Virtual Desktop Infrastructure Market Report Scope & Overview:

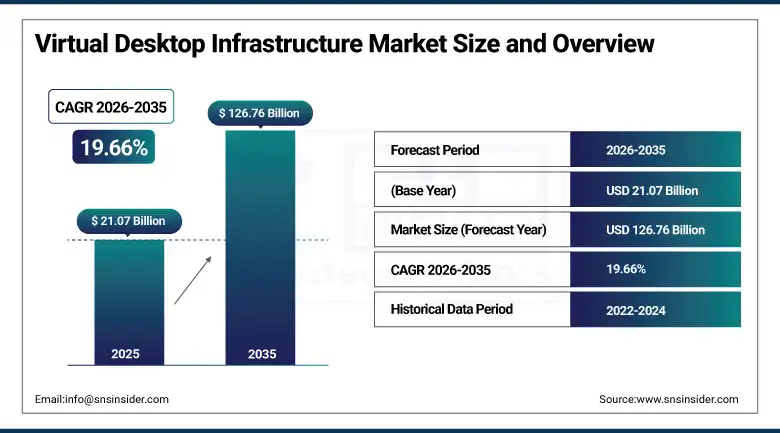

The Virtual Desktop Infrastructure Market was valued at USD 21.07 Billion in 2025 and is expected to reach USD 126.76 Billion by 2035, growing at a CAGR of 19.66% from 2026–2035.

The Virtual Desktop Infrastructure (VDI) market is growing rapidly because more people need remote and hybrid work setups. These setups need secure and flexible ways to access enterprise systems. Plus, rising cybersecurity concerns are pushing organizations to adopt centralized desktop management to cut down endpoint risks and data breaches. Businesses also aim to save money by cutting hardware dependency and boosting IT efficiency. Furthermore, the uptake of cloud services and the benefits of scalability, together with better high-speed internet, are speeding up VDI deployments. The increased use in BFSI, healthcare, and government sectors is also aiding global market growth in these areas.

According to the International Labour Organization ILO, around 27–30% of global employees were able to work remotely during peak digital adoption, permanently accelerating hybrid work models and increasing reliance on secure virtual desktop infrastructure for enterprise operations and workforce continuity across industries. According to GSMA GSMA, there are over 4.7 billion mobile internet users globally, enabling widespread cloud access and remote connectivity, which significantly supports virtual desktop infrastructure deployment for seamless enterprise access across devices and geographies.

Virtual Desktop Infrastructure Market Size and Forecast

-

Market Size in 2026E: USD 25.21 Billion

-

Market Size by 2035: USD 126.76 Billion

-

CAGR: 19.66% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Virtual Desktop Infrastructure Market - Request Free Sample Report

Virtual Desktop Infrastructure Market Trends

-

Rising demand for remote work enablement and secure digital workspaces is driving the virtual desktop infrastructure (VDI) market.

-

Growing adoption across BFSI, healthcare, IT, education, and government sectors is boosting market growth.

-

Expansion of cloud computing, hybrid work models, and digital transformation initiatives is fueling VDI deployment.

-

Increasing focus on centralized desktop management, data security, and cost efficiency is shaping adoption trends.

-

Advancements in cloud-hosted VDI, desktop-as-a-service (DaaS), and GPU virtualization technologies are enhancing performance and scalability.

U.S. Virtual Desktop Infrastructure Market Outlook

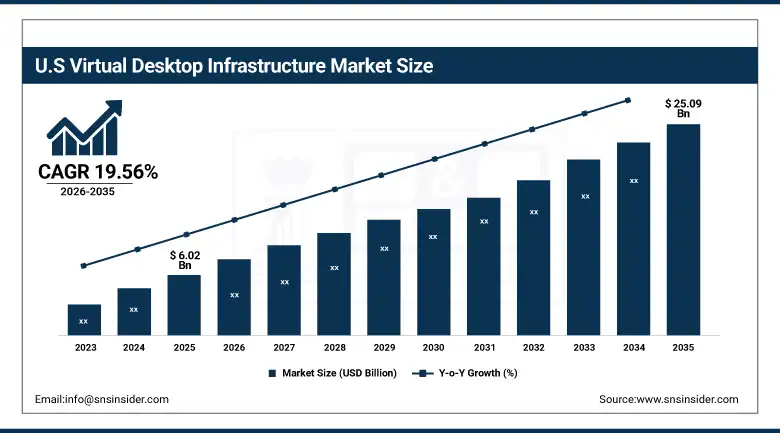

The U.S. Virtual Desktop Infrastructure Market was valued at approximately USD 6.02 Billion in 2024 and is expected to reach approximately USD 25.09 Billion by 2032, growing at a CAGR of approximately 19.56%.

