Aromatic Solvents Market Report Scope & Overview:

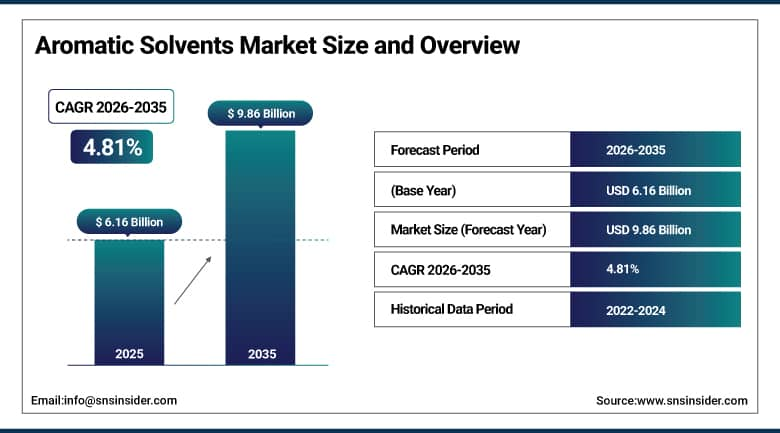

The Aromatic Solvents Market was valued at USD 6.16 Billion in 2025 and is expected to reach USD 9.86 Billion by 2035, growing at a CAGR of 4.81% from 2026 to 2035.

Aromatic solvents market growth is being bolstered by increased application in paints, coatings, adhesives, and industrial cleaners as a result of urbanization and low-VOC policies. Players in the market have been making use of circular technology and process optimization through data. Innovations in toluene and benzene compounds will help boost sustainable formulations in aromatic solvents. Efficient production methods and collaborations play a vital role in boosting market position, and usage of these products in adhesives, sealants, and inks is helping drive demand in the industrial economy at large. Increased refining capacity for aromatic solvents in petrochemical industries, especially in the Asia Pacific region, is adding value to supplies. Asia Pacific has more than 50% share of production capacity in the world for aromatic solvents, and VOC emissions policies are pushing towards development of low aromatic and high purity products.

In July 2024, the American Chemistry Council and the American Petroleum Institute formed the Naphthalene Workgroup to address benzene derivative regulations, reflecting the industry's coordinated response to tightening environmental oversight of aromatic hydrocarbon solvents in the United States.

Market Size and Forecast

- Market Size in 2026E: USD 6.46 Billion

- Market Size by 2035: USD 9.86 Billion

- CAGR: 4.81% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: Asia Pacific

To Get More Information On Aromatic Solvents Market - Request Free Sample Report

Aromatic Solvents Market Trends

- Rising demand in construction, paints, and coatings continues expanding industrial cleaning applications alongside stronger regulatory push for low-VOC formulations.

- Strategic R&D in benzene and toluene derivatives is supporting cleaner, more sustainable solvent formulations across industrial applications.

- Adoption of bio-based aromatic solvents is gaining traction as manufacturers seek alternatives to petroleum-derived feedstocks.

- Process optimization through digitalization and AI-driven analytics is improving production efficiency across major manufacturing facilities.

- Expanding use in automotive and infrastructure projects continues broadening the addressable market beyond traditional coatings applications.

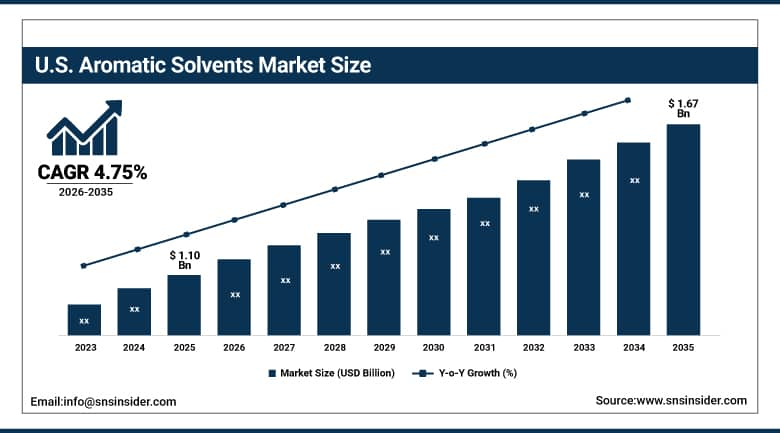

U.S. Aromatic Solvents Market Outlook

The U.S. aromatic solvents market was valued at approximately USD 1.10 Billion in 2026 and is expected to reach approximately USD 1.67 Billion by 2035, growing at a CAGR of approximately 4.75%.

