Veterinary Artificial Insemination Market Report Scope & Overview:

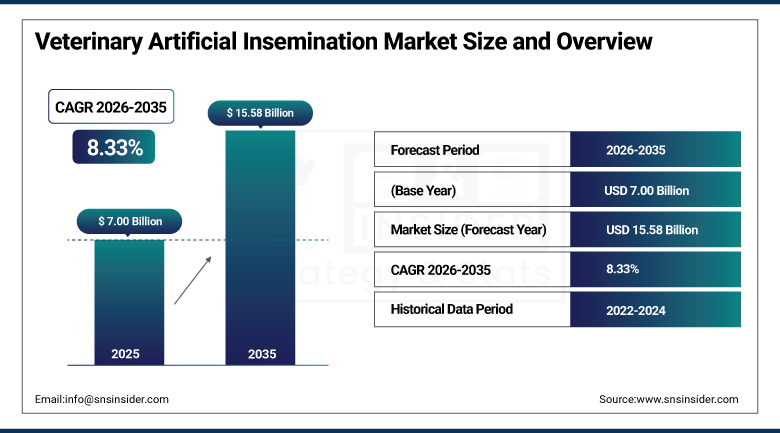

The Veterinary Artificial Insemination Market was valued at USD 7.00 Billion in 2025 and is expected to reach USD 15.58 Billion by 2035, growing at a CAGR of 8.33% from 2026 to 2035.

The Market for Artificial Insemination in Veterinary is steadily growing, considering the need for genetically enhanced and disease resistant breeds among livestock farmers in the world, who have a global herd of cattle exceeding 987 million and a global herd of swine surpassing 1.5 billion to address the increasing demand for meat, milk, and dairy products. Livestock farmers prefer more advanced technologies for artificial insemination that increase fertility rates and help reduce the possibility of disease transmission along with quick genetic improvement in cattle, swine, and equine populations. Artificial insemination programs utilizing extended boar semen are being employed by swine breeders to bring in superior genetics into commercial herds and minimize the risks posed by moving live boars from farm to farm.

The merger of URUS Group and Leachman Cattle was successfully accomplished in 2025 with an incorporation of the cutting edge genetics technology and large database from Leachman into URUS Group in order to enhance the company's performance in the international market for cattle genetics.

Market Size and Forecast

-

Market Size in 2026E: USD 7.58 Billion

-

Market Size by 2035: USD 15.58 Billion

-

CAGR: 8.33% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Veterinary Artificial Insemination Market- Request Free Sample Report

Veterinary Artificial Insemination Market Trends

-

Sexed semen adoption continues expanding as producers seek greater control over offspring gender for both dairy and beef operations.

-

Swine breeders are increasingly using extended boar semen to minimize biosecurity risks associated with live boar movement.

-

Government-backed artificial insemination programs continue expanding free or subsidized breeding services across emerging livestock economies.

-

Precision breeding tools and data-driven reproductive management are becoming standard across commercial dairy and beef operations.

-

Advancements in cryopreservation technology continue improving semen viability across longer storage and transport distances.

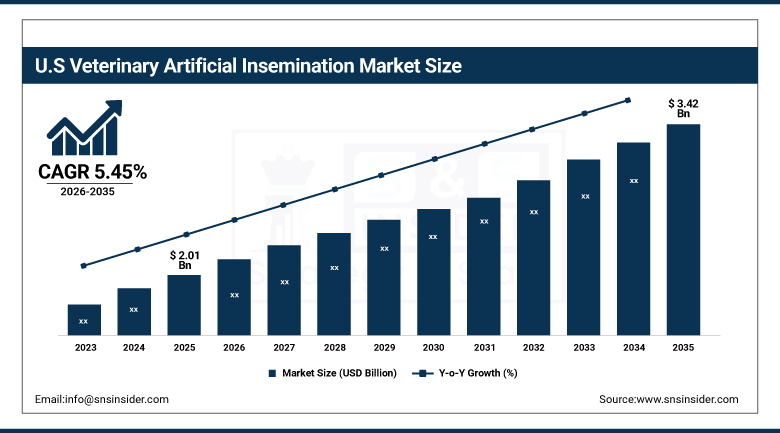

The United States Veterinary Artificial Insemination Market Outlook

The United States veterinary artificial insemination market was valued at USD 2.01 Billion in 2025 and is expected to reach USD 3.42 Billion by 2035, growing at a CAGR of 5.45% from 2026 to 2035.

The USA occupied a leading position among the states of North America regarding the demand for veterinary artificial insemination. This was attributed to the increase in the demand for dairy cattle that produced higher yields because of artificial insemination, especially the Holstein dairy cattle known for producing large quantities of milk, as well as due to advances in cryopreservation. In the United States alone, more than sixty-one percent of dairy cattle are artificially inseminated, thus enabling the selection of good genetics for milk production and disease resistance, among others.

