Textile Chemicals Market Report Scope & Overview:

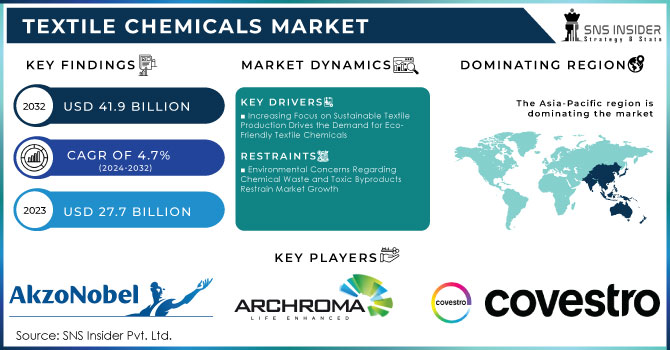

The Textile Chemicals Market Size was valued at USD 27.7 billion in 2023 and is expected to reach USD 41.9 billion by 2032 and grow at a CAGR of 4.7% over the forecast period 2024-2032.

Dynamic changes are occurring in the textile chemicals market, which is driven by increased demand from rising consumers for sustainable and eco-friendly solutions and also pressure to meet stringent environmental regulations. Therefore, bio-based chemicals become more prominent because producers are focusing on efforts to reduce environmental impacts from textile production. For example, in July 2024, leading textile chemical companies began exploring bio-based feedstocks as an alternative to traditional petrochemical inputs for greener alternatives. This trend also aligns with rising attention to the circular economy model as well as decreasing chemical waste from initiatives within various industries around the globe. Other drives in demand for sustainable options include consumer awareness and policies implemented by governmental bodies encouraging manufacturers to use non-polluting, renewable chemicals in their textile production processes.

Textile Chemicals Market Size and Forecast

-

Market Size in 2023: USD 27.7 Billion

-

Market Size by 2032: USD 41.9 Billion

-

CAGR: 4.7% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get more information on Textile Chemicals Market - Request Sample Report

Textile Chemicals Market Trends

-

Growing demand for performance and functional textiles is driving textile chemicals consumption, with the global market expanding at a CAGR of over 4–5%, supported by rising sportswear and technical textile production.

-

Increasing focus on sustainable processing is accelerating adoption of bio-based and low-VOC chemicals, with over 35% of textile manufacturers shifting toward eco-friendly formulations.

-

Expansion of textile manufacturing in Asia-Pacific, which accounts for more than 55% of global textile output, is boosting demand for dyes, auxiliaries, and finishing agents.

-

Rising implementation of water-saving and energy-efficient processing technologies is reducing water usage by 20–30%, increasing demand for high-performance specialty chemicals.

-

Growth in home textiles and apparel exports is strengthening demand for colorants and finishing chemicals, with global textile trade growing at over 6% annually in key exporting nations.

Notable recent developments from industry leaders support this evolving direction toward sustainability. For instance, in January 2024, ERCA Group unveiled a new line of textile chemical solutions to enable the acceleration of the circular revolution in textile manufacturing. This entire effort centers around waste reduction and reutilization of resources as part of an industry movement toward the closing of the loop in textile production. Thus, ERCA Company, like other such organizations, seems to be trying increasingly hard to get the innovations of the company to be aligned with the principles of a circular economy not just to decrease the environmental footprint but also to enhance cost-effectiveness. The same line was also observed when the company, Fibre2Fashion, saw its portfolio expand in February 2024, offering solutions that could contribute to efficiency and sustainability in textile chemical production. This thirst for more extensive services manifests the ever-growing demand for chemical efficiency in the textile industry, an industry in which environmental sustainability has been the primary imperative that ensures the successful assimilation of innovation.

The other notable development was when the government and the industry were on discussion terms to find a solution to the problems resulting from this industry. In October 2022, for example, it was a summit of several countries manufacturing textiles together, united under one aim, to minimize the chemical wastes generated in the manufacturing of textiles. This collaboration was geared toward stronger handling of chemical waste management and the establishment of the use of environment-friendly chemicals, partly in line with an international campaign that targets reducing adverse environmental impacts resulting from textile production. This work of most countries worldwide showcases more concerted efforts toward global cooperation over the responsible use of sustainable chemicals in textile production.

