Water Cut Monitors Market Report Scope & Overview:

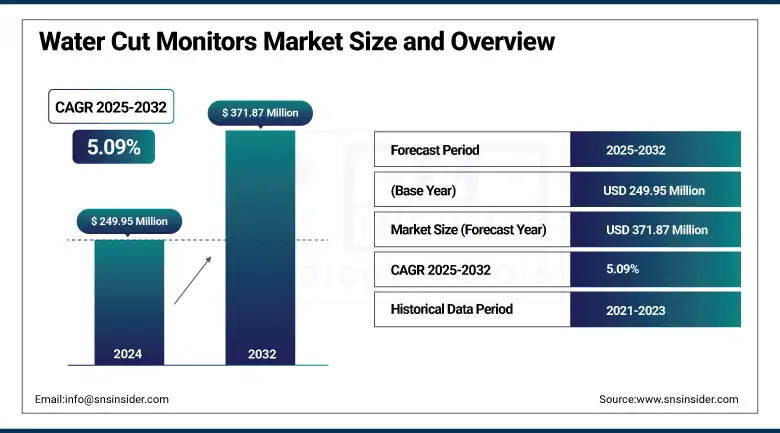

The Water Cut Monitors Market size was valued at USD 249.95 million in 2024 and is expected to reach USD 371.87 million by 2032, growing at a CAGR of 5.09% over the forecast period of 2025-2032.

An increasing interest and the upward trend of this market is observed due to the necessity to ascertain the water content in crude oil in both upstream and downstream operations. This demand has garnered considerable acceptance of the advanced brewing of Water Cut Measurement Systems & Water Cut Detection Equipment by the oil and gas industry. These technologies help to improve the process efficiency of operators, hydrocarbon production, and reduce costs in water handling and disposal. With growing exploration activities and increasing environmental regulations, inline and real-time monitoring systems are becoming common, thereby increasing water cut detection equipment demand and further boosting the water cut meter market.

To Get more information On Water Cut Monitors Market - Request Free Sample Report

Innovations are paving a path for the future of water cut monitors markets. Advanced sensor technology, automation, and integration with digital platforms have all contributed to enhancing the accuracy and reliability of these systems. The creation of non-intrusive, high-performance monitors capable of operating under adverse conditions is helping industries to comply with regulations and cut down costs. Such innovations open doors to smarter and more economical monitoring systems.

Opportunities emerging in the water cut monitors market are across several industrial applications beyond oil, such as in chemical, mining, and water treatment industries. The adoption of automation and data analytics in water cut monitoring offers promising potential to improve overall performance and maintenance aspects. In line with industries moving toward sustainable and cost-saving technologies, a growing demand for high-quality and innovative water cut monitoring solutions is expected to rise steadily.

In March 2024: the Environmental Agency in England and Wales required water companies to install monitors on 7,000 additional emergency overflow pipes by 2025. This aims to increase transparency around sewage discharges, particularly in bathing waters, shellfish areas, and chalk rivers, enhancing environmental monitoring and oversight.

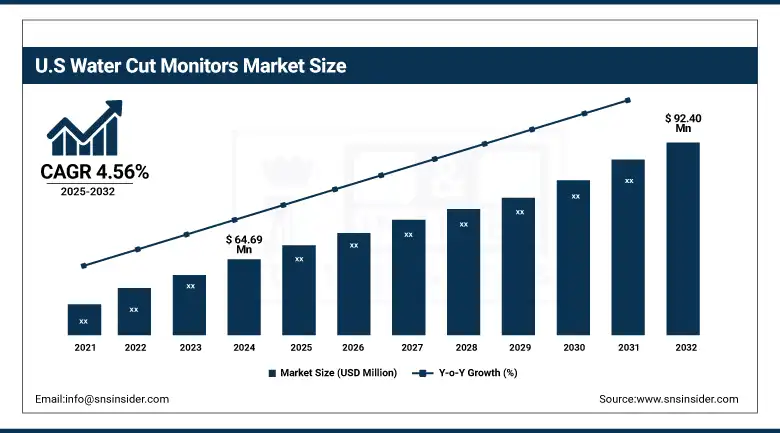

In 2024, the U.S. water cut monitors market is valued at USD 64.69 million, and by 2032, it is projected to reach USD 92.40 million, with a CAGR of 4.56%. This indicates good, steady demand for water cut monitoring technology as the continuing growth of the need for accurate analysis of fluids in the oil and gas sector proliferates. The market in the U.S. is predicted to enjoy steady growth with advancements in technology and the growing emphasis on efficient resource management across different sectors.