The United States dominates in terms of growth as a result of wide usage in the automobile and construction industries with support from EPA rules for aromatic hydrocarbon solvents. As stated by American Coatings Association, the demand for architectural paints in the United States went up by 4.5% in 2022, thus increasing solvent usage. The new EPA rules have prompted innovation in low-VOC products in the solvent manufacturing industry in the country. The development of electric vehicles and constructions is still leading to growth in its usage.

ExxonMobil expanded high-purity toluene output at its Texas manufacturing facilities to meet growing demand from paints, coatings, and industrial cleaning customers, reinforcing the company's position as a leading domestic supplier of aromatic solvents to the U.S. market.

Aromatic Solvents Market Segment Analysis

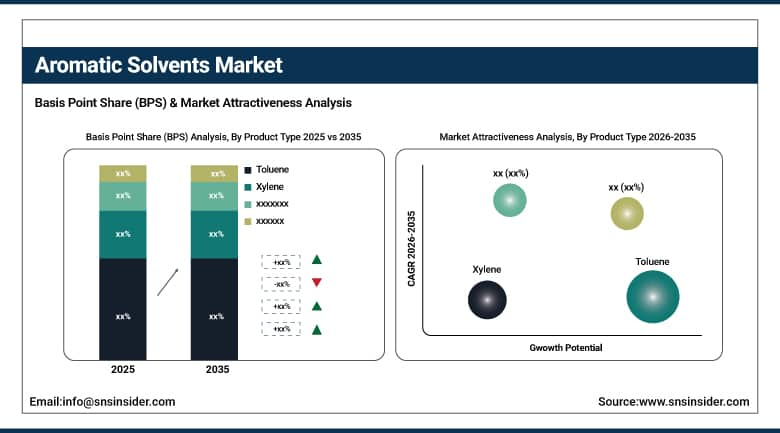

- By Product Type, toluene dominated the market in 2025, holding 45.4% share, while xylene is the fastest-growing product type at a CAGR of 5.23%.

- By Application, paints & coatings led the market in 2025, accounting for 37.9% of share, and is also the fastest-growing application, at a projected CAGR of 5.15%.

By Product Type, Toluene leads, Xylene grows fastest

Toluene dominated the aromatic solvents market in 2025, holding 45.4% share, driven by demand from paints, coatings, and industrial cleaning solutions, despite being classified as a VOC by the EPA. Its high-purity applications, highlighted by the National Institute of Standards and Technology, reinforce its role as a market driver, and toluene's versatility across such a broad range of formulations has kept it the market's clear leading product type.

Xylene is projected to grow at a 5.23% CAGR through the forecast period, fueled by electronics and automotive coating applications. Specialty-grade xylene blends meet low-VOC regulations and are increasingly used for cleaning resins and delicate equipment, and advances in benzene derivatives and aromatic hydrocarbon solvents across industries keep positioning xylene as an increasingly significant contributor to the expansion of the aromatic solvents market.

By Application, Paints & Coatings lead and grow fastest

The paint and coating application accounted for the largest market share of 37.9%, followed by the use of toluene and xylene in the paint and coating industry in 2025 due to occupational safety supervision to ensure the safety of the application on a large scale and also due to the increase in construction and the growth of urban infrastructure and automobiles.

It is also the fastest-growing application and is expected to grow at a CAGR of 5.15% during the forecast period. As per the NIST, the specialty solvents used for automotive paint and nanocoating applications have seen an increased demand since 2022, and the increased investments in customizing the solvent system have increased the market growth with paints and coating being the single most important driver of aromatic solvents market growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

