Autonomous Aircraft Market Report Scope & Overview:

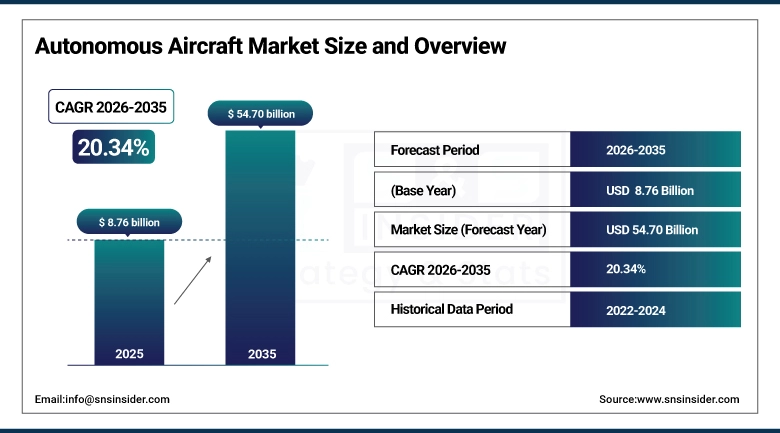

The Autonomous Aircraft Market was valued at USD 8.76 billion in 2025 and is expected to reach USD 54.70 billion by 2035, growing at a CAGR of 20.34% from 2026–2035.

The Autonomous Aircraft Market is witnessing strong expansion driven by the rapid integration of artificial intelligence in flight control systems, increasing defense modernization programs focused on unmanned and autonomous combat and surveillance platforms, and the rising demand for advanced air mobility solutions including eVTOL aircraft and autonomous cargo delivery systems. The growing emphasis on reducing pilot dependency, enhancing operational efficiency, and improving mission safety is further accelerating the adoption of autonomous aviation technologies across both military and commercial sectors.

Supporting this trend, regulatory and industry bodies such as the Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) have been actively advancing frameworks for unmanned aircraft systems (UAS) integration into controlled airspace, including structured testing corridors and certification pathways for autonomous flight operations, which is directly accelerating commercialization readiness across North America and Europe.

In parallel, major aerospace OEMs including Boeing, Airbus, and defense-focused innovators such as Lockheed Martin and Northrop Grumman have significantly expanded investment into AI-enabled autonomous flight programs, while companies like Joby Aviation and Archer Aviation are advancing urban air mobility platforms, reinforcing the transition toward scalable autonomous aviation ecosystems globally.

Autonomous Aircraft Market Size and Forecast

-

Market Size in 2025: USD 8.76 Billion

-

Market Size by 2035: USD 54.70 Billion

-

CAGR: 20.34% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Autonomous Aircraft Market - Request Free Sample Report

Autonomous Aircraft Market Trends

-

Rapid adoption of AI-enabled autonomous flight systems is improving navigation accuracy and in-flight decision-making.

-

Growing deployment of UAVs and autonomous platforms is expanding ISR, surveillance, and combat capabilities.

-

Rising development of eVTOL and hybrid VTOL aircraft is accelerating urban air mobility and autonomous logistics.

-

Increasing use of sensor fusion (LiDAR, radar, optical) is enhancing obstacle detection and flight safety.

-

Expansion of AI-based avionics and edge computing is strengthening real-time autonomous flight performance.

-

Rising OEM–defense collaboration is accelerating testing, certification, and deployment of autonomous aircraft systems.

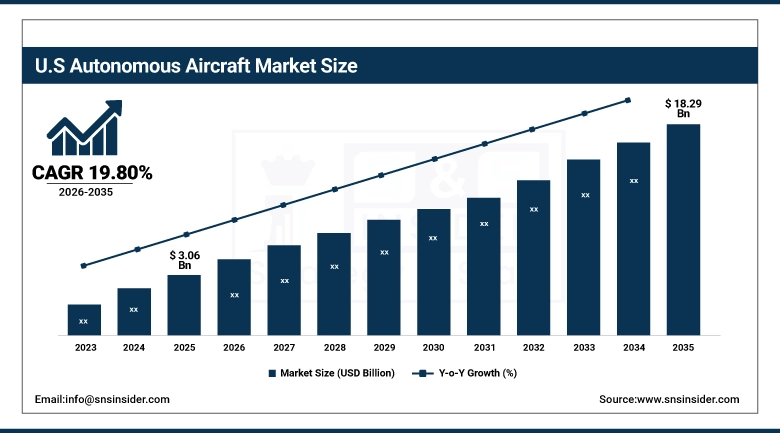

The U.S. Autonomous Aircraft Market was valued at USD 3.06 billion in 2025 and is expected to reach around USD 18.29 billion by 2035, growing at a CAGR of 19.80% from 2026–2035.

