Teleradiology Market Size:

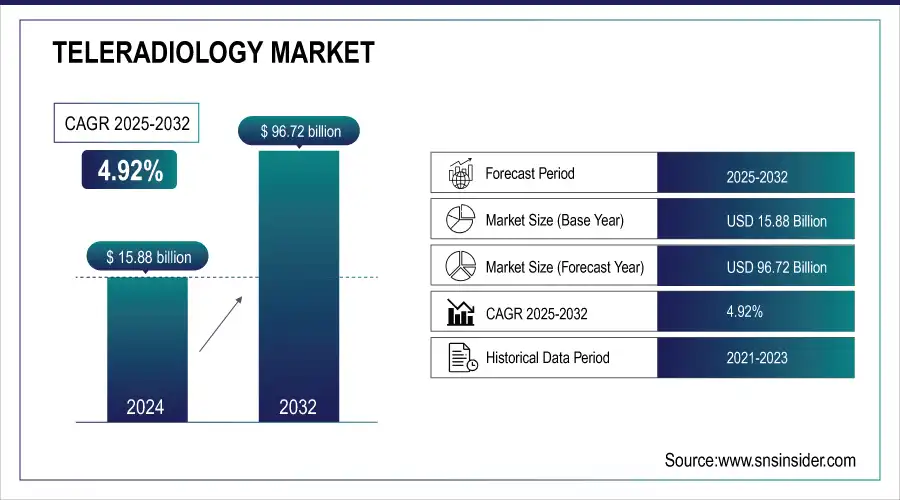

The Teleradiology Market Size was valued at USD 19.91 billion in 2025 and is expected to reach USD 190.81 billion by 2035, growing at a CAGR of 25.36% over the forecast period 2026-2035.

Get more information on Teleradiology Market - Request Free Sample Report

The Teleradiology industry is growing at the speed of light, thanks to advanced technological developments and increasing worldwide demand for fast and accurate diagnostic services. Teleradiology makes it possible to securely send radiological images (X-rays, CT, MRIs) for interpretation from one location to another and in doing so enable a diagnosis by experts distant from the patient. The National Institutes of Health (NIH) states that due to chronic diseases such as heart disease and cancer, demand for diagnostic imaging continues to increase. According to the Centers for Disease Control and Prevention (CDC), cardiovascular diseases result in about 17.9 million lost lives every year across the globe where diagnostic imaging has enormous contribution to early diagnosis and patient management. Furthermore, cancer imaging is growing steadily, with the National Cancer Institute (NCI) projecting over 1.9 million new cancer cases in the U.S. alone for 2023, emphasizing the need for scalable diagnostic solutions like teleradiology.

Key Teleradiology Market Trends:

-

Integration of AI and deep learning algorithms enhances diagnostic accuracy, reduces reading times, and supports radiologists in complex cases.

-

Cloud-based teleradiology platforms enable secure remote access to imaging data, improving collaboration between hospitals, clinics, and radiology experts globally.

-

Adoption of advanced imaging modalities like MRI, CT, and PET with remote reporting increases workflow efficiency and patient care quality.

-

Expansion of outpatient and rural imaging centers drives demand for teleradiology services to address radiologist shortages and improve timely diagnosis.

-

Regulatory compliance, data security, and HIPAA adherence are shaping investments in secure tele-imaging platforms and healthcare IT infrastructure.

-

Teleconsultation and cross-border reporting services are rising, facilitating 24/7 diagnostic support and bridging gaps in specialist availability worldwide.

Telehealth adoption, including teleradiology, surged during the COVID-19 pandemic. The U.S. Department of Health and Human Services (HHS) reported a 63-fold increase in telehealth utilization within Medicare, rising from approximately 840,000 visits in 2019 to 52.7 million in 2020. This growth highlighted the importance of remote healthcare solutions in maintaining continuity of care during emergencies.

HIPAA and other privacy regulations have been an important enabler for teleradiology. Secure encrypted government approved platforms to receive and store images so that both patients and providers has nothing to worry about. Research shows that 60% of data breaches are prevented when HIPAA-compliant systems are in place, which then encourages healthcare providers to use those portals due to trust between end users and the service provider.

Teleradiology Market Drivers:

-

Technological advancements, increasing healthcare demands, and evolving regulatory frameworks.

One of the main drivers is a growing imaging workload worldwide, with the American College of Radiology (ACR) predicting that radiologist productivity must rise by 30% to keep pace with demand. This divide is further widened by the increasing occurrence of chronic conditions. As a case in point, an increased demand for musculoskeletal imaging has been reported by the all-important Global Burden of Disease Study5 over the past decade and it is remote interpretation (here Teleradiology) that needs to cater to it.

