Aircraft Actuator Market Report Scope & Overview:

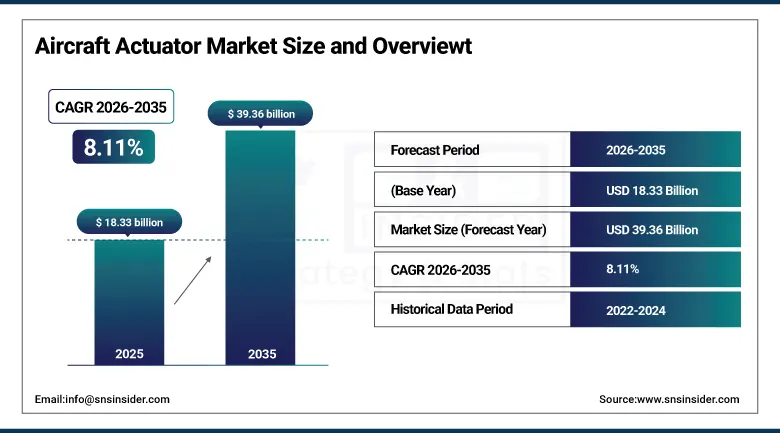

The Aircraft Actuator Market was valued at USD 18.33 Billion in 2025 and is expected to reach USD 39.36 Billion by 2035, growing at a CAGR of 8.11% from 2026 to 2035.

Aircraft actuators form the basic movement architecture that is responsible for flight critical and other mechanical functions on every type of contemporary aircraft. Whether it is wing flap actuation, landing gear actuation, thrust reversers, brake actuation, or environmental control, actuators ensure reliable and redundant movement in all directions, using hydraulic, electrical, or pneumatic sources. However, the market for actuators is witnessing a revolutionary transition due to the changing approach of the entire aerospace industry towards replacing traditional hydraulic power architectures with electrical and electro-hydrostatic actuator systems, which provide greater advantages of weight savings, reduced maintenance costs, better system monitoring capability, and lower lifetime costs.

Parker Hannifin Corporation, a global leader in motion and control technologies, reported full-year fiscal 2024 revenues of USD 19.96 Billion across its Aerospace Systems and Diversified Industrial segments, with its Aerospace Systems segment identifying actuation and flight control systems as sustained growth priorities supported by commercial aircraft production rate recovery and expanding defense platform content value per aircraft.

Market Size and Forecast

-

Market Size in 2026E: USD 19.52 Billion

-

Market Size by 2035: USD 39.36 Billion

-

CAGR: 8.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Aircraft Actuator Market - Request Free Sample Report

Aircraft Actuator Market Trends

-

Growing adoption of electro-mechanical and electro-hydrostatic actuators is driven by more-electric aircraft initiatives, offering lower weight and maintenance requirements than hydraulic systems.

-

Recovery in Airbus and Boeing aircraft production rates is increasing actuator demand across flight control, landing gear, and thrust reverser applications.

-

Expansion of UAV and unmanned aircraft markets is boosting demand for lightweight, compact, and digitally integrated actuator solutions.

-

Rising defense modernization programs are driving demand for high-reliability actuator systems in advanced military aircraft and transport platforms.

-

Integration of digital health monitoring and predictive maintenance is improving actuator reliability, reducing downtime, and extending service intervals.