Water Cut Monitors Market Dynamics:

Drivers:

-

Technological Advancements and IoT Integration Driving Growth in the Water Cut Monitor Market

Technological advancements and the integration of IoT represent major forces impacting the water cut monitors market trends. The newer sensors have higher accuracy, sensitivity, and stability, which are needed to face the challenging environments upstream in ready oil and gas operations. The use of IoT water cut monitors imparts real-time data acquisition and analysis with remote monitoring, which enhances operational visibility and efficiency. It is used to ensure predictive maintenance, reduction of downtime, and minimizing the costs of equipment failure. Perhaps the major lines of trend driving adoption are shifting toward digital oilfields in which smart technologies will be the nucleus of automation and optimization.

Further developments in wireless communications and cloud analytics continue to accelerate the pace of deployment in IoT-integrated monitoring systems. Whatever the case-category, there is still increasing demand for the newer technologies and connected water cut monitors as companies seek better operational efficiency and compliance with a stricter regime of regulations. This, in a nutshell, is just a reflection of a bigger industry trend toward smarter, greener solutions in resource management.

In November 2024, TotalEnergies revealed its plans to implement real-time methane leak detection systems across all its upstream assets by the end of 2025. This move supports the company’s goal of reaching near-zero methane emissions by 2030, highlighting its dedication to environmental sustainability and adherence to strict regulatory requirements.

-

Stricter Environmental Regulations Drive the Adoption of Advanced Water Cut Monitoring Systems

Adoption of advanced water cut monitoring systems in the oil and gas industries and others is being increasingly propelled by stringent environmental regulations and industry standards. These regulations demand that companies correctly measure the water content in crude oil as high water content can create operational inefficiencies and cause environmental damage. By relying on dependable water cut monitoring instruments, companies can reduce contamination and leakage risks and hence improve environmental safety and sustainability.

Moreover, these state-of-the-art systems allow companies to comply with safety standards that aim to reduce the environmental footprint caused by their operations. In this way, precise monitoring aids the systems in managing resources better, reducing wastage, and optimizing production processes. While environmental concerns take center stage, these technologies are finding rather acute acceptance in water cut monitoring. They serve as a first line of defense in guaranteeing the operator's compliance with regulations, environmental guidelines, and operational efficiency while limiting the negative impact on the environment.

In March 2025: The U.S. Environmental Protection Agency (EPA) is revising wastewater regulations for oil and gas extraction to align with advanced pollution control technologies, emphasizing the role of water cut monitors for compliance and minimizing environmental impact.

Restraints:

-

Impact of Oil Price Volatility on Investments in Water Cut Monitoring Technologies Impede Market Expansion

Oil price fluctuations can greatly influence investments in monitoring technologies, including water cut monitoring systems. When the price of crude is down, oil and gas companies tend to suffer low margins, causing them to curtail capital expenditures. Thus, investment in newly emerging technologies, such as advanced water cut management system, is either delayed or postponed. Such companies might prefer retrofitting an existing piece of equipment rather than acquiring new equipment, which may be inefficient or out of date. This behavior, being cost-driven during a period of price instability becomes one major hurdle for the newer technologies. Older technologies, by being used longer, can never meet up to the promised accuracy and operational effectiveness of the new monitoring systems, thereby adversely affecting production processes in general. So, price volatility in oil is another crucial factor affecting investment patterns in this sector.