In March 2025, STgenetics unveiled the next generation of their semen sorting technology under the GenX Plus project, which not only enhanced sorting capabilities but also increased the conception rates along with the production of female calves for dairy farmers in America.

Veterinary Artificial Insemination Market Segment Analysis

-

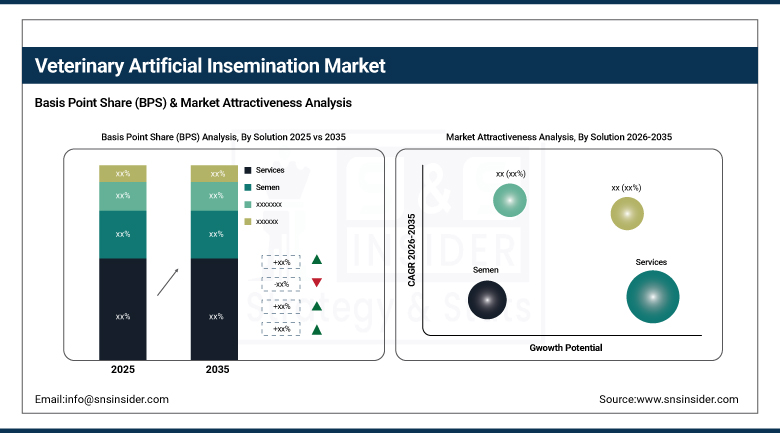

By Solution, the services segment held approximately 39.06% share of veterinary artificial insemination market in 2025, while the semen segment is the fastest growing, with a CAGR of approximately 8.40% during the forecast period.

-

By Animal Type, the bovine segment held approximately 58.40% share of veterinary artificial insemination market in 2025, while the porcine segment is the fastest growing, with a CAGR of approximately 8.10% during the forecast period.

-

By Technology Type, the conventional semen segment held the larger share of approximately 68.30% in veterinary artificial insemination market in 2025, while the sexed semen segment is the fastest growing, with a CAGR of approximately 9.60% during the forecast period.

-

By Distribution Channel, the private segment held approximately 56.49% share of veterinary artificial insemination market in 2025, while the public segment is the fastest growing, with a CAGR of approximately 7.20% during the forecast period.

By Solution, services led the market, semen grew fastest

Segment Services dominated the category solution in 2025, accounting for about 39.06% of the overall revenue due to the complicated nature of artificial insemination and rising need for professional knowledge in animal reproduction. That reliance on trained technicians for accurate insemination timing and technique continues keeping services firmly at the top of the broader solution segmentation across nearly every major livestock-producing region.

The semen segment is projected to grow at the fastest CAGR during the forecast period, driven by rising adoption of sexed semen technology that lets producers select offspring gender for both dairy and beef operations. Advancements in semen processing, including genomic selection techniques, continue enabling producers to make more informed breeding decisions, pushing this solution category's growth rate ahead of the broader solution segmentation.

By Animal Type, bovine led the market, porcine grew fastest

The bovine segment dominated the animal type category in 2025, holding approximately 58.40% of total revenue, owing to the widespread and long-established adoption of artificial insemination practices within the global cattle industry. Extensive semen distribution networks and strong dairy and beef genetic programs continue keeping bovine firmly at the top of the broader animal type segmentation across nearly every major livestock-producing economy.

The porcine segment is projected to grow at the fastest CAGR during the forecast period, as swine breeders increasingly implement artificial insemination programs using extended boar semen to introduce superior genetics into commercial herds. Rising demand for improved litter size, growth rate, and carcass quality, combined with reduced biosecurity risk relative to live boar movement, continues pushing this animal type category's growth rate ahead of the broader animal type segmentation.

By Technology Type, conventional semen led the market, sexed semen grew fastest

The conventional semen segment held the larger technology type share in 2025, anchored by its lower cost and established compatibility with existing breeding infrastructure across the majority of commercial livestock operations worldwide. That cost and infrastructure advantage keeps conventional semen technology the default choice across price-sensitive and smallholder farming operations in particular.

The sexed semen segment is projected to grow at the fastest CAGR during the forecast period, as producers increasingly value the ability to select offspring gender for optimizing dairy herd replacement rates or beef production economics. India alone produced over ten million doses of sex-sorted semen in a single recent year, reflecting the rapid global expansion of this technology category ahead of the broader technology type segmentation.

