Web3 Gaming Market Report Scope and Overview:

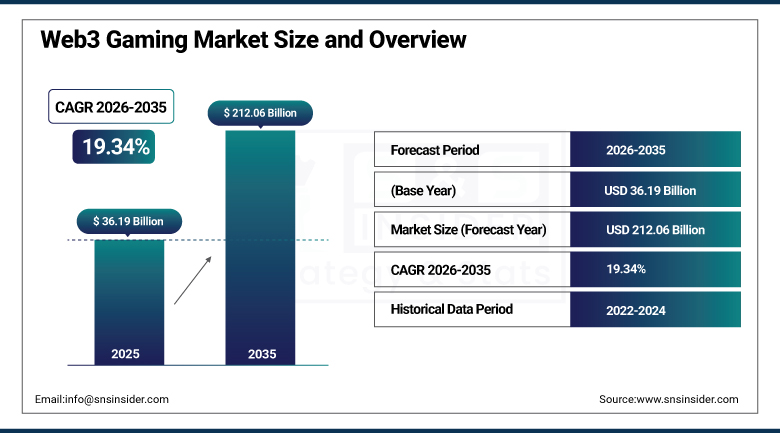

The Web3 Gaming Market was valued at USD 36.19 Billion in 2025 and is projected to reach USD 212.06 Billion by 2035, registering a CAGR of 19.34% from 2026 to 2035.

The growth of the Web3 Gaming Market is fueled by an increased adoption of blockchain technology, increasing popularity of the Play-to-Earn gaming model, and increasing demand for true ownership of digital assets via NFTs. The players are increasingly drawn towards gaming ecosystems which facilitate the secure trade of in-game assets, reward systems using tokens, and virtual economies that work together. The growth of cryptocurrency adoption, the development of smart contracts, and metaverse experiences are driving the growth of the market. Moreover, the increasing investment by game developers, venture capitalists, and blockchain platforms is fueling the development of innovative Web3 games.

In 2024, Telegram's Web3 gaming ecosystem achieved remarkable success as simple clicker games powered by decentralized technologies added 50 million new users to the platform in a single year, demonstrating how accessible, low-friction blockchain gaming experiences could drive genuinely mainstream adoption well beyond crypto-native early adopters.

Market Size and Forecast

-

Market Size in 2026E: USD 43.19 Billion

-

Market Size by 2035: USD 212.06 Billion

-

CAGR: 19.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Web3 Gaming Market - Request Free Sample Report

Web3 Gaming Market Trends

-

Cloud gaming, decentralized identity, and AI integration continue complementing blockchain technology, paving the way for smarter, more adaptive gaming environments.

-

GameFi innovations, including staking and liquidity farming in gaming environments, continue attracting both players and investors to blockchain-based titles.

-

Increasing interoperability across blockchains and real-time trading of NFT assets continue making Web3 games more sophisticated and sustainable.

-

Developers continue moving beyond hype to focus on delivering high-quality gaming experiences with long-term user engagement at the core.

-

Enhanced tokenomics models continue evolving as major developers respond to demand for genuine interoperability and cross-chain asset portability.

U.S. Web3 Gaming Market Outlook

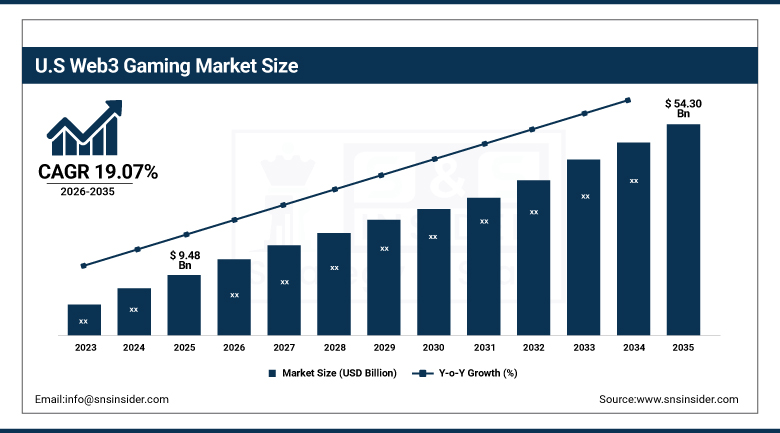

The U.S. Web3 Gaming Market was valued at approximately USD 9.48 Billion in 2025 and is projected to reach approximately USD 54.30 Billion by 2035, registering a CAGR of approximately 19.07% from 2026 to 2035.

The growth of the US market was further supported by the rising popularity of blockchain games, play-to-earn game mechanics, and the players' possession of assets using NFTs. Further venture capital investments and innovations in decentralized technologies contributed to adoption and market development in the long run, with 45% of Web3 gamers in America preferring play-to-earn game mechanics and over 60% of their money spent on in-game purchases originating from income on NFTs and in-game assets. The ability to earn real money and possess assets further distinguished Web3 games from traditional games for the domestic audience.

