Industrial Cables Market Report Scope & Overview:

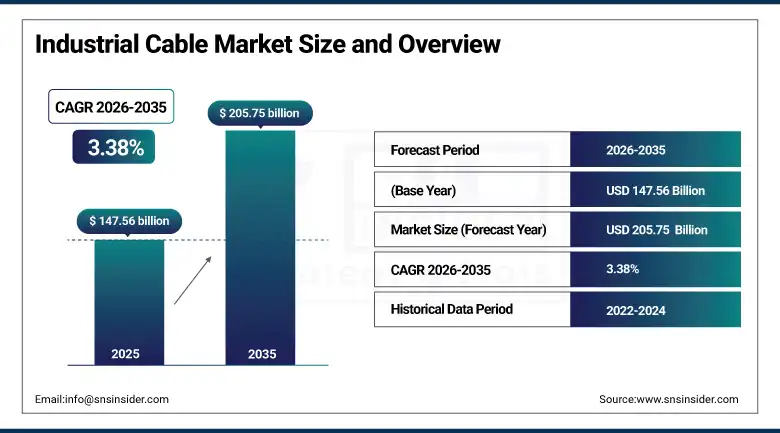

The industrial cables market was valued at USD 147.56 billion in 2025 and is expected to reach USD 205.75 billion by 2035, growing at a CAGR of 3.38% from 2026–2035.

The global industrial cables market is undergoing a meaningful transformation driven by the simultaneous forces of industrial digitalization under Industry 4.0 frameworks, the electrification megatrend spanning electric vehicle manufacturing, renewable energy infrastructure, and the replacement of fossil-fuel industrial processes with electric alternatives, and the data infrastructure build-out required by AI computing, 5G telecommunications, and cloud services. The market’s structural growth is underpinned by the irreversibility of its primary demand drivers: the global electricity network requires approximately USD 21 trillion of grid infrastructure investment through 2040 according to IEA projections, electric vehicle production is scaling to a level requiring substantially more automotive-grade cable per vehicle than internal combustion equivalents, and the 5G telecommunications network densification requires millions of kilometers of new fiber optic cable deployment annually. Prysmian Group’s May 2025 production capacity expansion and Nexans’s January 2025 launch of new sustainable industrial cable solutions collectively demonstrate the leading players’ strategic investment in serving the energy transition and industrial digitalization demand defining the market’s growth trajectory.

The global renewable energy infrastructure investment cycle, encompassing onshore and offshore wind, utility-scale solar, grid interconnection projects, and cross-border electricity transmission, is creating the largest concentrated demand for high and extra-high voltage cable in the history of the industry, with offshore wind farm array cables, export cables, and grid connection systems alone requiring hundreds of thousands of kilometers of specialized submarine and land cable annually at a global investment rate creating multi-year backlogs at the world’s largest cable manufacturers.

Market Size and Forecast

-

Market Size in 2026E: USD 152.55 Billion

-

Market Size by 2035: USD 205.75 Billion

-

CAGR (2026-2035): 3.38%

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Industrial Cable Market - Request Free Sample Report

Industrial Cables Market Trends

-

Accelerating demand for high-performance data and fiber optic cables across industrial automation environments where the deployment of IIoT sensors, machine vision systems, collaborative robots, and real-time process control networks is creating exponentially growing data communication requirements.

-

Growing adoption of halogen-free, low-smoke, and zero-halogen cable compounds across industrial, commercial, and public infrastructure installations, driven by fire safety regulatory tightening that requires cables to minimize toxic gas emission during combustion, combined with growing environmental awareness of halogenated compound lifecycle.

-

Rising integration of smart and sensing cable technologies including embedded fiber Bragg grating temperature and strain sensors, distributed acoustic sensing cables, and power line carrier communications-enabled cable systems that transform passive conductor infrastructure into active monitoring and data communications assets enabling predictive maintenance and structural health monitoring.

-

Growing development of cable systems specifically engineered for the offshore wind farm application, including array cables connecting turbines, dynamic export cables, and long-distance HVDC submarine cables connecting offshore generation clusters to onshore grid connection points, each requiring distinct electrical, mechanical, and environmental performance specifications.

-

Expanding deployment of aluminum conductor cable as an alternative to copper in power distribution and transmission applications, with aluminum conductor steel reinforced and all-aluminum alloy conductor cable finding growing application in overhead transmission, medium voltage distribution, and large-scale industrial power supply installations.

