Water-Based Barrier Coatings Market Report Scope & Overview:

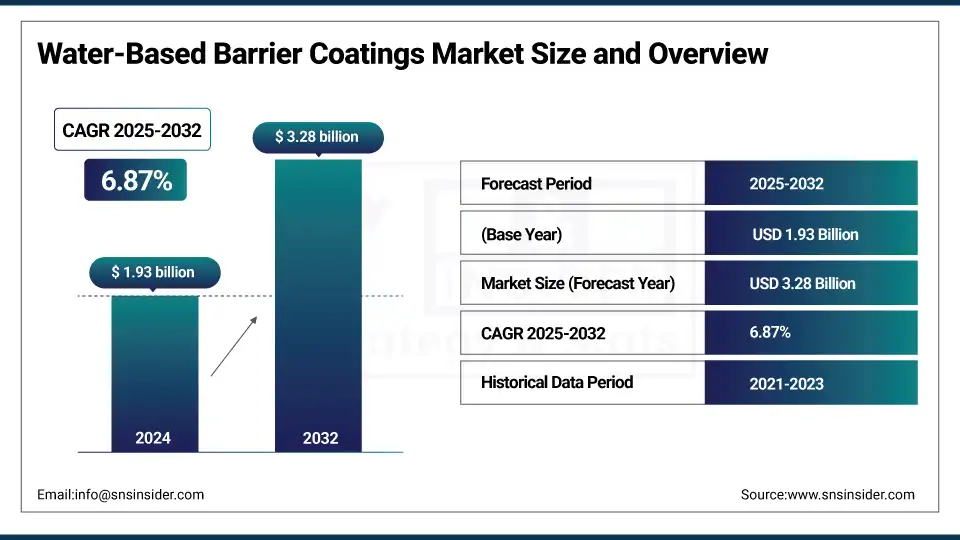

The Water-Based Barrier Coatings Market size was valued at USD 1.93 billion in 2024 and is expected to reach USD 3.28 billion by 2032, growing at a CAGR of 6.87% over the forecast period of 2025-2032.

The waterborne barrier coatings market is influenced by the rising demand for eco-friendly solutions such as bio-based barrier coatings and biodegradable coatings required in compostable packaging and antimicrobial coatings. Barred by unparalleled environmental consciousness, prominent water-based barrier coatings manufacturers such as Michelman, are high on innovation with mono-material and plastic-free solutions that bolster barrier functionality for food & beverage packaging, thereby mirroring crucial trends in the water-based coatings industry. Alliances such as that between UPM Specialty Papers and Michelman demonstrates that there is widespread attention to increase in oxygen and moisture vapor barriers. Water-based barrier coatings industry reports strong industry adoption, with USDA’s BioPreferred Program certifying approximately 10,000 biobased products and recognizing nearly 20,000 biobased offerings. The overall barrier coatings market added USD 489 billion to the U.S. economy and supported close to 4 million jobs in 2021, highlighting that robust market gains and market share shift in water-based barrier coatings are on the horizon due to sustainability and innovation.

To Get more information On Water-Based Barrier Coatings Market - Request Free Sample Report