The US ranks first in the global market for autonomous aerial vehicles because of its robust programs of defense modernization, adoption of AI-based drones, and existence of leading aerospace OEMs like Boeing, Lockheed Martin, and Northrop Grumman. Ongoing growth in autonomous ISR, combat drones, and advanced air mobility projects is helping consolidate its market leadership position.

Supporting this growth, the Federal Aviation Administration (FAA) is actively advancing integration frameworks for unmanned aircraft systems (UAS) into national airspace, including expanded BVLOS (Beyond Visual Line of Sight) approvals and certification pathways for autonomous operations.

In parallel, sustained investments from the U.S. Department of Defense (DoD) under programs like Collaborative Combat Aircraft (CCA) and autonomous swarm drone initiatives are accelerating real-world deployment and scaling of AI-driven autonomous aviation technologies across military operations.

Autonomous Aircraft Market Segment Highlights

-

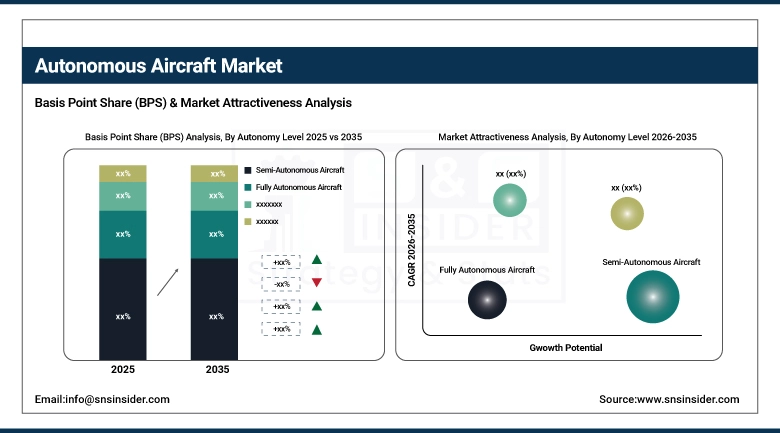

By Autonomy Level, Semi-Autonomous Aircraft dominated the Autonomous Aircraft Market with 41.36% share in 2025; Fully-Autonomous Aircraft are fastest growing CAGR

-

By Platform Type, UAVs / Drones dominated the Autonomous Aircraft Market with 34.15% share in 2025; Hybrid VTOL / eVTOL Aircraft are fastest growing CAGR

-

By Application, Defense & Military dominated the Autonomous Aircraft Market with 48.85% share in 2025; Logistics & Delivery Services are fastest growing CAGR

-

By Technology, Artificial Intelligence (AI) & Machine Learning Systems dominated the Autonomous Aircraft Market with 30.24% share in 2025; Edge Computing & Real-Time Data Processing are fastest growing CAGR

-

By End User, Defense Forces & Military Organizations dominated the Autonomous Aircraft Market with 49.51% share in 2025; Logistics & E-commerce Companies are fastest growing CAGR

By Autonomy Level, Semi-Autonomous Aircraft dominates the Autonomous Aircraft Market, Fully-Autonomous Aircraft expected to grow fastest

In 2025, the Semi-Autonomous Aircraft segment maintained its dominant position in the Autonomous Aircraft Market, accounting for 41.36% of total revenue. This form of leadership is due to its high level of integration with military UAVs and commercial flights test programs, where human-in-the-loop control systems guarantee increased operational safety, compliance with regulations, and the transition to full autonomy.

From 2026 to 2035, the Fully-Autonomous Aircraft segment is projected to register the highest CAGR. The fast-paced growth is fueled by the ongoing development of AI-enabled flight decision-making systems, rising demand for unmanned logistics and air transportation services, and increased funding in the military sector for autonomous combat and reconnaissance aircraft that can operate in hostile conditions independently of any human presence.

By Platform Type, UAVs / Drones dominate the Autonomous Aircraft Market, Hybrid VTOL / eVTOL Aircraft expected to grow fastest

In 2025, the Unmanned Aerial Vehicles (UAVs / Drones) segment held the largest share of 34.15%, driven by widespread adoption in defense surveillance, border monitoring, and commercial inspection applications. UAVs remain the most cost-effective and operationally flexible autonomous platforms, with strong penetration across both military and industrial use cases.

From 2026 to 2035, the Hybrid VTOL / eVTOL Aircraft segment is expected to record the highest CAGR. Growth will be driven by the fast-growing ecosystem of urban air mobility, growing investment in self-flying passenger aircraft, and increasing need for cargo aircraft that can take off and land vertically in urban areas.

