Propylene Carbonate Market Report Scope & Overview:

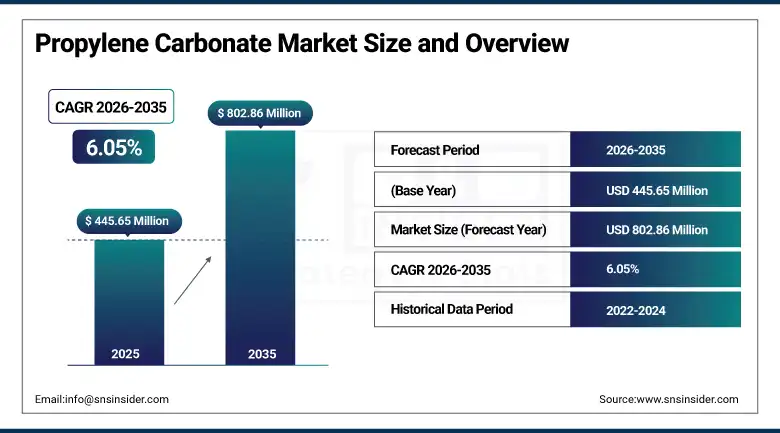

The Propylene Carbonate Market was valued at USD 445.65 Million in 2025 and is expected to reach USD 802.86 Million by 2035, growing at a CAGR of 6.05% from 2026–2035.

The global propylene carbonate market is growing at a sustained and commercially significant pace. Propylene carbonate (PC) is a cyclic organic carbonate produced from propylene oxide and carbon dioxide. As an aprotic polar solvent, PC dissolves a wide range of organic and inorganic compounds including lithium salts, polar polymers, and refractory materials, making it indispensable in lithium-ion battery electrolytes, industrial coatings, adhesive formulations, and pharmaceutical synthesis. The primary driver of market growth is rising demand for lithium-ion batteries whose electrolyte formulation requires PC as a co-solvent, combined with increasing regulatory restrictions on conventional VOC-emitting solvents that position PC as an environmentally compliant alternative in paints, coatings, and cleaning applications.

In 2024, BASF expanded its propylene carbonate production capacity at its Ludwigshafen facility, targeting growing European demand from lithium-ion battery manufacturers establishing gigafactory production in Germany, France, and Hungary. The expansion responds to the EU Battery Regulation’s mandated domestic battery supply chain requirements whose accelerated European gigafactory construction is creating structured regional propylene carbonate procurement that previously relied on Asian import supply chains. The facility expansion reflects BASF’s commercial strategy of aligning production capacity with the European battery manufacturing investment cycle.

Market Size and Forecast

-

Market Size in 2026E: USD 472.59 Million

-

Market Size by 2035: USD 802.86 Million

-

CAGR: 6.05% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Propylene Carbonate Market - Request Free Sample Report

Propylene Carbonate Market Trends

-

Battery-grade high-purity propylene carbonate demand is increasing due to EV gigafactories requiring electrolyte-grade solvents with strict impurity control standards.

-

VOC regulation tightening under REACH and EPA frameworks is driving solvent substitution toward propylene carbonate due to low volatility and biodegradability.

-

Bio-based propylene carbonate production using CO₂ utilization and bio-propylene oxide is gaining traction as a sustainable green chemistry alternative.

-

Pharmaceutical applications are expanding, with propylene carbonate used as a carrier solvent in drug delivery and API synthesis processes.

-

Solid-state and hybrid battery research is increasing demand for propylene carbonate in next-generation electrolyte and gel polymer systems.