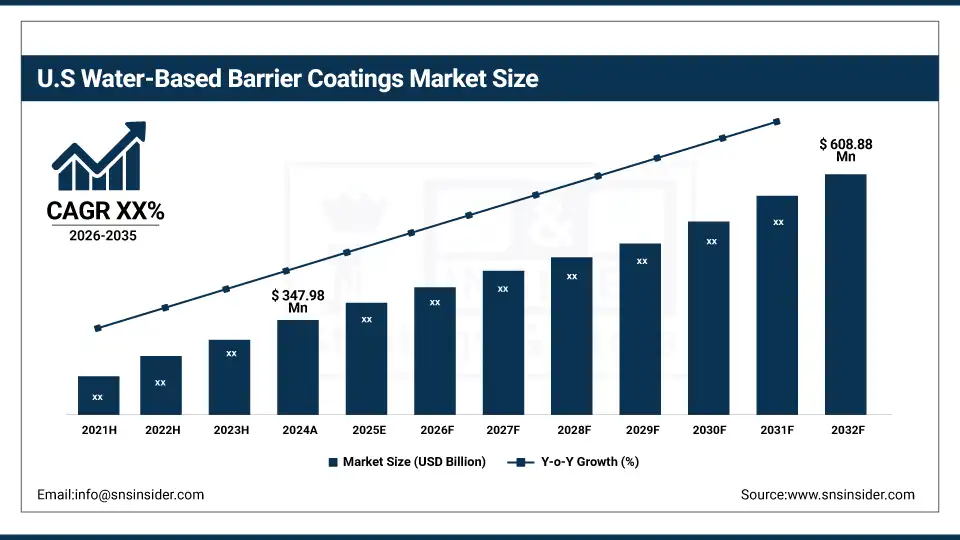

The U.S. dominates North America’s water-based barrier coatings market with a market size of USD 347.98 million in 2024 and is projected to reach a value of USD 608.88 million by 2032 with a market share of about 76%. The dominance of the two superpowers is the result of advanced R&D and strict regulation. Packaging safety approvals of US FDA make it attractive for broader applications in the food and beverage industries, and the USDA Certified Biobased Product Label also promotes use of biopolymer-based coatings. Large companies that are known for water-based barrier coatings, like H.B. Fuller and Michelman, have released recyclable, water-based technologies targeted at big brands. Further, EPA’s Circular Economy Strategy encourages industry innovation and makes the US the regional leader as sustainability targets match production-scale solutions.

Water-Based Barrier Coatings Market Dynamics:

Drivers:

-

Increasing Regulatory Emphasis on Sustainable Packaging Accelerates Water-Based Barrier Coatings Market Growth

Water-based barrier coatings market is driven by stringent environmental regulations curbing VOC emissions and encouraging use of biodegradable coatings for compostable packaging applications. Almost 10,000 biobased products are certified by the USDA BioPreferred Program, helping drive increased use. Partnerships, such as Michelman’s bio-based barrier coatings for sustainable packaging, fall within these parameters. All these measures contribute towards getting the water-based barrier coatings companies to increase the share of water-based barrier coatings and facilitate in the transition of barrier coatings industry from environmentally harmful products to eco-friendly and sustainable measures in terms of functionality and consumer demand.

-

Rising Demand for Lightweight and Recyclable Packaging Drives Water-Based Coatings Market Trends

The barrier coatings industry takes advantage of the global drive for lightweight, recyclable packaging that reduces the cost and environmental burden of transportation. Mondi Plc and Stora Enso Oyj create plastic-free alternatives with water-based barrier coatings, which are in line with circular economy targets. The U.S. EPA reports that packaging is nearly 30% of municipal solid waste; it’s hard to argue that sustainable alternatives don’t matter. This trend allows the water-based barrier coatings market to project positive trends and allows for increased water-based barrier coatings market share increase to fiber-based and compostable packaging.

Restraints:

-

High Initial Formulation and Processing Costs Hinder Broader Adoption of Water-Based Barrier Coatings

However, while having long-term advantages, increased foundation and processing expenses inhibit the growth of the water-based barrier coatings market. Investments in sophisticated raw materials and in upgrades to equipment raise upfront costs, locking smaller companies out. There are ongoing energy efficiency concerns in water-based coating processes noted in an article by the U.S. Department of Energy, which contribute to costs. Factors restrictive water-based barrier coatings market penetration especially in budget sensitive sectors, despite the increasing demand for bio-based barrier coatings and Biodegradable Coatings in the barrier coatings market.

Water-Based Barrier Coatings Market Segmentation Analysis:

By Resin Type

Acrylic dominated the water-based barrier coatings market in 2024 with a 36.8% market share attributed to superior flexibility, and processability of the polymers. These coatings are FDA compliant for indirect food contact, help brands convert away from plastic laminates to a recycle-ready paper-based solution and offer ultimate flexographic printability. Commercial acceptance such as Stora Enso’s barrier boards bodes well for the growth in the market for water-based barrier coatings. Increased interest in eco-friendly packaging is driving demand for acrylic, enhancing the strong position acrylic has in the market for barrier coatings as the industry continues to emphasize high-performance and eco-sensitive solutions in food, beverage and specialty packaging applications worldwide.