By Application, Defense & Military dominates the Autonomous Aircraft Market, Logistics & Delivery Services expected to grow fastest

In 2025, the Defense & Military segment accounted for 48.85% of total market revenue, maintaining its dominant position As a result of widespread use of autonomous systems for ISR, combat support, reconnaissance, and mission execution. Continuous defense modernization and greater dependence on unmanned systems for highly risky operations greatly consolidate its leadership position.

From 2026 to 2035, the Logistics & Delivery Services segment is projected to register the highest CAGR.This growth is driven by the rapid expansion of e-commerce logistics automation, last-mile drone delivery systems, and increasing adoption of autonomous cargo aircraft for time-sensitive and remote-area transportation.

By Technology, Artificial Intelligence (AI) & Machine Learning Systems dominates the Autonomous Aircraft Market, Edge Computing & Real-Time Data Processing expected to grow fastest

In 2025, the Artificial Intelligence (AI) & Machine Learning Systems segment maintained its dominant position in the Autonomous Aircraft Market, accounting for 30.24% of total revenue. Such leadership is due to the key role it plays in the capability to make independent decisions, flight path optimization, real-time object recognition, and mission adaptability within the context of defense drones as well as commercial autonomous planes. AI-based systems are the foundation of autonomous intelligence, which makes them necessary in all aircraft applications.

From 2026 to 2035, the Edge Computing & Real-Time Data Processing segment is projected to register the highest CAGR.

By End User, Defense Forces & Military Organizations segment dominates the Autonomous Aircraft Market, Logistics & E-commerce Companies segment expected to grow fastest

The Defense Forces & Military Organizations segment maintained the highest end-user share of 49.51% in 2025Such dominance is fueled by the wide use of unmanned aircraft for intelligence gathering and reconnaissance, border surveillance, combat support, and reconnaissance purposes. Ongoing defense modernization efforts and increasing purchases of drones and autonomous combat systems have further contributed to their widespread application in military aviation environments.

The Logistics & E-commerce Companies segment is projected to achieve the highest growth rate during 2026–2035.

Autonomous Aircraft Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38.77% |

|

Europe |

Germany |

27.34% |

|

Asia Pacific |

China |

23.99% |

|

Middle East & Africa |

UAE |

4.64% |

|

Latin America |

Brazil |

5.26% |

North America Autonomous Aircraft Market Insights

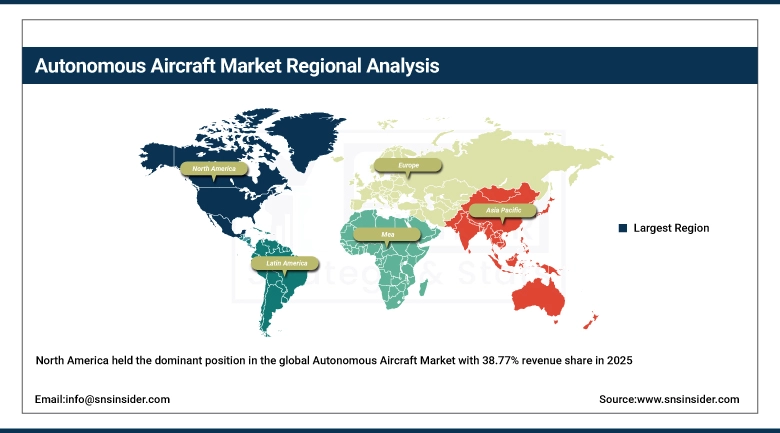

North America held the dominant position in the global Autonomous Aircraft Market with 38.77% revenue share in 2025, fueled by the presence of an advanced aerospace industry ecosystem, robust defense autonomy initiatives, and early adoption of unmanned aircraft systems enabled by AI technology. The region enjoys the advantages of widespread use of UAVs, autonomous ISR vehicles, and new eVTOL programs with backing from major OEMs and defense companies, alongside highly advanced test and certification capabilities. The United States is the most prominent contributor to the market in the region, thanks to high-value defense spending initiatives, significant R&D initiatives on AI-powered aircraft systems, and fast-tracking autonomous capabilities in future-generation military aircraft platforms.

Supporting this dominance, the Federal Aviation Administration (FAA) is actively advancing regulatory frameworks for unmanned aircraft integration, including expanded BVLOS approvals and structured certification pathways for autonomous flight operations. These initiatives are accelerating safe deployment of autonomous aircraft across both defense and commercial airspace.