The United States VDI market is driven by the largest enterprise technology investment base among major economies whose combination of hybrid work normalisation, the most stringent data privacy and cybersecurity regulatory requirements, and the highest cloud infrastructure adoption rate creates the most comprehensive commercial VDI demand profile globally. Federal government VDI deployment, where agencies managing classified and sensitive government data require secure desktop computing environments that VDI's centralised data control provides, creates substantial government-funded demand whose security requirements sustain premium VDI platform specification and create reference deployments that commercial enterprise procurement follows.

Virtual Desktop Infrastructure Market Segment Analysis

-

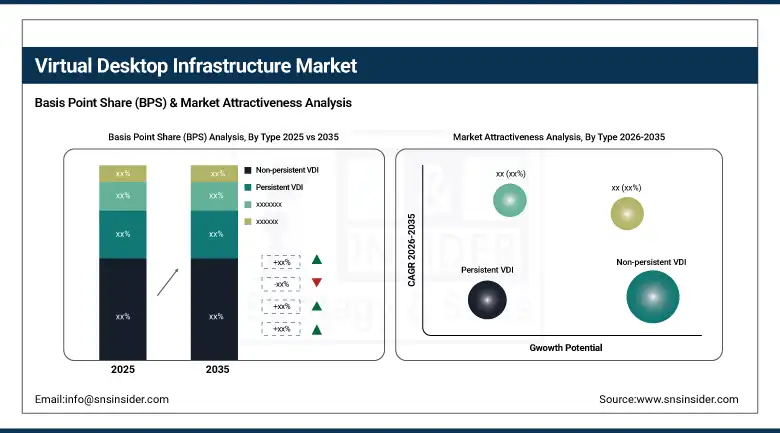

By Type, non-persistent VDI segment dominated the virtual desktop infrastructure market in 2025 with 63% share; persistent VDI segment is the fastest growing segment.

-

By Application, BFSI segment dominated the market in 2025 with 27% share; healthcare segment is the fastest growing segment.

-

By Deployment Model, on-premise segment dominated the market in 2025 with 55% share; cloud segment is the fastest growing segment.

-

By Component, software segment dominated the market in 2025 with 48% share; services segment is the fastest growing segment.

By Type, Non-persistent VDI segment dominates the Market, while persistent VDI segment is expected to grow fastest

Non-persistent VDI dominated the Virtual Desktop Infrastructure Market in 2025 because of its cost-effectiveness, easy management, and scalability in big companies. Users get a standard session that wipes clean when logging out, which cuts storage needs and lessens security threats. This model works great for task-driven places like call centers and schools. Plus, its simple setup and maintenance make it popular among organizations looking for an efficient way to deliver virtual desktops.

Persistent VDI is the fastest growing segment because people want personal desktops with their individual settings no matter where they log in from. Users keep all their apps and info between sessions, making them more productive. As remote and hybrid working become norms, the need for a seamless desktop experience rises too. Companies needing special setups and top-tier performance are turning to persistent VDI at lightning speed, driving market growth.

By Application, BFSI segment dominates the Market, while healthcare segment is expected to grow fastest

The BFSI segment dominated the market because they rely heavily on secure, scalable, and regulated IT environments. Virtual desktop infrastructure helps banks and financial institutions keep data secure and comply with rules, too. Plus, it lets workers access stuff remotely without putting info at risk. Given how many transactions they handle and their need for always-on operations, it’s no surprise that BFSI drives a good portion of the VDI market demand.

