Suture Anchor Devices Market Report Scope & Overview:

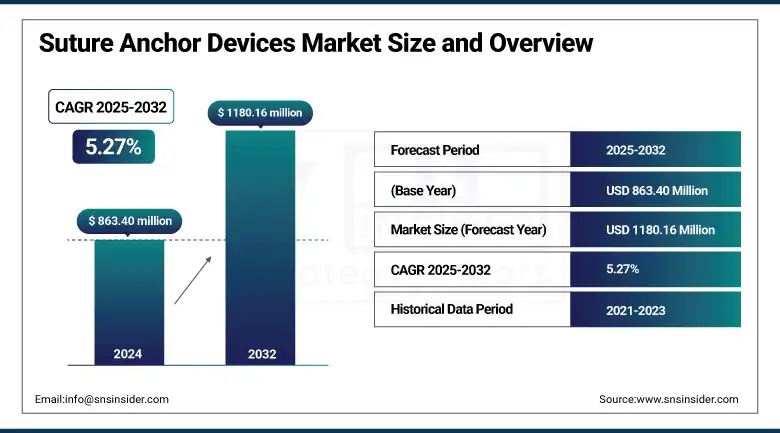

The suture anchor devices market size was valued at USD 863.40 million in 2024 and is expected to reach USD 1180.16 million by 2032, growing at a CAGR of 5.27% over the forecast period of 2025-2032.

The global suture anchor devices market is growing at a steady pace owing to the increase in sports injuries, orthopedic disorders, and the growing geriatric population that demands joint repair surgeries. Advancements in arthroscopic surgery and the introduction of bioresorbable and knotless anchors are increasing clinical indications for shoulder, knee, hip, and ankle procedures. Furthermore, the growing prevalence of ambulatory surgery centers and outpatient procedures is propelling market demand globally.

To Get more information On Suture Anchor Devices Market - Request Free Sample Report

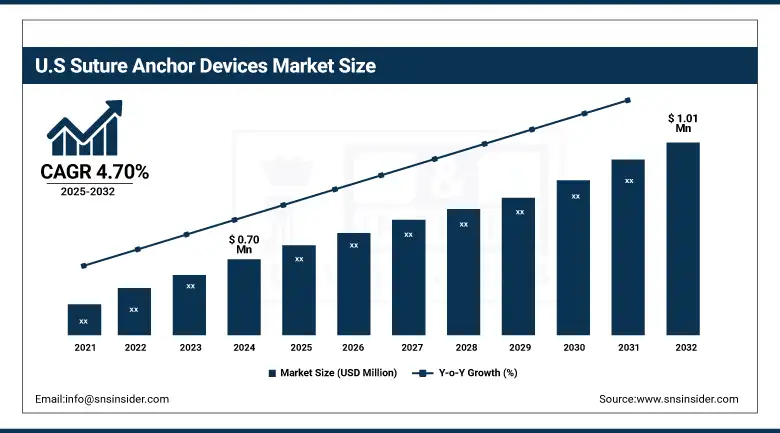

The U.S. suture anchor devices market size was valued at USD 0.70 million in 2024 and is expected to reach USD 1.01 million by 2032, growing at a CAGR of 4.70% over the forecast period of 2025-2032.

The U.S. dominated the North American suture anchor devices market growth with the massive number of orthopedic and sports injury procedures, a well-established healthcare setup, and the availability of minimally invasive surgical procedures in place. Furthermore, the presence of prominent manufacturers and favorable reimbursement policies further supports the dominance of the country in the market.

Smith+Nephew’s Q‑FIX Knotless All‑Suture Anchor (July 2025) sets a new standard for all‑suture anchors with ultra-low displacement and simplified insertion that delivers superior fixation strength and time savings in arthroscopic shoulder, hip, and ankle surgeries.

Market Dynamics:

Drivers:

-

Advances in Arthroscopic and Minimally Invasive Surgeries are Anticipated to Expedite Market Growth

Increasing preference for arthroscopic and minimally invasive procedures is driving demand for suture anchors. These techniques result in less invasive surgery, with smaller incisions and damage to surrounding tissue, and shorter recovery time versus traditional “open” treatments. Suture anchors are common devices used with arthroscopy to repair soft tissues, such as tendons and ligaments to bone. Their applications in rotator cuff repair, labral tear repair, and meniscal fixation are increasing. As hospitals and ASCs' capabilities increase, they require suture anchors that are compact, efficient, and reliable.

Medacta’s X‑Twist anchor platform, available in knotless and knotted configurations, addresses shoulder-to-foot-and-ankle repairs with simplified instrumentation, continuing the current trend toward versatile, minimally invasive systems.

