AI Supercomputer Market Report Scope & Overview:

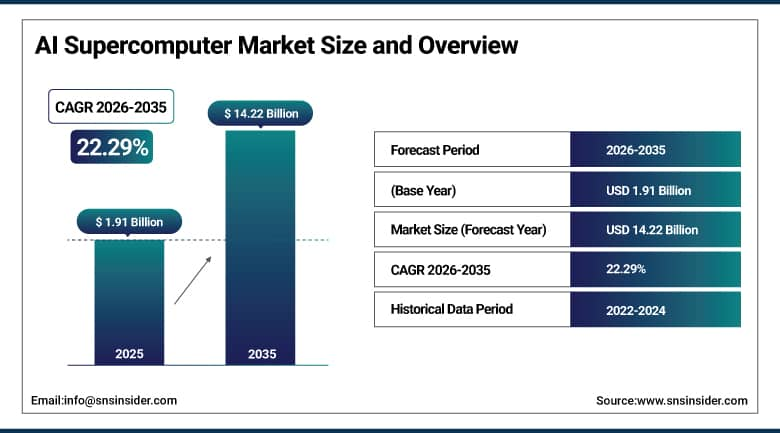

The AI Supercomputer Market was valued at USD 1.91 billion in 2025 and is expected to reach USD 14.22 billion by 2035, growing at a CAGR of 22.29% from 2026-2035.

AI Supercomputer Market is growing due to increasing adoption of AI and deep learning across industries, rising demand for high-performance computing to process massive datasets, and expansion of cloud-based AI solutions. Continuous investments in research, generative AI, autonomous systems, and advanced scientific simulations are driving the need for faster, efficient, and scalable AI supercomputing infrastructure, fueling significant market growth during the forecast period.

AWS announced an investment of up to USD 50 billion starting in 2026 to build AI supercomputing infrastructure for U.S. government customers across secure cloud regions, strengthening national-scale AI and HPC capabilities.

AI Supercomputer Market Size and Forecast

-

AI Supercomputer Market Size in 2025: USD 1.91 Billion

-

AI Supercomputer Market Size by 2035: USD 14.22 Billion

-

CAGR: 22.29% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On AI Supercomputer Market - Request Free Sample Report

AI Supercomputer Market Trends

-

Rising demand for high-performance computing in AI, deep learning, and big data analytics is driving the AI supercomputer market.

-

Growing adoption across research institutions, data centers, and cloud service providers is boosting market growth.

-

Expansion in industries like healthcare, automotive, finance, and defense is fueling deployment.

-

Increasing focus on accelerated training, inference, and large-scale simulations is shaping adoption trends.

-

Advancements in GPUs, TPUs, and specialized AI accelerators are enhancing computing power and efficiency.

-

Rising investments in AI research, autonomous systems, and predictive modeling are supporting market expansion.

-

Collaborations between supercomputer manufacturers, AI developers, and technology providers are accelerating innovation and global adoption.

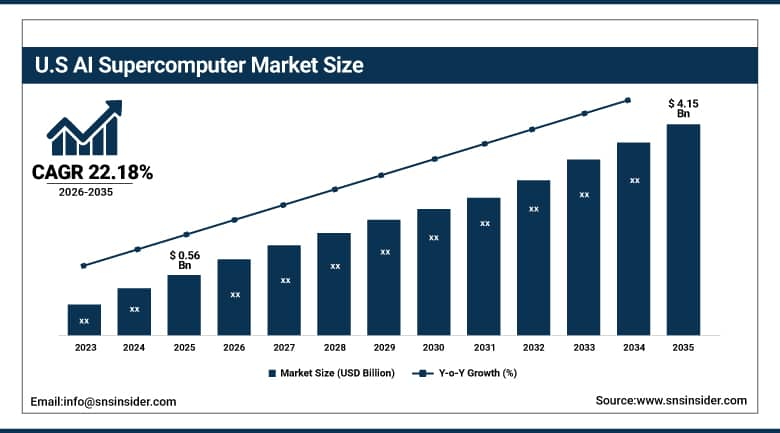

The U.S. AI Supercomputer Market was valued at USD 0.56 billion in 2025 and is expected to reach USD 4.15 billion by 2035, growing at a CAGR of 22.18% from 2026-2035.