Investments in the textile chemical sector are unrelenting, and multinational companies are staunch contributors to the growth of the market. This January, 10 multinational companies announced a total investment of Tk 2000 crore in the textile chemicals market, further investing in the process of achieving enhanced production capacities and scaling up sustainable chemical solutions. These investments reflect the major players' confidence in the future of textile chemicals, particularly in developing countries, where much of the manufacturing takes place. The large-scale investments support the innovation for chemical formulations and show longer-term commitments to improving sustainability across the entire textile value chain. These trends altogether represent the quick transformation of the textile chemical market in reaction to pressures from the environment and industry-led initiations.

Textile Chemicals Market Dynamics

KEY DRIVERS:

-

Increasing Focus on Sustainable Textile Production Drives the Demand for Eco-Friendly Textile Chemicals

The regulation pressure coupled with consumer demand, more and more, makes the textile industry shift toward sustainable production practices. Textile chemicals are important for enhancing the quality and functionality of fabrics. However, the pollution caused by the use of chemical products has created concern over these chemicals' impact on the environment. Manufacturers have developed bio-based and biodegradable chemicals to ensure that pollution is kept at the lowest level, thereby reducing the carbon footprint of this industry. The increased severity of government regulations within regions such as Europe and North America has also helped drive the adoption of green textile chemicals. These regulations are directly related to corporate social responsibility while also providing an avenue through which businesses may comply with international standards on environmental concerns. This much broader focus on sustainability has opened up new possibilities for innovation and product development by chemical companies. With products geared towards the concept of the circular economy, for instance, with water-efficient dyes and non-toxic coatings, this trend has led to accelerated growth in the textile chemicals market.

-

Technological Advancements in Textile Chemical Formulations Enhance Fabric Quality and Durability

Advances in the formulating of chemicals for textiles have led to innovations in high performance chemicals that dramatically improve the durability, colorfastness, and quality of fabrics. Nanotechnology-based chemicals and smart coatings offer opportunities to create functional textiles that possess such characteristics as water repellency, UV protection, and antimicrobial functionalities. Since high-performance fabrics are exactly what these industries need, such innovations are presently being widely applied in sportswear, healthcare, and automotive textiles. Moreover, durable and functional textiles have enabled manufacturers to meet changing demands for high-quality and durable products from consumers. In addition, resource efficiency can be achieved by fewer times of washing, a lesser amount of water usage, and longer lifecycles of textiles. Advanced chemicals that enhance the performance of the fabric have been a boon in their own right for the textile chemicals market.

RESTRAIN:

-

Environmental Concerns Regarding Chemical Waste and Toxic Byproducts Restrain Market Growth

Although many innovations have been made in sustainable textile chemicals, the core problems of this industry are its disposal of chemical wastes and the management of toxic by-products. Most of these textile chemicals contain elements that pose dangers to humans and the environment. Improper means of dealing with and disposing of the chemicals have caused pollution of water and soil, hence increased regulatory scrutiny. However, since the environmental regulations of developing regions may not be strict, and in many cases are probably quite lax, these problems are compounded, which makes the problem even worse. In response to this, manufacturers are pressured to create waste management systems that have a more minimal impact on the environment in which their processes take place. These costs related to safe disposal, besides the adoption of greener alternatives, have been the major growth inhibitors of this market, especially for small players who do not have adequate funds to invest in green solutions.

OPPORTUNITY:

-

Surging demand for functional and high-performance textiles opens up opportunities for innovation in chemical applications in textile fabrics.

Functional textiles, such as fabrics having flame-retardant properties, water-resistance, and antimicrobial action-open up major opportunities for innovation in textile chemicals. More sectors - constructive, military, sportswear, and healthcare areas - use high-performance textiles where specific functionalities are more critical. Antimicrobial fabrics, for example, gained increased demand because of raised hygiene requirements, especially in the healthcare sector, which has become tougher after the recent global health challenges. Simultaneously, through the demand for durable and weather-resistant textiles in the outdoor apparel and construction industries, developments of advanced chemical treatments in fabrics are being made. This growing interest in functional textiles provides opportunities for innovation in the development of specialized products specifically tailored to meet the requirements of various industries. The key to the successful exploitation of such emerging opportunities will be the ability to produce chemicals that improve fabric performance with environmental sustainability.