-

Technological Advancements in Suture Anchor Design and Material are Expected to Boost the Market Consensus

The important factor contributing to the growth of the market is the ongoing advancements and changes in the materials and design of the anchors. The latest suture anchors are molded from high-tech materials including PEEK, PEEK with carbon fiber, and biodegradable polymers, such as PLLA and PLGA. These materials increase biocompatibility and minimize the risk of postoperative complications, and in the case of absorbable anchors, prevent the need for implant removal. Furthermore, the proposed knotted and tape anchor systems will provide surgeons with enhanced fixation strength, streamline operative times, and make the system more user-friendly, especially reducing implantation time and invasiveness in minimally invasive applications. Such advancements, fast-tracking the adoption by surgeons, and better patient outcomes, are driving overall market growth.

According to MDPI, in a recent systematic review, it is reported that bioabsorbable PLLA/PLGA anchors would achieve levels of pull-out strength comparable with those of non-absorbable ones, and that PLLA/PLGA degrades in 7‑90 months, confirming the possibility of using resorbable devices.

Stryker’s Citrefix system brings together a citrate-based bioresorbable body with a PEEK eyelet, for tissue-friendly healing and structural integrity, as a relatively modern mix of concepts and materials. Hornyak calls a hybrid design innovation.

Restraints:

-

Expensive Advanced Suture Anchor Devices are Hindering the Growth of the Market

The high cost of modern suture anchor instruments is an obstacle to the global suture anchor devices market growth due to cost-sensitive areas. Novel implants, such as knotless anchors, tape-based implants, or bioabsorbable materials are more favorable in the clinical outcome, and demand a higher price compared with traditional metallic or knotted implants. These high costs are out of reach of especially poor healthcare providers in developing countries with more limited budgets and with only limited public funding for healthcare.

Furthermore, the values of associated adaptation costs are not limited to the device cost, but also include those of specific surgical instruments, techniques, arthroscopic tools, and postoperative care. Even in such weak or no-reimbursement scenarios, patients have to pay out of pocket, which would further discourage the use of these relief solutions. Therefore, even though there are clinical advantages, there may not be enough for a large number of providers to move from traditional low-cost anchors and maintain their financial status.

Segmentation Analysis:

By Product

The non-absorbable segment dominated the suture anchor devices market in 2024, with a share of 54.28%, attributed to the increasing use of these anchors for high-load bearing repairs and long-term fixation procedures, such as rotator cuff and knee ligament repairs. These anchors, which are typically composed of metal or PEEK (polyetheretherketone) material, provide a high level of mechanical strength, long-term resistance, and have shown clinical results, and are, for this reason, favored by orthopedic surgeons. Their robustness and image compatibility also contributed to their widespread use in hospitals and surgical centers.

The absorbable segment is projected to register the highest CAGR during the forecast period, on account of growing demand for biocompatible and resorbable materials, which reduce long-term effects. Bio-absorbable anchors, typically formed from polymers, such as PLLA and PLGA, will eventually degrade within the body, negating the need for removal by surgery and decreasing the probability of chronic tissue irritation. The improvement in material science and the increasing employment of minimally invasive approaches and tissue-sparing repair techniques are driving the trend for absorbable anchor solutions, especially in younger and more active patient populations.

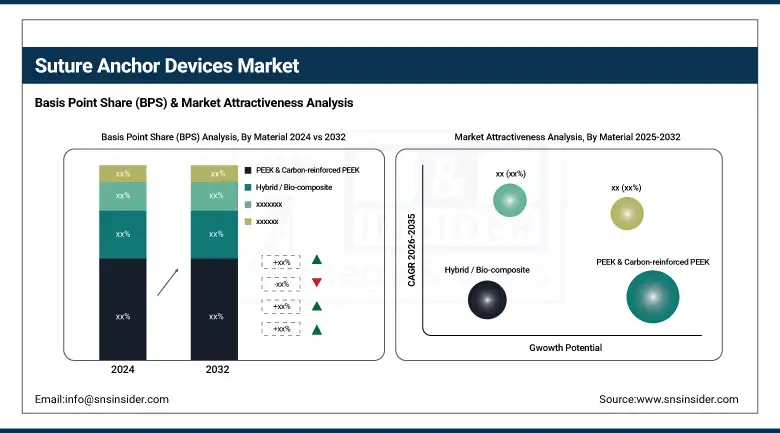

By Material

The PEEK and carbon-reinforced PEEK segment dominated the suture anchor devices market in 2024 with a 33.26% market share, being highly preferred owing to its excellent mechanical strength, biocompatibility, and image compatibility. They have strong load-bearing properties and do not produce artifacts on MRI and CT examinations, and are therefore suitable for follow-up after surgery. PEEK-based anchors are remarkably preferred for the vast orthopedic practices with the multi-directional forces, such as the shoulder and knee ligament reconstructions, due to the long-term stability and endurance. Inherent durability and low inflammatory response assisted widespread acceptance by surgeons.

