Wood Recycling Market Report Scope & Overview:

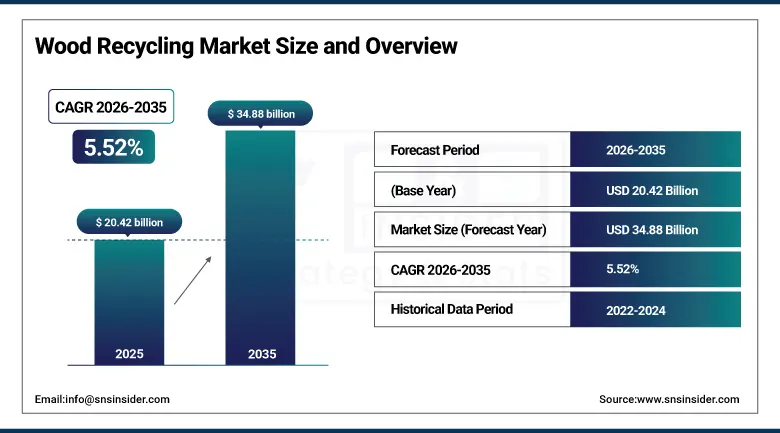

The Wood Recycling Market was valued at USD 20.42 billion in 2025 and is expected to reach USD 34.88 billion by 2035, growing at a CAGR of 5.52% from 2026–2035.

The wood recycling market is witnessing significant growth in the global market due to increasing environmental regulations and circular economy initiatives. Rising demand for sustainable raw materials and biomass energy is driving strong market expansion across multiple sectors. Increasing construction and demolition waste generation is significantly supporting recycling activities. Growing adoption of eco-friendly packaging and engineered wood products is further strengthening demand. Rapid urbanization and industrial expansion are boosting consumption of recycled wood materials worldwide.

Growth Rate Increase for Global wood recycling market as Result of Introduction of Circular Economy Strategies Worldwide. This phenomenon is represented by such companies as Veolia, Waste Management, and Stora Enso, which have increased capacity in recycling wood with the help of new technologies of sorting and biomass conversion. As a result of investments in decentralized recycling plants and AI-based technology of segregation, a significant improvement in recovery rate was achieved, being equal to 15-20 percent.

Market Size and Forecast:

-

Market Size 2026E: USD 21.51 Billion

-

Market Size 2035: USD 34.88 Billion

-

CAGR (2026 - 2035): 5.52%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Wood Recycling Market - Request Free Sample Report

Wood Recycling Market Trends:

-

Rising construction and demolition waste diversion mandates driving wood recycling integration into circular material recovery systems globally

-

Accelerating adoption of automated sorting and AI-based wood segregation systems improving recovery rates by nearly 25 percent

-

Government incentives and landfill taxation policies increasing recycled wood utilization rates across industrial processing hubs by 30 percent

-

Expansion of engineered wood product manufacturing driving demand for recycled feedstock with quality standardization requirements rising sharply

-

Private sector investments in biomass energy and wood waste-to-fuel projects exceeding multi-billion-dollar capacity expansions across 2025

-

Urban circular economy initiatives promoting decentralized wood collection networks reducing landfill leakage rates below 40 percent threshold

U.S. Wood Recycling Market Size Outlook:

