Synthetic Media Market Analysis & Overview:

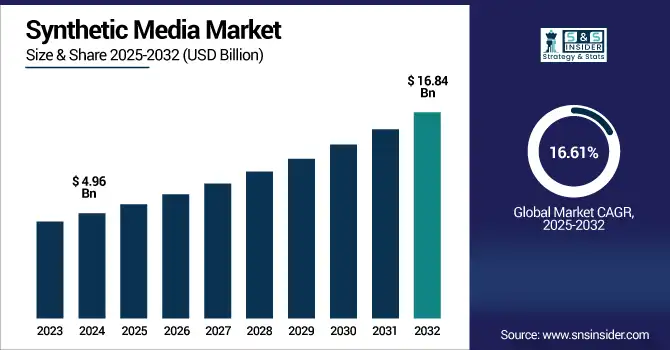

The synthetic media market size was valued at USD 4.96 billion in 2024 and is expected to reach USD 16.84 billion by 2032, growing at a CAGR of 16.61% over 2025-2032.

To Get more information on Synthetic-Media-Market - Request Free Sample Report

The synthetic media market growth is driven by the increasing utilization of generative AI in personalized content creation in the entertainment and marketing industries and the increment in the virtual digital content adoption across the education sector. This wave is also being fueled by a growing need for personalized and scalable digital content together with new innovations in speech synthesis, deepfakes, and computer vision.

-

For instance, Microsoft Azure AI supports real-time speech-to-text in 125 languages/dialects, with Neural Text-to-Speech (TTS) usage increasing by over 50% YoY from 2023 to 2024.

Businesses are leveraging synthetic media to enhance user engagement, reduce production costs, and enable real-time content delivery.

-

According to Deloitte (2024), 76% of marketing leaders plan to increase investment in AI-generated content, with expectations to reduce campaign production time by 25–40%.

The expansion of social media and API integrations is also fueling usage. Additionally, the advancements in the natural language processing and ethical content governance frameworks are building greater trust and increasing enterprise adoption in the BFSI, Healthcare, and e-learning segments.

The U.S. synthetic media market size was valued at USD 1.36 billion in 2024 and is expected to reach USD 4.55 billion by 2032, growing at a CAGR of 16.27% over 2025-2032.

The U.S. synthetic media market is growing due to rising need of AI powered content in entertainment, marketing and education, technological advancements, robust digital infrastructure, and surge in investment in generative AI solutions by organizations for scalable and cost-effective content generation.

Synthetic Media Market Dynamics:

Drivers:

-

Rising Demand for Personalized Content Experiences Across Entertainment, Marketing, and Education is Accelerating Adoption of Synthetic Media Technologies

The rapid expansion of content-starved digital platforms, the advent of hyper-personalized experiences is in huge demand. AI-generated synthetic media taking form as audio, video, and avatars provides a means for creators, educators, and marketers to drive personalized experiences at scale. These innovations are restructuring how content, such as virtual influencers, ads driven by deepfake technology, and adaptive e-learning are consumed. As a result, brands have increasingly implemented synthetic media for the swift and cost-effective creation of location-specific, multilingual content. This demand for both efficiency and personalization is influencing innovations across gaming, e-commerce, education, and digital entertainment sectors.

-

TikTok introduced AI-powered avatars and voice cloning, with 15%+ of video uploads in mid-2024 incorporating synthetic media effects.

-

Meta (Facebook & Instagram): Independent analysis (Nov 2024) found that approximately 41% of Facebook long-form posts were such as AI-generated, up from 24% in 2023, marking a 4.3× increase since ChatGPT’s launch.