Healthcare is the fastest growing segment due to more patient records are going digital, telemedicine is expanding, and people want secure access to medical systems from anywhere. So, VDI fits perfectly here, letting healthcare providers view records safely from any location. With more remote diagnosis and mobile health services coming online, demand is speeding up in this area. To wrap it up, the need for protected, centralized IT setups in healthcare settings is really fuelling this growth.

By Deployment Model, On-premise segment dominates the, while cloud deployment segment is expected to grow fastest

On-premise deployment dominated the market due to its solid security and strong data privacy benefits, which align perfectly with industry regulations. Companies were comfortable owning all of their infrastructure and storing sensitive info within their own networks. Big businesses and government agencies in particular went for this option since it gave them total control over IT assets. The initial higher costs didn't matter much compared to the peace of mind from its reliability, flexible customization, and tight performance controls.

Cloud deployment is the fastest growing segment due to its easy scalability, cheaper costs, and sheer flexibility. No more giant initial investments in hardware; setting up is a breeze along with enabling work-from-anywhere scenarios. Cloud VDI solutions have never been more in demand with the current shift towards remote and hybrid work models. Plus, boosts in cloud security and the rise of pay-as-you-go pricing make this choice super attractive for many companies.

By Component, Software segment dominates the Market, while services segment is expected to grow fastest

The software segment dominated the market because it enables virtualization, desktop management, and control of user sessions. This bit of VDI manages crucial tasks like resource allocation, security enforcement, and central management. Businesses invest heavily in these solutions to roll out virtual desktops on a large scale in various locations. With constant updates, solid compatibility with diverse IT structures, and a huge push for secure digital environments, this sector keeps its dominant status.

Services are the fastest growing segment due to the surge in demand for consulting and managed VDI services. Most companies need experts to create and fine-tune their virtual desktop systems. The intricate job of embracing hybrid cloud setups and maintaining security makes them highly dependent on service providers. Small businesses hopping on these tech trends but short on in-house expertise boost this segment's growth too.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Virtual Desktop Infrastructure Market Insights

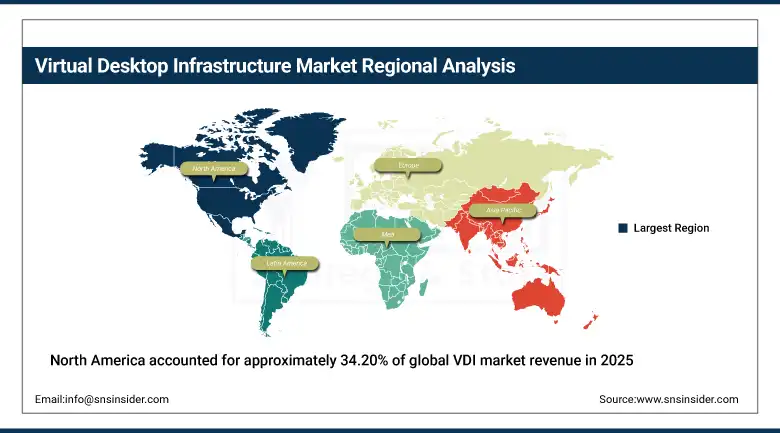

North America accounted for approximately 34.20% of global VDI market revenue in 2024, maintained through the highest enterprise cloud adoption rate, most mature hybrid work implementation, and most stringent cybersecurity and data privacy regulatory requirements of any regional market. The United States accounts for approximately 82.5% of North American revenues through the commercial concentration of VDI platform leaders including VMware by Broadcom, Citrix, Microsoft, and AWS WorkSpaces whose U.S. headquarters and primary enterprise customer relationships define global market standards and whose combined product development investment sustains the innovation pace that competitive VDI deployment requires.

According to the U.S. Bureau of Labor Statistics BLS, around 27% of U.S. workdays are still conducted in remote or hybrid formats, reinforcing sustained enterprise reliance on virtual desktop infrastructure to support flexible work arrangements, secure access, and continuity across distributed workforce environments.

