025 and is expected to reach USD 12.46 Billion by 2035, growing at a CAGR of 6.87% from 2026–2035.

The Surgical Staplers Market is witnessing robust growth owing to factors such as the rising number of surgical procedures being performed across the globe, the high incidence of chronic ailments necessitating surgical procedures, and the increased inclination toward minimally invasive surgeries. With technology advancements like powered and disposable staplers, improved precision during surgery, shorter procedure times, and enhanced patient results have been observed. Moreover, the rising geriatric population, rising healthcare spending, and continuous healthcare infrastructure investment will boost the market growth.

According to the World Health Organization (WHO), noncommunicable diseases account for approximately 74% of global deaths annually, increasing the need for surgical treatments and supporting demand for advanced surgical stapling solutions. According to the United Nations, the global population aged 65 years and older is projected to more than double by 2050, significantly increasing surgical procedures associated with age-related health conditions.

Surgical Staplers Market Size and Forecast

-

Market Size in 2026E: USD 6.85 Billion

-

Market Size by 2035: USD 12.46 Billion

-

CAGR: 6.87% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Surgical Staplers Market - Request Free Sample Report

Surgical Staplers Market Trends

-

Increasing adoption of powered surgical staplers to improve surgical precision, operational efficiency, and patient outcomes during complex procedures

-

Growing preference for minimally invasive and laparoscopic surgeries driving demand for advanced surgical stapling devices across healthcare settings

-

Rising use of disposable surgical staplers to enhance infection control, reduce contamination risks, and support patient safety initiatives

-

Continuous technological advancements in stapler design, including smart feedback systems and enhanced staple line security for better performance

-

Expanding application of surgical staplers in bariatric, colorectal, thoracic, and gastrointestinal surgeries due to increasing surgical procedure volumes worldwide

U.S. Surgical Staplers Market Outlook

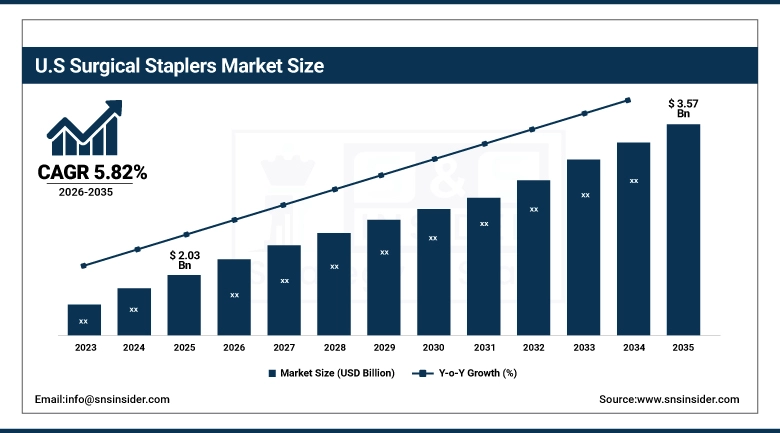

The U.S. Surgical Staplers Market is projected to grow from USD 2.03 Billion in 2025 to USD 3.57 Billion by 2035, at a CAGR of 5.82%.

The United States surgical staplers market is driven by the world's most extensive hospital and ambulatory surgical centre network, the highest per-capita adoption of minimally invasive surgical techniques that require endoscopic stapler consumption, and the largest bariatric surgery programme globally whose sleeve gastrectomy and bypass procedure volumes create above-average stapler consumption per procedure. FDA adverse event reports are driving regulatory improvements and clinician awareness, increasing adoption of advanced powered staplers with enhanced safety.

The U.S. Centers for Disease Control and Prevention (CDC) reports approximately 51.4 million inpatient procedures performed annually in U.S. hospitals, highlighting the substantial procedural volume driving demand for surgical stapling devices.

Surgical Staplers Market Segment Analysis

-

By Product Type, manual surgical staplers held the largest market share of 58.72% in 2025, while powered surgical staplers are expected to grow at the fastest cagr of 9.62% during 2026–2035.

-

By Type, disposable surgical staplers dominated with a 63.15% share in 2025, while reusable surgical staplers are projected to expand at the fastest cagr of 9.47% during the forecast period.