Restraints:

-

Growing Concerns Over Misinformation, Deepfakes, and Manipulation are Limiting Synthetic Media's Mainstream Acceptance and Regulatory Freedom

The growing realism of synthetic media poses dire threats in itself, opening doors to misinformation and fake news, identity theft, and the creation of malicious media content. The growing sophistication of deepfake technology has led to worries that it could be misused for political purposes, cybercrime, or damage to people’s reputation. This has led to a global regulatory scrutiny, proposed laws, and labeling requirements. The challenge for platforms is the need to deploy detection tools and ensure ethical AI deployment. While these challenges can hinder innovation, raise compliance costs, and undermine public trust potentially restricting the widespread use and expansion of synthetic media technologies.

-

A June 2025 U.S. survey found that 85% of Americans report decreased trust in online information due to deepfakes, and 81% fear personal harm from fake audio or video content. Only about 10% had used detection tools.

-

The Entrust & Onfido Identity Fraud Report (2025) revealed that deepfake attacks occurred every 5 minutes in 2024, while digital document forgery rose 244% YoY, now comprising 57% of all document fraud.

-

According to academic survey data in the U.K. (mid‑2024), although only 8% of respondents had created deepfakes, over 90% expressed concern, and 15% had seen harmful deepfakes, including scams or fake sexual content.

Opportunities

-

Expansion Of Low-Code and No-Code Synthetic Media Platforms is Empowering Non-Technical Users and Creators to Scale Content Production

Emerging low-code and no-code tools are making it possible for marketers, educators, and influencers to make AI-powered videos, voiceovers, and visuals without the need of coding skills. With pre-trained templates, a new drag-and-drop functionality, and cloud rendering, these platforms have drastically lowered technical barriers. When more people create realistic avatars, explainer videos, and virtual humans, the content becomes rapid, democratized, and scalable. In emerging economies, where technical expertise is often limited, this democratization is accelerating adoption across e-learning, HR training, digital advertising, and social media channels.

-

77% of organizations reported using low-code/no-code tools in 2023, with 80% of non-IT professionals leveraging them to build apps by 2024.

-

Low-code/no-code solutions can cut development time by up to 90%, significantly boosting productivity and accessibility.

-

As of January 2025, Synthesia serves over 60,000 customers, including more than 60% of Fortune 100 companies, demonstrating widespread non-developer adoption of low-code AI video generation tools.

Challenges

-

Ethical Dilemmas and Legal Ambiguities Around Identity Rights and Content Authenticity Pose Ongoing Challenges for Synthetic Media Regulation

The proliferation of synthetic representations, such as computerized-synthesized voices and digital twins presents substantial legal and ethical issues. The property law and even contract law are yet to catch up with the issues around consent, ownership rights, and accountability for misuse. The absence of a global unified legislation makes it very complicated to have content distributed cross-border. The landscape of synthetic media is rapidly evolving, leading to more compliance burdens, legal grey areas for companies, and a stalling of innovation as greater transparency and ethical safeguards come to play.

Synthetic Media Market Segmentation Analysis:

By Component

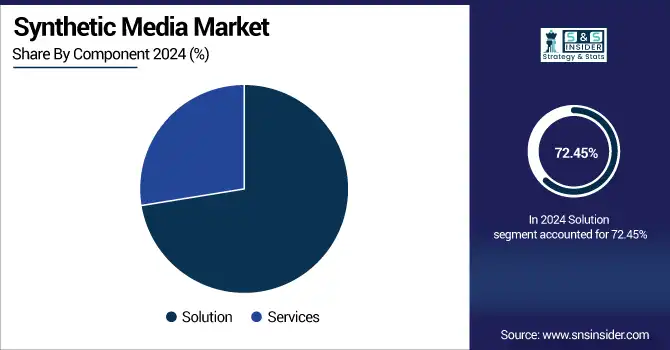

The Solution segment dominated the synthetic media market in 2024 due to the increasing use of software to generate content across verticals through artificial intelligence. Enterprises are investing massively in synthetic media platforms to automate video, voice, and image generation for branding, training, and marketing. As they are the centerpiece of operations, these tools reflect scalability and creative flexibility, and thus, command a major share of the overall market revenue.

