Turboprop Aircraft Market Report Scope & Overview:

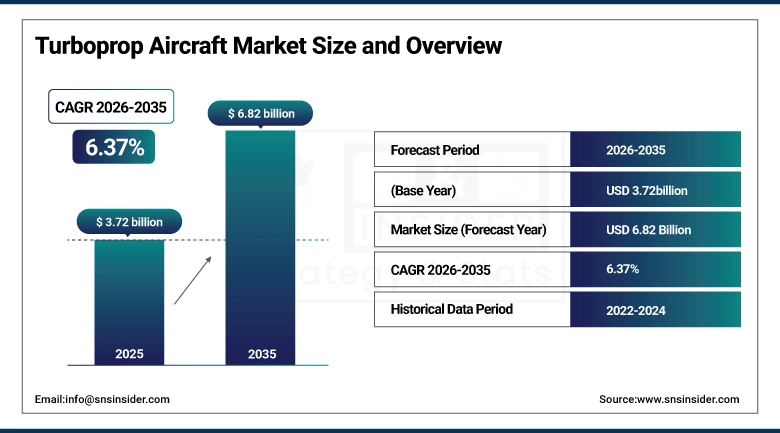

The Turboprop Aircraft Market size is valued at USD 3.72 Billion in 2025 and is projected to reach USD 6.82 Billion by 2035, growing at a CAGR of 6.37% during the forecast period 2026–2035.

The Turboprop Aircraft Market research report gives an overview of market dynamics, fleet dynamics, and usage trends. Increasing needs for regional connectivity, growing use of cargo/freight services due to online business and trade, increasing use of turboprops for military applications including observation and training, and farming operations are some of the factors boosting the market growth from 2026 to 2035.

More than 1,200 turboprops were delivered in 2025, owing to the growth in regional airliners across the world by multinationals.

Market Size and Forecast:

-

Market Size in 2025: USD 3.72 Billion

-

Market Size by 2035: USD 6.82 Billion

-

CAGR: 6.37% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Turboprop Aircraft Market - Request Free Sample Report

Turboprop Aircraft Market Trends:

-

Growing requirements of regional connectivity are favoring turboprop usage in short distance flights.

-

The demand for cargo and freight services is rising sharply owing to the expansion in e-commerce activities.

-

Turboprops increasing deployment in the area of military surveillance, intelligence gathering, and training missions ensures continued military demand.

-

The relatively economical nature of turboprops as compared to regional jets ensures their increased usage.

-

Business and general aviation segments are being driven by single engine turboprops used in corporate and private sector flights.

-

Humanitarian missions, medevac and agricultural sectors account for constant niche demand for turboprops.

-

Fleet modernization projects entail the replacement of legacy Dash 8, Beechcraft and Antonov models with modern ATR, Pilatus and De Havilland turboprops.

-

Demand for environmentally friendly aircraft and development of hybrid technology will shape turboprop market in future.

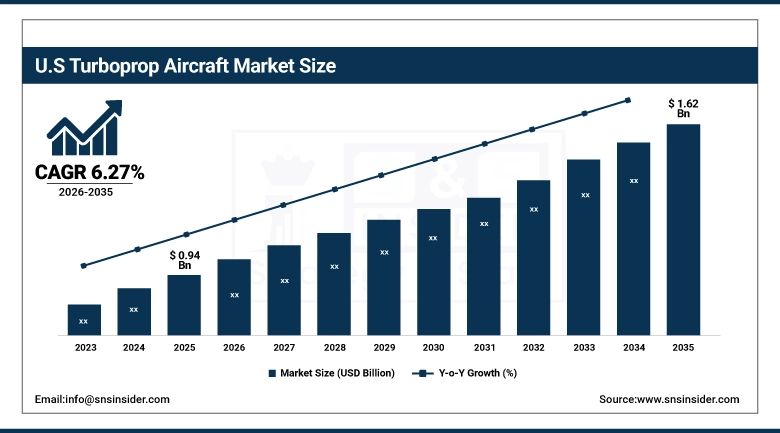

U.S. Turboprop Aircraft Market Insights:

The U.S. Turboprop Aircraft Market is projected to grow from USD 0.94 Billion in 2025 to USD 1.62 Billion by 2035, at a CAGR of 6.27%. Growth will be fueled by an increase in the need for connectivity within the region, increased activity in cargo and freight services owing to e-commerce, wide use of turboprop in the military for surveillance and reconnaissance and for training missions, and investment in new and fuel-efficient aircraft.