The U.S. Aircraft Actuator Market Outlook

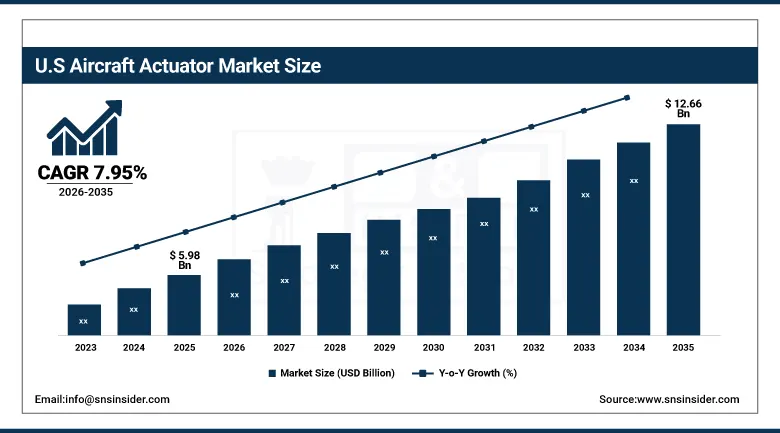

The U.S. Aircraft Actuator Market was valued at USD 5.98 Billion in 2025 and is expected to reach USD 12.66 Billion by 2035, growing at a CAGR of 7.95%.

The United States is the single largest domestic aircraft actuator market in the world, due to the unique combination of its commercial aviation fleet size, military aircraft expenditure, and location of the most advanced manufacturers of aerospace original equipment. The commercial aviation market in the United States operates over 7,500 mainline and regional aircraft within its airline network, ensuring an uninterrupted cycle of actuator sales for both new deliveries and aircraft MRO services. No other domestic market in the world comes close in terms of aircraft actuator purchase volumes.

Moog Inc. reported fiscal year 2024 revenues of USD 3.31 Billion, with its Aircraft Controls segment achieving strong performance driven by F-35 flight control actuator production, commercial aircraft flight control system deliveries, and growing space vehicle actuation program content.

Aircraft Actuator Market Segment Analysis

-

By Type, hydraulic actuators dominated the market with 30.45% share in 2025, while electro-hydrostatic actuators (EHA) are the fastest growing type with the highest CAGR of 9.36% from 2026 to 2035.

-

By Technology, hydraulic actuation systems dominated the market with 48.75% share in 2025, while electrical actuation systems are the fastest growing technology with the highest CAGR of 8.57% from 2026 to 2035.

-

By Application, flight control systems dominated the market with 35.41% share in 2025, while engine control systems are the fastest growing application with the highest CAGR of 9.40% from 2026 to 2035.

-

By Platform, commercial aircraft dominated the market with 45.16% share in 2025, while military aircraft is the fastest growing platform segment with the highest CAGR of 7.57% from 2026 to 2035.

By Type, hydraulic actuators dominate the aircraft actuator market, while electro-hydrostatic actuators (EHA) are the fastest-growing segment.

Hydraulic Actuators segment dominated the market with the highest revenue share of approximately 30.45% in 2025 due to their established position across legacy and in-production commercial and military aircraft platforms where hydraulic power distribution infrastructure is already integrated into the aircraft's fundamental architecture. The reliability record, force density advantages, and long-term maintenance ecosystem surrounding conventional hydraulic actuators continue to support their specification across new aircraft platforms in applications where hydraulic power remains the primary aircraft power source. The global installed base of hydraulically-powered commercial and military aircraft operating across multi-decade service lifespans create a substantial aftermarket actuator replacement demand stream that sustains hydraulic actuator revenue volumes independent of new platform production activity.

Electro-Hydrostatic Actuators (EHA) segment is estimated to register the highest CAGR of 9.36% during the forecast period of 2026–2035 owing to the critical role EHA systems play in the aerospace industry's more electric aircraft transition by combining hydraulic power efficiency and force density with self-contained local power conditioning that eliminates the need for centralized hydraulic circuit routing. EHA systems offer lower hydraulic fluid usage, reduced leak risk, improved monitoring, and weight savings, making them attractive for next-generation commercial and military aircraft focused on reducing maintenance costs and improving operational efficiency.

By Technology, hydraulic actuation systems dominate the aircraft actuator market, while electrical actuation systems are the fastest-growing segment.

