Animal Biotechnology Market Report Scope & Overview:

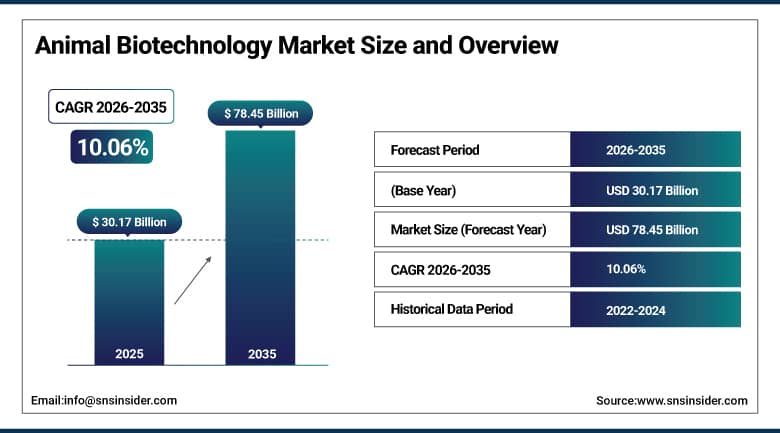

The Animal Biotechnology Market was valued at USD 30.17 Billion in 2025 and is expected to reach USD 78.45 Billion by 2035, growing at a CAGR of 10.06% from 2026 to 2035.

The animal biotech market is huge and important, growing fast within life sciences and agriculture. This field covers lots of areas like making vet vaccines, advanced treatments, precise reproduction tech, and more. It's really useful too, playing key roles in livestock farming, pet care, research, and keeping food safe. Improvements in biotech let us do things we couldn't before, such as enhancing animals and products way beyond what traditional methods can manage. Thanks to progress in areas like genomics and info tech, there are amazing new ways to develop better vet medicines, breed disease-resistant animals, and speed up genetic progress through smart reproductive techniques. So, biotech keeps evolving, bringing game-changing benefits.

Zoetis Inc., the world’s largest animal health company by revenue, reported net revenues exceeding USD 9.0 Billion in fiscal year 2024, reflecting the sustained structural growth of the veterinary biologics and diagnostics segments, with its companion animal and livestock vaccine portfolios recording consistent double-digit organic revenue growth supported by expanding global livestock populations and accelerating companion animal humanization trends across key markets.

Market Size and Forecast:

-

Market Size in 2026E: USD 33.12 Billion

-

Market Size by 2035: USD 78.45 Billion

-

CAGR: 10.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Animal Biotechnology Market - Request Free Sample Report

Animal Biotechnology Market Trends:

-

Rising adoption of genomic selection and gene-editing technologies is accelerating livestock genetic improvement.

-

Growing companion animal healthcare spending is boosting demand for veterinary biologics and diagnostics.

-

Increasing global protein demand is driving investment in reproductive biotechnology and animal productivity solutions.

-

Expansion of AI-powered bioinformatics tools is enhancing disease diagnostics and breeding efficiency.

-

Supportive regulations for veterinary vaccines and animal health innovations are expanding market opportunities.

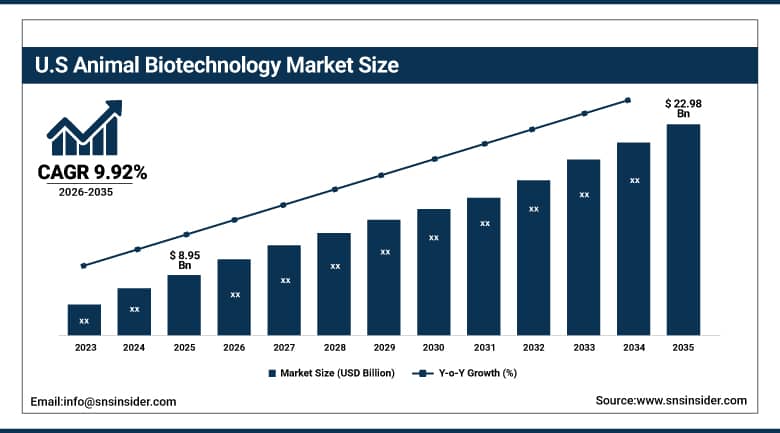

U.S. Animal Biotechnology Market Outlook

The U.S. Animal Biotechnology Market was valued at USD 8.95 Billion in 2025 and is expected to reach USD 22.98 Billion by 2035, growing at a CAGR of 9.92%.