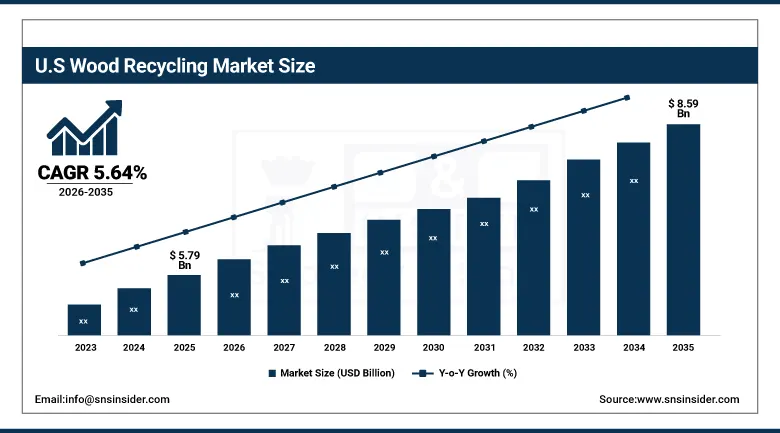

The U.S. Wood Recycling Market was valued at USD 5.79 billion in 2025 and is expected to reach around USD 8.59 billion by 2035, growing at a CAGR of 5.64% from 2026–2035.

The U.S. wood recycling market is witnessing constant growth because of strict environmental regulations and strong circular economy adoption across industries. Wood recycling usage in construction and demolition waste management, biomass energy generation, and industrial material recovery has been responsible for steady market expansion. Increasing investment in sustainable infrastructure development and advanced recycling facilities has led to an increase in demand for such solutions.

According to the U.S. Environmental Protection Agency (EPA), wood in municipal solid waste reached about 18.09 million tons in 2018, representing a significant share of U.S. waste streams, with nearly 3.1 million tons recycled primarily through pallet recovery and reuse applications. The U.S. Forest Service highlights growing emphasis on recovering construction wood and industrial residues to reduce landfill dependency and support circular bioeconomy initiatives. This shift is strengthening the U.S. wood recycling ecosystem through sustainable material recovery practices.

Wood Recycling Market Segment Analysis:

-

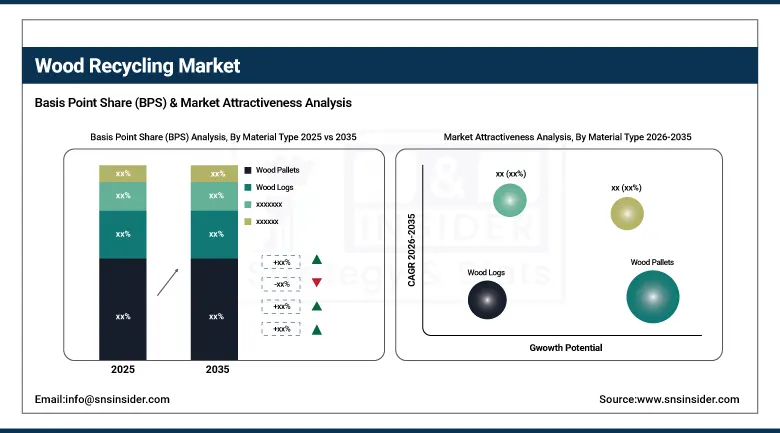

By Material Type, wood pallets dominated the wood recycling market with 34.25% share in 2025; while construction and demolition wood are the fastest growing segment with CAGR of 7.39% during 2026 to 2035.

-

By Application, particle board and MDF dominated the wood recycling market with 32.80% share in 2025; while bioenergy is the fastest growing segment with CAGR of 9.63% during 2026 to 2035.

-

By End Market, packaging industry dominated the wood recycling market with 30.60% share in 2025; while furniture industry is the fastest growing segment with CAGR of 7.78% during 2026 to 2035.

By Material Type, wood pallets dominated the wood recycling market, while construction and demolition wood are the fastest growing segment.

Wood Pallets was the dominant player in the wood recycling market with maximum revenue market share in 2025. This is due to the extensive use of wooden pallets in logistics, warehouses, and supply chain management. High availability of waste wood pallets along with effective reverse logistics systems ensures high recycling volume. Additionally, high demand from packaging and shipping sectors has added to the recovery rate. Ease of recycling processes and low costs are the key reasons behind this being the most commercially profitable segment in the wood recycling industry.