The march of technology – especially the convergence of 5G and AI – is re-shaping how teleradiology works. According to a research published by U.S. National Library of Medicine, AI tools can increase diagnostic accuracy up to 95% for some imaging applications, greatly lighten the workload of radiologists. Moreover, 5G networks improve the efficiency of image transmission which is faster and more stable, thereby supporting synchronous clinic consultations.

Regulations enabling telehealth have also driven market expansion. The U.S. Health Resources and Services Administration (HRSA) announced a 36% increase in funding for telehealth programs in fiscal year 2023, underlining the value of remote care service such as teleradiology. Worldwide governments are promoting the use of digital health, and teleradiology is no exception especially considering that it offers cost-effective solutions for rural and poor areas.

Growing if uptake of cloud-based solutions is also driving the market as HIPAA-certified systems provide secure storage and rapid accessibility of imaging data. According to recent studies, cloud adoption can result in savings of 20% for operational costs- and this reduced cost makes a solution appealing to healthcare providers.

Teleradiology Market Restraints:

-

Data Security and Privacy Concerns

Due to the threat of cyberattacks and/or data breaches, it is challenging to transfer and store medical PS images. Even though measures such as HIPAA are implemented, a 25% rise in data breaches in healthcare compared to 2023 (based on reports by the U.S. Department of Health and Human Services), led to concerns about patient privacy for teleradiology systems.

-

High Initial Implementation Costs

Developing a strong teleradiology platform requires significant effort and investment to secure the technology, networks, and training. According to an American Telemedicine Association report, small medical organizations are hampered with financial issues: The cost of a teleradiology solution can range from USD 100,000 to USD 1 million making it difficult for many smaller facilities to afford the technology.

Teleradiology Market Segmentation Analysis:

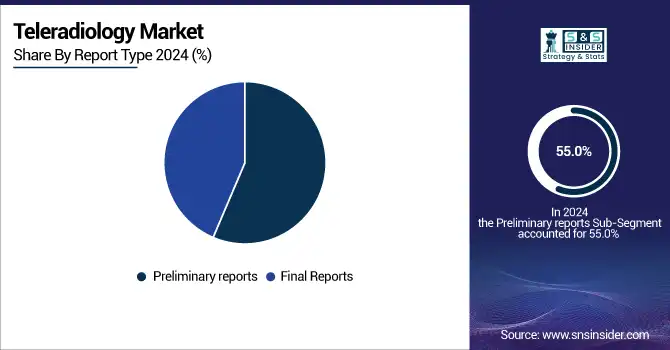

By Report Type, Preliminary Reports, Lead Market Share, and Final Reports are Growing Rapidly

Reading the preliminary reports was the leading segment in 2025, accounted for around 55.0% share of the market. Such a timely diagnostic interpretation is crucial in the context of emergency care because it drives clinical decision-making at bedside. Preliminary reports enable quick and accurate evaluation of radiology images to identify emergent conditions such as fractures, hemorrhages, or infections. With the rapid expansion of teleradiology systems on emergency departments and urgent care facilities stimulated by an escalating international deficit in radiologists, the dependence on preliminary reports has been growing rapidly. Also, with the development of real-time image transmission technology, the delay in preparing these reports could be minimized and there should be good acceptability.

End of report reading is the area showing the most rapid growth, driven by the need for comprehensive and validated radiological interpretations that adhere to clinical and legal requirements. Such analyses are subject to very strict scrutiny, providing a well-documented diagnosis used for targeted treatment. Final reports are being increasingly acknowledged by healthcare service providers to reach precise diagnosis, enhance patient care and stay in compliance with healthcare standards. The trend is quite severe in specialist settings such as oncology and neurology where definitive diagnosis is essential. Application of AI based tools that improve reporting accuracy by reducing discrepancies is contributing to the growth in the market for this segment as well.

By Product, X-Ray Dominates Teleradiology Market; MRI Shows Fastest Growth

X-ray was the leading category in 2025, with a share of approximately 40.0% in the market. X-ray is still the foundation of diagnostic radiology, as it is most affordable, available everywhere and can be adapted to use for variety of purposes. Its widespread application in the detection of fractures, lung diseases, infections and other musculoskeletal disorders has become a standard for care. Additionally, growing prevalence of respiratory disorders such as tuberculosis and pneumonia has increased the requirement for X-ray-based teleradiology services. This dominance has gained further leverage through the use of portable X-ray equipment, which also take and transmit digital images via Picture Archiving and Communication Systems (PACS), improving upon the efficiency with which X-rays can be transmitted and interpreted in remote communities.