-

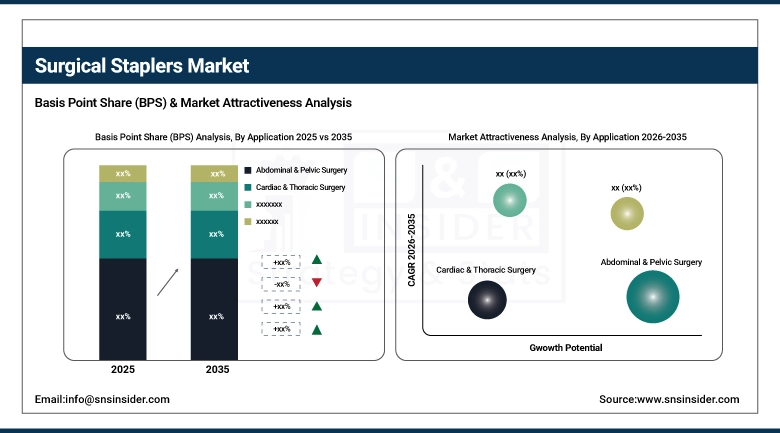

By Application, abdominal & pelvic surgery accounted for the highest market share of 35.88% in 2025, while cardiac & thoracic surgery is anticipated to record the fastest cagr of 9.84% through 2026–2035.

-

By End User, hospitals & clinics held the largest share of 71.42% in 2025, while diagnostic centers are expected to grow at the fastest cagr of 9.75% during 2026–2035.

By Product Type, manual surgical staplers segment dominates the market, while powered surgical staplers segment is expected to grow at the fastest rate

Manual Surgical Staplers dominated the market due to their broad acceptance in general surgery, gastrointestinal surgery, and gynecology surgery. The relatively low price of the product, easy operation, and ability to be used in varied surgical procedures account for its popularity among hospitals and healthcare organizations. Manual staplers also require very little maintenance and training, which further increases their attractiveness for healthcare facilities in both developed and emerging healthcare markets.

Powered Surgical Staplers are projected to witness the fastest growth driven by growing demands for precision and consistency in surgical procedures. Powered staplers alleviate hand fatigue and allow for precise and consistent creation of staples, reducing tissue trauma during the process. Growth in minimally invasive surgeries, advances in technology used in surgical equipment, and investments in operating rooms have contributed to the increasing adoption of powered staplers in modern hospitals.

By Type, disposable surgical staplers segment dominates the market, while reusable surgical staplers segment is expected to grow at the fastest rate

Disposable Surgical Staplers held the largest market share because they provided better protection against infections and did not pose any risks of cross contamination. The disposable feature of these products was in line with the strict guidelines that exist regarding the safety of health care services, as well as the need to sterilize surgical equipment. Moreover, the use of disposable staplers lowered the costs incurred through their processing and saved time as well. The increased concern for patient safety and high surgical volumes were responsible for this trend.

Reusable Surgical Staplers are expected to grow at the fastest rate due to the current trend toward cost efficiency in healthcare organizations. These staplers minimized waste and allowed hospitals to purchase fewer instruments since they were used repeatedly. Thanks to advances in sterilization technologies and designs of such staplers, their performance improved. Environmental concerns and cost saving motives drove the adoption of reusable surgical staplers.

By Application, abdominal and pelvic surgery segment dominates the market, while cardiac and thoracic surgery segment is expected to record the fastest CAGR

Abdominal and Pelvic Surgery accounted for the highest market share owing to the extensive procedure count in gastroenterology, colorectal surgery, bariatric surgery, and gynecological procedures. Stapler systems play a key role in such procedures by providing effective tissue closure, shorter surgical times, and better healing results. The growing incidence of digestive problems and weight-loss surgeries, along with increased availability of surgical facilities, keeps fueling robust demand from this application segment.

Cardiac and Thoracic Surgery is anticipated to record the fastest CAGR due to increasing incidents of cardiovascular disease and pulmonary diseases that require surgery. Enhanced accuracy with advanced stapler devices makes it possible to conduct less invasive thoracic surgery. Robotic and video-assisted surgery, combined with increased healthcare investments in heart surgery centers, is driving fast demand for surgical staplers in this application segment.

By End User, hospitals and clinics segment dominates the surgical staplers market, while diagnostic centers segment is expected to experience the fastest growth

Hospitals and Clinics dominated the market because most surgical procedures which require use of surgical staplers were performed here. They have modern surgical equipment and surgeons who use their skills to carry out procedures. An increase in patient admission, number of elective and emergency operations and constant investment towards the improvement of the operating theatres plays a huge role in the use of the surgical staples. They will remain major players in the market for a long period of time.

Diagnostic Centers are expected to experience the fastest growth as a result of the growing trend towards development of all-round medical institutions which provide diagnostic and surgical treatment. The investments into the infrastructure of outpatient surgery as well as the increase in the development of minimally invasive techniques encourage the use of staplers during surgery. Moreover, a growing preference among the patients towards affordable and convenient healthcare encourages this trend.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Surgical Staplers Market Insights

North America dominated the global Surgical Staplers Market in 2025, through its high surgical procedure volumes, premium device adoption culture, and commercial concentration of major surgical stapler manufacturers including Ethicon (Johnson & Johnson), Medtronic, and Becton Dickinson. The United States accounts for approximately 82.5% of North American revenues through its extensive hospital and ambulatory surgical centre network, the highest minimally invasive surgery adoption rate, and the robust bariatric and thoracic surgical programme volumes whose combined stapler consumption creates the world's largest national stapler procurement market.