Construction & Demolition Wood is anticipated to register fastest CAGR over the forecast period from 2026 to 2035. Growing urbanization and massive infrastructure reconstruction projects globally have been driving growth in this market segment. Rising production of construction waste results in high availability of waste wood feedstock. Government incentives to divert waste material from landfills have also boosted adoption. Recycling of construction waste wood into bioenergy products, engineered wood and sustainable building materials has been driving growth in this segment.

By Application, particle board and MDF dominated the wood recycling market, while bioenergy is the fastest growing segment.

Particle Board and MDF category is anticipated to capture dominated market share in the wood recycling market with revenue contributions in 2025. Particle board and MDF are popular due to their extensive application in furniture manufacturing and interior purposes. The use of recycled wood is more efficient in terms of costs and consistent quality. Sustainability of construction materials and restrictions on the use of virgin wood will contribute to increased usage of particle boards and MDF.

Bioenergy category is projected to register the fastest CAGR during 2026-2035 owing to increasing demand for renewable energy sources around the world. Recycled wood can be utilized in the process of generating biomass power as well as in other applications such as in industrial heating processes. Clean energy transition and growth in investments towards waste-to-energy facilities will accelerate the trend of using recycled wood in bioenergy applications.

By End Market, packaging industry dominated the wood recycling market, while furniture industry is the fastest growing segment.

Packaging Industry segment had the dominated revenue share in 2025. The major driver responsible for leading market position is the high demand for recycled wood in the manufacturing of pallets, crates, and protective packages. Growing demand for sustainable packaging material coupled with the need for cost-effective substitutes of virgin wood will drive adoption in packaging industry. Trade activities and circular packaging initiatives will continue to drive wide-spread use of recycled wood in packaging sector.

Furniture Industry segment is projected to exhibit fastest CAGR during forecast period, i.e. 2026–2035. Key drivers behind the projected fast growth include increasing demand for sustainable and eco-friendly furniture products manufactured using recycled wood materials. Urbanization and growth in residential and commercial constructions will lead to higher consumption of furniture products. Trends towards modularity and customization in furniture products along with sustainability certification will drive demand for recycled wood. Increasing demand for sustainable interior decoration products will fuel the growth of recycled wood in the furniture segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

81.35% |

|

Europe |

Germany |

27.20% |

|

Asia Pacific |

China |

38.60% |

|

Middle East & Africa |

UAE |

16.80% |

|

Latin America |

Brazil |

44.10% |

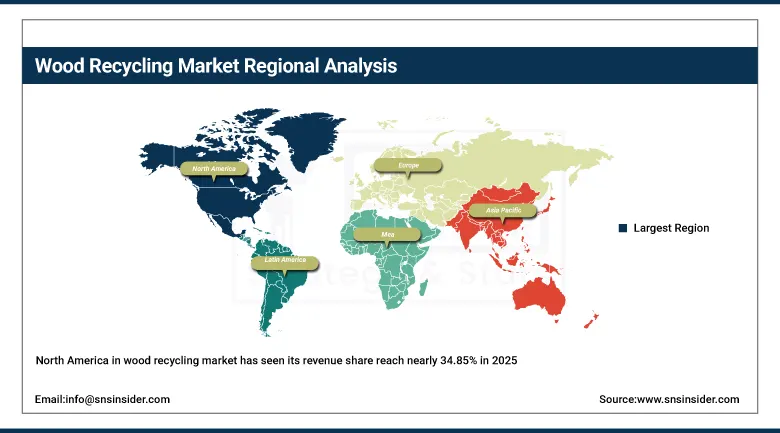

North America Wood Recycling Market Insights.

North America in wood recycling market has seen its revenue share reach nearly 34.85% in 2025 due to strong waste management systems and recycling infrastructure development. The region benefits from advanced collection networks, industrial recycling facilities, and high adoption of circular economy practices. Increasing demand for sustainable raw materials in packaging, construction, and biomass energy is driving steady growth across the United States and Canada. Expanding environmental regulations and corporate sustainability targets are further supporting market expansion.