The United States leads in the global animal biotechnology market because of its strong research setup, innovative biotech ability, and rules that encourage new ideas while ensuring safety. They've got a huge livestock and pet healthcare industry too, which drives demand for advanced vet products. In the US, the biggest cattle and pig farming systems in the world make a massive need for tech that boosts animal performance. This includes things like bovine somatotropin and fancy AI methods. Embryo transfer and genomic selection tools now speed up breeding improvement way more than ever before - from years down to months.

The American Veterinary Medical Association estimates that more than 70% of U.S. households own at least one pet, generating a companion animal healthcare market that supports sustained premium pricing for advanced veterinary biologics and diagnostics, with total U.S. animal health product expenditures exceeding USD 38 billion annually across veterinary services and pharmaceutical products.

Animal Biotechnology Market Segment Analysis

-

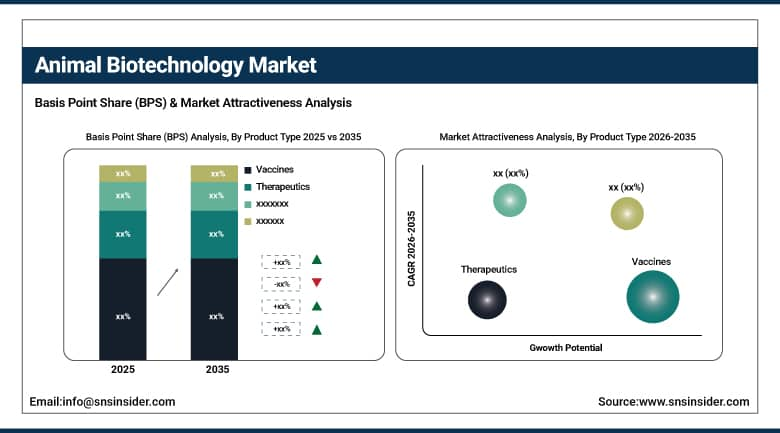

By Product Type, vaccines dominated the market with 34.15% share in 2025, while reproductive biotechnology products are the fastest growing product type with the highest CAGR of 11.75% from 2026 to 2035.

-

By Technology, genetic engineering dominated the market with 31.12% share in 2025, while bioinformatics is the fastest growing technology segment with the highest CAGR of 11.38% from 2026 to 2035.

-

By Animal Type, livestock animals dominated the market with 60.43% share in 2025, while swine is the fastest growing animal type with a CAGR of 11.05% from 2026 to 2035.

-

By End User, veterinary hospitals & clinics dominated the market with 30.06% share in 2025, while animal breeding centers are the fastest growing end user segment with the highest CAGR of 11.09% from 2026 to 2035.

By Product Type, vaccines dominate the animal biotechnology market, while reproductive biotechnology products are the fastest-growing segment.

Vaccines segment dominated the animal biotechnology market with the highest revenue share of 34.15% in 2025, owing to the fundamental and indispensable role that prophylactic veterinary biologics play across commercial livestock production, companion animal healthcare, and government-mandated disease control programmes worldwide. The expansive and continuously evolving veterinary vaccine portfolio targeting bacterial, viral, and parasitic pathogens across livestock, poultry, swine, and companion animal species ensures that this segment maintains its market leadership by addressing the biosecurity requirements of global food systems and the healthcare expectations of companion animal owners.