Biopolymers are the fastest-growing segment with a forecasted CAGR of 7.91% from 2025 to 2032, led by the demand for compostable packaging. Restrictive EU rules on single-use plastics and corporate announcements to phase out fossil-based packaging are driving the demand for PHA and PLA coatings. The trend of replacing traditional plastics with cellulose-based barrier coatings is increasing the demand for water-based barrier coatings, such as those being developed by companies like Melodea. These solutions meet brand sustainability goals and comply with regulations on bio-based materials, according to which biopolymers are a key component within increasingly green-focused packaging markets globally.

By Component

Binder dominated the water-based barrier coatings market in 2024 with a 41.50% share, supported by its essential role in ensuring coating integrity. Water-based binders by BASF improve recyclability and product durability and continue to comply with the food safety requirements. Growth of fiber based packaging for takeaway, and other retail packaging applications has increased the use of the binders, resulting in a greater market share. The need to enhance mechanical properties that eliminates unsafe additives to meet global packaging sustainability standards manufacturers target product weight reduction to achieve market expansion.

Additives are the fastest-growing segment with a forecasted CAGR of 7.84% from 2025 to 2032, due to the demand for functional packaging. Solenis and Omya collaborate on biobased additives for grease resistance and surface integrity. EPA-motivated PFAS restrictions spur safer alternatives, especially in fast-food and bakery packaging. This ground-breaking solution enables compostable and recyclable packaging targets, increases share for water-based barrier coatings, and addresses changing environmental needs and increased demand for value-added coatings that offer performance, sustainability, and regulatory compliance.

By Barrier Type

Water vapor barrier dominated the water-based barrier coatings market in 2024 with a 56.4% share with surge in brand demand for maintaining the freshness. Companies like Kuraray make water-based coatings, making ordinary paper packaging more resistant to moisture, which is popular for snacks and baked goods. FDA approved for food safety and Brand sustainability goals to move from PE laminates to recyclable alternatives. This reinforces water-based barrier coatings market share expansion and resonates with the packaging sustainability agendas across the globe which are fueled by stringent regulations over the plastic packaging waste.

Oil and grease barrier is the fastest growing segment with a forecasted CAGR of 7.18% from 2025 to 2032, due to the rising demand for quick- service food packaging. Mondi and Michelman Unveil Recyclable Barrier Paper Reducing Oil Ingress and Free from PFAs. The European Chemicals Agency’s proposals to restrict harmful substances are making the demand for safer, water-based alternatives boom. These developments reinforce trends in the water-based barrier coatings market that are driving sustainability and food safety in the rapidly expanding takeaway and bakery packaging market globally.

By End-Use Industry

Food and beverage dominated the water-based barrier coatings market in 2024 with a 46.70% share owing to sustainable packaging that is replacing plastic. Companies like Sonoco are making recyclable paperboard products that meet Food and Drug Administration standards, which have been taken up by multi-national food brands in search of greener packaging. Lawmakers are also using their influence to promote adoption through legislation to reduce single-use plastic waste. Combined, these trends help drive water-based barrier coatings market growth and further grow the barrier coatings industry’s role in protecting food and beverages while also giving a boost to recyclability and compostability goals.

Personal care and cosmetics are the fastest-growing segment with a forecasted CAGR of 7.90% from 2025 to 2032, with the demand of premium eco-friendly packaging products. Stora Enso’s barrier boards and Omya’s natural mineral additive substitute for plastics, but provide grease and moisture resistance for cosmetic cartons. The demand is driven by EPA sustainability programs and customer interest in plastic free packing. These developments boost the share of water-based barrier coatings promoting luxury packaging innovation that embodies sustainability as well as meets escalating consumer demands.