According to the U.S. Census Bureau U.S. Census Bureau, over 92% of enterprises use cloud services, enabling scalable virtual desktop deployment and accelerating adoption of centralized digital workspaces that improve operational efficiency, reduce IT complexity, and support enterprise-wide remote access capabilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Virtual Desktop Infrastructure Market Insights

Europe held a significant share of the global VDI Market in 2025. Germany, the United Kingdom, France, the Netherlands, and Sweden are the leading national markets whose GDPR data protection requirements, strong enterprise IT investment culture, and progressive hybrid work adoption create consistent and growing VDI demand. Germany accounts for approximately 28.5% of European revenues through its large enterprise technology sector, the commercial presence of SAP and Deutsche Telekom whose enterprise infrastructure creates VDI adoption reference, and the German banking and insurance sector's stringent data security requirements that VDI's centralised data control satisfies.

According to the European Commission European Commission Digital Economy report, over 75% EU enterprises use cloud computing services, enabling widespread VDI adoption across industries by supporting scalable infrastructure, remote access capabilities, and secure centralized desktop environments for modern digital operations.

According to Eurofound reports, around 30% EU workers engage in hybrid or remote work arrangements, sustaining demand for virtual desktop access and secure enterprise systems across organizations in the region and digital workplace continuity solutions.

Asia Pacific Virtual Desktop Infrastructure Market Insights

Asia Pacific is the fastest-growing regional VDI market with an estimated CAGR of approximately 20.54% during 2024-2032, driven by rapid digital transformation, increasing cloud adoption, rising IT spending in emerging nations, and growing regulatory data protection requirements. China accounts for approximately 38.5% of Asia Pacific revenues through its large enterprise technology sector, growing financial services and healthcare VDI adoption, and domestic cloud VDI platform development from Alibaba Cloud Desktop and Huawei CloudDesktop whose domestic market presence complements international platform offerings.

According to GSMA GSMA, APAC accounts for over 60% of global mobile internet users, enabling large-scale remote workforce connectivity and supporting cloud-based collaboration and virtual desktop infrastructure adoption across enterprises and digital service ecosystems in the region.

India’s IT-BPM industry employs over 5 million professionals, with widespread adoption of hybrid and remote work models driving demand for VDI systems that enable secure access, centralized management, and scalable digital work environments across global delivery operations.

MEA & Latin America Virtual Desktop Infrastructure Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its advanced digital economy infrastructure, the Smart Dubai initiative's government digitisation programmes creating public sector VDI adoption, and the financial services and technology sectors whose data security requirements create VDI demand at premium enterprise specification. Saudi Arabia's Vision 2030 digital transformation and growing cloud infrastructure investment are creating expanding VDI adoption across government and enterprise sectors.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its large financial services sector's LGPD data protection compliance requirements creating VDI security motivation, the growing enterprise technology adoption in retail and manufacturing sectors, and the hybrid work adoption whose corporate real estate optimisation creates financial incentive for VDI-enabled flexible workplace deployment.

Market Dynamics

Growth Drivers: Hybrid and remote work normalisation increases enterprise demand for secure desktop delivery through VDI adoption.

The VDI market's extraordinary growth rate is driven by the permanent structural shift in enterprise work models whose hybrid and remote work adoption, accelerated by the pandemic and sustained by demonstrated productivity, talent retention, and real estate cost benefits, has elevated VDI from a specialised disaster recovery and secure access tool into a mainstream enterprise IT infrastructure requirement.

Each organisation that establishes a permanent hybrid work policy, estimated at over 70% of knowledge worker employers in developed economies, creates an IT infrastructure requirement for consistent, secure, and managed desktop computing delivery whose VDI implementation is progressively becoming the enterprise standard over legacy VPN plus physical device management approaches whose security limitations, management complexity, and end-user experience inconsistency become commercially unacceptable as hybrid work models mature.

Restraints: High initial infrastructure costs and bandwidth limitations restrict VDI deployment in capital-constrained enterprise environments.

Enterprise VDI deployment's upfront capital investment, encompassing high-performance server infrastructure, shared storage systems, network upgrade investment, and VDI platform software licensing whose combined capital cost per concurrent user ranges from USD 800 to USD 2,500 depending on deployment architecture and performance specification, creates procurement barriers whose justification requires ROI analysis spanning infrastructure, licence, support, and end-user productivity considerations that procurement teams without VDI deployment experience may approach conservatively.