CDC data indicate around 1.3 million cesarean sections, 719,000 total knee replacement surgeries, 332,000 total hip replacement surgeries, and 395,000 coronary artery bypass graft surgeries are carried out each year, a lot of which utilize surgical staplers for tissue approximation and superior surgical results.

Europe Surgical Staplers Market Insights

Europe held a significant share of the global Surgical Staplers Market in 2025. Germany, France, the United Kingdom, Italy, and Spain are the leading national markets whose universal healthcare surgical care programmes, advanced hospital surgical infrastructure, and growing minimally invasive surgery adoption create consistent and growing surgical stapler demand. Germany accounts for approximately 28.5% of European revenues through its large hospital surgical volume, early adoption of robotic surgical systems creating robotic stapler cartridge demand, and the commercial presence of B. Braun and Aesculap whose European surgical stapler product lines serve domestic and regional markets.

According to Eurostat, approximately 22% of the European Union population, or nearly 99 million people, were aged 65 years and older in 2025, contributing to higher demand for surgical procedures and advanced surgical stapling devices.

Eurostat reports that the share of the EU population aged 65 and above increased from 17% in 2005 to 22% in 2025, while individuals aged 80 years and older accounted for 6% of the population, supporting increased volumes of orthopedic, cardiovascular, and general surgical interventions.

Asia Pacific Surgical Staplers Market Insights

Asia Pacific is the fastest-growing regional Surgical Staplers Market with a CAGR of approximately 8.34%, driven by the rapid expansion of surgical infrastructure investment across China, India, Japan, South Korea, and Southeast Asia whose growing hospital networks, increasing surgical procedure volumes, and progressive minimally invasive surgery adoption create above-trend stapler demand.

China accounts for approximately 38.5% of Asia Pacific revenues through its enormous hospital surgical volume, the progressive adoption of laparoscopic techniques in tier 1 and tier 2 city hospital surgical programmes, and the growing domestic surgical stapler manufacturing industry whose product portfolio development is progressively expanding beyond basic linear staplers toward advanced endoscopic and powered configurations.

According to UNFPA Asia-Pacific, the number of people aged 60 years and above in the region is projected to triple between 2010 and 2050, reaching nearly 1.3 billion, thereby increasing demand for surgical procedures associated with age-related health conditions.

MEA & Latin America Surgical Staplers Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class hospital surgical infrastructure, the advanced minimally invasive surgery programmes of major Dubai and Abu Dhabi teaching hospitals, and the medical tourism sector whose high surgical volume includes significant bariatric and oncological procedures. Saudi Arabia's expanding hospital network and growing surgical capacity create above-regional-average stapler demand growth.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its large public and private hospital surgical volume, the growing adoption of laparoscopic and thoracoscopic techniques, and the significant bariatric surgery programme whose global ranking as the second-largest by annual procedure count creates substantial linear stapler consumption. Mexico and Colombia are growing secondary markets with expanding surgical infrastructure and increasing minimally invasive technique adoption.

Market Dynamics

Growth Drivers: Rising global surgical volumes, ageing populations, and minimally invasive procedures are significantly increasing demand for endoscopic staplers.

The surgical staplers market's growth is driven by the convergence of rising surgical procedure volumes and the progressive adoption of minimally invasive surgical techniques that create specific endoscopic stapler demand above open surgical stapler baseline growth. Ageing populations in developed economies whose elevated surgical disease burden from cancer, cardiovascular disease, and orthopaedic conditions is creating sustained surgical procedure volume growth provide the foundational demand driver for all surgical stapler categories.

The progressive adoption of laparoscopic and robotic minimally invasive techniques across colorectal, thoracic, bariatric, and gynaecological surgery, where technique migration from open to minimally invasive procedures requires replacement of open stapler configurations with endoscopic equivalents at typically higher per-unit price points, creates both procedure volume growth and per-procedure stapler value increase that compound into above-trend market revenue expansion.

Restraints: FDA scrutiny over stapler complications and high powered stapler costs limit adoption in budget-constrained healthcare settings.

FDA's medical device reporting system documentation of thousands of annual adverse events attributed to surgical stapler malfunction, including staple line leaks, misfires, and deployment failures, has attracted regulatory scrutiny that is simultaneously motivating manufacturer performance improvement investment and creating medico-legal risk awareness that makes some surgeons and hospital administrators cautious about adoption of newer stapler platform generations without substantial outcome data.