The MRI segment is the most rapidly growing in the market as it offers high imaging resolution that is essential for diagnosis of complicated diseases. Because MRI allows detailed imaging of soft tissues, it is invaluable in the diagnosis of many diseases of the central nervous and cardiovascular systems. The ever growing implementation of high-speed data transfer is likely to provide lossless transmission of huge MRI image files, which encourages the use in remote radiological assessments. And, AI-based solutions are revolutionizing MRI reading, allowing rapid and accurate reads especially in the more complicated diagnoses. This technological progression and increasing understanding among medical professionals for the advantages of MRI teleradiology is increasing its demand in different healthcare institutions.

Teleradiology Market Regional Analysis:

North America Dominates the Teleradiology Market in 2024

North America holds an estimated 40% market share in 2024, driven by advanced healthcare infrastructure, a growing radiologist shortage, and high adoption of digital imaging technologies, which accelerates teleradiology implementation across hospitals and diagnostic centers.

Need any customization research on Teleradiology Market - Enquiry Now

-

United States Leads North America’s Teleradiology Market

The market for radiological information systems is led by the US, which has a developed healthcare sector, a large amount of spending on health IT and high consumption rates for both chronic conditions and acute diseases. PACS, high speed internet and AI based diagnostic tools allow for immediate transmission and interpretation of the images. Moreover, growing trend of remote consultations and telehealth implementation rising government incentives for digital healthcare solutions also solidify U.S. as the dominating contributor to North America teleradiology market growth.

Asia Pacific is the Fastest-Growing Region in the Teleradiology Market in 2024

Asia Pacific is projected to grow at an estimated CAGR of 12.5%, fueled by rising healthcare awareness, increasing chronic disease burden, and government initiatives promoting telemedicine, which boosts adoption of teleradiology solutions.

-

China Leads Teleradiology Market Growth in Asia Pacific

China leads with rapid urbanization and large population needing immediate diagnostic imaging and government investments in telehealth infrastructure. High utilization of cloud teleradiology platforms and AI-aided imaging tools increases the accessibility in remote areas. Both peer-to-peer sharing between both hospitals and diagnostic centers as well as among technology vendors speeds implementation. Moreover, growing incidence of cardiovascular, neurological and orthopedic diseases further surge demand for imaging, making China the focal point in top provider of teleradiology solution across APAC.

Europe Teleradiology Market Insights, 2024

Europe holds a large market share, owing to rise in the demand for teleradiology services in remote areas, rise in cross border healthcare and advanced imaging technologies. Ease of diagnostic processes, backed by aggressive uptake of digital healthcare in Germany, help to enhance the efficiency level in diagnostics accelerating the market growth of teleradiology. Notably, Germany leads by virtue of its sophisticated hospital systems, dense population of radiologists and extensive IT adoption. The government is promoting use of digital health facilities through national e-health programs. Advanced PACS deployment and AI-based imaging enable faster diagnostics, improve reporting accuracy and reduce turnaround time. In terms of the political, technical and medical-structural components, Germany has become an example for teleradiology implementation in Europe.

Middle East & Africa and Latin America Teleradiology Market Insights, 2024

Growth in the Middle East & Africa and Latin America is mainly driven by adoption of telemedicine, growth in private healthcare industry, and increase in awareness of early detection of diseases. Cloud-based teleradiology platforms and AI-assisted imaging systems are helping improve diagnostic efficiency in nations such as the UAE, Saudi Arabia, Brazil and Mexico. Market adoption is being driven by the growing number of imaging centers, international radiology service providers and rural healthcare accessibility efforts. Although they trail behind North America, Europe and Asia Pacific region, these regions are establishing themselves as key markets for teleradiology solutions.

Competitive Landscape for the Teleradiology Market companies:

Virtual Radiologic (vRad)

Virtual Radiologic (vRad) is a U.S.-based practice partnering with local radiology practices, providing remote reads for its customers. Their team has a combined total of over 30 years experience, and they provide X-ray MRI, EN CT readings as well as other diagnostic imaging services to aid in reducing turn-around times so patients can benefit from faster treatment. vRad is a national network of board certified radiologists providing multi-modality interpretation in every subspecialty using highly advanced PACS and reporting systems for unparalleled physician collaboration and patient care. Its significance in the teleradiology market is paramount due to the provision of 24/7 radiology support, enhanced accuracy of diagnosis and availability of healthcare facilities in distant and rural locations.