33.75% |

|

North America |

United States |

79.60% |

|

Europe |

Germany |

24.90% |

|

Middle East & Africa |

UAE |

26.80% |

|

Latin America |

Brazil |

35.65% |

Asia Pacific Aromatic Solvents Market Insights

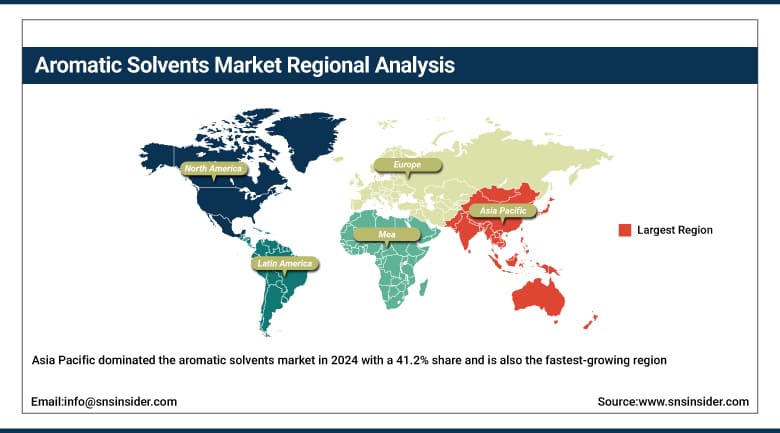

Asia Pacific dominated the aromatic solvents market in 2024 with a 41.2% share and is also the fastest-growing region, with the highest CAGR of 5.09%. China's and India's industrial growth is the cause of the increase, and regional development is being accelerated by government support for the toluene market and benzene derivatives across the region's largest manufacturing economies.

China leads the region, accounting for roughly 33.75% of regional revenue, supported by the country's massive petrochemical refining capacity and rapid industrial expansion. India and Japan contribute meaningful additional demand, and that broadening base of countries investing in domestic solvent production capacity keeps Asia Pacific both the largest and fastest-growing region tracked in this report.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Aromatic Solvents Market Insights

North America is a major source of contribution in terms of revenues generated in global aromatic solvents industry, owing to growth in the country's automotive and construction industries, as well as higher disposable incomes that drive up demands for quality coatings and finishes. North America enjoys petrochemical facilities and an established presence of leading aromatic solvent producers in the region.

United States is the market leader in North America with increasing market size that generates close to 79.60% of revenues in the region, due to widespread applications in the automotive and construction sectors in the presence of EPA regulations concerning aromatic hydrocarbon solvents. Contribution of Canada to the region comes through its low-VOC solvents that are developed due to eco-grants.

Europe Aromatic Solvents Market Insights

Europe holds a meaningful share of the global aromatic solvents market, supported by developed industries and increasing applications in pharmaceuticals and oil and gas sectors across the region's major economies. Strict environmental regulation around VOC emissions has pushed European manufacturers toward increasingly sophisticated low-aromatic and high-purity solvent formulations.

Germany leads regional demand at roughly 24.90% of European revenue, supported by its substantial industrial and automotive manufacturing base. The UK and France contribute substantial additional demand, and continued European regulatory tightening around VOC emissions should keep regional demand for compliant, high-purity aromatic solvents climbing steadily through the forecast period.

Middle East & Africa & Latin America Aromatic Solvents Market Insights

Middle East & Africa and Latin America are both showing steady growth in aromatic solvents adoption, driven by expanding petrochemical production capacity, growing construction and automotive manufacturing investment, and rising industrial activity across both regions. As these markets continue building out domestic refining and chemical manufacturing capability, aromatic solvents are proving essential to a genuinely broad range of industrial applications.

The UAE leads Middle East & Africa demand of regional revenue, supported by the country's substantial petrochemical refining infrastructure and growing industrial diversification. Saudi Arabia and South Africa contribute further regional demand through their own petrochemical production programs. In Latin America, Brazil accounts for approximately 35.65% of regional revenue, with growing construction and automotive manufacturing continuing to anchor regional demand for aromatic solvents.

Market Dynamics

Growth Drivers: Rising demand from paints, coatings, and industrial cleaning applications

The market for aromatic solvents is growing owing to increasing consumption in paints, coatings, adhesives, and industrial cleaning agents, which is a result of urbanization and regulations regarding low-VOC paints. The U.S. architectural paints consumption grew by 4.5% in 2022, thereby supporting the demand for aromatic solvents, and increased activities in the industrial sector in Asia Pacific, North America, and Europe are further cementing this trend in all major consuming regions.

Increased capacity additions in the petrochemicals refining industry, especially in Asia Pacific, is increasing the supply side, given that Asia Pacific has in excess of 50% of global aromatic solvents' manufacturing capacity. Increased electric vehicle production and recovering construction activities in Asia Pacific and Europe are contributing to faster growth, and chemical firms globally are increasing their investments in greener solutions as per environmental standards.