The bio-absorbable polymer (PLLA and PLGA) segment registers the fastest CAGR during the forecast period, due to the growing need for resorbable and body-friendly implant products. These polymers biodegrade endogenously, obviating the necessity for secondary surgical retrieval and decreasing the likelihood of chronic sequelae. Bio-absorbable anchors are being used more and more in active or younger patients, in whom a long-term implant is not desired. With the development of polymers and an increasing demand for minimally invasive and biologically incorporated procedures, the use of these materials is increasing globally.

By Tying Type

The knotless segment dominated the suture anchor devices market share in 2024 with a 47.16%, as these anchors help in simplifying procedures and lowering the operative time. Compared with the conventional knotted anchors, the knotless anchors do not require suture securing with the utilization of difficult suturing maneuvers, which makes the surgery procedure more effective but also minimizes the potential hazard of suture knot-mediated morbidity, such as irritation, inflammation, or damage to soft tissues. These instruments provide reliable, consistent tension control, and better fixation, for instance, in arthroscopic procedures centering on rotator cuff or labral repairs, and consequently are the orthopedic surgeon's first choice.

The tape-based segment is expected to be the fastest-growing segment during the forecast period due to its better load distribution and less chance of tissue cut-through. Integrated-tape suture anchors have been introduced, which use wider tape suture material to spread the force over a greater area of the repaired tissue, thereby providing improved fixation strength with a lower probability of tissue damage. This design is particularly advantageous in the management of fragile or degenerative tissues and has become more popular in technical shoulder and knee surgery. Increasing demand for soft-tissue repairs and developments in suture technology are anticipated to drive the growth of tape-form anchor systems globally.

By Application

The shoulder rotator cuff segment dominated the suture anchor devices market in 2024 with a 35.5% share on account of a large patient pool with rotator cuff injuries, especially in the elderly and athletes. The shoulder is a highly mobile joint, and it is subject to a lot of use and abuse, so it follows that one of the most frequently treated locations with suture anchors is here. Rotator cuff repair procedures often require the placement of multiple suture anchors for soft tissue to bone reattachment, and device volume is substantial. Furthermore, arthroscopic shoulder surgeries have become more prevalent, and developments in anchor technology, including knotless and bioresorbable systems fueled the growth of this segment.

The Hip–Labral & FAIS (Femoroacetabular Impingement Syndrome) segment is expected to grow at the highest rate during the forecast period, owing to the increasing awareness and diagnosis of labral tears and FAIS, especially in the young and active population. Progress in hip arthroscopy has made minimally invasive treatment of these pathologies possible, leading to the need for precise and bone-preserving suture anchor systems. Increased imaging and early diagnoses of hip joint pathologies, together with expanding surgeon experience and access to dedicated implants, have supported the growth of suture anchors in hip surgery.

By End-Use

The hospitals segment dominated the suture anchor devices market in 2024 with a 68.2% market share due to the large number of complex orthopedic procedures performed at hospitals, which include shoulder, knee, and hip reconstruction, and is the key factor driving the growth of this end-user segment. Hospitals possess sophisticated surgical facilities, multi-disciplinary care, and highly trained orthopedists, rendering them the go-to for urgently required trauma and elective joint surgery. In addition, their access to broad implant selection, reimbursement support, and postoperative care services further solidifies their lead in the use of suture anchors.

The ambulatory surgical centers (ASCs) segment is expected to register the highest CAGR during the forecast period on the basis of the growing preference for cost-effective, minimally invasive surgeries characterized by quicker recovery times. Ambulatory surgical centers (ASCs) provide an expedited and cost-effective environment for orthopedic procedures, such as arthroscopic repairs with suture anchors. With the refinement of techniques and advancements in technology and the increasing use of knotless, absorbable anchor systems, providing ambulatory use, open-label, under local anesthesia, fast procedures are now being applied.

Regional Analysis:

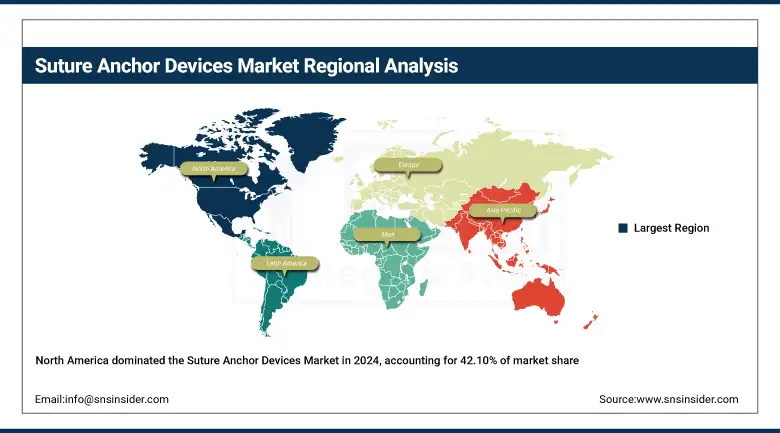

The suture anchor devices market is dominated by North America with a 42.10% market share in 2024, owing to the presence of a well-established healthcare sector, a high number of surgical procedures, and early adoption of innovative technologies in orthopedics. The market is largely driven by the presence of major market players, including Stryker, Arthrex, and Johnson & Johnson, who constantly invest in product development and innovation in the region. Moreover, the availability of favorable reimbursement policies along with growing awareness regarding sports medicine and minimally invasive surgery largely contributes to the continuous demand for suture anchor devices in hospitals, ambulatory surgical centers, and orthopedic clinics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the largest and fastest-growing region in the suture anchor devices market trends and holding, with an aging population, rising incidence of trauma and sports injuries, and growing accessibility to orthopedic care in countries, such as China, India, and Japan. Increasing healthcare spending, increasing medical tourism, and the emergence of private healthcare institutions are resulting in a high number of surgical procedures. Moreover, international manufacturers are venturing into Asia Pacific to explore its untapped market and serve cost-efficient solutions that are tailored for regional use.

In Europe, the suture anchor devices market analysis is expanding with a significant growth rate, attributable to the high prevalence of musculoskeletal disorders, increasing preference for arthroscopic procedures, and growing awareness about minimally invasive surgery. Germany, the U.K., France, and Italy are among the leading countries, backed up by established orthopaedic care networks and lifted by favorable reimbursement conditions. Furthermore, the availability of trained surgeons and the rising adoption of the advanced bioresorbable and knotless anchor systems are also fueling the growth of the market in the region.

Latin America and the Middle East & Africa (MEA) suture anchor devices market is growing at a moderate pace as the orthopaedic procedures rise along with the development of advanced surgical treatment awareness. Latin America has an increasing demand due to the growth of the private health infrastructure and medical tourism. In MEA, fast market growth is driven by government (healthcare) investment and increasing access to specialist surgical care, although its pace of development is slightly held back by restricted reimbursements and a professional skills shortage.

Key Players:

The suture anchor devices market companies are Smith & Nephew, Zimmer Biomet, Arthrex, Johnson & Johnson (DePuy Synthes), Stryker, CONMED, Medtronic, Parcus Medical, Wright Medical (Enovis), Teknimed, Enovis (DJO), Integra LifeSciences, Double Medical, Anika Therapeutics, Medartis, OrthoMed, B. Braun Melsungen, OrthAlign, Ceterix Orthopaedics, Teleflex Medical, and other players.

Recent Developments:

-

July 2025 – Global medical technology business Smith+Nephew launched its Q-FIX KNOTLESS All-Suture Anchor, intended for soft tissue-to-bone fixation in several joint spaces, such as the shoulder, hip, and foot & ankle. The new anchor improves surgical versatility while ensuring consistent fixation without knots.

-

January 2023 – Stryker launched Citrefix, a new generation of suture anchor system that was specifically designed for foot and ankle surgery. The system comes with Citregen, a citrate-based, bioresorbable material that is designed to closely resemble the chemistry and the mechanical composition of bone tissue, with better biocompatibility and healing response.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 863.40 million |

| Market Size by 2032 | USD 1180.16 million |

| CAGR | CAGR of 5.27% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Absorbable, Non-Absorbable) • By Material (Metal [Titanium / Stainless], Bio-absorbable Polymer [PLLA, PLGA], PEEK & Carbon-reinforced PEEK, Hybrid / Bio-composite) • By Tying Type (Knotted Suture Anchors, Knotless, Tape-based) • By Application (Shoulder-Rotator Cuff, Hip-Labral & FAIS, Knee-Meniscal & MCL, Foot & Ankle, Elbow & Wrist) • By End Use (Hospitals, Ambulatory Surgical Centers, Clinics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Smith & Nephew, Zimmer Biomet, Arthrex, Johnson & Johnson (DePuy Synthes), Stryker, CONMED, Medtronic, Parcus Medical, Wright Medical (Enovis), Teknimed, Enovis (DJO), Integra LifeSciences, Double Medical, Anika Therapeutics, Medartis, OrthoMed, B. Braun Melsungen, OrthAlign, Ceterix Orthopaedics, Teleflex Medical, and other players. |

Frequently Asked Questions

North America dominated the Suture Anchor Devices Market in 2024.

The “PEEK & Carbon-reinforced PEEK” segment dominated the Suture Anchor Devices Market.

Advances in arthroscopic and minimally invasive surgeries are anticipated to expedite market growth.

The Suture Anchor Devices Market was USD 863.40 million in 2024 and is expected to reach USD 1180.16 million by 2032.

The Suture Anchor Devices Market is expected to grow at a CAGR of 5.27% from 2025 to 2032.

Get in Touch