Immutable continued expanding its Web3 gaming infrastructure and developer tooling throughout 2025, supporting studios building NFT-based and play-to-earn titles on its layer-2 blockchain platform designed specifically to handle high-volume in-game transactions without the gas fees that have historically slowed mainstream Web3 gaming adoption.

Web3 Gaming Market Segment Analysis

-

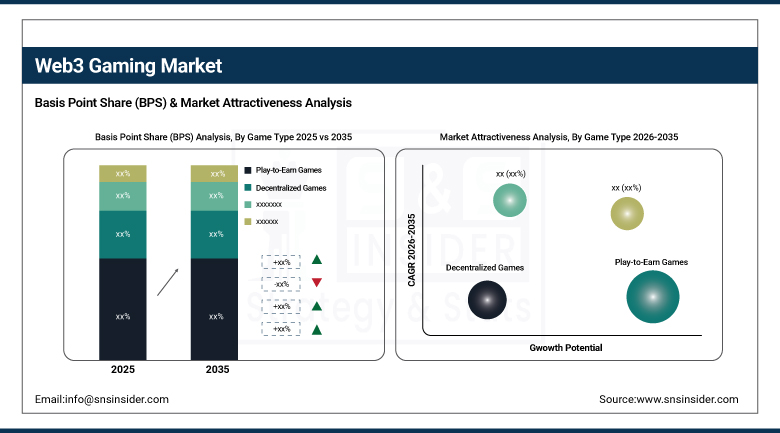

By Game Type, Play-to-Earn (P2E) Games segment dominated the Web3 Gaming Market in 2025 with 42% share; Decentralized Games segment is the fastest growing segment.

-

By Device Type, Mobile segment dominated the market in 2025 with 54% share; VR/AR segment is the fastest growing segment.

-

By End-Use, Casual Gamers segment dominated the market in 2025 with 38% share; Investors/Speculators segment is the fastest growing segment.

-

By Mode, Play-to-Earn (P2E) segment dominated the market in 2025 with 46% share; Hybrid Models segment is the fastest growing segment.

By Game Type, Play-to-Earn (P2E) Games Dominate the Web3 Gaming Market While Decentralized Games Witness the Fastest Growth

The Play-to-Earn (P2E) Games segment dominated the Web3 Gaming Market in 2025 because of the increased popularity in earning digital assets, cryptocurrencies, and blockchain rewards while playing video games. In the P2E gaming models, players are given the choice to own the assets inside the game and earn from their involvement in the games. Increasing popularity of NFTs, decentralized economy, and token rewards has been responsible for the development of various innovative gaming platforms which have been contributing to the growth of the segment.

The Decentralized Games segment is the fastest growing in the Web3 Gaming Market due to the rising adoption of blockchain technology providing transparent transactions, asset ownership, and even decentralized governance of the games. With decentralized games, users can have control over their digital assets and play using decentralized economies through smart contracts. The rising interest in blockchain-enabled gaming experience, peer-to-peer economies, and user-owned virtual worlds fuels the emergence of such games.

By Device Type, Mobile Dominates the Web3 Gaming Market While VR/AR Emerges as the Fastest-Growing Segment

The Mobile segment dominated the Web3 Gaming Market in 2025 due to increased use of smartphones, their accessibility, and blockchain-based mobile gaming applications. Mobile phones give users the ability to play Web3 games without having to invest in costly hardware, thus increasing the number of participants from the mass audience. Integration of digital wallets, mobile payments systems, and user interfaces helped boost the adoption of Web3 games based on mobiles.

The VR/AR segment is the fastest growing in the Web3 Gaming Market due to an increased demand for immersive gaming. Blockchain technology integrated with virtual and augmented realities provides digital ownership of assets, secure transactions, and personalized games. Improvements in VR/AR technologies, metaverses, and digital ecosystems have been motivating developers and players to adopt Web3 virtual reality and augmented reality games.

By End-Use, Casual Gamers Dominate the Web3 Gaming Market While Investors/Speculators Register the Fastest Growth

The Casual Gamers segment dominated the Web3 Gaming Market in 2025 owing to the rising availability of user-friendly blockchain-based games. Game developers are working towards enhancing the user experience as well as keeping the technical aspects simple to attract mainstream gamers. The mobile compatibility, reward-based mechanisms, and ease of onboarding process has motivated casual gamers to engage in Web3 games as they provide users with the scope of having fun along with digital ownership options.

The Investors/Speculators segment is the fastest growing in the Web3 Gaming Market owing to the rising interest in digital assets and virtual economies along with blockchain investment opportunities. The users are becoming a part of gaming ecosystems to buy, trade, and earn money from the valuable in-game assets. Increasing use of NFTs and digital asset markets is promoting investment-driven user engagement.