CHALLENGES:

-

Stringent Environmental Regulations Pose Challenges for Traditional Textile Chemical Manufacturers

The most challenging task for the textile chemicals market derives from increasingly stringent environmental regulations nowadays. Due to the environment, governments in regions such as Europe and North America, as well as parts of Asia, are imposing more stringent rules on the production, use, and disposal of textile chemicals, especially hazardous ones to the environment. These regulations, therefore, make the manufacturer think about their processes of manufacturing and move towards greener alternatives, which will be relatively expensive and time-consuming. Updating their standards to meet these regulations for traditional chemical manufacturers who have enjoyed the supply chains of conventional, petrochemical-based products for years requires a good amount of investment in research and development. Even the process of regulatory compliance is complicated by the presence of several certification and audit agencies and increases the operational costs. The biggest challenge in the textile chemicals market is that of balancing regulatory compliance with profitability requirements, particularly for firms that still rely on traditional chemical formulations.

Textile Chemicals Market Segments

By Fiber Type

In 2023, synthetic fiber dominated the textile chemicals market. With a market share of more than 60% of the market. This can be attributed to high usage of synthetic fibers, especially polyester, nylon, and acrylic, in various industrial applications such as clothing, automotive, and home textiles. Synthetic fibers are most desired for excellent durability and resistance to shrinkage and retention of color as well as shape even when exposed to multiple washes, thereby making them highly essential in high-performance applications. Besides, synthetic fibers face less environmental degradation than natural fibers, which in turn increase demand for such fibers. Synthetic fibers treated with advanced chemicals have thus been widely used by sportswear industries that assure moisture-wicking and antimicrobial properties to fabrics for providing high functionality, comfort, and freshness. Besides the domination of synthetic fibers in the textile chemicals market, the only advantage this has over the natural fibers is that synthetic fibers are a better product than their natural competitors since synthetic fibers outperform them in terms of cost-effectiveness.

By Product Type

The colorants & auxiliaries segment dominated the textile chemicals market, accounting for more than 35% of the market share in 2023. This is primarily on account of the rising demand for bright, rich, and high-quality dyes in the fashion and apparel industry. Colorants are required for fabrics, which serve to provide hard-wearing and long-lasting vibrant shades, and auxiliaries help facilitate dye penetration and also fabric treatment to ensure uniform coloring. Advanced colorant usage has largely increased in the fashion industry due to its aesthetic appeal and fast-fashion trends. However, with the rising trend of using eco-friendly and non-toxic dyes, innovation in this domain is equally on the upswing. For example, water-efficient and bio-based dyeing processes are becoming increasingly popular these days, mainly in textile hubs like India and China which are among the largest consumers of colorants and auxiliaries.

By Application

In 2023, the apparel segment dominated the textile chemicals market, accounting for an estimated 45% market share. The sustenance of this position is supported by the continued growth of the global fashion industry besides increasing demand for high-quality functional as well as sustainable clothing amongst consumers. Some commonly used textile chemicals in the manufacturing of apparel include colorants, finishing agents, and surfactants, thereby enhancing the durability, appearance, and performance of fabrics. The current rise in fast fashion and athleisure has further pushed the need for more advanced chemicals in textiles that can achieve stretchable, moisture-wicking, and stain-resistant clothing. Currently, chemical treatments are gaining increasing prevalence in wrinkle-free and antimicrobial clothing products aligned with consumer demands for convenient, hygienic, and low-maintenance garment wear. In contrast, the new thrust in environmentally friendly fashion has pushed more pressure for developments in sustainable chemicals for textile apperceiving.

Textile Chemicals Market Regional Analysis

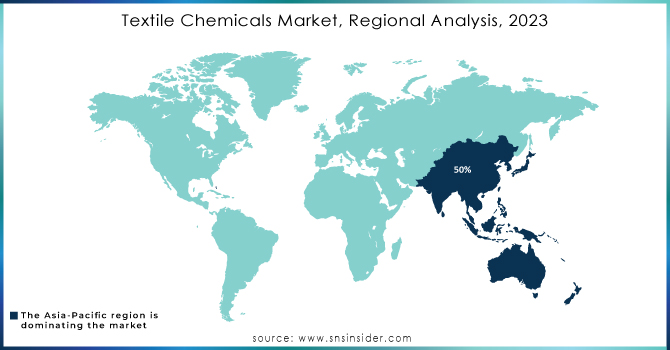

The Asia-Pacific region dominated textile chemicals in 2023, accounting for more than 50% market share. This is mainly attributed to being a strong base for textile production in countries such as China, India, Bangladesh, and Vietnam. The region is one of the largest textile and apparel exporting blocks in the world. Therefore, the demand for textile chemicals arises from the need for chemicals in dyeing, finishing, and fabric treatments. China being one of the world's biggest producers of textiles, is making heavy use of chemicals that ensure quality along with international standards for the produced fabrics. Cheap labor and raw materials available in the region itself have made it the top for textile manufacturing, and this also increases its consumption of textile chemicals. For example, the PLI scheme initiated for textiles by the government of India has supplemented growth in the industry and multiplied their requirement for textile chemicals.