Turboprop Aircraft Market Growth Drivers:

-

Rising demand for regional connectivity and expanding e‑commerce logistics are driving strong adoption of turboprop aircraft.

The growing number of passengers in short distance flights and the increase in cargo and freight flights are major factors contributing to the growth of the turboprop aircraft market. Airlines, military forces, and specialized organizations are making efforts to procure advanced turboprops, such as regional passenger turboprops, commuter turboprops, and cargo freight turboprops, in order to improve their efficiency and lower operating expenses. The development of new-age fuel-efficient engines, hybrid propulsion systems, and avionics are helping drive the adoption of these turboprop aircraft and improving their performance.

More than 63 percent of regional airlines, military organizations, and specialized organizations used advanced turboprop aircraft in 2025 due to increased demand for passengers, enhanced cargo capacity, and surveillance.

Turboprop Aircraft Market Restraints:

-

High operating and maintenance costs, limited speed compared to regional jets, and dependence on short‑haul demand present significant restraints for the turboprop aircraft market.

Factors including the unpredictability of fuel pricing, problems related to noise pollution at urban airfields, and competition from regional jet and novel electric planes hinder the wider acceptance of these aircraft. Commercial air carriers, military forces, and specific airline operators frequently lack sufficient funds for upgrading their fleet and purchasing advanced turboprop aircraft. Turboprop manufacturers also encounter difficulties associated with regulatory compliance, lengthy certification processes, and infrastructural problems in underdeveloped countries. Persistent pilot shortages, logistical challenges, and delayed adoption of hybrid technology also act as barriers to growth.

In 2025, more than 42% of regional airlines and operators encountered delays and limited use of turboprop planes owing to high maintenance expenses, rivalry from jets, and infrastructural barriers.

Turboprop Aircraft Market Opportunities:

-

Growing development of fuel‑efficient engines, hybrid propulsion systems, and advanced avionics presents significant market expansion opportunities.

Opportunities in the market will arise from the growing emphasis on sustainability, lower operating costs, and higher performance. Commercial airlines, defense agencies, and specialized aircraft services are utilizing modern turboprops to improve regional connections, provide freight and cargo operations, and assist in surveillance and humanitarian operations. Modern aircraft manufacturers designing innovative, safe, and passenger-friendly aircraft will be able to take advantage of this opportunity. The continual improvement in lightweight material, digital cockpit system compatibility, and alternative fuels, along with increased efficiency and safety, makes this possible.

Advanced turboprop aircrafts were adopted by more than 47% of regional airlines, defense organizations, and specialized service firms in 2025, due to the increasing demands of passengers, logistic operations, and mission-critical defense needs.

Turboprop Aircraft Market Segmentation Analysis:

-

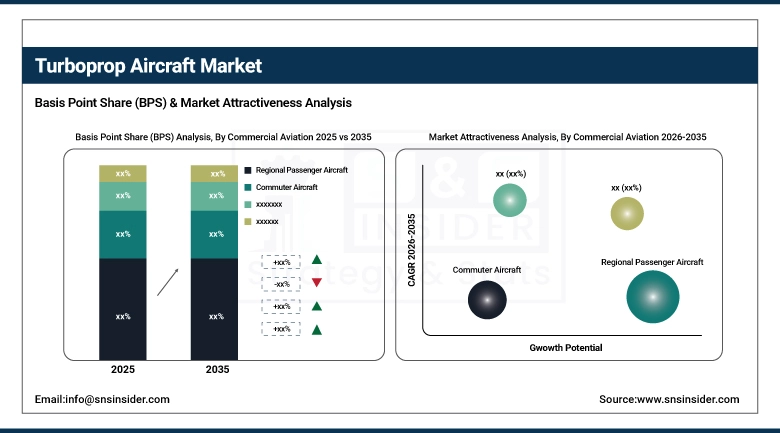

By Commercial Aviation, Regional Passenger Aircraft held the largest market share of 43.19% in 2025, while Cargo/Freight Aircraft are expected to grow at the fastest CAGR of 7.65% during 2026–2035.