Additionally, sustained investments from the U.S. Department of Defense (DoD) in programs such as Collaborative Combat Aircraft (CCA), autonomous drone swarms, and AI-enabled mission systems are significantly strengthening regional leadership in high-end autonomous aviation technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Autonomous Aircraft Market Insights

The Asia Pacific region is projected to register the highest CAGR of 21.26% from 2026–2035, fueled by growing advancements in UAV manufacturing, modernizing efforts in defense systems, and increased use of autonomous flight technology in logistics and UAM. Nations such as China, India, Japan, South Korea, and Singapore are taking the lead in this regard, with China and India being the main players for UAVs and cost-effective autonomous systems.

Supporting this growth, regulatory bodies such as China’s Civil Aviation Administration of China (CAAC) and India’s Directorate General of Civil Aviation (DGCA) are progressively introducing frameworks for drone corridors, unmanned traffic management systems, and certification standards for autonomous aircraft operations. These developments are accelerating structured commercialization of autonomous aviation across the region.

In addition, rising investments in smart city infrastructure, expanding e-commerce logistics networks, and increasing regional focus on AI-driven defense systems are further driving adoption of autonomous aircraft technologies across both commercial and military applications.

Europe Autonomous Aircraft Market Insights

The European region occupied a substantial portion of the market share globally during 2025 because of its well-established aerospace industry, robust defense aviation capabilities, and early implementation of autonomous air vehicle technology solutions. Nations like Germany, France, the UK, and Italy lead in the region, backed by major aerospace Original Equipment Manufacturers (OEMs) and strategic defense modernization programs for future unmanned systems.

Supporting this position, the European Union Aviation Safety Agency (EASA) is actively developing regulatory frameworks for U-space integration, autonomous flight certification, and safe drone corridor deployment across member states. These initiatives are enabling structured integration of autonomous aircraft into controlled civil airspace.

Additionally, increasing investments in collaborative combat aircraft programs, expansion of eVTOL development projects, and strong EU-funded aerospace R&D initiatives are reinforcing Europe’s role as a key innovation hub for autonomous aviation technologies.

Latin America, Middle East & Africa (LAMEA) Autonomous Aircraft Market Insights

The LAMEA region is witnessing steady growth in the Autonomous Aircraft Market, driven by increasing adoption of UAVs for surveillance, infrastructure monitoring, and border security applications, along with gradual expansion of commercial drone logistics in select countries. Brazil, Mexico, South Africa, the UAE, and Saudi Arabia are emerging as key contributors, particularly in defense surveillance and industrial inspection use cases.

In the Middle East, governments in the UAE and Saudi Arabia are actively investing in advanced air mobility programs, smart mobility initiatives, and AI-driven defense modernization projects, accelerating early adoption of autonomous aviation technologies in both civilian and military sectors.

Additionally, growing collaborations between regional aviation authorities and global aerospace companies are improving regulatory readiness, enabling pilot projects for drone delivery systems, autonomous inspection services, and emerging eVTOL-based transport solutions, thereby gradually strengthening the regional autonomous aviation ecosystem.

Autonomous Aircraft Market Growth Drivers:

-

Rapid expansion of autonomous aviation programs across defense, logistics, and urban air mobility is driving strong adoption of AI-enabled flight control systems and fully integrated autonomous aircraft platforms across global aerospace ecosystems.

The main structural factor behind the Autonomous Aircraft Market is the growing trend towards unmanned and autonomous flights, not only for the military but also for civil applications. The growing requirements of ISR activities, autonomous surveillance, and advanced combat systems are leading to an increase in the number of unmanned aerial vehicles and remotely piloted aircraft systems; whereas the upcoming commercial applications, like autonomous cargo deliveries and eVTOL urban air mobility, are also contributing towards market penetration.

Supporting this transformation, aerospace innovation programs led by major OEMs such as Boeing, Airbus, and Lockheed Martin are actively advancing autonomous flight testbeds and AI-enabled aviation platforms, while defense-led initiatives like the U.S. Department of Defense’s Collaborative Combat Aircraft (CCA) program are accelerating real-world deployment of autonomous combat systems and unmanned swarm technologies.

Additionally, regulatory progress from aviation authorities such as the Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) is enabling structured integration of unmanned aircraft systems into controlled airspace through BVLOS approvals, digital air traffic management frameworks, and certification pathways for autonomous flight operations.

Autonomous Aircraft Market Restraints:

-

High technological complexity and stringent certification requirements for autonomous flight systems are increasing development burden and slowing large-scale commercialization of fully autonomous aircraft platforms.