The U.S. Industrial Cables Market Outlook

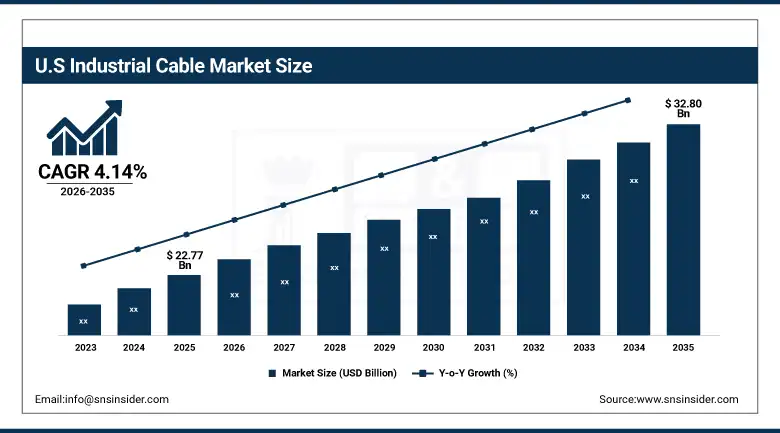

The U.S. industrial cables market was valued at approximately USD 22.77 billion in 2025 and is expected to reach approximately USD 32.80 billion by 2035, growing at a CAGR of 4.14%, driven by large-scale investments in automation, electrification, and clean energy infrastructure, supported by the CHIPS Act’s semiconductor manufacturing facility construction programme, the Bipartisan Infrastructure Law’s grid modernisation and broadband deployment funding, and the Inflation Reduction Act’s renewable energy incentives that collectively direct hundreds of billions of infrastructure capital toward projects requiring substantial industrial cable procurement. The CHIPS Act’s directed investment in semiconductor fabrication facility construction, with facilities including TSMC’s Arizona fab, Intel’s Ohio fab, and Samsung’s Texas expansion collectively requiring billions of dollars of industrial cable for power distribution, process control, clean room communications, and building systems, represents a distinctive U.S. procurement driver.

The U.S. industrial cable market’s competitive landscape is being reshaped by the growing domestic manufacturing investment of international cable manufacturers including Prysmian’s General Cable acquisition operations and Nexans’s North American manufacturing footprint whose IRA domestic content qualification strategies are expanding U.S.-based cable production capacity for the types of infrastructure and renewable energy cables that federal incentive programmes require to access the highest tier of tax credit support.

Industrial Cables Market Segment Analysis

-

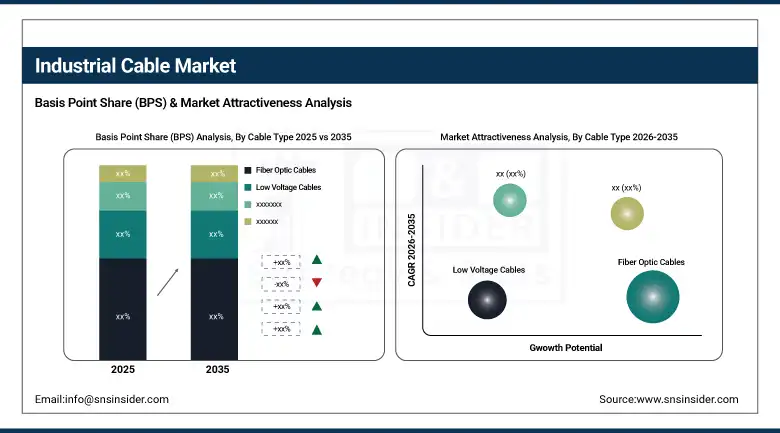

By cable type, fiber optic cables dominated with approximately 43.87% revenue share in 2025; medium voltage cables are the fastest-growing cable type at a CAGR of approximately 4.97%.

-

By conductor material, copper led with approximately 62.10% share in 2025; fiber optics is the fastest-growing conductor material.

-

By end user application, power and energy dominated in 2025; automotive and transportation is the fastest-growing application at a CAGR of approximately 4.78%.

By Cable Type, fiber optic cables dominate, medium voltage grows fastest

Fiber optic cables retained the dominant cable type position with approximately 43.87% of the industrial cables market in 2025. The industrial fiber optic cable segment encompasses the full application range from tight-buffered multimode fiber running between equipment and control cabinets within an automation cell, through single-mode OS2 fiber carrying communications across plant-wide networks, to armored and ruggedized fiber assemblies used in outdoor and harsh environment applications across mining, oil and gas, and outdoor industrial installations where fiber’s immunity to electromagnetic interference and ability to span long distances without signal amplification provide compelling advantages. Prysmian Group’s leadership in industrial fiber optic cable supply, particularly for applications requiring specialized jacket materials, armored construction, and fire-rated performance, exemplifies the technical depth that leading industrial cable manufacturers maintain in the fiber segment’s most specification-demanding application categories.