-

By Military & Defense, Surveillance & Reconnaissance Aircraft dominated with 48.62% market share in 2025, whereas Training Aircraft are projected to record the fastest CAGR of 7.38% through 2026–2035.

-

By Business & General Aviation, Single-Engine Turboprops accounted for the highest market share of 54.55% in 2025, while Twin-Engine Turboprops are expected to grow at the fastest CAGR of 7.13% during the forecast period.

-

By Specialized Applications, Agricultural Aircraft dominated with a 39.82% share in 2025, while Utility Aircraft are anticipated to expand at the fastest CAGR of 7.52% through 2026–2035.

By Commercial Aviation, Regional Passenger Aircraft Dominate While Cargo/Freight Aircraft Grow Rapidly:

Regional Passenger Aircraft account for the majority share due to their high level of efficiency in catering to short haul flights, and the extensive adoption of the type of aircraft across the regional airlines. Their reliable service, efficiency, and capability to connect even smaller airports have made them indispensable for turboprop transport.

Freight/Cargo Aircraft have the fastest growth rate since they benefit from the increasing use of e-commerce logistics, the rising demand for fast delivery options, and the need to be highly flexible and adaptable in different environments. This is why there is rapid adoption due to the expanding fleet of cargo aircraft.

By Military & Defense, Surveillance & Reconnaissance Aircraft Dominate While Training Aircraft Face Operational Challenges:

The Surveillance & Reconnaissance Aircraft category leads the defense market due to its importance in providing intelligence information, conducting border surveillance, and monitoring maritime activities. Its capability to perform efficiently during slow-speed and low-altitude operations makes it indispensable for defense organizations.

Training Aircraft confront constraints associated with high purchasing and operating expenses, financial limitations of smaller defense entities, and rivalry from simulation technology. Even though there is demand for aircraft for pilot training, dependency on simulators and cost-effective substitutes hinders their acceptance, posing difficulties for growth within the subcategory.

By Business & General Aviation, Corporate Shuttle Aircraft Dominate While Private Charter Aircraft Expand Rapidly:

Corporate Shuttle Aircraft remain the leading players in the market, owing to their extensive usage by businesses in need of effective point-to-point transportation of personnel. The combination of efficiency and convenience offered by Corporate Shuttle Aircraft is making them highly sought after in the business sector, especially in areas where commercial air services are not available.

Private Charter Aircraft are becoming the fastest-growing aircraft types, due to the increasing popularity of individualized trips and their adoption by wealthy customers and businesses. Private Charter Aircraft offer greater comfort and convenience compared to other aircraft types, and hence are poised to drive market growth in the near future.

By Specialized Applications, Humanitarian & Medical Evacuation Aircraft Dominate While Training & Simulation Platforms Expand Rapidly:

Aircraft for Humanitarian & Medical Evacuation take the top spot due to their crucial contribution during emergency situations, humanitarian aid, and patient transportation. Being capable of reaching inaccessible areas makes them an essential asset in the hands of governments, NGOs, and specialized operators.

Training & Simulation Platforms are proving to be the most fastest growing niche, backed by growing expenditures in pilot training solutions and mission-specific simulation platforms. A greater focus on safety, economic feasibility, and training requirements makes them a crucial growth area for specialized turboprop applications.

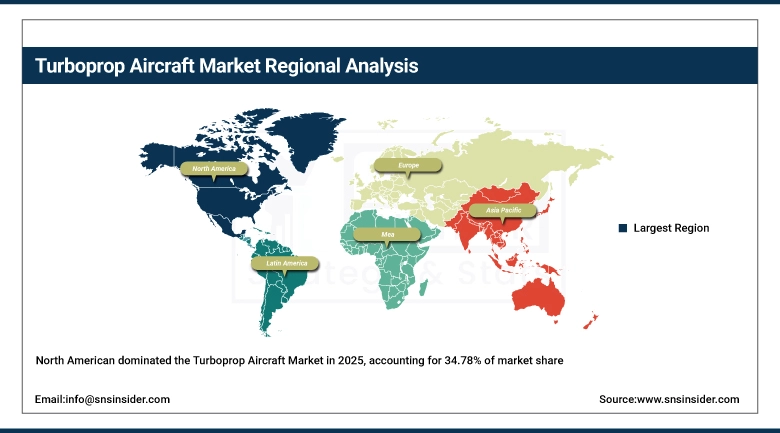

Turboprop Aircraft Market Regional Analysis:

North America Turboprop Aircraft Market Insights:

North America still leads with its 34.78% share of the market, owing to its superior regional airline fleets, cargo industry, and military defense procurements. There are highly advanced aviation systems in place within the United States and Canada, which use the turboprop engine extensively for passenger and cargo transportation. The continual upgrading of fleets, along with research into sustainable aviation technology, ensures that North America continues to dominate in this established market. Demand for business aviation and private charters is helping to maintain this trend.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Turboprop Aircraft Market Insights:

The U.S. market is characterized by high levels of connectivity within the region, high cargo loads, and considerable military requirements. The prevalence of turboprop aircraft with regional carriers, and their use for surveillance and training purposes, makes America the biggest market within North America. The continuous development of hybrid power systems and advanced avionics adds to this advantage.

Asia Pacific Turboprop Aircraft Market Insights:

Asia Pacific region is expected to be the most rapidly growing market with CAGR of 8.16% due to increasing airline connectivity within the region, passenger demand, and cargo traffic. Countries such as India, Indonesia, and Australia have made huge investments in the purchase of turboprops aircrafts for linking smaller airports in order to foster economic development. Growing defense acquisitions and humanitarian missions play a key role in fueling market growth. Increased investments in aviation schools are helping to enhance operational capabilities.

China Turboprop Aircraft Market Insights:

The Chinese markets have been growing due to investment in regional aircraft by the Chinese government, increased cargo transport, and greater defense modernization initiatives. More turboprops have been used in China to aid in surveillance and linking secondary cities. Manufacturers within the domestic industry have grown stronger.

Europe Turboprop Aircraft Market Insights:

The European continent enjoys a favorable standing, backed by the presence of a reliable regional airline network, an effective cargo market, and defense uses. France, the United Kingdom, and Italy have emerged as the primary adopters of turboprops, with support from companies such as ATR and Pilatus. Sustainable solutions and hybrid propulsion technologies are contributing to the anticipated growth in the coming years in the region. Moreover, increasing interest in business aviation and private charter services is bolstering the reputation of the continent as an important center for adopting turboprops.

Germany Turboprop Aircraft Market Insights:

Germany’s market relies on high levels of business aviation activity, regional linkages, and defense uses. Sustainable technologies and advanced production in Germany encourage the adoption of turboprop aircraft. Increased adoption in corporate shuttle and mission operations cements Germany’s standing as an important European market.

Latin America Turboprop Aircraft Market Insights:

Latin America is experiencing continued growth due to the need for connectivity in the region among distant locations, coupled with growing cargo traffic. Nations such as Brazil and Mexico are investing in turboprop aircraft in order to meet requirements for tourism, agricultural activities, and humanitarian efforts. The economic upturn and development projects are also contributing to market growth.

Middle East & Africa Turboprop Aircraft Market Insights:

The Middle East and Africa markets are growing due to defense spending, humanitarian activities, and connectivity programs. The use of turboprop aircrafts in conducting surveillance operations, and evacuation and freight transport services, is becoming more common in areas where there was no previous activity. The government efforts to improve aviation infrastructures are encouraging the growth, thus making the region poised to sustain its growth momentum in the coming years.

Turboprop Aircraft Market Competitive Landscape:

ATR

ATR is a top aircraft manufacturer based in France and Italy. The company manufactures regional turboprop aircraft such as the ATR 42 and ATR 72 series. ATR holds a major share of the turboprop aircraft industry due to its ability to provide economical, efficient, and reliable options in the aviation industry for short haul flights. The reach of ATR, collaborations with regional airlines, and consistent efforts in developing hybrid engines make ATR highly competitive in the aerospace sector.