Network performance dependency creates deployment quality risk in locations where internet bandwidth, latency, or reliability falls below the thresholds that acceptable VDI user experience requires, creating geographic coverage gaps in rural, international, and branch office locations whose connectivity characteristics constrain VDI quality below the performance standard that mandating VDI as the sole computing architecture requires. End-user resistance to VDI adoption whose perceived performance inferiority versus native desktop computing, particularly for graphics-intensive and locally cached application workloads, creates change management investment requirements that extend VDI deployment programmes and create reputational risk from negative user experience early in deployment rollout.

Opportunities: Desktop-as-a-Service and AI-powered workspace intelligence enable scalable, personalized, and barrier-free VDI cloud experiences.

Desktop-as-a-Service platforms whose cloud delivery of fully managed virtual desktop environments eliminates the on-premise infrastructure capital investment, hypervisor management complexity, and storage administration burden that have historically made VDI viable primarily for organisations with substantial IT infrastructure competence represent the most commercially transformative VDI market development in the current decade. Each organisation that adopts DaaS in preference to on-premise VDI accesses enterprise virtual desktop capability at operating expense subscription economics without the capital investment that infrastructure-based VDI requires, expanding the addressable VDI market to include SMEs and organisations without dedicated infrastructure teams whose on-premise VDI barriers were previously insurmountable.

Recent Developments:

-

2025: Citrix launched Citrix Virtual Apps and Desktops 2025 with AI-powered session performance optimisation that dynamically adjusts bandwidth allocation, display compression, and protocol parameters based on real-time network conditions and user interaction patterns, improving VDI user experience under variable connectivity conditions.

-

2024: VMware by Broadcom enhanced its Horizon VDI platform with expanded cloud-native deployment options, improved Azure Virtual Desktop integration, and AI-powered workspace analytics enabling IT administrators to identify underutilised resources, predict capacity requirements, and optimise licence allocation based on actual usage patterns.

-

2024: Microsoft expanded Azure Virtual Desktop with Windows 365 Boot capability enabling organisations to configure physical devices whose entire desktop experience streams from the cloud, eliminating local operating system management while delivering a native-quality Windows computing experience from any hardware connected to Azure.

Virtual Desktop Infrastructure Market Key Players

-

Citrix Systems

-

Microsoft

-

Amazon Web Services (AWS)

-

IBM

-

Hewlett Packard Enterprise (HPE)

-

Dell Technologies

-

Oracle

-

Huawei Technologies

-

Nutanix

-

Red Hat

-

Parallels International

-

NComputing

-

IGEL Technology

-

Teradici

-

Stratodesk

-

V2 Cloud

-

Fujitsu

-

Centerm

Virtual Desktop Infrastructure Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.07 Billion |

| Market Size by 2035 | USD 126.76 Billion |

| CAGR | CAGR of 19.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Persistent VDI and Non-persistent VDI) • By Application (BFSI, IT & telecom, Aerospace & defense, Government, Manufacturing, Education, Retail, Transportation, Healthcare and Others) • By Deployment Model (On-premise and Cloud) • By Component (Hardware, Software and Services) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | VMware, Citrix Systems, Microsoft, Amazon Web Services (AWS), IBM, Cisco Systems, Hewlett Packard Enterprise (HPE), Dell Technologies, Oracle, Huawei Technologies, Nutanix, Red Hat, Parallels International, NComputing, IGEL Technology, Teradici, Stratodesk, V2 Cloud, Fujitsu and Centerm. |

Frequently Asked Questions

The Virtual Desktop Infrastructure Market is expected to grow at a CAGR of 19.66% from 2026 to 2035.

The Virtual Desktop Infrastructure Market was valued at USD 21.07 Billion in 2025.

Hybrid work, cybersecurity risks, cloud DaaS adoption, AI optimisation, and regulatory compliance are driving strong VDI market growth globally.

The Non-Persistent VDI segment dominated the Virtual Desktop Infrastructure Market with approximately 57.50% share in 2025.

North America dominated the Virtual Desktop Infrastructure Market in 2024 with approximately 34.20% of global revenue.

Get in Touch