U.S. AI Supercomputer Market is growing due to strong government and private sector investments, widespread adoption of AI across industries, advanced research initiatives, and increasing demand for high-performance computing to support deep learning and complex AI workloads.

The U.S. Department of Energy’s Office of Science allocated USD 23 million through ORNL’s New Frontiers program to advance energy-efficient post-exascale supercomputers targeting 2029 and beyond.

AI Supercomputer Market Growth Drivers:

-

Rising demand for advanced AI workloads and deep learning applications driving AI supercomputer adoption across various industries globally

AI supercomputers are increasingly deployed due to growing requirements for processing complex AI workloads, including deep learning, machine learning, and neural network models. Industries such as healthcare, finance, automotive, and research heavily rely on large-scale computation to generate insights, simulations, and predictive models. The increasing adoption of generative AI and autonomous technologies further fuels the need for high-performance computing infrastructure. Organizations are prioritizing AI supercomputers for faster computation, parallel processing of millions of parameters, and enhanced model accuracy, which strengthens the market growth and adoption globally over the forecast period.

DOE’s Frontier supercomputer delivers exascale performance with 1.1 exaflops of sustained capability for AI, machine learning, and data analytics across human health and manufacturing applications, while Intel Labs continues to advance responsible AI research focused on transparency, security, and human–AI collaboration for neural workloads.

AI Supercomputer Market Restraints:

-

Complex integration and maintenance requirements of AI supercomputers slowing large-scale deployment across enterprises

AI supercomputers involve sophisticated hardware, software, and networking components that require specialized knowledge for installation, integration, and ongoing maintenance. Organizations need skilled personnel to optimize performance, manage large datasets, and ensure seamless operation across heterogeneous computing environments. Lack of trained professionals and technical expertise poses challenges for enterprises attempting large-scale deployment. Integration with existing IT infrastructure can be complicated, time-consuming, and costly. Regular updates, firmware upgrades, and troubleshooting add further complexity. These operational challenges restrict smooth adoption and scalability, slowing down market growth despite increasing demand for high-performance AI computing solutions across industries.

AI Supercomputer Market Opportunities:

-

Growing adoption of cloud-based AI supercomputing services providing scalable, cost-effective solutions worldwide

Cloud deployment of AI supercomputers enables organizations to access scalable, high-performance computing resources without significant upfront investment. It reduces infrastructure and maintenance costs while supporting real-time processing of massive datasets and rapid AI model deployment. Cloud-based platforms also improve collaboration across geographies and accelerate innovation. Industries such as healthcare, finance, automotive, and research leverage these capabilities to enhance computational efficiency, improve model performance, and gain a competitive edge in advanced AI and deep learning applications.

-

Reflecting this momentum, Microsoft Azure hosts AI supercomputers powering services such as OpenAI’s ChatGPT, with more than 60,000 customers using Azure AI to drive automation and productivity.

-

Google Cloud’s A3 supercomputers, built on NVIDIA H100 GPUs, deliver up to 26 exaFLOPS of AI performance, significantly reducing training time and costs for large machine learning models.

-

Additionally, Google Kubernetes Engine running on the AI Hypercomputer enables clusters of up to 65,000 nodes, reducing generative AI serving costs by 30%, cutting tail latency by 60%, and improving throughput by 40%, underscoring the scalability and efficiency advantages of cloud-based AI supercomputing.