The U.S. Propylene Carbonate Market Outlook

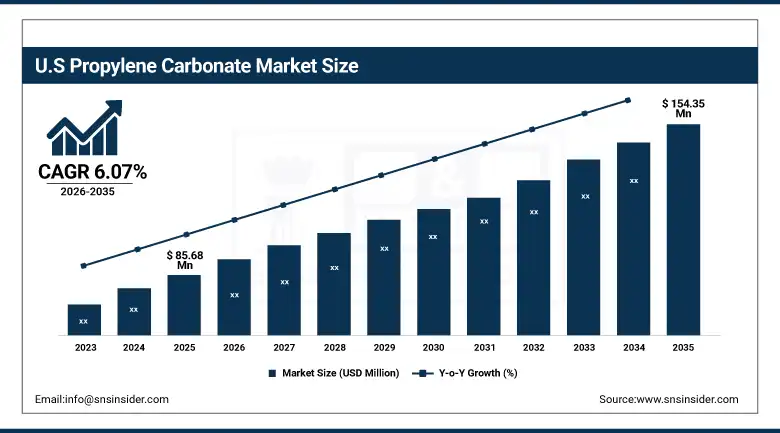

The U.S. propylene carbonate market was valued at approximately USD 85.68 Million in 2025 and is expected to reach approximately USD 154.35 Million by 2035, growing at a CAGR of approximately 6.07%.

The U.S. is the most commercially significant propylene carbonate market within the fastest-growing North American region. Huntsman Corporation, LyondellBasell, and Lonza’s U.S. chemical operations serve the domestic market across industrial solvent, battery electrolyte, and specialty chemical applications. EPA’s VOC regulations create structured specification motivation for PC adoption in coatings and cleaning formulations where conventional solvent alternatives face compliance restriction. The domestic EV battery gigafactory investment, including Tesla’s Nevada facility, LG Energy Solution’s Michigan plant, and Panasonic’s Kansas facility, creates growing domestic battery-grade PC procurement whose IRA domestic content preference creates supply chain localization motivation.

Huntsman Corporation completed the qualification of its Jeffsol PC electrolyte-grade propylene carbonate at battery-grade purity specification in 2024, targeting the growing U.S. EV battery manufacturer market. The qualification reflects the commercial opportunity created by IRA’s domestic content requirements for EV battery supply chains whose incentive creates economic motivation for U.S. battery manufacturers to specify domestic chemical suppliers over lower-cost Asian alternatives.

Propylene Carbonate Market Segment Analysis

-

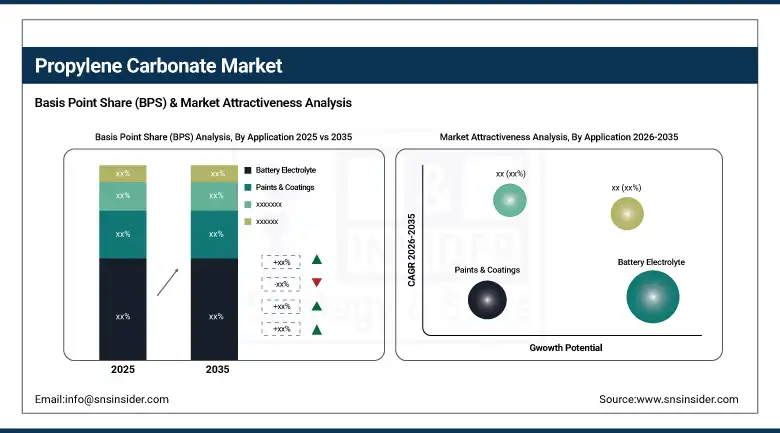

By Application, the battery electrolyte/lithium-ion batteries segment dominated the market with approximately 42% share in 2025, while the solvent segment is the fastest growing.

-

By Grade, the industrial grade segment dominated the market with approximately 55% share in 2025, while the battery grade/high purity segment is the fastest growing.

-

By End User, the electronics & battery manufacturing segment dominated the market with approximately 46% share in 2025, while the paints & coatings segment is the fastest growing.

By Application, battery electrolyte dominates, solvent grows fastest

Battery electrolyte retained the dominant application position with approximately 42% of the propylene carbonate market in 2025. PC’s role as an electrolyte co-solvent in lithium-ion batteries reflects its exceptional lithium salt dissolution capability, wide electrochemical stability window, and high dielectric constant that collectively create superior ionic conductivity in electrolyte formulations. While ethylene carbonate serves as the primary high-boiling co-solvent in most commercial lithium-ion electrolyte formulations, PC’s lower melting point of -49°C enables low-temperature electrolyte operation that sustains ionic conductivity in cold climate EV applications where EC’s higher freezing point creates conductivity limitation.