The market for wood recycling in North America is highly dependent on the circular economy framework and recovery of municipal solid waste recycling. The U.S. EPA reported that in 2018, the U.S. produced 18.09 million tons of wood waste, out of which 17.1% was recycled, including wooden pallets and packaging. Wood packaging alone accounted for 3.1 million tons of waste recycled.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Wood Recycling Market Insights.

The Europe wood recycling market makes an important mark in the year 2025 owing to strong sustainability regulations and circular economy policies. Countries like Germany, France, United Kingdom, and Italy are leading contributors to regional demand. High focus on renewable materials, bioenergy production, and sustainable construction practices is supporting consistent market expansion. Increasing investments in recycling infrastructure and strict waste diversion targets are strengthening wood recovery systems across industrial and municipal sectors.

According to European Environment Agency, around 44% of total EU waste is recycled, with recovery rates reaching 61.4% in 2022 (EEA). Eurostat data shows that waste recovery has increased by over 40% since 2004. EU waste directives and circular economy policies are accelerating wood waste recovery, supporting resource efficiency and reducing landfill dependency across construction and bioenergy applications.

Asia Pacific Wood Recycling Market Insights.

Asia Pacific is well positioned for growth in the wood recycling market in 2025 with a CAGR of around 6.80% because of rapid industrialization and urban construction activities. China, India, Japan, and Southeast Asian countries are key contributors. Rising construction and demolition waste generation, along with increasing demand for sustainable materials, is boosting recycling adoption. Expanding biomass energy projects and growing manufacturing capacity are further strengthening market development across the region.

The Asia Pacific wood recycling market is expanding steadily due to rising construction waste recovery and government-led circular economy policies across China, Japan, and India. According to FAO forestry statistics, Asia-Pacific generates ~250 million m³ of logging residues annually, with only ~25 million m³ economically utilized, highlighting major recycling potential. FAO also reports mill residues of ~61 million m³ from sawmilling and plywood sectors.

Middle East & Africa and Latin America Wood Recycling Market Insights.

The Middle East & Africa region along with Latin America is expected to have steady growth in the wood recycling market in 2025 due to increasing urbanization and waste management initiatives. The UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging contributors. Growth in construction activities, packaging demand, and environmental sustainability programs is supporting gradual expansion of recycling systems across these developing economies.

Current trends show that wood recycling through waste-to-resource strategies is gaining momentum in MENA & Africa and Latin America due to an increase in waste generated from construction projects. According to a report by the World Bank, the MENA region produces more than 155 million tons of waste per year, which will almost double in 2050, with 83% being recyclable. The Latin American construction and furniture industries produce about 9% of wood waste reuse possibilities.

Market Dynamics:

Growth Drivers: Growth in Construction and Demolition Waste Generation Driving Large-Scale Wood Recycling Activities

With rapid urbanization and infrastructure growth, the amount of construction and demolition waste generated has increased substantially on a global level. There is a large amount of wood available from demolition waste that can be recycled into various products. Renovation operations are another factor responsible for the increase in demand for recyclable wood. Improved technology for separation and processing is resulting in enhanced efficiency. Growing government regulations to prevent landfill dumping are driving the growth of recycled wood product demand.

Based on the Indian Government’s information on Open Government Data (OGD) portal, construction and demolition waste generation is officially monitored across states, where multiple cities have recorded high quantities of C&D waste generated due to urbanization and development. Swachh Bharat Mission Urban projects have shown that almost 50% of C&D waste collected gets recycled to make bricks, blocks, pavers and aggregates. Increasing construction projects have boosted the amount of wood being recovered and recycled

Restraints: Lack of Standardized Waste Collection Systems and Quality Inconsistency Restricting Market Efficiency

Inconsistency in the waste collection and separation process among various regions affects the efficiency of wood recycling. Quality inconsistency and contamination by paints, chemical substances, and adhesives affect the recyclability of wood. The insufficient development of waste management practices among developing countries makes it difficult for recycling to happen. Lack of awareness regarding appropriate segregation of waste among companies and consumers has an adverse effect on wood recovery.

