Urology Devices Market Report Scope & Overview:

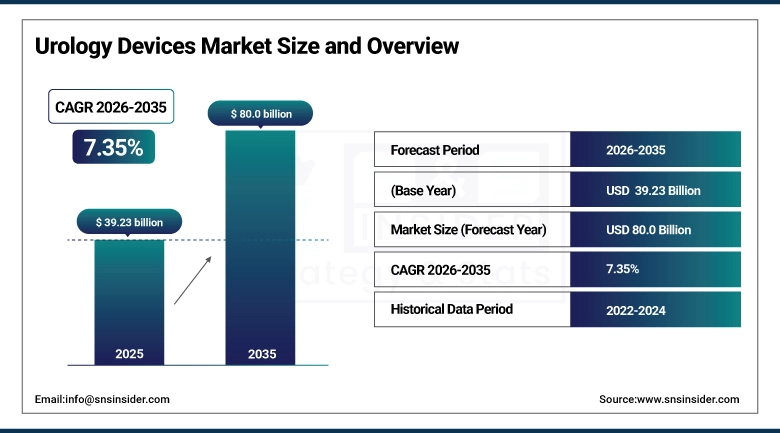

The Urology Devices Market was valued at USD 39.23 billion in 2025 and is expected to reach USD 80.0 billion by 2035, growing at a CAGR of 7.35% from 2026-2035.

The urinary system and the male reproductive system together encompass an extraordinary range of conditions whose clinical management requires equally diverse device technologies. Kidney failure requiring dialysis, kidney stones requiring lithotripsy, bladder cancer requiring cystoscopic resection, urinary incontinence requiring slings or neuromodulators, enlarged prostate requiring laser vaporization or robotic enucleation, erectile dysfunction requiring penile implants each represents a distinct clinical problem with a distinct device solution that the urology device industry has developed over decades of clinical innovation. What unites them commercially is their demographic driver: the aging of global populations creates disproportionate prevalence growth in each of these conditions simultaneously, as the processes of biological aging consistently manifest in kidneys that gradually lose function, prostates that gradually enlarge, bladders whose control mechanisms gradually weaken, and pelvic floors whose structural integrity gradually diminishes. The urology device market's 7.35% CAGR reflects this demographic compounding not one condition growing but an entire family of age-correlated conditions growing in the same direction and at the same time.

The CDC documents that approximately 37 million Americans 15% of the adult population have chronic kidney disease, with the majority unaware of their diagnosis, representing a massive unmet need for diagnostic and treatment devices as CKD awareness and screening improve. The American Urological Association's 2023 epidemiological summary estimates that 50% of men over 60 have clinically significant benign prostatic hyperplasia requiring some form of intervention a prevalence rate that, when applied to aging global demographics, generates tens of millions of BPH treatment device procedures annually.

Urology Devices Market Size and Forecast

-

Market Size in 2025: USD 39.23 Billion

-

Market Size by 2035: USD 80.0 Billion

-

CAGR: 7.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Urology Devices Market - Request Free Sample Report

Urology Devices Market Trends

-

Robotic-assisted laparoscopic urological surgery including robotic prostatectomy, robotic nephrectomy, and robotic cystectomy using the da Vinci Surgical System and competing platforms — is driving surgical precision improvements and faster patient recovery across the most complex urological oncology procedures.

-

Single-use digital flexible ureteroscopes with chip-on-tip imaging are replacing reusable ureteroscopes in many kidney stone treatment settings, eliminating reprocessing costs and infection transmission risk while providing equivalent optical quality.

-

Artificial urinary sphincters and advanced male sling systems are expanding surgical treatment access for post-prostatectomy incontinence, a prevalent and underdiagnosed condition affecting up to 30% of radical prostatectomy patients.

-

MRI-targeted prostate biopsy systems that fuse pre-procedure MRI with real-time ultrasound guidance are improving prostate cancer detection accuracy while reducing the number of unnecessary biopsies compared to random systematic biopsy approaches.

-

Wearable bladder activity monitors and connected catheters providing continuous urodynamic data are enabling outpatient urological monitoring that generates clinical data quality previously achievable only during formal urodynamics laboratory studies.

-

Focused shockwave lithotripsy technology advances including miniaturized portable lithotripter systems for ambulatory surgical center deployment are expanding kidney stone treatment access beyond major hospital settings.