Hydraulic Actuation Systems segment dominated the market with the largest revenue share of approximately 48.75% in 2025 attributed to their fundamental integration across the world's commercial and military aircraft fleets where hydraulic power has served as the primary actuation energy source for more than seven decades. The force density, reliability, and failure tolerance characteristics of hydraulic actuation systems make them the specification of choice for safety-critical primary flight control applications where actuation force margins, system redundancy, and failure mode predictability are paramount design requirements. Continued production of Airbus A320, Boeing 737 MAX, Airbus A350, and Boeing 787 aircraft is sustaining demand for hydraulic actuation systems across flight control applications.

Electrical Actuation Systems segment is projected to witness the fastest CAGR of 8.57% during 2026–2035 due to the compelling weight reduction, maintenance efficiency, and digital integration advantages that electro-mechanical and electro-hydrostatic actuation approaches offer for new aircraft platform designs operating under increasingly stringent operating cost and environmental performance requirements. The growing adoption of electric actuation architectures across business jet platforms, regional jet designs, urban air mobility vehicles, and advanced UAV systems is accelerating the electrical actuation system supply chain maturity and manufacturing cost reduction trajectory that is progressively improving the economic case for broader electrical actuation adoption across commercial and military aircraft segments.

By Application, flight control systems dominate the aircraft actuator market, while engine control systems are the fastest-growing segment.

Flight Control Systems segment dominated the aircraft actuator market with the highest revenue share of 35.41% in 2025 due to the fundamental criticality of primary and secondary flight control actuation to aircraft safety, performance, and handling quality across all operating conditions and failure scenarios. The combination of high actuator counts per aircraft, stringent reliability and redundancy requirements, high per-unit content value, and the non-discretionary nature of flight control actuator replacement in the maintenance and overhaul cycle creates a structurally stable and high-value application segment that benefits from both new aircraft production and the vast commercial aviation fleet maintenance demand base.

Engine Control Systems segment is projected to register the highest CAGR of 9.40% during the forecast period of 2026–2035 owing to the increasing complexity of next-generation turbofan and turboprop engine variable geometry, thrust management, and nacelle actuation systems that require sophisticated, high-precision actuators capable of operating in the extreme temperature and vibration environment of modern high-bypass turbofan engines. Growing adoption of next-generation engine platforms including the CFM LEAP, Pratt & Whitney GTF, and GE9X series, combined with expanding UAV propulsion system actuator requirements, is driving significant engine control system actuator content value growth.

By Platform, commercial aircraft dominates the aircraft actuator market, while military aircraft is the fastest-growing segment.

Commercial Aircraft segment dominated the aircraft actuator market with the highest revenue share of approximately 45.16% in 2025 owing to the unprecedented scale of the global commercial aviation fleet, the sustained recovery in narrow-body and wide-body aircraft production rates following the post-pandemic order backlog drawdown, and the high-value actuator content per aircraft across flight control, landing gear, thrust reverser, and auxiliary systems applications. The combined Airbus and Boeing order backlog of over 13,000 commercial aircraft representing approximately seven to eight years of current production rates at both manufacturers creates a structural demand visibility for commercial aircraft actuator suppliers that enables long-cycle supply chain investment and capacity planning.

Military Aircraft segment is projected to witness the fastest CAGR of 7.57% during the forecast period of 2026–2035 due to escalating defense budgets across NATO member nations, Asia Pacific treaty allies, and Middle Eastern strategic partners driving accelerated procurement of fifth-generation fighter aircraft, next-generation military transport platforms, and advanced rotary-wing systems incorporating sophisticated fly-by-wire flight control actuation architectures. Expanding F-35 program deliveries, Eurofighter Typhoon and Dassault Rafale export programs, and emerging sixth-generation combat aircraft development programs across the United States, United Kingdom, and Japan are contributing incremental high-value actuator content demand across the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.40% |