Reproductive Biotechnology Products segment is estimated to register the highest CAGR during the forecast period of 2026–2035, driven by accelerating adoption of advanced artificial insemination, embryo transfer, sexed semen technologies, and in vitro fertilization protocols across commercial cattle, swine, and sheep production systems globally. Growing emphasis on rapid genetic improvement, reduction in generation intervals, and maximisation of superior sire utilisation is compelling commercial livestock producers to invest substantially in reproductive biotechnology services and equipment.

By Technology, Genetic Engineering dominates the animal biotechnology market, while Bioinformatics is the fastest-growing segment.

Genetic Engineering segment dominated the animal biotechnology market with the largest revenue share of approximately 31.12% in 2025, reflecting its foundational role across veterinary vaccine antigen development, disease-resistance trait introduction in commercial livestock, and production of recombinant proteins and biologics for veterinary therapeutic applications. The maturity and regulatory acceptance of genetic engineering platforms across key markets, combined with the continuous expansion of commercially validated recombinant vaccine and therapeutic product portfolios by major animal health corporations, sustains the segment’s market leadership position across forecast years.

Bioinformatics segment is projected to witness the fastest CAGR during 2026–2035, driven by the exponentially growing volume of genomic and phenotypic data generated across livestock improvement programmes, companion animal disease diagnostics, and veterinary pharmaceutical discovery workflows. The integration of machine learning algorithms, cloud-based genomic analysis platforms, and real-time data analytics tools into veterinary precision medicine and livestock management systems is creating structural demand for bioinformatics solutions that can transform raw biological data into actionable breeding and health management decisions at scale across global animal agriculture and companion animal healthcare markets.

By Animal Type, livestock animals dominate the animal biotechnology market, while swine is the fastest-growing segment.

Livestock Animals segment dominated the animal biotechnology market with the highest revenue share of approximately 60.43% in 2025, underpinned by the global scale of commercial cattle, poultry, swine, and small ruminant production systems that collectively generate the largest demand base for veterinary vaccines, therapeutics, reproductive technologies, and precision genomic tools. The fundamental economic importance of livestock production to global food security, combined with the high per-animal and per-flock investment in disease prevention and genetic performance optimisation, ensures that livestock remains the structurally dominant animal type category within animal biotechnology by a substantial margin.

Swine segment is projected to register the fastest CAGR through 2035, owing to the rising global demand for pork as a primary protein source, particularly across Asia Pacific markets, combined with the increasing prevalence of complex viral and bacterial disease challenges in commercial swine production that are driving adoption of advanced biotechnology-based vaccines and diagnostics. The devastation caused by African Swine Fever across Asian pig populations has permanently elevated biosecurity investment levels within swine production systems globally, creating structural demand for next-generation swine health biotechnology products across both the prevention and management categories.

By End User, veterinary hospitals & clinics dominate the animal biotechnology market, while animal breeding centers are the fastest-growing segment.

Veterinary Hospitals & Clinics segment dominated the animal biotechnology market with the highest revenue share of approximately 30.06% in 2025, reflecting the central role of veterinary clinical infrastructure in administering biotechnology-based vaccines, therapeutics, and diagnostics across companion animal and livestock healthcare markets. The ongoing professionalisation of companion animal veterinary care in developed markets and the rapid expansion of organised veterinary clinic networks in emerging economies continue to support this segment’s leadership position as the primary commercial delivery channel for advanced animal biotechnology products.

Animal Breeding Centers segment is estimated to register the fastest CAGR during the forecast period of 2026–2035, driven by growing commercial demand for genomic selection services, sexed semen technologies, embryo transfer programmes, and in vitro fertilization protocols that are being adopted by professional breeding organisations seeking to compress genetic improvement timelines and maximise the commercial value of elite animal genetics across cattle, swine, and equine species. Increasing integration of precision genomics platforms within commercial breeding centre operations is further accelerating the adoption of advanced biotechnology tools that support data-driven breeding decisions across global animal genetics markets.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.39% |