By Distribution Channel, private led the market, public grew fastest

The private segment dominated the distribution channel category in 2025, holding approximately 56.49% of total revenue, supported by an extensive network of private veterinary clinics, breeding centers, and animal husbandry service providers offering readily accessible artificial insemination services and products. That established private-sector distribution depth continues keeping this channel firmly at the top of the broader distribution channel segmentation across most developed livestock markets.

The public segment is projected to grow at the fastest CAGR during the forecast period, driven by government initiatives and cooperative programs supporting livestock improvement, particularly across emerging economies. India's Rashtriya Gokul Mission and National Artificial Insemination Programme, which provides free artificial insemination services across more than six hundred districts, continues pushing this distribution channel category's growth rate ahead of the broader distribution channel segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.00% |

|

Asia Pacific |

India |

34.60% |

|

Europe |

Germany |

26.80% |

|

Middle East & Africa |

South Africa |

28.10% |

|

Latin America |

Brazil |

39.40% |

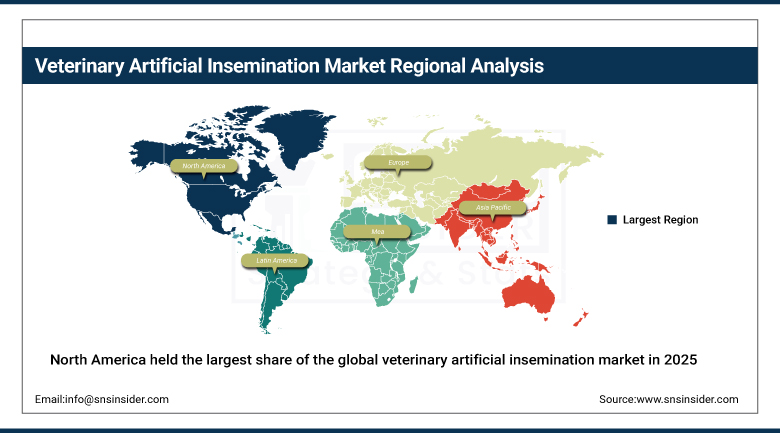

North America Veterinary Artificial Insemination Market Insights

North America held the largest share of the global veterinary artificial insemination market in 2025, at approximately 31.65%, supported by extensive bovine genetic programs, widespread semen distribution networks, and strong adoption of advanced sex-sorted semen technologies across large-scale dairy operations. That combination of genetic program depth and distribution infrastructure continued keeping North America firmly ahead of every other region in this market throughout the year.

The United States accounted for roughly 83.00% of regional revenue, reflecting its concentration of large dairy herds and genomic breeding program investment. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding dairy and beef genetics programs, keeping North America among the most commercially significant regional markets for veterinary artificial insemination throughout the year.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Veterinary Artificial Insemination Market Insights

Europe contributed significantly to the world veterinary artificial insemination market in 2025 due to the presence of well-established dairy and beef genetic improvement programs and excellent cooperative breeding organization structures in Europe. Germany generated about 26.80% of regional revenue owing to its dairy cooperatives and genetic improvement programs.

France, the United Kingdom, and the Nordic countries followed a broadly similar trajectory, as continued genomic selection adoption and cooperative breeding program investment extended veterinary artificial insemination demand across the continent's largest dairy and beef markets. Continued emphasis on genetic improvement and disease resistance is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Veterinary Artificial Insemination Market Insights

Asia Pacific was the fastest-growing region in the global veterinary artificial insemination market, with India expected to register the highest country-level CAGR across the entire region, fueled by increasing demand for improved livestock productivity, supportive government initiatives, a high population of cattle, and rising awareness among end users. The Indian government has implemented various initiatives to enhance the bovine artificial insemination market, including the Rashtriya Gokul Mission and the National Artificial Insemination Programme.

India was responsible for around 34.60% of regional revenues, helped by the use of government-sponsored artificial insemination programs along with the rapid growth in the production capacity of sex-sorted semen from multiple government-run semen stations. The contribution of China and Southeast Asian countries to the region was also significant due to their growing efforts in livestock productivity.

MEA & Latin America Veterinary Artificial Insemination Market Insights

The Middle East & Africa segment experienced stable adoption of artificial insemination among veterinarians in 2025 due to increased livestock production programs and increasing governmental investments towards modernizing animal husbandry activities in Gulf countries and southern Africa. South Africa contributed around 28.10% to the regional revenue, backed by its well-developed cattle farming and dairy sector.

Latin America expanded at a comparable pace, led by Brazil at roughly 39.40% of regional revenue, where growing beef and dairy export infrastructure investment continued to support category growth. Argentina and Mexico followed a similar trajectory as regional livestock genetics adoption expanded further through the remainder of the forecast period.