-

In March 2025, vRad expanded its AI-assisted imaging platform, enabling faster detection of critical conditions such as fractures, lung nodules, and neurological abnormalities, enhancing efficiency and diagnostic accuracy.

Agfa-Gevaert Group

About Agfa-Gevaert Group, The Agfa-Gevaert Group is headquartered in Belgium and supplies medical imaging directly to hospitals and other healthcare providers and the DR 600 digital radiography, PACS, Enterprise Imaging solutions. The company focuses on automation of images’ acquisition, storage and management processes, helping hospitals and clinics in increasing the efficiency of delivering accurate general diagnostics. PHILIPS: Agfa-Gevaert’s next-gen imaging software helps improve reading productivity for radiologists, enables remote care delivery and encourages interoperability between healthcare facilities. Its position in the teleradiology space is core, delivering the technology that supports vital images to be sent and read anywhere in the world.

-

In January 2025, Agfa-Gevaert launched an upgraded PACS module with AI-assisted image analysis, improving radiology workflow efficiency and supporting remote teleradiology services globally.

ONRAD Inc.

ONRAD, Inc. is a leading U.S-based teleradiology provider offering 24 x 7 remote reading services for radiographic exams to hospitals, imaging centers and select specialty clinics. It provides X-ray, MRI, CT and ultrasound interpretations through a network of board-certified radiologists and cloud-based ultramodern technology to empower rapid image access. This is a win-win for ONRAD, it results in better quality interpretations, which is more satisfying work for our radiologists and benefits the clients. Its position in the teleradiology industry is crucial to deliver scalable, dependable and high-quality imaging services to healthcare institutions.

-

In May 2025, ONRAD implemented a cloud-native AI platform for automated preliminary readings, accelerating emergency diagnostics and optimizing radiology workflows across partner facilities.

Everlight Radiology

About Everlight Radiology Everlight Radiology is the U.K.’s largest teleradiology company, providing remote diagnostic reporting services to hospitals, clinics and imaging centers globally. Services include X-ray, CT, MRI and mammography readings through a team of board-certified radiologists as well as the leading-edge PACS solutions. Everlight increases radiology coverage, lowers turnaround times and maintains a consistent level of diagnostic quality. It plays a key role in the teleradiology market, bringing healthcare to the far corners of our world and enabling 24/7 radiology services.

-

In February 2025, Everlight Radiology introduced AI-powered decision support tools for chest and musculoskeletal imaging, improving reporting accuracy and enabling faster remote diagnostics.

Teleradiology Market Key Players:

Teleradiology Market Companies

-

Agfa-Gevaert Group

-

ONRAD, Inc.

-

Everlight Radiology

-

4ways Healthcare Ltd.

-

RamSoft, Inc.

-

USARAD Holdings, Inc.

-

Koninklijke Philips N.V.

-

Matrix (Teleradiology Division of Radiology Partners)

-

Teleradiology Solutions

-

All-American Teleradiology

-

Philips Healthcare

-

GE Healthcare

-

Mednax Services, Inc.

-

Cerner Corporation

-

TeleDiagnostic Solutions, Inc.

-

NightHawk Radiology Services

-

RADNet, Inc.

-

vRad Health Systems

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.91 billion |

| Market Size by 2035 | USD 190.81 billion |

| CAGR | CAGR of 25.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Computed Tomography (CT), Ultrasound, X-ray, Nuclear Imaging, Magnetic Resonance Imaging (MRI)) • By Report Type (Preliminary Reports, Final Reports) • By End-Use (Hospital, Radiology Clinics, Ambulatory Imaging Center) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Virtual Radiologic (vRad), Agfa-Gevaert Group, ONRAD, Inc., Everlight Radiology, 4ways Healthcare Ltd., RamSoft, Inc., USARAD Holdings, Inc., Koninklijke Philips N.V., Matrix (Teleradiology Division of Radiology Partners), Medica Group PLC, Teleradiology Solutions, All-American Teleradiology, Philips Healthcare, GE Healthcare, Mednax Services, Inc., Cerner Corporation |

Frequently Asked Questions

Teleradiology Market is expected to reach USD 190.81 billion by 2035.

North America holds the biggest offer in the teleradiology market.

The by Products Type is divided into FIive sub segments is Computed Tomography (CT), Ultrasound, X-Ray, Nuclear Imagingand Magnetic Resonance Imaging (MRI)

The challenges faced by Teleradiology is Breach of data and cyber-threats.

Ans: TheTeleradiology Market is growing at a CAGR of 25.36% over the forecast period 2026-2035.

Get in Touch