Opportunities: Expansion of Bioenergy and Renewable Power Generation Creating Strong Demand for Recycled Wood Feedstock

Increasing trend towards renewables opens great prospects in terms of the use of recycled wood for the production of bioenergy. Growing numbers of investments in biomass-based power plants have resulted in high demand for wood chips and recycled products. The governments stimulate the introduction of renewable energy technologies by applying various incentives and measures aimed at carbon emissions reduction. The use of wood wastes as a cost-efficient fuel is also becoming more widespread among industrial enterprises.

Growing amounts of investment in bioenergy and renewables are increasing the demand for wood recycling as one of the main sources of material for power generation. In the words of the IEA, current modern bioenergy already provides more than 55% of renewable energy in the world and is expected to grow significantly up until 2030, as a result of the needs of energy decarbonization. One of the pillars of the renewable energy system of the EU includes biomass as a renewable energy source.

Recent Developments:

-

2026: Veolia Environnement advanced GreenUp circular economy strategy through expanded UK municipal waste contracts and integration of AI-enabled recycling infrastructure alongside stakeholder engagement forums.

-

2025: ALBA Group strengthened recycling operations in Germany, expanding plastics recovery, e-waste processing and AI-enabled sorting facilities.

-

2025: Biffa plc enhanced UK recycling capabilities, expanding electric fleet adoption and developing advanced materials recovery facilities nationwide.

-

2024: DS Smith agreed acquisition by International Paper, strengthening sustainable packaging and circular fibre recycling capabilities across Europe.

Wood Recycling Market Key Players are:

-

Veolia Environnement

-

Waste Management Inc.

-

Republic Services

-

Waste Connections

-

REMONDIS SE & Co. KG

-

ALBA Group

-

Interzero

-

FCC Environment

-

Casella Waste Systems

-

Cleanaway Waste Management

-

Biffa plc

-

Renewi plc

-

Reworld Waste (formerly Covanta)

-

DS Smith

-

Smurfit Westrock

-

Stora Enso

-

UPM-Kymmene Corporation

-

Mondi Group

-

Sappi Limited

-

Kronospan

Wood Recycling Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.42 Billion |

| Market Size by 2035 | USD 34.88 Billion |

| CAGR | CAGR of 5.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Wood Pallets, Construction and Demolition Wood, Wood Logs, Wood Chips) • By Application (Paper and Pulp, Particle Board and MDF, Bioenergy, Construction Materials, Chemicals and Materials) • By End Market (Packaging Industry, Furniture Industry, Construction Industry, Paper Industry) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Veolia Environnement, Waste Management Inc., Republic Services, Waste Connections, REMONDIS SE & Co. KG, ALBA Group, Interzero, FCC Environment, Casella Waste Systems, Cleanaway Waste Management, Biffa plc, Renewi plc, Reworld Waste (formerly Covanta), DS Smith, Smurfit Westrock, Stora Enso, UPM-Kymmene Corporation, Mondi Group, Sappi Limited, Kronospan. |

Frequently Asked Questions

The wood recycling market is expected to grow at a CAGR of 5.52% from 2026 to 2035.

The wood recycling market was valued at USD 20.42 billion in 2025.

Increasing construction and demolition waste generation, along with circular economy initiatives and rising demand for biomass energy and sustainable raw materials, is driving market growth.

Wood pallets led the wood recycling market in 2025 due to their extensive use in logistics, warehousing, and high recycling availability from reverse supply chains.

North America led the wood recycling market in 2025 due to strong recycling infrastructure, advanced waste management systems, and high adoption of circular economy practices.

Get in Touch