The FDA's 2019 safety communication specifically addressing serious complications associated with surgical staplers identified over 32,000 malfunctions, 9,000 injuries, and 366 deaths attributed to stapler-related adverse events in a five-year period, creating a regulatory and litigation backdrop that motivates both product quality investment and clinical due diligence in stapler selection and technique. Powered surgical stapler systems' higher acquisition cost relative to manual equivalents creates budget justification requirements in value-conscious hospital purchasing that necessitate clinical outcome evidence documentation and total cost of care analysis whose preparation creates adoption friction beyond the product's technical merits.

Opportunities: Robotic surgery integration and AI-driven adaptive firing technologies are creating new growth opportunities in surgical staplers.

Robotic surgical system integration creates the most commercially significant near-term opportunity for premium surgical stapler product development, as each new robotic surgical platform whose growing installed base creates demand for compatible stapler cartridges optimised for robotic instrument arm actuation generates a captive consumable market whose per-procedure revenue scales with robotic case volumes that are growing at 15 to 25% annually across major adopting specialties.

Each new robotic stapler cartridge product generation whose data demonstrates superior clinical outcomes in robotic-specific tissue management scenarios sustains premium pricing and preferential inclusion in robotic programme stapler formularies that hospital procurement committees establish. AI-powered adaptive firing optimisation whose closed-loop control integrates real-time tissue characterisation, firing speed modulation, and post-fire formation quality assessment into powered stapler control algorithms creates a technological differentiation platform whose clinical performance advantage is progressive and documentable through controlled outcome comparison studies that sustain premium market positioning.

Recent Developments:

-

2025: Ethicon launched the ETHICON 4000 Stapler with 3D Stapling and Gripping Surface Technology, enhancing staple-line integrity, reducing anastomotic leaks across open and laparoscopic applications, and establishing a robotic integration pathway with OTTAVA surgical systems.

-

2025: Medtronic introduced an enhanced Signia Stapling System with upgraded Adaptive Firing and advanced articulation for minimally invasive surgery, providing real-time tissue compression feedback and automated firing speed optimisation across variable tissue thickness conditions.

-

2024: Becton Dickinson expanded its Echelon Circular Powered Stapler portfolio with new cartridge configurations for improved access in deep pelvic colorectal and gynaecological anastomosis applications, addressing the stapler access limitation that anatomically constrained pelvic surgery creates for conventional circular stapler insertion.

Surgical Staplers Market Key Players

-

Johnson & Johnson (Ethicon)

-

Medtronic plc

-

B. Braun Melsungen AG

-

3M Company

-

Smith & Nephew plc

-

CONMED Corporation

-

Intuitive Surgical, Inc.

-

Stryker Corporation

-

Zimmer Biomet Holdings, Inc.

-

Meril Life Sciences Pvt. Ltd.

-

Purple Surgical Holdings Limited

-

Frankenman International Limited

-

Dextera Surgical Inc.

-

Grena Ltd.

-

Reach Surgical, Inc.

-

Welfare Medical Ltd.

-

Lepu Medical Technology (Beijing) Co., Ltd.

-

XNY Medical

-

Boston Scientific Corporation

-

Becton, Dickinson and Company

Surgical Staplers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.41 Billion |

| Market Size by 2035 | USD 12.41 Billion |

| CAGR | CAGR of 6.87% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Manual Surgical Staplers, Powered Surgical Staplers) • By Type (Disposable Surgical Staplers, Reusable Surgical Staplers) • By Application (Abdominal & Pelvic Surgery, Cardiac & Thoracic Surgery, Orthopedic Surgery, General Surgery, Gynecological Surgery, Others) • By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Diagnostic Centers, Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson & Johnson (Ethicon), Medtronic plc, B. Braun Melsungen AG, 3M Company, Smith & Nephew plc, CONMED Corporation, Intuitive Surgical, Inc., Stryker Corporation, Zimmer Biomet Holdings, Inc., Meril Life Sciences Pvt. Ltd., Purple Surgical Holdings Limited, Frankenman International Limited, Dextera Surgical Inc., Grena Ltd., Reach Surgical, Inc., Welfare Medical Ltd., Lepu Medical Technology (Beijing) Co., Ltd., XNY Medical, Boston Scientific Corporation, Becton, Dickinson and Company |

Frequently Asked Questions

The Surgical Staplers Market is expected to grow at a CAGR of 6.87% from 2026 to 2035.

The Surgical Staplers Market was valued at USD 6.41 Billion in 2025.

Ageing populations, rising surgeries, minimally invasive procedures, powered stapler innovations, and expanding healthcare infrastructure are driving market growth.

The Manual Surgical Staplers segment dominated the Surgical Staplers Market with approximately 58.72% share in 2025.

North America dominated the Surgical Staplers Market in 2025.

Get in Touch