In November 2024: Claudio Descalzi, CEO of Eni, expressed concerns about prolonged volatility in oil markets at an industry event in Abu Dhabi. He stated that such instability, driven by OPEC+ supply cuts, could delay investments in new oil and gas production due to uncertainty in price forecasts.

Water Cut Monitors Market Segmentation Outlook:

By Function

The onshore segment dominated the market with more than 62% water cut monitors market share in 2024 as onshore facilities give better accessibility compared to offshore operations for quick deployment and maintenance activities. Additionally, the initial capital expenditures and operating expenditures for onshore projects are usually low, which makes them attractive to investors and operators.

The offshore sector is projected to experience the highest growth rate in the WCM market due to the expansion of offshore exploration and production activities that require higher levels of monitoring in managing the complexities of offshore environments. Offshore facilities require heavy water cut monitors to accurately measure the water content in crude oil, accordingly helping them to operate and manage costs in problematic conditions.

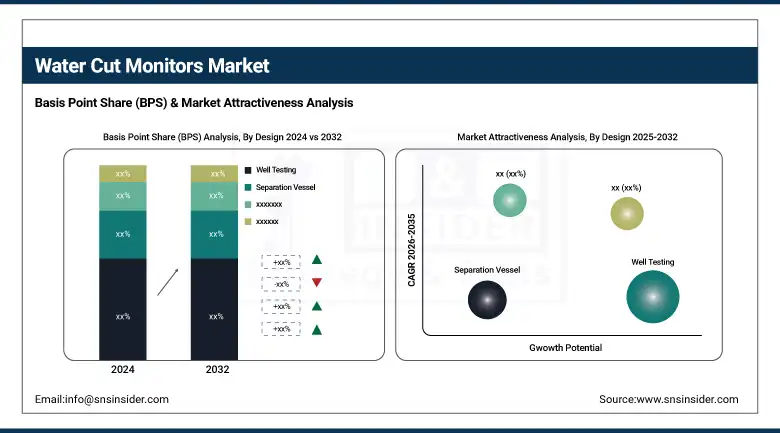

By Design

The Well Testing design segment dominates the water cut monitors market with over 25% share in 2024 owing to its critical role in the early stages of oil, gas exploration, and production. The segment is extensively used to assess reservoir performance, establish production rates, and analyze the nature of fluids being taken out, including water cut. The well-testing procedure should precisely guide an operator to decide on field development and production optimization.

LACT is the fastest-growing segment within the water cut monitors market, emerging from the rising demand for accurate measurement and transfer of hydrocarbons. The need for regulatory compliance, oil custody transfer, and consistent product quality is driving this growth, which is forecasted to witness large-scale expansions between 2024 and 2032.

By Application

The upstream segment dominated the water cut monitors market in 2024, accounting for 64% of the total share. This monopolistic position is due to the rising need for real-time monitoring during E&P (exploration and production) operations. Oil producers require accurate water cut data to ensure maximum recovery of crude oil while limiting the cost of water generation and handling, finally preventing formation damage. With maturing oilfields, water production increases, thus necessitating constant monitoring of the water content in the fluid extracted from the reservoir.

The midstream sector is experiencing the fastest growth in the water cut monitor market. This growth is driven by the need for the measurement of water content in pipelines and storage to guarantee product quality and compliance with regulatory standards. As crude oil and refined products are increasingly traded and transported worldwide, this escalates demand for water cut monitors from the midstream sector, making it the fastest-growing segment.

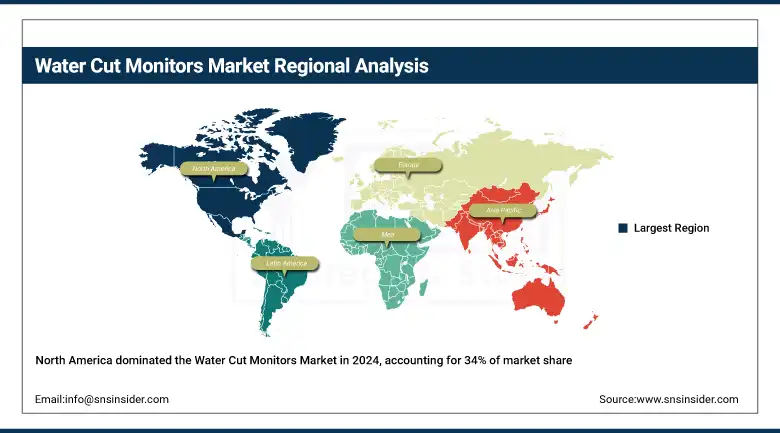

Water Cut Monitors Market Regional Analysis:

North America dominated the water cut monitors market in 2024, capturing 34% of the global market share. This dominance is mainly driven by the region's established oil and gas infrastructure and the early adoption of advanced monitoring technologies in the North America water cut monitors market. A great deal of money has been spent on upstream oilfield automation and real-time monitoring systems in the U.S. to improve production efficiency and lessen operational hazards. Along with the presence of leading market players and an active regulatory framework for the North America water cut monitors market, these factors have further strengthened regional growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is emerging as the fastest-growing water cut monitors market. This trend is the result of various factors, such as growing demand for energy, rapid industrialization, and heavy investments in oil and gas exploration. In this respect, the activities upstream are growing bigger in China and India, where process monitoring is gaining more and more attention.

China and India are dominating the water cut monitors market. Both countries are experiencing rapid industrialization and expanding their upstream oil and gas activities. China, With China making some major investments into energy infrastructure and exploring the oil and gas sector, it stands as a major player in this market. On the other hand, India also sees this market growing because of rising energy demand and global adoption of advanced process monitoring technologies. In their march with the technologies of water cut monitoring, these countries are also driving the overall market growth in this region.

Europe holds a significant share of the water cut monitors market driven by its strong regulatory framework and continued investments in offshore oil and gas exploration. Norway and the U.K. are major contributors, using these monitoring systems for the sake of environmental compliance and efficiency in production. The presence of well-established oilfield service providers, along with a focus on sustainable extraction practices, has led to the growth in demand for accurate water cut measurement technologies.

Water Cut Monitors Companies are:

Lemis Process, AMETEK Inc, Schlumberger Limited, ZelenTech, TechnipFMC, Eesiflo, Agar Corporation, Emerson Electric Co., Sentech AS, and Weatherford.

Recent Developments:

- In February 2024: Drexelbrook launched the Universal V Water Cut Monitor, featuring RF Admittance technology to improve the accuracy of water-in-oil measurement. Designed for high-pressure and high-temperature environments, the device includes a 3-year warranty and minimizes maintenance by resisting paraffin accumulation.

- In July 2024: TechnipFMC secured a major contract from Petrobras to deliver flexible pipes for water injection and gas lift operations in Brazil’s pre-salt fields, with the contract valued between $250 million and $500 million.

- In October 2024: TechnipFMC won an iEPCI contract from BP for the Kaskida project in the Gulf of Mexico, featuring the deployment of 20,000 psi standardized subsea trees and manifolds representing a major leap forward in subsea technology.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 249.95 Million |

| Market Size by 2032 | USD 371.87 Million |

| CAGR | CAGR of 5.09% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Function (Onshore, Offshore) • By Design (Well Testing, Separation Vessel, LACT (Lease Automatic Custody Transfer), Tank Farm & Pipeline, MPFM (Multiphase Flow Meters), Refinery, Others) • By Application (Upstream, Midstream, Downstream) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lemis Process, AMETEK Inc, Schlumberger Limited, ZelenTech, TechnipFMC, Eesiflo, Agar Corporation, Emerson Electric Co., Sentech AS, Weatherford |

Frequently Asked Questions

The North America region dominated the Water Cut Monitors Market in 2024.

The “onshore” segment dominated the Water Cut Monitors Market.

Technological Advancements and IoT Integration Driving Growth in the Water Cut Monitor Market

The Water Cut Monitors Market was USD 249.95 million in 2024 and is expected to reach USD 371.87 million by 2032.

The Water Cut Monitors Market is expected to grow at a CAGR of 5.09% from 2025-2032.

Get in Touch