-

AI-enhanced cystoscopy imaging using deep learning polyp and tumor detection algorithms is improving bladder cancer surveillance cystoscopy quality, reducing the flat lesion miss rates that conventional white-light cystoscopy historically produces.

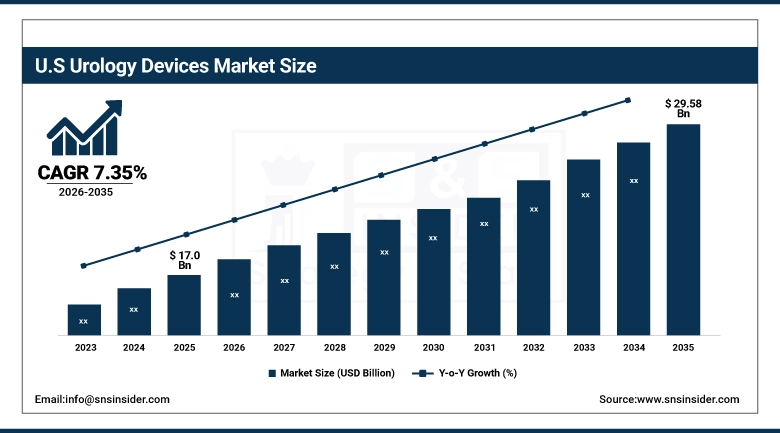

U.S. Urology Devices Market was valued at USD 17.0 billion in 2023 and is expected to reach USD 29.58 billion by 2032, growing at a CAGR of 7.35% from 2026-2035.

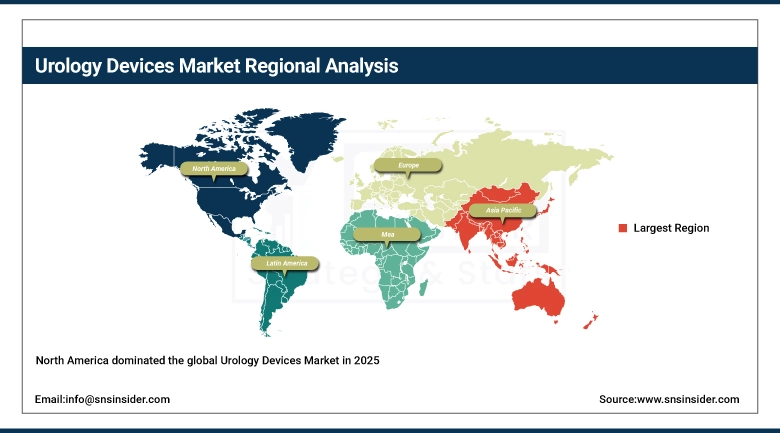

North America dominated the global Urology Devices Market, with the United States representing the world's largest national urology device market. The U.S. market's scale reflects the convergence of high urological disease prevalence driven by an aging population, high obesity rates that accelerate kidney disease, high diabetes prevalence, and high rates of prostate cancer screening with a healthcare system that provides extensive access to advanced urological interventions including robotic surgery, laser stone treatment, and neuromodulation. U.S. hospitals performed over 4.5 million urological procedures in 2023, the highest single-country procedure volume globally, sustaining device procurement across all urology device categories. The U.S. market's advanced surgical technology adoption culture — reflected in the U.S. accounting for over 60% of installed da Vinci robotic surgical systems globally — drives premium urology device revenue that markets with less access to expensive surgical technology cannot generate.

Intuitive Surgical's 2024 annual report documents that robotic prostatectomy now represents over 85% of all radical prostatectomies performed in the U.S. the highest robotic penetration rate of any major surgical procedure creating a generation of urologists whose primary surgical training is robotic rather than open or laparoscopic. The American Urological Association's 2024 practice survey shows that 78% of board-certified urologists in community practice now have access to a robotic surgical system, compared to 45% in 2018.

Urology Devices Market Segment Analysis

-

By Product, Instruments dominated the market in 2025; Consumables & Accessories both growing substantially.