Get Customized Report as per your Business Requirement - Request For Customized Report

Textile Chemicals Market Key Players

-

AkzoNobel NV (Interpon powder coatings, Bonderite chemical pretreatment)

-

Archroma (Livaqua dyes, Smartrepel Eco water repellents)

-

Covestro (Desmophen polyols, Bayhydur crosslinkers)

-

Croda International Plc (Crodasurf surfactants, Crodapearl emulsifiers)

-

DowDuPont (DOWSIL silicone additives, BETASEAL adhesives)

-

Evonik Industries (TEGO textile additives, AEROSIL fumed silica)

-

FCL (FCL Textile Dyes, FCL Auxiliaries)

-

Huntsman International LLC (Avalon dyes, Syntheton textile chemicals)

-

Indofil (IndoPrint dyes, Indosperse dispersing agents)

-

Kemin Industries (Kemin Dyestuff, Kemin Textile Treatments)

-

OMNOVA Solutions Inc (Nexis functional additives, VITEL thermoplastic elastomers)

-

Rudolf GmbH (Rudolf Group Textile Finishing Agents, Eco-Pearl water repellents)

-

TANATEX Chemicals B.V. (Tanatex Textile Auxiliaries, Tanacoat finishing agents)

-

GIOVANNI BOZZETTO S.p.A. (Bozzetto dyes, Bozzetto finishing agents)

-

BASF SE (BASF textile dyes, Ecolab cleaning agents)

-

Clariant International Ltd (Clariant dyes, Clariant textile chemicals)

-

Dystar Group (DyStar dyes, Texapret textile auxiliaries)

-

Sarex Chemicals (Sarex dyes, Sarex finishing agents)

-

Wacker Chemie AG (Wacker silicone emulsions, Wacker textile finishing agents)

-

Zschimmer & Schwarz (Zschimmer textile dyes, Zschimmer & Schwarz auxiliaries)

Raw Material Suppliers in the Textile Chemicals Market

-

BASF SE

-

DowDuPont

-

Evonik Industries

-

SABIC

-

Solvay

-

Clariant International Ltd

-

Eastman Chemical Company

-

Wacker Chemie AG

-

Huntsman International LLC

-

Chemtura Corporation

Users in the Textile Chemicals Market

-

Apparel Manufacturers

-

Home Textile Manufacturers

-

Automotive Textile Suppliers

-

Technical Textile Producers

-

Fashion Brands

-

Interior Decor Companies

-

Sporting Goods Manufacturers

-

Hospitality Industry (Hotels, etc.)

-

Medical Textile Companies

-

Textile Retailers

RECENT DEVELOPMENTS

-

April 2024: BASF SE announced the company's portfolio of polyamides for the textile industry. The company's sustainable polyamide PA6 and PA6.6 product range have been certified under the Recycled Claim Standard -Textile applications. This certification gives the right to BASF SE to market textiles produced using recycled raw materials.

-

October 2024: Researchers developed water-proof coatings from textile waste, thereby inducting sustainability into the textile chemicals industry.

-

January 2023: Ten multinational companies invested Tk 2,000 crore to textile chemicals showing a robust commitment toward increasing production capacity and sustainability to the industry.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 27.7 Billion |

| Market Size by 2032 | USD 41.9 Billion |

| CAGR | CAGR of 4.7% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Fiber Type (Natural Fiber, Synthetic Fiber) •By Product Type (Coating & Sizing Agents, Colorants & Auxiliaries, Finishing Agents, Surfactants, Desizing Agents, Bleaching Agents, Denim Finishing Agents, Others) •By Application (Apparel, Home Textile, Technical Textile, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Archroma, DowDuPont, Evonik Industries, TANATEX Chemicals B.V., GIOVANNI BOZZETTO S.p.A., Kemin Industries, Covestro, OMNOVA Solutions Inc, FCL, Indofil, Huntsman International LLC, Wacker Chemie AG, Rudolf GmbH, AkzoNobel NV, Croda International Plc and other key players |

| Key Drivers | •Increasing Focus on Sustainable Textile Production Drives the Demand for Eco-Friendly Textile Chemicals •Technological Advancements in Textile Chemical Formulations Enhance Fabric Quality and Durability |

| Restraints | •Environmental Concerns Regarding Chemical Waste and Toxic Byproducts Restrain Market Growth |

Get in Touch