|

Europe |

Germany |

28.57% |

|

Asia Pacific |

China |

42.59% |

|

Middle East & Africa |

UAE |

34.49% |

|

Latin America |

Brazil |

42.78% |

North America Animal Biotechnology Market Insights

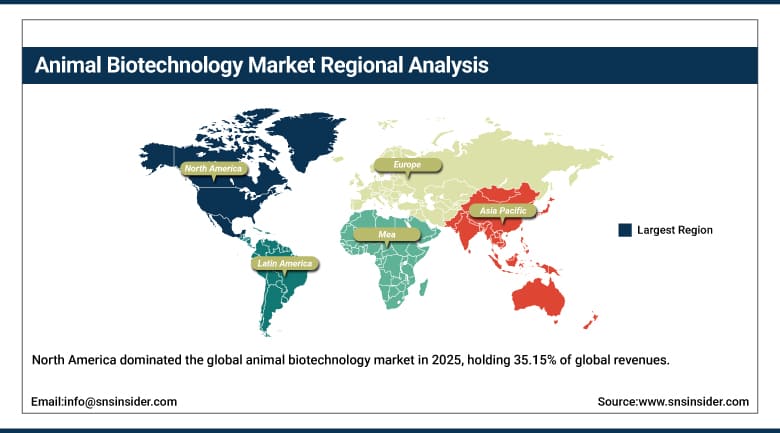

North America dominated the global animal biotechnology market in 2025, holding 35.15% of global revenues, with the United States accounting for 84.39% of regional revenue. The region’s market leadership reflects its unparalleled depth of animal health biotechnology research infrastructure, the commercial scale of its livestock and companion animal healthcare industries, and the regulatory frameworks that have enabled earlier commercial adoption of advanced veterinary biologics, genomic selection technologies, and precision reproductive products compared to other major global markets.

The concentration of world-leading animal health corporations including Zoetis, Elanco, and Merck Animal Health within the North American market ensures that new biotechnology platform products achieve their earliest and most commercially impactful launches in this region before progressively expanding into international markets.

Canada contributes additional regional demand through its significant commercial beef cattle, pork, and poultry production industries, which represent substantial demand bases for veterinary vaccines, reproductive technologies, and genomic tools. The Canadian market benefits from proximity to U.S. biotechnology innovation pipelines and shares many of the regulatory and commercial characteristics that define the North American animal health market as a globally distinctive and commercially advanced ecosystem.

The U.S. animal health products market represents the single largest national market globally, with annual expenditures on veterinary biologics, pharmaceuticals, and diagnostics exceeding USD 12 billion, supported by a commercial livestock industry that includes more than 93 million cattle, 75 million swine, and over 9 billion poultry birds annually in domestic production.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Animal Biotechnology Market Insights

European animal biotechnology market maintains a well-established position as the second-largest regional market globally, supported by a combination of advanced agricultural biotechnology research capabilities, robust regulatory frameworks governing veterinary biological product approvals, and diverse livestock production systems across major markets including Germany, France, the United Kingdom, and the Netherlands. Germany represents the largest single national contributor to European revenues, serving as both a significant commercial livestock production market and the headquarters location for Boehringer Ingelheim Animal Health, one of the world’s leading veterinary vaccine and therapeutics corporations.

Europe’s animal biotechnology sector benefits from a unified regulatory framework under the European Medicines Agency that supports simultaneous multi-country approval processes for veterinary biologics, enabling product launches across the EU’s combined livestock population of 87 million cattle, 145 million swine, and 1.6 billion poultry to achieve commercial scale more rapidly than fragmented national approval processes would permit.

Asia Pacific Animal Biotechnology Market Insights

Asia Pacific is the fastest-growing regional animal biotechnology market at a CAGR of 10.64% through 2035. China accounts for the largest share of Asia Pacific revenues as the world’s largest pig producing and consuming nation, whose commercial swine sector has experienced transformative biosecurity investments following the African Swine Fever outbreaks that devastated the national herd between 2018 and 2022, creating structural and sustained demand for advanced swine vaccines, molecular diagnostic platforms, and biosecurity management technologies at unprecedented commercial scale.