-

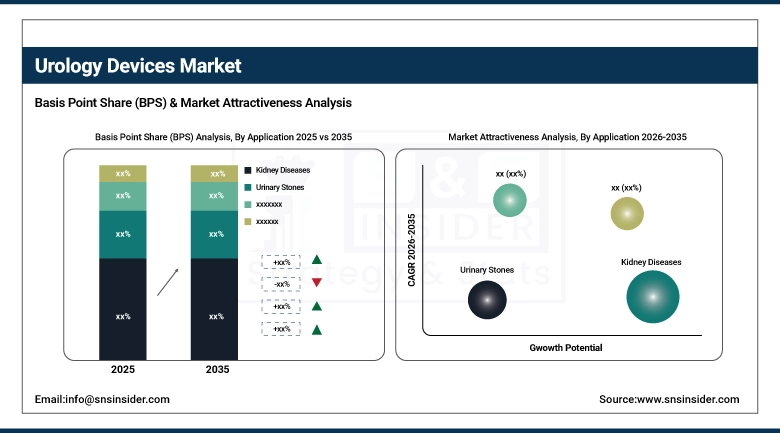

By Application, Kidney Diseases dominated with 37% share in 2025; Prostate conditions and Urological Cancer both growing substantially.

-

By End-User, Hospitals, ASCs & Clinics dominated with 45% share in 2025; Specialty Urology Centers fastest growing; Home Care Settings growing steadily.

By Application: Kidney Diseases dominates, Urological Cancer & BPH growing

Kidney Diseases held the dominant application position with approximately 37% of the Urology Devices Market in 2023, reflecting the enormous global burden of chronic kidney disease and its treatment requirements across the full continuum from early-stage CKD management through end-stage renal disease requiring dialysis or transplantation. The dialysis equipment market encompassing hemodialysis machines, dialyzers, peritoneal dialysis systems, and water treatment systems represents the single largest device category within urology by revenue, driven by the 3.5 million patients globally requiring dialysis therapy multiple times weekly for life-sustaining kidney replacement. Dialysis's non-discretionary, recurring utilization pattern where every ESRD patient requires treatment three times per week indefinitely creates the most reliable and predictable revenue stream in urology devices, explaining the sub-market's commercial scale.

Urinary Stones (urolithiasis) represent a growing application segment as kidney stone prevalence increases with obesity, dietary patterns, climate-related dehydration, and the aging of populations in developed markets. The American Urological Association's 2024 epidemiology data documents that approximately 1 in 10 Americans will develop a kidney stone during their lifetime, with recurrence rates above 50% creating recurring treatment needs. Ureteroscopy with laser lithotripsy has become the dominant treatment approach for most kidney stones, creating growing demand for single-use digital flexible ureteroscopes whose optical quality, single-use infection control profile, and elimination of reprocessing downtime are making them the preferred technology at high-volume stone treatment centers. Benign Prostatic Hyperplasia represents a growing application where the technology transition from traditional TURP toward laser-based surgical treatments and minimally invasive office-based procedures is creating device market value growth above the underlying BPH incidence growth rate.

The Global Burden of Disease study documents that urinary tract diseases including CKD caused 3.5 million deaths globally in 2022, making urological disease the 12th leading cause of death worldwide — a burden that is growing proportionally with global demographic aging and the rising prevalence of metabolic risk factors including hypertension and diabetes that accelerate kidney disease progression.

By End-User: Hospitals/ASCs/Clinics dominate, Specialty Urology Centres growing fastest

Hospitals, Ambulatory Surgical Centers, and Clinics collectively held approximately 45% of the Urology Devices Market in 2023, representing the broadest institutional cross-section of urological care delivery across the disease severity spectrum from primary care urology clinic visits for UTI diagnosis through major academic medical center robotic cancer surgery. The hospital segment's dominance reflects the complexity and capital intensity of major urological procedures: robotic prostatectomy, robotic cystectomy, percutaneous nephrolithotomy, and open renal surgery each require the operating room infrastructure, anesthesia capability, intensive care support, and post-operative care capacity that only hospitals can provide at adequate quality standards.

Specialty Urology Centers are growing at the fastest end-user CAGR, representing the trend toward dedicated urology practices that provide focused urological care across office, procedure room, and ambulatory surgery settings under one clinical organization. Specialty urology centers offer same-day procedure capability for cystoscopy, urodynamics, and in-office BPH procedures, significantly shorter appointment wait times than hospital urology departments, and a clinical environment optimized for urological patient flow and device utilization efficiency. Home Care Settings represent a growing segment driven by the aging population's preference for managing chronic conditions including urinary incontinence, intermittent self-catheterization, and peritoneal dialysis in home environments, creating growing demand for home-compatible urological device products.