|

Europe |

Germany |

26.14% |

|

Asia Pacific |

China |

37.64% |

|

Middle East & Africa |

UAE |

30.45% |

|

Latin America |

Brazil |

46.29% |

North America Aircraft Actuator Market Insights

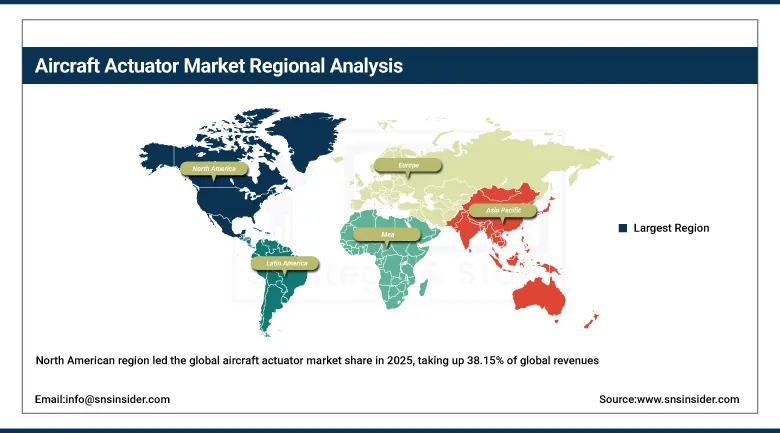

The North American region led the global aircraft actuator market share in 2025, taking up 38.15% of global revenues, where the United States captured 85.40% of regional revenues. This can be attributed to the unique conglomeration of the highest concentration of commercial aircraft manufacturing, defense aerospace prime contractors, and tier-one actuation systems suppliers that characterize the North American aerospace industrial base as the largest and most technologically advanced in the world. The United States acts as the host country for the most significant aircraft actuator programs globally, comprising Boeing's commercial narrowbody and widebody manufacturing programs in Washington and South Carolina, the Lockheed Martin F-35 production facilities in Fort Worth, Texas, and a comprehensive MRO and aftermarket program for the largest commercial air fleet in the world.

Canada supplements demand in the region due to its aerospace manufacturing center located primarily in the Greater Montreal region, consisting of Bombardier's business jet and commercial aircraft programs, major Tier 1 aerospace component manufacturing facilities, and the North American aftermarket support network for Pratt & Whitney Canada turboprop and turbofan engine programs. The Bombardier Global 7500 and Challenger 3500 business jet platforms include fly-by-wire flight control actuation systems and advanced engine nacelle actuation systems.

The U.S. aerospace and defense industry generates more than USD 900 billion annually in economic impact, with commercial aircraft manufacturing and defense aerospace procurement collectively representing the world's single largest demand center for advanced aircraft actuation systems and flight control technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Aircraft Actuator Market Insights

Europe sustained its position as the world's second-largest aircraft actuator market in 2025, accounting of global revenues, supported by the Airbus production ecosystem concentrated in Toulouse, Hamburg, and Seville that drives the world's highest commercial aircraft production rate as measured in deliveries, alongside a deeply established defense aerospace industrial base spanning France, the United Kingdom, Germany, Italy, and Spain that sustains demand for military aircraft actuation systems across a broad portfolio of in-production and development programs. The Airbus A320neo family, A330neo, and A350 XWB programs collectively represent the world's highest-volume advanced actuation system demand environment for commercial aircraft, with production rates supported by an order backlog extending well beyond 2030 across all three platform families.

The European defense aerospace sector, led by Dassault Aviation's Rafale export campaign, the Eurofighter Typhoon's multinational production program, and the UK-led Global Combat Air Programme representing Europe's most ambitious sixth-generation fighter development effort, creates a sustained military aircraft actuation demand stream that complements commercial sector growth. France's Safran group and the United Kingdom's Meggitt and Ultra Electronics operations are among the leading European actuation system technology developers with significant global market presence across both commercial and defense applications.