Market Dynamics

Growth Drivers: Livestock productivity demands and sexed semen adoption

Growing demand to improve animal efficiency and productivity, alongside rising consumption of meat, milk, and dairy products, continues to be the central force behind veterinary artificial insemination market growth. The need for sustainable food production, combined with supportive initiatives by industry stakeholders and rising global livestock populations exceeding 987 million cattle and 1.5 billion pigs, continues reinforcing structural demand growth across nearly every major livestock-producing region.

Rising adoption of sexed semen technology continues letting producers select offspring gender to optimize dairy herd replacement rates or beef production economics, while technological advancements in cryopreservation continue improving genetic material viability across longer storage and transport distances. Increased focus on genetic improvement and disease resistance in breeding programs continues establishing artificial insemination as a key modern reproductive technique across bovine, porcine, and equine populations worldwide.

Restraints: Technician shortages and high capital costs for smaller operations

Inadequacy of qualified technicians and logistical issues in remote locations continue to act as a constraint on the growth of the veterinary artificial insemination market, especially in small-scale agricultural settings that lack veterinary networks. That skills and access gap continues limiting adoption in exactly the regions where livestock productivity improvement could deliver the greatest economic benefit.

High capital and operational costs for small and marginal farms continue posing a genuine barrier to broader artificial insemination adoption, as the equipment, semen, and technician expertise required can represent a meaningful expense relative to smallholder farm revenue. That cost barrier continues concentrating the most advanced artificial insemination technology adoption among larger, better-capitalized commercial livestock operations.

Opportunities: Government-backed program expansion and genomic selection advancement

Furthering the artificial insemination programs, such as the National Artificial Insemination Program in India offering free services in over six hundred districts, offers considerable opportunities for genetics firms that have the ability to capitalize on the expansion of these public channels. Those companies that have the ability to ramp up production and distribution to cater to subsidized programs will find considerable growth opportunities in these areas.

Continued advancement in genomic selection and precision breeding technology presents a further significant growth avenue, as producers increasingly seek data-driven reproductive management tools that go beyond basic insemination services. Genetics companies capable of delivering integrated genomic selection, sexed semen, and herd management technology stand to capture meaningful new revenue streams as precision livestock farming continues maturing through 2035.

Recent Developments:

-

2025: Select Sires announced a strategic partnership in January with an agri-tech firm to develop AI monitoring software for livestock farms, integrating estrus detection sensors with AI scheduling algorithms.

-

2024: ABS Global unveiled a new line of sexed semen in November optimized for high-altitude farming environments, targeting cattle breeders in mountainous states including Colorado and Utah.

-

2025: Geno launched a campaign in February showcasing Norwegian Red cattle and the impact of artificial insemination and embryo transfer technology in improving fertility and sustainability across dairy herds.

Veterinary Artificial Insemination Market key players are:

-

URUS Group LP

-

IMV Technologies

-

Zoetis Inc.

-

STgenetics

-

Semex Alliance

-

World Wide Sires, Ltd.

-

Alta Genetics Inc.

-

ABS Global, Inc.

-

Select Sires Inc.

-

Cogent Breeding Ltd.

-

Minitube GmbH

-

Swine Genetics International, Ltd.

-

Livestock Improvement Corporation Limited

-

Genetics Australia Cooperative Ltd.

-

Munster Bovine

-

VikingGenetics

-

Geno SA

Veterinary Artificial Insemination Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.00 Billion |

| Market Size by 2035 | USD 15.58 Billion |

| CAGR | CAGR of 8.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Services, Semen, Equipment Consumables) • By Animal Type (Bovine, Porcine, Equine, Ovine, Caprine) • By Technology Type (Conventional Semen, Sexed Semen) • By Distribution Channel (Private, Public) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | URUS Group LP, Genus plc, CRV Holding B.V., Neogen Corporation, IMV Technologies, Zoetis Inc., STgenetics, Semex Alliance, World Wide Sires, Ltd., Alta Genetics Inc., ABS Global, Inc., Select Sires Inc., Cogent Breeding Ltd., Minitube GmbH, Swine Genetics International, Ltd., Livestock Improvement Corporation Limited, Genetics Australia Cooperative Ltd., Munster Bovine, VikingGenetics, Geno SA |

Frequently Asked Questions

The Veterinary Artificial Insemination Market was valued at USD 7.00 Billion in 2025.

The Veterinary Artificial Insemination Market is expected to grow at a CAGR of 8.33% from 2026 to 2035.

Growing demand to improve animal efficiency and productivity combined with rising sexed semen adoption is the major growth factor.

The Bovine segment held approximately 58.40% share in 2025.

North America held the largest share of the Veterinary Artificial Insemination Market in 2025, at approximately 31.65%, while Asia Pacific was the fastest-growing region.

Get in Touch