India represents the region’s most rapidly growing country-level market through the expansion of its dairy and poultry biotechnology adoption, growing organised veterinary healthcare infrastructure, and government programmes supporting livestock productivity improvement that are collectively driving adoption of veterinary biologics, reproductive technologies, and genomic tools across its enormous cattle and buffalo population.

China’s commercial livestock sector, which includes the world’s largest swine production system at approximately 700 million pigs annually pre-ASF, and a cattle population exceeding 95 million head, creates one of the highest-potential demand environments globally for animal biotechnology products, with government biosecurity investment programmes allocating billions of renminbi annually to veterinary vaccine stockpiling, diagnostics infrastructure, and disease surveillance systems that directly stimulate commercial animal biotechnology market development.

MEA & Latin America Animal Biotechnology Market Insights

Middle East & Africa and Latin America represent two commercially important and structurally distinct animal biotechnology markets that together offer significant growth potential over the forecast period, supported by expanding livestock populations, rising food protein demand, government investment in agricultural productivity enhancement, and improving veterinary healthcare infrastructure across their respective geographies. The Middle East & Africa region, with the UAE benefits from government-supported livestock productivity programmes, growing demand for biosecure and traceable animal protein production, and expanding organised veterinary healthcare networks that are driving adoption of advanced animal biotechnology products across Gulf Cooperation Council and sub-Saharan African markets.

Latin America represents a globally significant commercial opportunity for animal biotechnology providers, with Brazil owing to its position as one of the world’s largest commercial beef cattle and poultry production systems, generating structural and high-volume demand for veterinary vaccines, reproductive biotechnology services including artificial insemination and embryo transfer, and genomic selection tools that are enabling Brazilian producers to achieve global competitiveness through accelerated genetic improvement of their commercial cattle herds.

Latin America’s commercial beef cattle sector, led by Brazil’s herd of 220 million head representing the world’s largest commercial beef cattle population, generates one of the globally highest demand environments for bovine reproductive biotechnology products and veterinary biologics, with the Brazilian animal health market valued at over USD 5 billion annually and expanding at rates consistently above the global average.

Market Dynamics:

Growth Drivers: Rising livestock disease burden and companion animal healthcare premiumisation

The increasing global burden of economically significant infectious diseases affecting commercial livestock populations, including foot-and-mouth disease, avian influenza, African Swine Fever, bovine respiratory disease, and emerging zoonotic pathogens, is creating sustained and structurally reinforced demand for advanced veterinary biotechnology solutions encompassing prophylactic vaccines, rapid molecular diagnostics, and targeted therapeutics that enable producers to protect the productive value of their herds and flocks from pathogen-driven economic losses. The premiumization of companion animal healthcare is increasing demand for advanced veterinary biologics, monoclonal antibody therapies, and sophisticated diagnostic platforms across developed markets.

Restraints: Lengthy regulatory approval timelines and high product development costs

The development and commercialisation of novel animal biotechnology products, particularly genetically engineered organisms, gene therapy platforms, and novel veterinary biologics, involves regulatory approval processes that can extend across multiple years and impose substantial development cost burdens on innovating companies, creating significant barriers to entry that disadvantage smaller biotechnology enterprises and slow the commercial availability of breakthrough technologies. The high cost of conducting the multi-phase safety, efficacy, and quality clinical trials required for veterinary biologic product registration across major regulatory jurisdictions including the FDA Centre for Veterinary Medicine, EMA, and national regulatory authorities in key emerging markets creates financial constraints that can restrict the breadth and pace of commercial pipeline expansion even for established animal health corporations.

Opportunities: Gene-editing technology adoption and precision livestock farming expansion

The animal biotechnology industry stands at the threshold of a transformative gene-editing revolution whose commercial applications in livestock genetic improvement, disease-resistance trait introduction, and production efficiency enhancement represent opportunities of potentially similar magnitude to those created by the original introduction of recombinant DNA technologies into the veterinary biologics market. CRISPR-Cas9 and related precision gene-editing platforms are enabling researchers and commercial developers to introduce specific, validated disease-resistance traits into commercial livestock populations with unprecedented precision and speed, creating the potential for reduced veterinary intervention costs and improved production system sustainability that will be compelling value propositions for large-scale commercial livestock producers globally.