Water-Based Barrier Coatings Market Regional Outlook

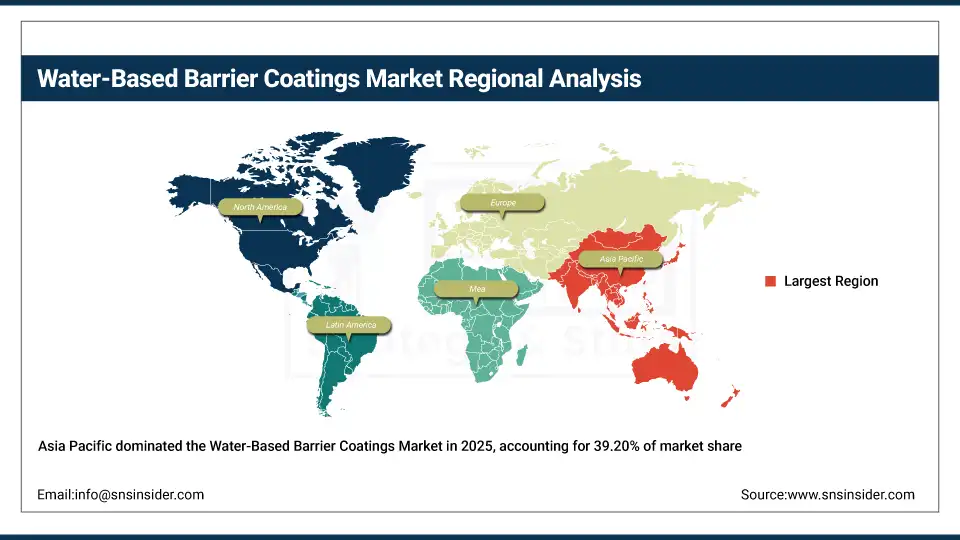

Asia Pacific dominates with 39.20% market share owing to China Ministry of Ecology and Environment promoting bio-based barrier coatings and sustainable paper packaging. South Korea raises the bar for antimicrobial coatings in cosmetics packaging, courtesy the 'Korea Environmental Industry & Technology Institute' India’s packaging laws favoring compostable materials are also gaining market share. These multiple initiatives in Asia Pacific´s largest economies drive water-based barrier coatings market dynamics and strengthen the region’s position as an industry leader in sustainable, biodegradable packaging solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is the fastest-growing region in the water-based barrier coatings market from 2025 to 2032, due to increasing demand for compostable packaging, bio-based barrier coatings, and antimicrobial coatings. The Canadian Packaging Association notes growth in PFAS-free coatings for quick-service packaging, and in Mexico, it is food exports that are driving the switch to biodegradable coatings. Local, collaborative sustainable solutions with the Sustainable Packaging Coalition. The local work focuses on regional collaborations to advance recyclability and innovation across industries, driving the growth of the market while accelerating the shift of the barrier coatings industry away from nonrenewable and less-safe alternatives.

Key Players in the Water-Based Barrier Coatings Market are:

The major water-based barrier coatings market competitors include Michelman, Inc., Solenis, Paramelt B.V., Melodea Ltd, Follmann GmbH & Co. KG, CH-Polymers Oy, Mica Corporation, AQUASPERSIONS Limited, Empowera Technorganics Pvt Ltd, and Siegwerk Druckfarben AG & Co. KGaA.

Recent Developments:

-

In February 2025, Cosmo Specialty Chemicals launched eco-friendly water-based barrier coatings for paper packaging, enhancing recyclability, grease resistance, and compostability to support sustainable packaging goals.

-

In October 2024, Michelman unveiled water-based barrier coatings and PE alternatives at Pack Expo, enabling recyclable fiber-based packaging and meeting rising demand for sustainable, plastic-free packaging solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.93 billion |

| Market Size by 2032 | USD 3.28 billion |

| CAGR | CAGR of 6.87% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Resin Type (Acrylic, Polyethylene (Pe), Polyurethane (Pu), Biopolymers, Epoxy, Others) •By Component (Water, Filler, Binder, Additive) •By Barrier Type (Water Vapor, Oil/Greece, Others) •By End-Use Industry (Food, Beverage, Pharmaceutical, Chemical, Personal Care & Cosmetics, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Michelman, Inc., Solenis, Paramelt B.V., Melodea Ltd, Follmann GmbH & Co. KG, CH-Polymers Oy, Mica Corporation, AQUASPERSIONS Limited, Empowera Technorganics Pvt Ltd, and Siegwerk Druckfarben AG & Co. KGaA. |

Frequently Asked Questions

Strict regulations favor biodegradable coatings, boosting water-based barrier coatings market share and reducing single-use plastics reliance.

Food and beverage packaging, personal care, cosmetics, and specialty paper sectors drive the water-based barrier coatings market growth.

Trends include bio-based barrier coatings, compostable packaging, antimicrobial coatings, and plastic-free recyclable mono-material solutions.

Key water-based barrier coatings companies include Michelman, Solenis, Paramelt, Melodea, Follmann, and CH-Polymers Oy.

The water-based barrier coatings market size was valued at USD 1.93 billion in 2024, showing strong growth potential.

Get in Touch