AI Supercomputer Market Segment Highlights

-

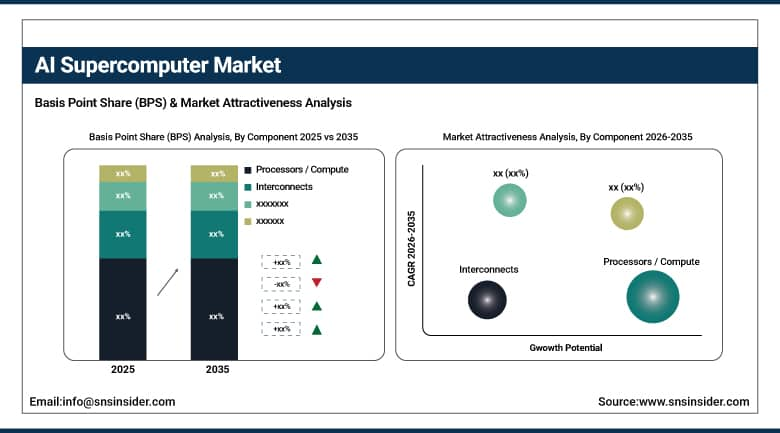

By Component, Processors / Compute dominated with ~44% share in 2025; Interconnects fastest growing (CAGR).

-

By Application, Government dominated with ~38% share in 2025; Commercial fastest growing (CAGR).

-

By End-User, Government & Public Sector dominated with ~29% share in 2025; Healthcare & Life Sciences fastest growing (CAGR).

-

By Deployment Type, Cloud dominated with ~61% share in 2025; Cloud fastest growing (CAGR).

AI Supercomputer Market Segment Analysis

By Component, Processors / Compute dominates the AI Supercomputer Market, Interconnects are expected to grow fastest

Processors / Compute segment dominated the AI Supercomputer Market in 2025 due to its ability to handle complex AI workloads, including deep learning, neural network training, and large-scale simulations. High-performance CPUs and GPUs enable faster computation, efficient parallel processing, and improved model accuracy, making it the preferred choice across industries.

Interconnects segment is expected to grow at the fastest CAGR from 2026-2035 as organizations increasingly demand seamless communication between heterogeneous computing resources. Advanced interconnects reduce latency, enhance data transfer speed, and enable efficient scaling of AI supercomputing systems, supporting high-performance workloads and emerging AI applications, driving rapid adoption across commercial and research sectors.

By Application, Government dominates the AI Supercomputer Market, Commercial applications are expected to grow fastest

Government segment dominated the AI Supercomputer Market in 2025 due to extensive investments in defense, cybersecurity, scientific research, and large-scale simulations. Governments require high-performance AI computing infrastructure to process massive datasets, improve national security, and accelerate technological innovation, making this sector the leading adopter of AI supercomputers worldwide.

Commercial segment is expected to grow at the fastest CAGR from 2026-2035 owing to the rising adoption of generative AI, autonomous technologies, computer vision, and drug discovery applications. Enterprises are leveraging AI supercomputers to enhance operational efficiency, accelerate innovation, and gain competitive advantage in data-intensive commercial applications.

By End-User, Government & Public Sector dominates the AI Supercomputer Market, Healthcare & Life Sciences are expected to grow fastest

Government & Public Sector segment dominated the AI Supercomputer Market in 2025 as public institutions invest heavily in research, defense, and cybersecurity projects. The need for large-scale data processing, simulations, and AI-based decision-making drives substantial adoption, positioning this segment as the primary end-user of AI supercomputing solutions.

Healthcare & Life Sciences segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing demand for AI-powered drug discovery, genomics research, disease modeling, and personalized medicine. High-performance computing enables faster processing of complex biological datasets, supporting innovation and precision healthcare applications worldwide.

By Deployment Type, Cloud dominates the AI Supercomputer Market, Cloud deployment is expected to grow fastest

Cloud segment dominated the AI Supercomputer Market in 2025 due to its ability to offer scalable, flexible, and cost-effective high-performance computing infrastructure. Organizations benefit from reduced operational costs, easy deployment, and on-demand access to powerful AI resources without heavy upfront investment. It is expected to grow at the fastest CAGR from 2026-2035 as increasing adoption of AI-as-a-service, remote collaboration, and cloud-based AI workloads drives demand for scalable, efficient, and easily managed supercomputing solutions globally.