-

In April 2025, ATR announced advancements in hybrid‑electric propulsion systems, aiming to reduce emissions and enhance efficiency in regional aviation.

De Havilland Aircraft of Canada

De Havilland Aircraft of Canada is an important aerospace corporation based in Canada known for manufacturing various turboprop airplanes including the Dash 8 range of planes that have been extensively used in many regional airlines across the world. The main products of the corporation include the characteristics of high reliability, passenger convenience, and flexibility to operate under different environmental conditions. With its fleet modernization and after-market services alongside sustainable aviation technologies, De Havilland will grow into a leader in the regional aircraft industry.

-

In June 2025, De Havilland launched the Dash 8‑400 cargo conversion program, expanding its offerings to meet rising freight demand.

Pilatus Aircraft

Pilatus Aircraft is an aircraft manufacturing company from Switzerland that has made significant strides in the turboprop industry using its PC 12 and PC 21 product lines. The company offers its products for various purposes including business, training, and defense missions. It has continued to innovate by extending its services to both civil and military customers. Its products are known for their effectiveness and efficiency. Pilatus Aircraft offers efficient customer support which ensures improved performance among its operators.

-

In December 2025, Pilatus delivered its 2,000th PC‑12, marking a milestone in business aviation and reinforcing its dominance in single‑engine turboprops.

Turboprop Aircraft Market Key Players:

Some of the Turboprop Aircraft Market Companies are:

-

ATR

-

De Havilland Aircraft of Canada

-

Pilatus Aircraft

-

Textron Aviation (Beechcraft & Cessna)

-

Embraer

-

Leonardo (Alenia Aermacchi)

-

Daher (TBM series)

-

Viking Air

-

Lockheed Martin (C‑130 Hercules turboprop variants)

-

Airbus (military turboprops like C295)

-

Boeing (defense turboprop programs)

-

Saab AB

-

Mitsubishi Heavy Industries

-

Antonov Company

-

RUAG Aviation

-

Hindustan Aeronautics Limited (HAL)

-

Ilyushin Design Bureau

-

Kawasaki Heavy Industries

-

Aero Vodochody

-

Dornier Seawings

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.72 Billion |

| Market Size by 2035 | USD 6.82 Billion |

| CAGR | CAGR of 6.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Commercial Aviation (Regional Passenger Aircraft, Commuter Aircraft, Charter & Tourism Aircraft, Cargo/Freight Aircraft, Others), • By Military & Defense (Surveillance & Reconnaissance Aircraft, Training Aircraft, Transport Aircraft, Special Missions Aircraft, Others), • By Business & General Aviation (Single-Engine Turboprops, Twin-Engine Turboprops, Corporate Shuttle Aircraft, Private Charter Aircraft, Others), • By Specialized Applications (Agricultural Aircraft, Humanitarian & Medical Evacuation Aircraft, Utility Aircraft, Training & Simulation Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ATR, De Havilland Aircraft of Canada, Pilatus Aircraft, Textron Aviation (Beechcraft & Cessna), Embraer, Leonardo (Alenia Aermacchi), Daher (TBM series), Viking Air, Lockheed Martin (C-130 Hercules turboprop variants), Airbus (military turboprops like C295), Boeing (defense turboprop programs), Saab AB, Mitsubishi Heavy Industries, Antonov Company, RUAG Aviation, Hindustan Aeronautics Limited (HAL), Ilyushin Design Bureau, Kawasaki Heavy Industries, Aero Vodochody, Dornier Seawings. |

Frequently Asked Questions

North America dominated with a 34.78% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 8.16% during 2026–2035.

Regional Passenger Aircraft dominated with a 43.19% share in 2025, while Cargo/Freight Aircraft are projected to grow at the fastest CAGR of 7.65% during 2026–2035.

Growth is driven by increasing demand for rising cargo and freight operations fueled by e‑commerce, the cost efficiency and fuel savings of turboprops on short‑haul routes.

The market is valued at USD 3.72 Billion in 2025 and is projected to reach USD 6.82 Billion by 2035.

The Turboprop Aircraft Market is projected to grow at a CAGR of 6.37% during 2026–2035.

Get in Touch