Medium voltage cables are the fastest-growing cable type at a CAGR of approximately 4.97% through 2035. The electric vehicle charging infrastructure deployment across North America, Europe, and Asia Pacific is creating growing demand for medium voltage cable to connect DC fast charging stations and high-power charging depots to the utility distribution network at the 350 kW and above power levels that modern EV charging standards require. Nexans’s active innovation in medium voltage solutions tailored for smart grids and energy-efficient systems reflects the strategic importance that leading cable manufacturers place on this segment whose growth trajectory is among the strongest in the broader industrial cable portfolio.

By Conductor Material, copper dominate, fiber optics grows fastest

Copper retained the dominant conductor material position with approximately 62.10% of the industrial cables market in 2025. The copper conductor cable market spans the full application spectrum from fine gauge signal and instrumentation cables whose precise electrical characteristics require copper’s consistent conductivity, through medium and high voltage power cables carrying industrial and utility electrical loads, to specialty automotive wiring harnesses whose mechanical and thermal performance requirements demand copper’s combination of conductivity and mechanical workability. Copper’s commercial position is reinforced by the difficulty of substituting alternative materials in many highest-volume applications: aluminum cannot practically substitute copper in flexible cables, small-gauge signal wiring, or the compact high-strand-count constructions that automotive and control cable applications require.

Fiber optics is the fastest-growing conductor material in the industrial cables market, driven by the structural shift in industrial data communications away from copper-based Ethernet and fieldbus protocols toward fiber optic networks that deliver the bandwidth, distance, and electromagnetic immunity performance that modern industrial automation, smart factory, and telecommunications infrastructure demands require and that copper data cables cannot cost-effectively provide. The industrial fiber optic cable market’s fastest-growing sub-segments include bend-insensitive single-mode fiber for data center inter-rack communications, harsh-environment armored fiber for manufacturing floor automation networks in heavy industry environments, and submarine and direct-burial fiber for outdoor industrial site networks and telecommunications infrastructure.

By End User Application, power & energy dominate, automotive grows fastest

Power and energy retained the dominant end user application position in 2025, reflecting the foundational role of electrical power cable in the construction, expansion, and modernisation of electricity infrastructure that supports every economic activity globally. The power and energy application’s commercial scale encompasses the full electricity value chain from extra-high voltage transmission cables carrying bulk power across grid interconnection corridors, through high and medium voltage distribution cables serving industrial complexes and commercial districts, to the low voltage cables connecting end-use electrical equipment, EV charging points, and rooftop solar installations to the distribution network. The renewable energy installation wave is the most commercially consequential growth driver within this application, with the offshore wind sector’s demand for submarine array and export cables in particular creating multi-billion-dollar annual procurement requirements.

Automotive and transportation is the fastest-growing end user application at a CAGR of approximately 4.78% through 2035, propelled by the electric vehicle revolution whose impact on per-vehicle cable content is approximately 1.5 to 3 times the cable length of a comparable internal combustion engine vehicle as the combination of high-voltage battery system cabling at 400V or 800V operating voltages, low-voltage control and communication network wiring, and increasingly comprehensive ADAS sensor and camera wiring are collectively increasing vehicle wiring harness weight, complexity, and per-unit cable procurement value with each new vehicle generation. Sumitomo Electric Industries is a leading beneficiary of automotive cable demand growth, with continuous R&D investment in lightweight aluminum automotive wiring harnesses, high-voltage cable for EV traction systems, and high-speed data cable for in-vehicle Ethernet network architectures.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Industrial Cables Market Insights

North America is the fastest-growing regional industrial cables market at a projected CAGR of approximately 5.06% through 2035, driven by the extraordinary federal infrastructure investment programme across the CHIPS Act’s semiconductor manufacturing facility construction, the Bipartisan Infrastructure Law’s grid and broadband investment, and the Inflation Reduction Act’s renewable energy incentives collectively representing the largest peacetime federal infrastructure investment in American history. The United States accounts for approximately 87.4% of North American industrial cable revenues through its dominant share of the region’s infrastructure investment, manufacturing base, and industrial cable procurement. Canada contributes approximately 12.6% of North American revenues through its significant mineral and energy resource extraction industries, rapidly growing clean energy infrastructure investment, and advanced manufacturing sector whose collective industrial cable requirements sustain meaningful ongoing procurement across both power and data cable categories.