The Services segment is projected to grow at the fastest CAGR of 18.43% over 2025-2032 as the demand for consulting, integration and maintenance support for the synthetic media systems are on the rise. With so many organizations deploying AI-driven tools, it requires technical guidance to deploy these tools and customize content. Non-tech sectors and SMEs transitioning into synthetic content are driving this service-centric growth.

By Application

The Media & Entertainment segment held the largest market share at 30% in 2024, due to its early adoption for content localization, CGI replacement, and virtual production. To minimize expenses but not creativity, studios and streaming platforms are utilizing AI-powered performers, dubbing instruments, and digital platforms. Its size and speed of innovation have made it the top revenue generator for the sector.

The Gaming segment is expected to grow at the highest CAGR of 19.98% over 2025-2032, owing to the rising applications of synthetic media to create NPCs, virtual characters, and other immersive environments for games. AI-generated assets are quickly becoming a popular tool for game developers looking for quicker content development cycles, improved personalization, or deeper narrative possibilities. Scalability and captivation in game experiences are also driving synthetic media adoption in the gaming workflows.

By Technology

The Generative AI segment led the market with a share of a 46% in 2024 due to its integral part in generating synthetic images, videos and avatars. Generative AI, which creates hyper-realistic content across formats, is a cornerstone of almost all synthetic media applications. As more powerful and accessible models continue to develop, we expect generative AI to keep delivering significant content breakthroughs globally, within industries.

The Natural Language Processing (NLP) segment is set to grow at a CAGR of 19.45% over 2025-2032, due to increasing adoption of text-to-speech, voice cloning, and conversational AI. With its ability to fuel virtual assistants, AI narrators and multilingual dubbing, it is an integral technology to interactive synthetic media. Growing demand for real-time, intelligent, and natural language processing is accelerating the market traction of NLP.

By Channel

The Web-Based segment dominated the market in 2024 with a 35% revenue share owing to the accessibility, scalability, and easy deployment services across the various industry verticals. Bitcoin mining is the equivalent of generating and editing synthetic content to fit into the trailer. They offer real-time collaboration, low-cost distribution, and are integrated with cloud ecosystems, the ideal choice for companies and artists who need content quickly without compromising quality.

The Social Media Platforms segment is expected to grow at the highest CAGR of 20.18% over 2025-2032 owing to the surge in demand for AI-based influencers, avatars, and short-form content. Synthetic media is used by creators and brands to create viral marketing, boost trends, and engage with audiences. Demonstrably, the interactive real-time texture of social media ecologies enables experimental synthetic forms, and catalysts aggressive development in this space.

Synthetic Media Market Regional Outlook:

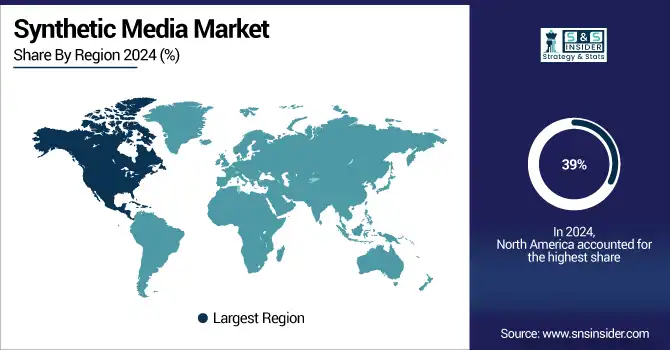

North America dominated the synthetic media market in 2024 with a 39% revenue share owing to investment by tech companies, strong digital infrastructure, and early adoption of AI. The market is dominated owing to the leading position of the synthetic media companies and high demand from entertainment, advertising, and gaming, among others. Furthermore, supportive regulations and innovation-friendly environments have fast tracked synthetic content adoption throughout the region.

The U.S. is dominating the synthetic media market due to advanced AI innovation, strong tech investments, and high adoption across media and enterprise sectors.