By Mode, Play-to-Earn (P2E) Dominates the Web3 Gaming Market While Hybrid Models Experience the Fastest Growth

The Play-to-Earn (P2E) segment dominated the Web3 Gaming Market in 2025 owing to the feature of offering monetary incentives in the form of blockchain-based rewards as well as digital asset ownership. Gamers like models that reward them with tokens, NFTs, and other virtual assets during their participation in gaming. The increase in crypto usage, blockchain gaming community growth, and the demand for monetized gaming experience is boosting the popularity of P2E models.

The Hybrid Models segment is the fastest growing in the Web3 Gaming Market as developers are using a combination of traditional gaming experience along with blockchain-based offerings to lure more gamers. The demand for sustainable gaming ecosystem, better user experience, and easy Web3 adoption is compelling developers to adopt hybrid models in emerging blockchain gaming platforms around the world.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.65% |

|

Europe |

United Kingdom |

24.50% |

|

Asia Pacific |

China |

29.70% |

|

Middle East and Africa |

UAE |

27.20% |

|

Latin America |

Brazil |

35.85% |

North America Web3 Gaming Market Insights

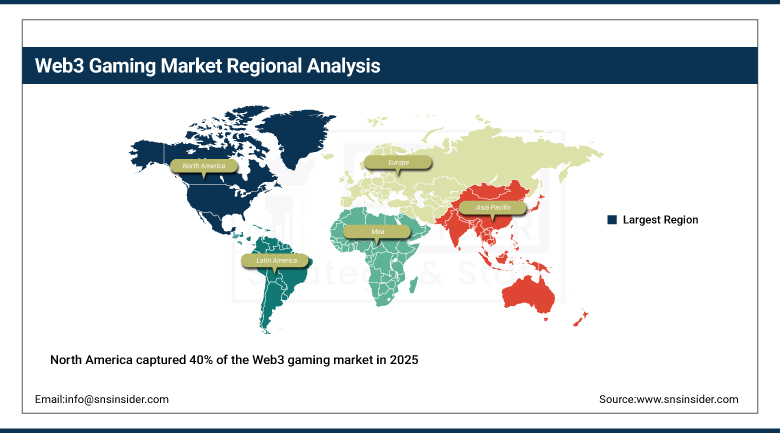

North America captured 40% of the Web3 gaming market in 20245 driven by sophisticated blockchain infrastructure, deep digital expertise, and early decentralizing adoption. Supported by healthy venture capital, experienced game developers, and favorable regulations, the region fostered fast-growing user numbers and creativity, and the play-to-earn game style proved a perfect fit given how many established gamers already influence broader adoption trends.

The United States accounted for roughly 82.65% of regional revenue, anchored by a deep concentration of leading Web3 game studios and blockchain infrastructure providers. Canada added further regional demand through its own growing blockchain gaming developer community, and that combined strength kept North America the largest addressable market for Web3 gaming vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Web3 Gaming Market Insights

Europe held a meaningful share of global revenue, with the continent leading innovation alongside North America and Asia Pacific through gaming start-ups and established tech giants entering the Web3 space. Venture capital funding in blockchain gaming projects surged in recent years across the continent, with major gaming studios adopting token-based economies and decentralized marketplaces.

The United Kingdom led demand at roughly 24.50% of European revenue, supported by London's position as a global fintech and gaming innovation hub. Germany and France contributed substantial additional demand, and continued European venture capital investment in blockchain gaming should keep regional demand climbing steadily through the forecast period.

Asia Pacific Web3 Gaming Market Insights

Asia Pacific is projected to grow at the highest CAGR of 21.27% during 2026 to 2035, on the back of a huge mobile-first gamer base and rising digitalization across the region's largest economies. Soaring smartphone usage, increasing interest in crypto assets, and support from governments in countries including Japan and South Korea remain among the key drivers accelerating regional adoption.

China led the region, accounting for roughly 29.70% of regional revenue, supported by its massive mobile gaming user base and rapidly expanding domestic blockchain infrastructure. Japan and South Korea contributed meaningful additional demand through supportive government policy and mature gaming industries, and Web3 gaming is increasingly being embraced by emerging economies including India and Southeast Asia, driving increased revenue generation with genuinely strong regional growth momentum.

MEA and Latin America Web3 Gaming Market Insights

The Middle East and Africa and Latin America both showed steady growth in Web3 gaming adoption, driven by expanding smartphone penetration, growing interest in cryptocurrency and digital assets, and rising venture capital investment in blockchain gaming startups across both regions. As these markets continued developing modern digital payment and blockchain infrastructure, Web3 gaming adoption grew correspondingly from a considerably smaller base than in more mature gaming markets.