AI Supercomputer Market Regional Analysis

North America AI Supercomputer Market Insights

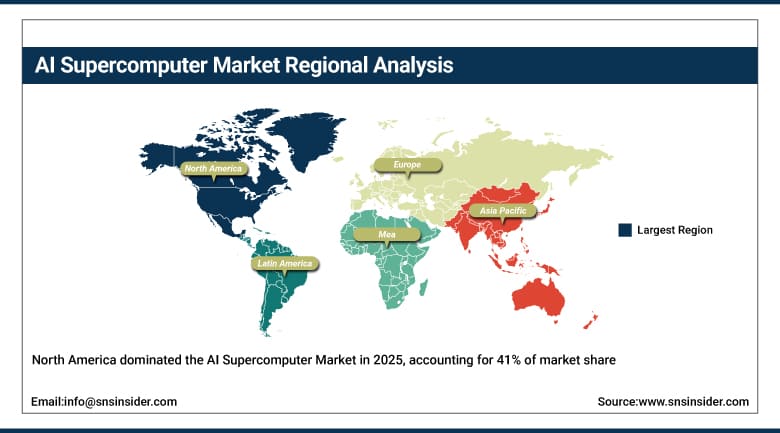

North America dominated the AI Supercomputer Market with the highest revenue share of about 41% in 2025 due to the presence of major technology companies, advanced research institutions, and substantial government and private sector investments in AI infrastructure. Early adoption of high-performance computing, strong funding for AI research, and widespread integration of AI technologies across industries contributed to the region’s leading position in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI Supercomputer Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 23.71% from 2026-2035 owing to increasing investments in AI research, expanding technology adoption, and government initiatives supporting high-performance computing. Rapid industrialization, growing demand for AI-driven applications in healthcare, finance, and autonomous systems, and the entry of key AI supercomputer vendors in emerging markets are driving accelerated growth in the region during the forecast period.

Europe AI Supercomputer Market Insights

Europe in the AI Supercomputer Market is witnessing steady growth due to strong government funding for research, adoption of AI in scientific and industrial applications, and presence of advanced technology infrastructure. Investments in high-performance computing for healthcare, defense, and climate modeling, along with collaborations between academic institutions and enterprises, are driving demand for AI supercomputing solutions across the region.

Middle East & Africa and Latin America AI Supercomputer Market Insights

Middle East & Africa and Latin America in the AI Supercomputer Market are witnessing growth due to increasing government investments, adoption of AI technologies, and expanding research activities. Rising demand for high-performance computing in industries such as healthcare, finance, defense, and smart city initiatives is driving the adoption of AI supercomputers across both regions during the forecast period.

AI Supercomputer Market Competitive Landscape:

NVIDIA Corporation

NVIDIA Corporation is a global leader in GPU and AI computing, driving innovation in high-performance computing, AI model training, and data center acceleration. The company develops hardware and software solutions enabling large-scale AI, scientific research, and generative AI applications. NVIDIA’s supercomputing platforms integrate advanced chip architectures and AI frameworks, cementing its leadership in powering exascale and trillion-parameter AI workloads.

-

2023: Announced the DGX GH200 AI supercomputer, linking 256 Grace Hopper Superchips into a 1‑exaflop system for giant generative AI model training.

-

2024: Revealed that nine supercomputers worldwide using Grace Hopper Superchips deliver 200 exaflops of AI computing, accelerating research in climate, science, and generative AI.

-

2025: Announced the Blackwell‑powered DGX SuperPOD AI supercomputer with 11.5 exaflops for generative AI and trillion‑parameter model training.

IBM Corporation

IBM Corporation is a pioneer in enterprise IT, cloud computing, AI, and quantum computing. Its hybrid approach integrates classical and quantum systems for high-performance and AI workloads, enabling advanced research, simulation, and AI model development. IBM focuses on scalable AI supercomputing solutions to support enterprises and research institutions in scientific computing, generative AI, and large-scale model training.