Europe's aerospace and defense industry contributes over EUR 250 billion annually in revenues, with the Airbus manufacturing network alone procuring actuation system components from over 1,500 tier-one and tier-two European suppliers across its commercial and military aircraft programs.

Asia Pacific Aircraft Actuator Market Insights

Asia Pacific is the fastest-growing regional aircraft actuator market at a CAGR of 8.83% through 2035, accounting for 24.11% of global revenues in 2025. The country China holds the highest proportion in the Asia-Pacific region due to being the fastest-growing commercial aviation market in the world, hence resulting in considerable demand for actuation systems for imported Airbus A320 Family and Boeing 737 MAX commercial airplanes supplied to China as well as domestic actuation systems for COMAC C919 narrow body and C929 widebody development programs that are gradually building up the commercial aircraft manufacturing capability in China.

There is well-established aerospace manufacturing capability in Japan and South Korea where companies have entrenched themselves within the Boeing and Airbus commercial aviation programs as major suppliers of structural and systems components in 787 and 777X commercial planes that involve a large number of actuators. The rising investment in the Australian defense aerospace due to the increase in the number of F-35 fighter jets along with a sovereign defense industry policy is contributing to regional actuator demand.

China's commercial aviation fleet is projected to grow to over 9,000 aircraft by 2035, creating one of the world's largest single-country aircraft actuation system aftermarket demand pools and driving significant Boeing and Airbus delivery-driven actuator procurement volumes through the forecast period.

MEA & Latin America Aircraft Actuator Market Insights

In addition, the Middle East and Latin American regions form key commercially valuable markets for aircraft actuators, with substantial growth potential driven by fleet expansion plans for the Gulf-based airlines, military modernization spending in the region, and ongoing development of commercial aviation infrastructure in the emerging markets of Latin America. In particular, the United Arab Emirates, accounting for a leading share of regional revenues for Middle East and Africa, attributes its market dominance to fleet expansion plans for the Emirates, Etihad, and flydubai airlines, which, altogether, have made some of the largest orders for wide-body and narrow-body aircraft worldwide.

The UAE's aviation sector managed over 118 million passengers in 2024, with Emirates and Etihad maintaining combined fleet orders exceeding 400 wide-body aircraft representing one of the world's largest aggregated commercial aircraft actuation system procurement commitments within the Middle East market.

Market Dynamics

Growth Drivers: Commercial aircraft production recovery and more electric aircraft transition

However, the recovery of aircraft manufacturing production rates for both Airbus and Boeing companies after the pandemic-related disruption, in addition to order books covering production for seven to eight years into the future, is leading to the creation of the strongest positive demand environment ever seen by aircraft actuator systems in the history of the aviation industry. The trajectory of ramp-ups of production rates for Airbus A320neo, A350, Boeing 737 MAX, and 787 airframes will lead to a structural growth of the market of primary flight controls, landing gear, thrust reverser, and auxiliary actuators, benefiting all qualifying actuator system suppliers.

Restraints: Supply chain capacity constraints and qualification certification lead times

The unprecedented recovery in terms of production rate is creating enormous pressure on the capacity of the global supply chain for the aircraft industry, with the actuator system manufacturers experiencing the same difficulties in accessing raw materials, hiring specialized labor, expanding manufacturing capabilities, and securing long lead time electronics components, all of which restricts the ability to increase production rates. Certification by the FAA and the EASA can drag qualification to a period ranging from two to five years, making it very difficult for small firms to compete in the aircraft electrification domain due to the technology integration challenges involved.

Opportunities: UAV market expansion and digital health monitoring integration

Unmanned aerial vehicles (UAVs) have experienced explosive adoption within industries ranging from commercial to governmental and defense, and as a result, there is now a demand stream for aircraft actuators that has fundamentally different technology priorities and purchase timing from traditional manned aircraft actuation. Actuator systems designed to be highly integrated, light-weight, compact, and capable of interfacing with a digital bus are finding success among both fixed-wing and rotary-wing unmanned aircraft used in agricultural management, inspections, package delivery, maritime surveillance, and tactical military operations.