The UAE led Middle East and Africa demand, supported by the country's favorable blockchain regulatory environment and growing gaming startup ecosystem. Saudi Arabia contributed further demand through its own digital entertainment investment programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing cryptocurrency adoption continuing to anchor regional demand for Web3 gaming.

Market Dynamics

Growth Drivers: Rising Distributed Platform Adoption and Player-Owned Economies

Expansion of this market will be driven by the increasing number of distributed systems, player-owned economies, and incorporation of NFTs worldwide. Enhanced engagement, increased blockchain security, and play-to-earn schemes remain attractive for both players and game developers. Growing investments and technological development continue to drive the adoption process and, thus, contribute to the expansion of this market within the larger industry.

Increasing adoption of blockchain games, high demand for player-owned assets, and increasing importance of play-to-earn schemes remain supportive of this factor. Web3 games offer transparency and interoperability that are really attractive for both game developers and players. Adding NFTs and virtual economies by using decentralized finance remains effective in enhancing the engagement of users who play these games.

Restraints: Regulatory Uncertainty and Volatile Token Economics

The changing regulatory approach to cryptocurrency and digital assets in various regions remains an important restraint for the accelerated adoption of these trends, as games development companies, developing titles that will reach the global audience, need to deal with quite inconsistent legal environments in regards to the issues of token issuance, NFT trading, and asset rights of gamers.

Another restraint is connected with the high level of token economics and asset valuations volatility, as players who have had a tough experience with the changes in the valuation of their assets inside the games can become quite skeptical about dedicating more time and money to such gaming models.

Opportunities: Immersive Technology Integration and Emerging Market Expansion

The combination of cloud gaming, decentralized identity, and AI with blockchain is a real chance and would result in a more advanced gaming experience that may help to expand the attractiveness of Web3 gaming outside its current crypto-focused customer base. The companies which would be able to successfully integrate these new technologies and blockchain ownership will be able to gain market share on this rapidly developing frontier.

The acceptance of Web3 gaming among developing countries such as India and Southeast Asia represents another major opportunity, because these regions are responsible for revenue creation through their strong growth rate. The vendors that are ready to offer mobile-first games without much difficulty for users to get into them are going to benefit from the growth of smartphone penetration and interest in cryptocurrencies among gamers.

Recent Developments:

-

2025: Illuvium launched its Overworld 2.0 update, adding enhanced NFT utilities and cross-chain support that let players trade and upgrade collectible characters across multiple blockchains.

-

2024: Sky Mavis continued expanding Axie Infinity's Ronin blockchain ecosystem, adding new game titles and infrastructure improvements aimed at reducing transaction costs for the platform's broader player base.

-

2025: Gala Games continued expanding its ecosystem of interconnected Web3 titles, adding new play-to-earn mechanics and cross-game asset utility across its growing portfolio of blockchain-based games.

Web3 Gaming Market key players are:

-

Animoca Brands

-

Sky Mavis

-

Dapper Labs

-

Immutable

-

Gala Games

-

Splinterlands

-

The Sandbox

-

Enjin

-

Sorare

-

Ultra

-

Mythical Games

-

Fortnite (Epic Games)

-

Star Atlas

-

Illuvium

-

MOBOX

-

Vulcan Forged

-

Chromia

-

Revomon

-

Alien Worlds

-

Big Time

Web3 Gaming Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 36.19 Billion |

| Market Size by 2035 | USD 212.06 Billion |

| CAGR | CAGR of 19.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Game Type (NFT-Based Games, Play-to-Earn Games, Decentralized Games) • By Device Type (PC/Desktop, Mobile, Consoles, VR/AR) • By End-Use (Casual Gamers, Hardcore Gamers, Investors/Speculators, Collectors, Community Builders) • By Mode (Play-to-Earn (P2E), Free-to-Play (F2P), Subscription-Based, Hybrid Models) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Animoca Brands, Sky Mavis, Dapper Labs, Immutable, Gala Games, Splinterlands, The Sandbox, Enjin, Sorare, Ultra, Mythical Games, Fortnite (Epic Games), Star Atlas, Illuvium, MOBOX, Vulcan Forged, Chromia, Revomon, Alien Worlds, Big Time |

Frequently Asked Questions

The Web3 Gaming Market is expected to grow at a CAGR of 19.34% from 2026 to 2035.

The Web3 Gaming Market was valued at USD 36.19 Billion in 2025.

The major growth factor is the rising number of distributed platforms, player-owned economies, and NFT incorporation demand globally.

The Play-to-Earn (P2E) Games segment dominated the Web3 Gaming Market by game type, holding a 42% share in 2025.

North America dominated the Web3 Gaming Market in 2025 with a 40% share of total global market revenue.

Get in Touch