Asia Pacific is expected to grow at the fastest CAGR of 19.13% over 2025 to 2032 owing to rapid digitalization, increasing smartphone penetration, and surge in localized content. China, India and South Korea are all pouring money into A.I. applications, in everything from entertainment to education to e-commerce. The enabling creator economies and friendly government policies are scaling synthetic media uptake across multiple users’ segments.

China is dominating the synthetic media market in Asia Pacific due to major investments in AI, government support, and adoption in the entertainment and e-commerce industry.

Europe's synthetic media market is expanding steadily, driven by rising need for AI generated content in media, advertising, and education. The region’s market dynamics are influenced by robust regulatory frameworks, increasing investments in digital transformation and increasing interest in ethical AI.

The U.K. is dominating the synthetic media market in Europe, driven by strong media-tech integration, AI startups, and high demand in advertising and entertainment.

The synthetic media market trends in the Middle East & Africa and Latin America indicate growing momentum, supported by increasing digitalization, expanding social media usage, and rising interest in AI-driven content creation across entertainment, marketing, and education sectors in emerging economies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

Synthetic media market companies are IBM, Microsoft, Synthesis AI, Inc., NVIDIA Corporation, Deepbrain AI, Baidu, Inc., Adobe, DataRobot, Inc., OpenAI, Google (Alphabet Inc.), Runway ML, Synthesia, Hour One, Descript, Inc., Veritone, Inc., Rephrase.ai, Soul Machines, Resemble AI, LALAL.AI, and D-ID.

Recent Developments:

-

2025 – Baidu revealed Ernie 4.5 and multimodal reasoning model Ernie X1 in March, boosting video, image, and audio synthesis capabilities for next-gen synthetic media use‑cases.

-

2025 – IBM launched enterprise-grade synthetic data sets for predictive AI and LLM training tailored to IBM Z and LinuxONE clients, improving privacy-compliant synthetic data options.

-

2024 – DataRobot introduced real-time AI observability tools with intervention capabilities for generative AI deployments across cloud, hybrid, and on-premises environments.

-

2023 – NVIDIA launched enterprise Gen‑AI cloud services for synthetic media engines, enabling businesses to generate AI-driven video and avatar content at scale via its cloud platform.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.96 Billion |

| Market Size by 2032 | USD 16.84 Billion |

| CAGR | CAGR of 16.61% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Technology (Generative AI, Speech Synthesis, Computer Vision, Natural Language Processing (NLP), Others) • By Application (Media & Entertainment, Education & E-Learning, Healthcare, Retail & E-commerce, BFSI (Banking, Financial Services, and Insurance), Gaming, IT & Telecom, Others) • By Channel (Web-Based, Mobile Applications, Offline/Desktop Software, API/SDK Integration, Social Media Platforms) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM, Microsoft, Synthesis AI, Inc., NVIDIA Corporation, Deepbrain AI, Baidu, Inc., Adobe, DataRobot, Inc., OpenAI, Google (Alphabet Inc.), Runway ML, Synthesia, Hour One, Descript, Inc., Veritone, Inc., Rephrase.ai, Soul Machines, Resemble AI, LALAL.AI, D-ID |

Frequently Asked Questions

Ans: North America led the market with 39% revenue share in 2024, driven by strong digital infrastructure and early AI adoption across sectors.

Ans: The Solution segment dominated the market in 2024 with about 72% revenue share, due to widespread use of AI-powered content creation tools.

Ans: Rising adoption of generative AI for content creation in entertainment, marketing, and education is a key factor fueling market growth.

Ans: The Synthetic Media Market was valued at USD 4.96 billion in 2024, supported by increasing demand for personalized and scalable content solutions.

Ans: The Synthetic Media Market is expected to grow at a CAGR of 16.61% from 2025 to 2032, driven by AI adoption across key industries.

Get in Touch