Restraints: Stricter safety regulations and crude oil price volatility

Strict regulation regarding the safety of benzene, toluene, styrene, ethylbenzene, and xylenes continues to pose constraints on fast market growth, as manufacturers have to incur heavy expenses to re-formulate their products and test the same for adherence to the increasing demands of the regulatory landscape within major market segments. The compliance of the changing environmental requirements, along with the costs associated with the transition of the manufacturing process towards greener production, creates genuine resistance to market growth.

The fluctuations in the price of crude oil affecting raw material costs present another constraint due to the fact that aromatic solvents are basically made from petroleum products and their costs can vary widely depending upon the condition of the energy market.

Opportunities: Bio-based solvent development and specialty-grade formulations

Adoption of bio-based aromatic solvents represents a genuinely significant opportunity for manufacturers looking to differentiate from conventional, petroleum-derived formulations as customers increasingly prioritize sustainability credentials. As green chemistry research continues maturing, vendors that can deliver genuine performance parity with bio-based feedstocks stand to capture meaningful share of environmentally conscious buyers across paints, coatings, and industrial cleaning applications.

Expanding specialty-grade, low-VOC solvent formulations offer a second substantial opportunity, particularly as over 30% of new product launches in the category are already focused on improved environmental compliance. As regulatory pressure keeps intensifying across every major market, vendors with proven, compliant high-purity formulations stand to capture disproportionate share as buyers consolidate around suppliers capable of meeting increasingly stringent environmental standards.

Recent Developments:

- 2025: ExxonMobil Product Solutions expanded its Solvesso aromatic solvents portfolio with ultra-low cumene (ULC) and ultra-low naphthalene grades to help coatings, agrochemical, and industrial formulators comply with evolving chemical labeling and safety regulations while maintaining high solvency performance. The development reflects the industry's increasing focus on regulatory compliance, worker safety, and high-performance aromatic solvent formulations.

- 2024: CEPSA Química launched NextLab Low Carbon, a lower-carbon linear alkylbenzene (LAB) produced at its Puente Mayorga, Spain facility using renewable heat. The product offers a 19% lower cradle-to-gate carbon footprint than conventional LAB while maintaining identical performance, supporting detergent and chemical manufacturers in reducing emissions and advancing sustainable aromatic solvent production.

Aromatic Solvents Companies are:

- Recochem Inc.

- Cepsa Química S.A.

- SK Geo Centric Co., Ltd.

- Haltermann Carless GmbH

- Panama Petrochem Ltd.

- SolvChem, Inc.

- Huntsman Corporation

- DHC Solvent Chemie GmbH

- Nova Molecular Technologies, Inc.

- Pon Pure Chemicals Group

- RB Products, Inc.

- GJ Chemical Co., Inc.

- ExxonMobil Corporation

- BASF SE

- LyondellBasell Industries Holdings B.V.

- Eastman Chemical Company

- Celanese Corporation

- China Petroleum & Chemical Corporation (Sinopec)

- China National Petroleum Corporation

- TotalEnergies SE

Aromatic Solvents Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.16 Billion |

| Market Size by 2035 | USD 9.86 Billion |

| CAGR | CAGR of 4.81% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Toluene, Xylene, Benzene, Ethylbenzene, Others), • By Application (Paints & Coatings, Adhesives & Sealants, Printing Inks, Industrial Cleaning, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Recochem Inc., Cepsa Química S.A., SK Geo Centric Co., Ltd., Haltermann Carless GmbH, Panama Petrochem Ltd., SolvChem, Inc., Huntsman Corporation, DHC Solvent Chemie GmbH, Nova Molecular Technologies, Inc., Pon Pure Chemicals Group, RB Products, Inc., GJ Chemical Co., Inc., ExxonMobil Corporation, BASF SE, LyondellBasell Industries Holdings B.V., Eastman Chemical Company, Celanese Corporation, China Petroleum & Chemical Corporation (Sinopec), China National Petroleum Corporation, and TotalEnergies SE |

Frequently Asked Questions

The Aromatic Solvents Market is expected to grow at a CAGR of 4.81% from 2026 to 2035.

The Aromatic Solvents Market was valued at USD 6.16 Billion in 2025.

The Toluene segment dominated the Aromatic Solvents Market with a 45.4% share by product type in 2025.

The major growth factor is rising demand in paints, coatings, adhesives, and industrial cleaning products, driven by urbanization and stricter low-VOC regulations.

Asia Pacific dominated the Aromatic Solvents Market in 2025 with a 41.2% share of total global market revenue.

Get in Touch