Solvent is the fastest-growing application because VOC emission regulation’s progressive tightening across North America, Europe, and progressively Asia Pacific is creating systematic substitution demand for low-VOC solvent alternatives in coating, cleaning, and chemical synthesis applications. PC’s vapor pressure of 0.04 mmHg at 25°C, compared to 30-100 mmHg for conventional organic solvents, creates VOC compliance advantage whose regulatory value sustains specification preference in regulatory-sensitive procurement contexts. Each new EPA VOC rule tightening and each EU REACH restriction creates commercial motivation for PC adoption in applications where conventional solvent alternatives face compliance restriction.

By Grade, industrial grade dominates, battery grade grows fastest

Industrial grade propylene carbonate retained the dominant grade position with approximately 55% of the propylene carbonate market in 2025. Industrial grade’s commercial primacy reflects the cost-competitive economics that standard synthesis quality PC provides for the majority of solvent, coating additive, and chemical synthesis applications whose performance requirements are satisfied by conventional purity specifications without the additional purification investment that battery and pharmaceutical grades require. Each industrial solvent application, coating formulation, and adhesive production programme that specifies PC creates industrial-grade procurement whose aggregate across the broad range of non-battery PC applications sustains the grade category’s commercial dominance.

Battery grade is the fastest-growing grade because the EV battery gigafactory commissioning cycle is creating new high-purity PC procurement at scales and specifications that industrial-grade alternatives cannot satisfy. Battery electrolyte qualification’s sub-10 ppm metal contamination requirement, moisture specification below 20 ppm, and color specification creates a distinct premium product category whose qualification investment creates commercial differentiation that sustains above-commodity pricing. BASF’s European capacity expansion and Huntsman’s U.S. battery-grade qualification each demonstrate the commercial investment that battery-grade PC’s premium procurement motivates.

By End User, electronics & batteries dominate, paints & coatings grow fastest

Electronics and battery manufacturing retained the dominant end-user position with approximately 46% of the propylene carbonate market in 2025. The lithium-ion battery industry’s extraordinary production capacity expansion, creating tens of gigawatt-hours of annual new battery manufacturing capacity across Asia, Europe, and North America, creates proportional PC procurement whose scale compounds with each successive year of EV market adoption. Consumer electronics’ portable device batteries create additional consistent industrial-grade PC procurement that sustains electronics and battery manufacturing’s aggregate commercial dominance across both premium EV and standard consumer electronics battery applications.

Paints and coatings is the fastest-growing end user because VOC regulation’s systematic restriction of conventional high-VOC solvent use in architectural, automotive, and industrial coating formulations is creating structured substitution demand for PC whose low-VOC profile creates regulatory compliance capability that conventional alternatives cannot provide. Each new VOC regulation jurisdiction that restricts conventional solvent use creates a new commercial PC adoption opportunity whose aggregate across multiple simultaneous regulatory programmes globally creates systematic demand growth that compounds with coating market volume expansion.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Propylene Carbonate Market Insights

North America is the fastest-growing regional propylene carbonate market, driven by IRA domestic content incentives creating EV battery supply chain localization, EPA VOC regulation driving solvent substitution, and pharmaceutical sector growth creating premium-grade PC procurement. The United States accounts for approximately 87.4% of North American revenues through the domestic EV gigafactory investment creating battery-grade demand and Huntsman’s Jeffsol PC commercial qualification sustaining domestic supply capability.

Canada contributes approximately 12.6% of North American revenues through its growing clean technology manufacturing sector, the pharmaceutical industry’s PC solvent adoption, and the coating industry’s VOC compliance investment creating structured PC specification procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Propylene Carbonate Market Insights

Europe is a commercially significant propylene carbonate market where EU Battery Regulation’s domestic supply chain requirements, REACH regulation’s VOC restrictions, and BASF’s domestic production capacity create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through BASF’s Ludwigshafen PC production, the automotive battery manufacturing sector’s electrolyte procurement, and the advanced coatings industry’s low-VOC solvent adoption.

France, Hungary, and Sweden are significant secondary markets where Stellantis, ACC, and Northvolt’s EV gigafactory battery manufacturing operations create domestic battery-grade PC procurement motivation whose EU Battery Regulation compliance creates supply chain localization investment.