Urology Devices Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

North America Urology Devices Market Insights

North America dominated the global Urology Devices Market in 2025, led by the United States where high urological procedure volumes, premium technology adoption, and extensive dialysis infrastructure create the world's most commercially developed urology device market. The U.S. dialysis sector dominated by DaVita and Fresenius Medical Care's combined 4,200+ outpatient dialysis centers serving approximately 500,000 ESRD patients creates the most structurally defined urology device procurement market of any application segment globally. U.S. government reimbursement for dialysis through Medicare's ESRD benefit which covers virtually all ESRD patients regardless of age creates a uniquely stable revenue stream that sustains dialysis equipment procurement independent of broader healthcare budget cycles.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Urology Devices Market Insights

Asia Pacific is the fastest-growing regional Urology Devices Market, driven by China's enormous and growing CKD and kidney stone burden, Japan's sophisticated urology technology adoption culture, India's expanding private healthcare sector, and South Korea's advanced medical device infrastructure. China's growing obesity and diabetes epidemic is creating proportional CKD prevalence growth that generates dialysis infrastructure demand at a scale that no other regional market approaches the Chinese Society of Nephrology estimates that China has over 150 million CKD patients, with a fraction progressing to ESRD requiring dialysis annually. Asia Pacific's private healthcare sector growth is also driving robot-assisted urology adoption: APAC da Vinci system installations have grown at 25% annually since 2020, with Japan, South Korea, and Australia leading adoption and China's public hospital investment program rapidly expanding the installed base.

Europe Urology Devices Market Insights

Europe's Urology Devices Market is driven by well-developed national healthcare systems that provide comprehensive urological care access, sophisticated clinical communities driving technology adoption in robotic surgery and laser lithotripsy, and the presence of major urology device manufacturers including Karl Storz, Richard Wolf, and Dornier MedTech within the European manufacturing base. Germany's healthcare system with universal coverage and no significant access barriers to specialist urological care sustains high urological procedure volumes across both hospital and outpatient urology practice settings. The European Association of Urology's clinical practice guidelines are influential globally in defining standard of care for urological conditions, and their progressive recommendations for minimally invasive treatment approaches drive device adoption across European markets.

Middle East & Africa and Latin America Insights

The Middle East's Urology Devices Market is growing with the Gulf states' healthcare infrastructure investment, where large hospital complexes in Riyadh, Dubai, and Abu Dhabi maintain comprehensive urology departments including robotic surgical capability and dedicated stone treatment centers. Saudi Arabia's Vision 2030 healthcare expansion is increasing the number of specialist urologists and the surgical capacity that serves the Kingdom's growing population with improving access to advanced urological care. Latin America's urology market concentrates in Brazil, Mexico, and Colombia, where private healthcare sectors serve patients with financial means to access advanced urology devices while public health system programs provide more limited urological care using cost-effective device options.

Urology Devices Market Growth Drivers:

Aging population and rising urological disease burden driving sustained urology devices market growth globally

The Urology Devices Market's 7.35% CAGR is driven by demographic certainty that no healthcare policy can reverse: global populations are aging, and urological disease prevalence correlates strongly with age. CKD, BPH, urinary incontinence, urolithiasis, and urological cancers collectively affect the majority of men above 60 and a significant proportion of women above 50 a patient population that is growing in absolute numbers at 3% annually as the global demographic pyramid's age distribution continues its decades-long upward shift. Simultaneously, minimally invasive technology innovation is expanding the population of patients who can benefit from surgical treatment: procedures that previously required open surgery with significant recovery burden are now performable laparoscopically, robotically, or endoscopically with outpatient recovery times, making the benefit-risk calculation favorable for older patients who would previously have been declined surgical treatment.

Urology Devices Market Restraints:

High procedure costs and reimbursement limitations restricting urology devices market access in cost-sensitive healthcare systems globally

The urology device market's commercial ceiling is constrained by reimbursement policy in ways that differ by application: dialysis equipment reimbursement in the U.S. operates under a bundled payment system where dialysis providers receive fixed per-session payments that create cost pressure on equipment procurement; robotic surgical systems face hospital capital budget scrutiny as their purchase price (USD 1.5-3 million per system) and maintenance costs (USD 150,000+ annually) require multi-year payback justification; and office-based urology procedures whose clinical evidence is newer face reimbursement coverage uncertainty that slows adoption below the clinical validation pace.