-

2024: IBM’s quantum system will integrate with the Fugaku supercomputer at Japan’s RIKEN Center, advancing hybrid quantum-HPC AI workflows.

-

2025: Partnered with CoreWeave to deliver a GB200-powered AI supercomputer for training IBM’s Granite AI models at supercomputing scale.

Hewlett Packard Enterprise (HPE)

HPE is a global IT infrastructure company providing servers, storage, networking, and AI-optimized supercomputing solutions. HPE focuses on turnkey systems, enterprise AI, and high-performance computing, collaborating with technology partners to accelerate generative AI, scientific research, and exascale computing. Its solutions integrate cutting-edge hardware and AI frameworks for public and private cloud supercomputing.

-

2023: Introduced a turnkey AI supercomputing solution powered by NVIDIA GH200 Grace Hopper Superchips for generative AI training.

-

2024: Delivered the Aurora exascale supercomputer with Intel and DOE, capable of AI-accelerated science with >10 exaflops mixed precision.

-

2025: Deepened NVIDIA integration for Private Cloud AI and expanded Blackwell support to accelerate enterprise AI supercomputing workloads.

Dell Inc.

Dell Technologies provides end-to-end IT infrastructure, cloud solutions, and AI-optimized hardware for enterprise computing. Its focus on AI integration spans data centers to edge computing, enabling scalable deployment of machine learning, generative AI, and supercomputing workloads. Dell combines advanced GPUs, storage, and networking to accelerate enterprise AI adoption while ensuring operational efficiency and performance.

-

2024: Launched the Dell AI Factory with NVIDIA infrastructure, speeding AI deployment from data center to edge.

-

2025: Enhanced the Dell AI Factory with new enterprise AI solutions and expanded Blackwell Ultra GPU infrastructure.

Key Players

-

IBM Corporation

-

Hewlett Packard Enterprise (HPE)

-

Dell Inc.

-

Fujitsu Limited

-

Lenovo

-

Atos SE

-

NEC Corporation

-

Penguin Solutions

-

INSPUR Co., Ltd.

-

Intel Corporation

-

Advanced Micro Devices (AMD)

-

Huawei Technologies

-

Google LLC

-

Meta Platforms Inc.

-

Amazon Web Services (AWS)

-

Samsung Electronics

-

Oracle Corporation

-

Micron Technology

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.91 Billion |

| Market Size by 2035 | USD 14.22 Billion |

| CAGR | CAGR of 22.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Processors / Compute, Storage, Memory, Interconnects) • By Deployment Type (Cloud, On-Premises) • By Application (Government, Academia & Research, Commercial) • By End-User (Government & Public Sector, Healthcare & Life Sciences, Automotive & Transportation, Finance & Banking, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, IBM Corporation, Hewlett Packard Enterprise (HPE), Dell Inc., Fujitsu Limited, Lenovo, Atos SE, NEC Corporation, Penguin Solutions, INSPUR Co., Ltd., Intel Corporation, Advanced Micro Devices (AMD), Cerebras Systems, Huawei Technologies, Google LLC, Meta Platforms Inc., Amazon Web Services (AWS), Samsung Electronics, Oracle Corporation, Micron Technology |

Frequently Asked Questions

The AI Supercomputer Market is expected to grow at a CAGR of 22.29% globally from 2026 to 2035, driven by increasing AI adoption.

The AI Supercomputer Market was valued at USD 1.91 billion in 2025, reflecting growing investments in high-performance computing and AI infrastructure.

Rising adoption of AI, deep learning, generative AI, and demand for high-performance computing across industries are the primary factors driving market growth.

The Processors / Compute segment dominated the AI Supercomputer Market due to its ability to handle complex AI workloads efficiently across industries.

North America dominated the AI Supercomputer Market in 2025 due to major technology companies, strong research infrastructure, and significant government and private investments.

Get in Touch