Recent Developments:

-

2025: Parker Hannifin Corporation completed the integration of Meggitt PLC's actuation product lines into its Aerospace Systems segment, expanding its electro-mechanical and hydraulic actuation system portfolio for both commercial and defense aircraft applications with combined engineering resources across North America and Europe.

-

2025: Moog Inc. was awarded a contract to supply electro-hydrostatic actuation systems for the U.S. Air Force's Next Generation Air Dominance program, marking one of the most significant new military aircraft flight control actuation content awards in the defense aerospace sector.

-

2026: Collins Aerospace, a subsidiary of RTX Corporation, announced the launch of its next-generation integrated electro-mechanical actuator family incorporating embedded health monitoring and predictive maintenance capability targeting commercial narrow-body and wide-body aircraft flight control applications.

-

2026: Safran S.A. expanded its electro-hydrostatic actuator production capacity at its Pitstone, UK and Massy, France facilities to support increasing demand from Airbus next-generation platform programs and growing export military aircraft actuation system content commitments.

Aircraft Actuator Market Key Players are:

-

Moog Inc.

-

Parker Hannifin Corporation

-

Collins Aerospace

-

Safran S.A.

-

Honeywell International Inc.

-

Woodward Inc.

-

Liebherr-Aerospace

-

Eaton Corporation

-

Curtiss-Wright Corporation

-

Crane Aerospace & Electronics

-

Meggitt PLC

-

Triumph Group Inc.

-

Ametek Inc.

-

Sitec Aerospace GmbH

-

Arkwin Industries Inc.

-

Electromech Technologies

-

Microtecnica S.r.l.

-

Kyntronics Inc.

-

Nook Industries Inc.

-

AeroControlex Group

Aircraft Actuator Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.33 Billion |

| Market Size by 2035 | USD 39.36 Billion |

| CAGR | CAGR of 8.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Linear Actuators, Rotary Actuators, Electro-Mechanical Actuators (EMA), Electro-Hydrostatic Actuators (EHA), Hydraulic Actuators, Pneumatic Actuators) • By Technology (Hydraulic Actuation Systems, Electrical Actuation Systems, Hybrid Actuation Systems (Hydro-Mechanical / Electro-Hydraulic)) • By Application (Flight Control Systems, Landing Gear Systems, Engine Control Systems, Thrust Reversers, Cabin & Interior Systems, Utility & Secondary Systems (doors, flaps, brakes support systems)) • By Platform (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, UAVs / Drones) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Moog Inc., Parker Hannifin Corporation, Collins Aerospace, Safran S.A., Honeywell International Inc., Woodward Inc., Liebherr-Aerospace, Eaton Corporation, Curtiss-Wright Corporation, Crane Aerospace & Electronics, Meggitt PLC, Triumph Group Inc., Ametek Inc., Sitec Aerospace GmbH, Arkwin Industries Inc., Electromech Technologies, Microtecnica S.r.l., Kyntronics Inc., Nook Industries Inc., AeroControlex Group. |

Frequently Asked Questions

The aircraft actuator market is expected to grow at a CAGR of 8.11% from 2026 to 2035.

The aircraft actuator market was valued at USD 18.33 Billion in 2025.

Key growth drivers include recovering Airbus and Boeing aircraft production rates, increasing actuator demand across critical systems, and the aerospace industry's shift toward more-electric aircraft, accelerating adoption of electro-mechanical and electro-hydrostatic actuators.

Electro-Hydrostatic Actuators (EHA) are the fastest-growing type in the aircraft actuator market, with a CAGR of 9.36% from 2026 to 2035.

North America dominated the aircraft actuator market in 2025, holding 38.15% of global revenues, with the United States accounting for 85.40% of North American revenues.

Get in Touch