The first constraint that limits the Autonomous Aircraft Market is the high degree of difficulty associated with attaining safe and reliable autonomous flights while meeting stringent safety norms set by the aviation industry. Autonomous flights need to incorporate some very sophisticated technologies including Artificial Intelligence, sensor fusion technology, data processing technology, and fail-proof flight control systems, among others. It also becomes quite difficult to maintain reliability of autonomous operations amid variable conditions in the air space.

Autonomous Aircraft Market Opportunities:

-

Expansion of AI-driven autonomous aviation ecosystems and emerging urban air mobility infrastructure is creating strong opportunities for scalable, next-generation autonomous aircraft deployment across defense and commercial sectors.

The most important growth opportunity within the Autonomous Aircraft Market is in the swift development of autonomous aircraft ecosystems, which involve the integration of AI capabilities, advanced avionics, and data connectivity to allow the operation of aircraft without any human involvement. With the growing need for unmanned aircraft to perform military operations and the increasing interest in using autonomous aircraft for the transportation of cargo and passengers, there is now an urgent requirement for developing autonomous software-enabled aircraft. This is allowing the development of modular autonomy systems that could work with multiple aircraft.

Recent Developments:

-

2026: Boeing and Lockheed Martin accelerated autonomous flight testing programs under next-generation unmanned combat and ISR platforms, expanding evaluation of AI-enabled flight autonomy, swarm coordination, and mission-adaptive decision systems across U.S. defense aviation initiatives, strengthening readiness for Collaborative Combat Aircraft (CCA) deployment.

-

2025: Airbus expanded its autonomous aviation roadmap by advancing flight trials of AI-assisted uncrewed systems and eVTOL prototypes, integrating enhanced sensor fusion, real-time navigation intelligence, and autonomous flight management systems across European test environments to support future urban air mobility deployment.

-

2024: The U.S. Department of Defense (DoD) increased funding under the Collaborative Combat Aircraft (CCA) program, enabling large-scale prototyping of semi-autonomous and autonomous drone wingman systems, while General Atomics and Northrop Grumman progressed AI-enabled UAV demonstrations for ISR and combat support missions, strengthening operational autonomy capabilities.

-

2024: Joby Aviation and Archer Aviation advanced eVTOL certification programs and autonomous flight testing initiatives in the United States, focusing on urban air mobility integration, autonomous flight control validation, and commercial air taxi ecosystem development under FAA regulatory frameworks.

Autonomous Aircraft Market Key Players

Some of the Autonomous Aircraft Market Companies

-

The Boeing Company

-

Airbus SE

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

RTX Corporation

-

General Atomics Aeronautical Systems

-

AeroVironment Inc.

-

DJI

-

Anduril Industries

-

BAE Systems

-

Saab AB

-

Thales Group

-

Leonardo S.p.A.

-

Honeywell Aerospace Technologies

-

Safran Group

-

Elbit Systems Ltd.

-

Kratos Defense & Security Solutions

-

Embraer

-

Joby Aviation

-

Archer Aviation

Autonomous Aircraft Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.76 Billion |

| Market Size by 2035 | USD 54.70 Billion |

| CAGR | CAGR of 20.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Autonomy Level (Fully Autonomous Aircraft, Semi-Autonomous Aircraft, Remotely Piloted Aircraft Systems (RPAS), Others) • By Platform Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Hybrid VTOL / eVTOL Aircraft, Unmanned Aerial Vehicles (UAVs / Drones), Others) • By Application (Defense & Military (ISR, combat missions, reconnaissance), Commercial Aviation (autonomous cargo & passenger trials), Logistics & Delivery Services, Agriculture & Industrial Monitoring, Emergency Response & Disaster Management) • By Technology (Artificial Intelligence (AI) & Machine Learning Systems, Sensor Fusion Systems (Radar, LiDAR, Optical), Flight Control & Avionics Automation Systems, Communication & Navigation Systems (GNSS, SATCOM), Edge Computing & Real-Time Data Processing Systems) • By End User (Defense Forces & Military Organizations, Commercial Airlines & Cargo Operators, Logistics & E-commerce Companies, Government & Public Safety Agencies, Private Operators / Advanced Air Mobility (AAM) Service Providers) |

Frequently Asked Questions

North America dominated the Autonomous Aircraft Market in 2025.

The Unmanned Aerial Vehicles (UAVs / Drones) segment dominated the Autonomous Aircraft Market in 2025.

Rapid expansion of AI-enabled autonomous aviation systems, including UAVs, eVTOL aircraft, and next-generation unmanned defense platforms, is the primary growth driver of the Autonomous Aircraft Market.

The Autonomous Aircraft Market was valued at USD 8.76 billion in 2025.

The Autonomous Aircraft Market is expected to grow at a CAGR of 20.34% from 2026 to 2035.

Get in Touch