Europe Industrial Cables Market Insights

Europe is a technically sophisticated and commercially important industrial cables market whose development is primarily driven by the extraordinary renewable energy and grid infrastructure investment cycle associated with the EU’s REPowerEU programme, the offshore wind expansion programmes of North Sea coastal nations, and the extensive cross-border grid interconnection investment required to integrate increasing shares of renewable generation across the integrated European electricity market. Germany accounts for approximately 22.3% of European industrial cables revenues as the region’s largest national market, anchored by the country’s dominant industrial manufacturing base in automotive, machinery, chemical, and semiconductor sectors whose combined industrial cable requirements represent Europe’s largest national industrial procurement volume, alongside substantial utility grid modernisation and offshore wind connection cable procurement that Germany’s Energiewende renewable energy transition programme requires. The European cable market’s sustainability focus is influencing product specifications, with halogen-free cable compounds, recycled content insulation materials, and certified responsible mineral sourcing becoming standard procurement requirements across major European infrastructure projects.

Asia Pacific Industrial Cables Market Insights

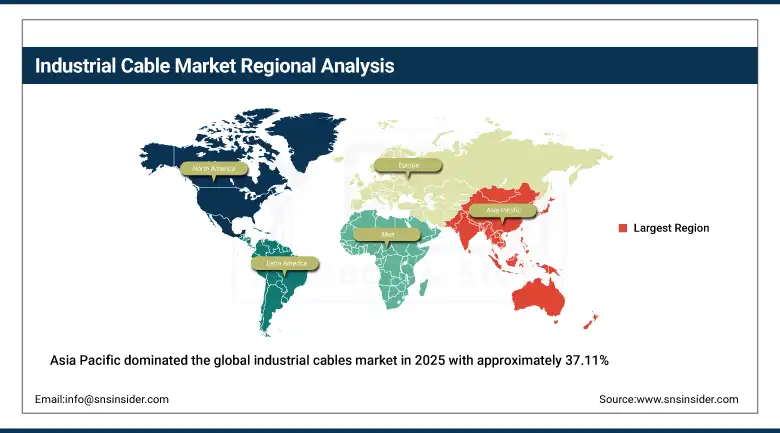

Asia Pacific dominated the global industrial cables market in 2025 with approximately 37.11% of global revenues, driven by the region’s extraordinary concentration of manufacturing capacity, infrastructure construction activity, and the world’s most rapidly expanding electricity network collectively generating the highest industrial cable demand volumes globally. China accounts for approximately 61.7% of Asia Pacific industrial cable revenues through its combination of the world’s largest electricity network requiring continuous expansion and upgrade cable procurement, the world’s largest manufacturing sector requiring industrial and automation cable throughout its production infrastructure, and the world’s leading renewable energy installation programme creating offshore and onshore wind, solar, and grid cable demand at scales making China the largest single-country cable procurement market by a substantial margin. Japan and South Korea represent advanced secondary Asia Pacific markets whose industrial cable demand is driven by sophisticated manufacturing automation adoption, advanced semiconductor facility construction, and significant renewable energy infrastructure investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Latin America and MEA Industrial Cables Market Insights

Latin America and the Middle East and Africa are growing industrial cables markets where rapid resource extraction investment, renewable energy infrastructure development, and industrial manufacturing expansion are creating growing cable demand across regions simultaneously increasing their economic complexity and infrastructure quality. Brazil accounts for approximately 44.2% of Latin American industrial cables revenues through its combination of the region’s largest and most diversified industrial economy, extensive oil and gas infrastructure requiring continuous cable maintenance and expansion procurement, growing wind and solar energy generation infrastructure, and a significant manufacturing sector whose automation adoption is progressing at an accelerating pace. Saudi Arabia leads Middle East and Africa industrial cables revenues at approximately 38.4% of the regional total, driven by Vision 2030’s enormous industrial diversification and infrastructure investment programme creating cable demand across petrochemical complex construction, new city development including NEOM, and the Kingdom’s rapidly growing renewable energy generation network.

Market Dynamics

Growth Drivers: Industry 4.0 automation and digitalization creating data cable demand, renewable energy and grid modernisation creating power cable demand

The primary structural growth drivers for the industrial cables market are the three megatrends of industrial digitalization, energy transition, and transportation electrification whose combined demand implications for industrial cable are mutually reinforcing and collectively define a sustained demand growth trajectory independent of any single sector’s economic cycle. The industry 4.0 automation trend’s requirement for reliable, high-speed, and electromagnetically immune data cable interconnections across smart factory sensor networks, robot interfaces, machine vision systems, and edge computing infrastructure creates a demand driver for industrial data and fiber optic cable that grows proportionally with automation capital investment. The IEA’s estimate that the global electricity network must nearly triple in length from 80 million to 230 million kilometers of power lines by 2040 represents a cable installation requirement whose annual investment volume is unprecedented in the industry’s history.