Urology Devices Market Opportunities:

Artificial intelligence imaging and home dialysis expansion creating significant urology devices market growth opportunities globally

Home dialysis — both peritoneal dialysis and home hemodialysis represents a significant growth opportunity within the urology device market as patient preference for home-based treatment, demonstrated clinical equivalence to in-center dialysis, and healthcare system cost advantages of home treatment over facility-based dialysis create aligned clinical and economic incentives for home dialysis program expansion. The Centers for Medicare & Medicaid Services' Kidney Care Choices model which creates financial incentives for dialysis providers to increase home dialysis utilization is accelerating home dialysis adoption in the U.S. market, with home-compatible dialysis equipment from NxStage (Fresenius), Baxter, and Outset Medical growing as a product category within the dialysis equipment market.

Recent Developments:

-

2026: Intuitive Surgical received FDA clearance for da Vinci 5, its fifth-generation robotic surgical system with improved haptic feedback capability through force sensing instrumentation, 10,000-frame-per-second 3D imaging, and integrated AI surgical guidance that provides real-time tissue identification during urological oncology procedures — with initial commercial deployment focused on radical prostatectomy and partial nephrectomy at leading academic urology programs across the United States and Europe.

-

2025: Boston Scientific launched its WaveOne Dual-mode flexible ureteroscope — a single-use digital ureteroscope with switchable standard and narrow-band imaging modes — enabling both standard white-light stone visualization and tissue characterization imaging in a single device, addressing the previous requirement to switch between different scope types during complex ureteropelvic junction cases requiring both stone treatment and transitional cell carcinoma surveillance.

-

2025: Fresenius Medical Care launched its 5008X CorDiax cycler home hemodialysis system with integrated cloud connectivity for remote monitoring by nephrology care teams, reducing the home HD patient management burden that has historically limited nephrologist enthusiasm for expanding home dialysis programs reporting 23% improvement in fluid management adherence and 18% reduction in unplanned hospitalizations in 300-patient clinical validation.

Urology Devices Market Key Players

Some of the Urology Devices Market Companies

-

Intuitive Surgical Inc.

-

Boston Scientific Corporation

-

Medtronic plc

-

Karl Storz SE & Co. KG

-

Olympus Corporation

-

Richard Wolf GmbH

-

Fresenius Medical Care AG & Co. KGaA

-

Baxter International Inc.

-

NxStage Medical Inc. (Fresenius)

-

Becton Dickinson & Company

-

Johnson & Johnson MedTech

-

Teleflex Incorporated

-

Coloplast A/S

-

C.R. Bard Inc. (BD)

-

Cook Medical LLC

-

American Medical Systems (Boston Scientific)

-

Dornier MedTech GmbH

-

Laborie Medical Technologies

-

Envision Scientific Pvt. Ltd.

-

Cogentix Medical Inc.

Urology Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.23 Billion |

| Market Size by 2035 | USD 80.0 Billion |

| CAGR | CAGR of 7.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Instruments, Consumables & Accessories) • By Application (Kidney Diseases, Benign Prostatic Hyperplasia, Urinary Stones, Urinary Incontinence, Urological Cancer, Erectile Dysfunction, Pelvic Organ Prolapse, Other Applications) • By End User (Hospitals, Ascs, And Clinics, Dialysis Centers, Home Care Settings) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intuitive Surgical Inc., Boston Scientific Corporation, Medtronic plc, Karl Storz SE & Co. KG, Olympus Corporation, Richard Wolf GmbH, Fresenius Medical Care AG & Co. KGaA, Baxter International Inc., NxStage Medical Inc. (Fresenius), Becton Dickinson & Company, Johnson & Johnson MedTech, Teleflex Incorporated, Coloplast A/S, C.R. Bard Inc. (BD), Cook Medical LLC, American Medical Systems (Boston Scientific), Dornier MedTech GmbH, Laborie Medical Technologies, Envision Scientific Pvt. Ltd., Cogentix Medical Inc. |

Frequently Asked Questions

Ans: North America dominated; Asia Pacific is the fastest growing regional market.

Ans: Hospitals, ASCs & Clinics dominated with approximately 45% share; Specialty Urology Centers fastest growing.

Ans: Kidney Diseases dominated with approximately 37% share in 2025.

Ans: The Urology Devices Market was valued at USD 39.23 billion in 2025.

Ans: The Urology Devices Market is expected to grow at a CAGR of 7.35% from 2026 to 2035.

Get in Touch