Recent Developments:

-

2026: Genus plc commercially deployed its PRRS-resistant pig genetics programme across commercial sow herds in the United States and Canada following successful completion of its CRISPR gene-editing commercialisation regulatory process, representing a landmark milestone in the commercial application of gene-editing technology within the livestock production industry.

-

2026: IDEXX Laboratories, Inc. launched the IDEXX VetLab Station AI platform, incorporating machine learning-based diagnostic interpretation across its in-clinic chemistry, haematology, and urinalysis instrument systems to support real-time clinical decision support for companion animal veterinary practitioners across global markets.

-

2025: Zoetis Inc. expanded its mRNA-based veterinary vaccine platform with the commercial launch of a novel swine influenza vaccine candidate incorporating lipid nanoparticle delivery technology, targeting the commercial swine production segment across North American and European markets.

-

2025: Elanco Animal Health Incorporated announced the regulatory submission of its next-generation bovine respiratory disease therapeutic biologic in the United States, combining a novel monoclonal antibody component with a conventional antimicrobial treatment protocol targeting the premium commercial cattle health segment.

Animal Biotechnology Market Key Players are:

-

Zoetis Inc.

-

Elanco Animal Health Incorporated

-

Boehringer Ingelheim Animal Health

-

Merck Animal Health

-

Ceva Santé Animale

-

Virbac S.A.

-

Phibro Animal Health Corporation

-

IDEXX Laboratories, Inc.

-

Neogen Corporation

-

Genus plc

-

Hendrix Genetics B.V.

-

CRV Holding B.V.

-

EW Group GmbH (Aviagen)

-

Cobb-Vantress, Inc.

-

Animalcare Group plc

-

Vetoquinol S.A.

-

HIPRA S.A.

-

Biogenesis Bagó S.A.

-

Allflex Livestock Intelligence (Merck Animal Health)

-

Thermo Fisher Scientific Inc. (Animal Genomics & Diagnostics)

Animal Biotechnology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.17 Billion |

| Market Size by 2035 | USD 78.45 Billion |

| CAGR | CAGR of 10.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Vaccines, Therapeutics, Diagnostics, Reproductive Biotechnology Products, Feed Additives & Nutritional Biotechnology Products, Others) • By Technology (Genetic Engineering, Tissue Engineering & Regenerative Medicine, Reproductive Technologies, Molecular Diagnostics, Bioinformatics, Others) • By Animal Type (Livestock Animals, Cattle, Swine, Others) • By End User (Veterinary Hospitals & Clinics, Animal Breeding Centers, Pharmaceutical & Biotechnology Companies, Research Institutes & Universities, Livestock Farms & Producers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zoetis Inc., Elanco Animal Health Incorporated, Boehringer Ingelheim Animal Health, Merck Animal Health, Ceva Santé Animale, Virbac S.A., Phibro Animal Health Corporation, IDEXX Laboratories, Inc., Neogen Corporation, Genus plc, Hendrix Genetics B.V., CRV Holding B.V., EW Group GmbH (Aviagen), Cobb-Vantress, Inc., Animalcare Group plc, Vetoquinol S.A., HIPRA S.A., Biogenesis Bagó S.A., Allflex Livestock Intelligence (Merck Animal Health), Thermo Fisher Scientific Inc. (Animal Genomics & Diagnostics) |

Frequently Asked Questions

The PET Foam Market is expected to grow at a CAGR of 7.7% from 2026 to 2035.

The PET Foam Market was valued at USD 493.07 Million in 2025.

Expansion of wind energy & composite blade manufacturing.

PET Foam Core dominated the PET Foam Market in 2025.

Asia Pacific dominated the PET Foam Market in 2025.

Get in Touch