Asia Pacific Propylene Carbonate Market Insights

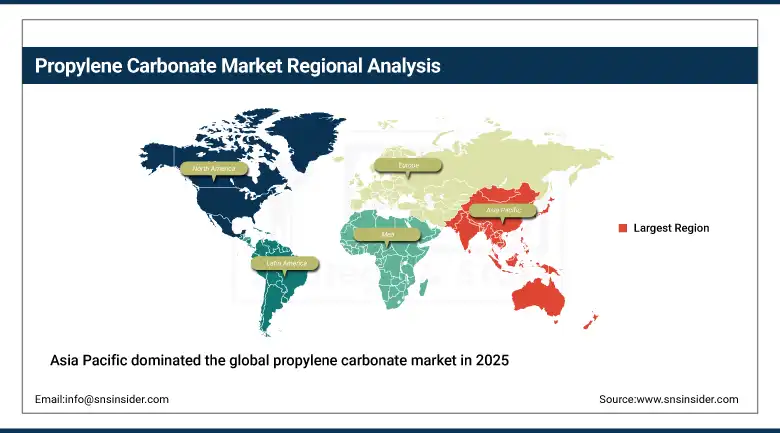

Asia Pacific dominated the global propylene carbonate market in 2025 with the highest revenue share. China accounts for approximately 54.6% of Asia Pacific revenues through its position as the world’s largest lithium-ion battery producer, the most commercially significant solvent application market, and the domestic PC production capacity base whose scale creates competitive pricing that sustains regional commercial dominance. The extraordinary expansion of Chinese EV battery gigafactories creates battery-grade PC procurement that represents the most commercially significant aggregate PC demand concentration globally.

South Korea and Japan represent technically sophisticated secondary markets where LG Energy Solution, Samsung SDI, Panasonic, and Murata’s battery manufacturing operations create consistent battery-grade PC procurement whose per-ton commercial value reflects the premium electrolyte specifications that advanced consumer and EV battery chemistry requires.

MEA & Latin America Propylene Carbonate Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through SABIC’s chemical manufacturing, the petrochemical complex’s PC production capability, and the industrial coating sector’s solvent application. Brazil leads Latin American revenues at approximately 44.2% through its industrial chemical sector, the growing automotive coating industry’s VOC compliance investment, and the pharmaceutical manufacturing sector’s PC solvent procurement.

UAE’s petrochemical manufacturing and South Africa’s industrial chemical sector create significant MEA secondary markets whose PC procurement reflects the progressive industrial development and VOC regulatory adoption across both jurisdictions.

Market Dynamics

Growth Drivers: EV lithium-ion battery demand and VOC regulation creating dual commercial demand vectors

Rising demand for lithium-ion batteries is the propylene carbonate market’s most commercially certain primary growth driver. The extraordinary pace of global EV market adoption, creating tens of millions of new EVs annually, generates proportional battery manufacturing capacity whose electrolyte component creates structured battery-grade PC procurement. Each new gigafactory commissioned creates long-duration supply relationships whose annual PC procurement scales with the facility’s cell production output. IEA’s projection that EV sales will represent 45% of new vehicle sales by 2030 creates a commercial demand trajectory whose PC procurement compound growth sustains above-market revenue expansion through the forecast period.

VOC regulation’s systematic restriction of conventional organic solvent use creates a complementary and non-correlated PC demand growth mechanism that sustains market growth independently of battery demand cycle variation. Each EPA VOC rule implementation, EU REACH solvent restriction, and emerging market environmental regulation creates new commercial motivation for PC specification in coating, cleaning, and synthesis applications.

Restraints: High-cost relative to conventional solvents and propylene oxide feedstock price volatility

Propylene carbonate’s production cost premium over conventional organic solvents creates adoption barriers in cost-sensitive industrial applications where the VOC regulatory compliance benefit must substantially exceed the cost premium to create positive ROI motivation for specification transition. Each industrial formulator whose conventional solvent alternative is not yet restricted by regulation faces limited commercial motivation to transition to PC’s higher-cost alternative absent the compliance requirement that creates mandatory adoption motivation.