Restraints: Copper and aluminum raw material price volatility creating cable product cost instability, offshore wind project permitting and installation delays

A significant restraint on the industrial cables market is the raw material cost volatility affecting cable manufacturing economics, particularly for copper whose price on the London Metal Exchange fluctuates significantly in response to macroeconomic conditions, Chinese manufacturing demand cycles, and mine supply disruptions, creating cost uncertainty for cable manufacturers whose pricing must balance pass-through of material cost changes against the risk of demand disruption when cable price increases exceed customer budget expectations. The offshore wind sector’s extraordinary cable demand growth is simultaneously creating supply chain constraints at submarine cable manufacturers whose cable-laying vessel capacity, specialized manufacturing equipment, and skilled technical workforce cannot be expanded as rapidly as the project development pipeline is growing.

Opportunities: Offshore wind submarine cable infrastructure creating high-value specialized cable demand, EV charging network expansion creating medium voltage cable growth

The offshore wind submarine cable opportunity is the most commercially exciting growth vector in the industrial cables market, as the extraordinary scale of global offshore wind development creates demand for array cables, export cables, and HVDC interconnection cables whose per-project value, technical specification complexity, and supply concentration among a small number of qualified submarine cable manufacturers create the most commercially valuable and highest-margin cable procurement opportunities in the global market. The EV charging infrastructure build-out represents a growing and geographically distributed medium voltage cable demand category whose annual procurement volumes are increasing as charging network operators, utilities, and commercial property developers across North America, Europe, and Asia Pacific invest in the charging infrastructure required to support the growing global EV fleet.

Recent Developments

-

2025: Prysmian Group expanded its industrial cable production capacity in May 2025 to support accelerating demand from renewable power and smart grid infrastructure upgrades across international markets, investing in new manufacturing lines for high and medium voltage cables that serve both the offshore wind and grid modernisation cable demand streams.

-

2025: Nexans launched new industrial cable solutions designed to improve sustainability and energy efficiency in January 2025, aligning its product portfolio with increasing electrification and carbon reduction initiatives across its major customer industries and demonstrating the company’s strategic commitment to its ‘Electrification Pure Player’ positioning.

-

2025: Sumitomo Electric Industries expanded its automotive wiring harness production capacity for electric vehicle applications, investing in new manufacturing infrastructure for high-voltage cable systems and lightweight aluminum conductor wiring harnesses designed for the 800-volt EV traction architecture that leading electric vehicle OEMs are adopting for next-generation BEV models.

Industrial Cables Market key players are:

-

Prysmian Group

-

Nexans S.A.

-

Sumitomo Electric Industries Ltd.

-

NKT A/S

-

Belden Inc.

-

Leoni AG

-

Lapp Group

-

HELUKABEL GmbH

-

LS Cable & System Ltd.

-

Furukawa Electric Co., Ltd.

-

Southwire Company LLC

-

General Cable (Prysmian)

-

Hengtong Group Co., Ltd.

-

ZTT Group

-

Far East Cable Co., Ltd.

-

Polycab India Limited

-

KEI Industries Limited

-

Finolex Cables Limited

-

Sterlite Technologies Limited

-

ABB Ltd. (Cable business)

Industrial Cables Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 147.56 Billion |

| Market Size by 2035 | USD 205.75 Billion |

| CAGR | CAGR of 3.38% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Cable Type (Fiber Optic Cables, Low Voltage Cables, Medium Voltage Cables, High Voltage Cables, Signal & Control Cables) • By Conductor Material (Copper, Aluminum, Fiber Optics) • By End User Application (Power & Energy, Automotive & Transportation, Telecommunications, Oil & Gas, Manufacturing & Automation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Prysmian Group, Nexans S.A., Sumitomo Electric Industries Ltd., NKT A/S, Belden Inc., Leoni AG, Lapp Group, HELUKABEL GmbH, LS Cable & System Ltd., Furukawa Electric Co., Ltd., Southwire Company LLC, General Cable (Prysmian), Hengtong Group Co., Ltd., ZTT Group, Far East Cable Co., Ltd., Polycab India Limited, KEI Industries Limited, Finolex Cables Limited, Sterlite Technologies Limited, ABB Ltd. (Cable business) |

Get in Touch