Propylene oxide feedstock price volatility, driven by crude oil price cycles and supply chain dynamics, creates PC production cost uncertainty that limits manufacturer pricing predictability.

Opportunities: Bio-based PC from CO₂ utilization and pharmaceutical-grade premium applications

Bio-based propylene carbonate production from CO₂ utilization and bio-derived propylene oxide creates a sustainable production pathway whose green chemistry credentials command premium pricing in environmentally sensitive procurement markets. Each commercial demonstration of bio-based PC production at commercially viable economics creates market development opportunity whose sustainability differentiation sustains premium pricing relative to petrochemically derived alternatives. BASF’s and Mitsubishi Chemical’s CO₂ chemistry programmes create the technology precedents whose commercial scale-up defines the bio-based PC market’s development trajectory.

Pharmaceutical-grade propylene carbonate represents a premium commercial opportunity whose regulatory quality requirements and specialized application in transdermal drug delivery, pharmaceutical synthesis, and cosmetic carrier formulation create above-commodity pricing relationships.

Recent Developments:

-

2026: LyondellBasell advanced carbon utilization and sustainable feedstock projects aligned with demand for environmentally responsible carbonate-based chemicals.

-

2026: Kowa Company Ltd. enhanced supply capabilities for high-purity chemical intermediates serving pharmaceutical and specialty chemical markets.

-

2025: Huntsman Corporation increased investment in sustainable chemical technologies supporting low-emission solvent production and circular economy initiatives.

Propylene Carbonate Market key players are:

-

BASF SE

-

Huntsman Corporation

-

LyondellBasell Industries Holdings B.V.

-

Mitsubishi Chemical Corporation

-

Shandong Shida Shenghua Chemical Group

-

Dongying City Longxing Chemical Co., Ltd.

-

UBE Corporation

-

Tangshan Chenhong Industrial Co., Ltd.

-

Tokyo Chemical Industry Co., Ltd. (TCI)

-

Lonza Group AG

-

Asahi Kasei Corporation

-

Toagosei Co., Ltd.

-

Kowa Company Ltd.

-

Empower Materials Inc.

-

Shanghai Changsen Carbon-Tech Co., Ltd.

-

Oriental Union Chemical Corporation (OUCC)

-

Anhui Lixing Chemical Co., Ltd.

-

Jiangsu Ruixing Chemical Group

-

Tianjin Grand Chemical Industry Co., Ltd.

-

Shandong Lixing Chemical Co., Ltd.

Propylene Carbonate Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 445.65 Million |

| Market Size by 2035 | USD 802.86 Million |

| CAGR | CAGR of 6.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Battery Electrolyte/Lithium-Ion Batteries, Solvent, Paints & Coatings, Adhesives & Sealants, Personal Care & Cosmetics, Pharmaceutical, Others) • By Grade (Industrial Grade, Battery Grade/High Purity, Pharmaceutical Grade) • By End User (Electronics & Battery Manufacturing, Paints & Coatings Industry, Pharmaceutical & Personal Care, Chemical Processing, Automotive) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Huntsman Corporation, LyondellBasell Industries Holdings B.V., Mitsubishi Chemical Corporation, Shandong Shida Shenghua Chemical Group, Dongying City Longxing Chemical Co., Ltd., UBE Corporation, Tangshan Chenhong Industrial Co., Ltd., Tokyo Chemical Industry Co., Ltd. (TCI), Lonza Group AG, Asahi Kasei Corporation, Toagosei Co., Ltd., Kowa Company Ltd., Empower Materials Inc., Shanghai Changsen Carbon-Tech Co., Ltd., Oriental Union Chemical Corporation (OUCC), Anhui Lixing Chemical Co., Ltd., Jiangsu Ruixing Chemical Group, Tianjin Grand Chemical Industry Co., Ltd., Shandong Lixing Chemical Co., Ltd. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 6.05% from 2026 to 2035.

The market was valued at USD 445.65 Million in 2025.

Rising demand for lithium-ion batteries creating structured battery-grade PC procurement from EV gigafactory expansion.

The solvent segment is the fastest growing in the propylene carbonate market.

Asia Pacific dominated the propylene carbonate market in 2025.

Get in Touch