Animal Parasiticides Market Report Scope & Overview:

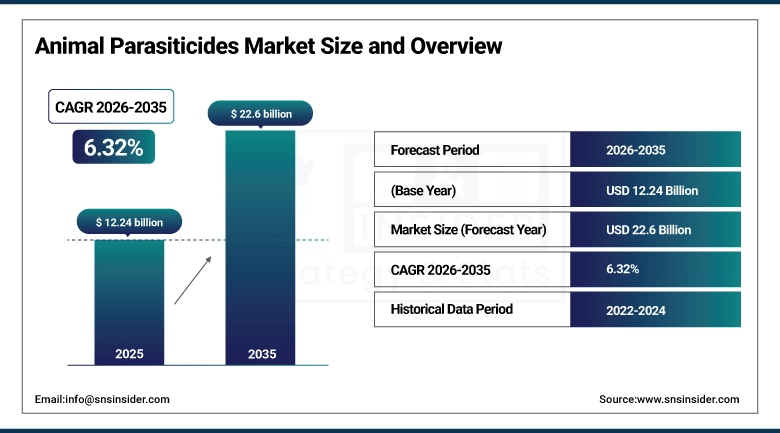

The Animal Parasiticides Market was valued at USD 12.24 billion in 2025 and is expected to reach USD 22.6 billion by 2035, growing at a CAGR of 6.32% from 2026-2035.

Parasites are among the most commercially consequential health threats that animals face, because their impact extends far beyond individual animal welfare to encompass the food security, agricultural productivity, and public health dimensions that make parasiticide use economically compulsory rather than discretionary. In livestock production, parasitic burdens whether gastro-intestinal helminths in sheep and cattle, external parasites in poultry, or blood parasites in cattle reduce weight gain, impair reproductive performance, reduce milk yield, and suppress immune responses that create secondary infection susceptibility. A cattle producer with high gastrointestinal parasite loads across a 500-cow herd may lose 15-20% of achievable beef production to parasite-induced growth suppression representing hundreds of thousands of dollars in annual revenue foregone per farm without treatment. In companion animals, the zoonotic dimension adds public health urgency ticks transmit Lyme disease and Rocky Mountain spotted fever roundworms transmit toxocariasis fleas transmit parasites of dogs and cats create human infection risk that motivates veterinary authorities and pet owners to maintain consistent parasiticide programs beyond pure animal welfare motivation. Companion animal humanization driving premium parasiticide adoption and livestock intensification driving systemic parasite control program implementation.

The WHO documents that zoonotic diseases diseases transmitted between animals and humans are responsible for approximately 2.5 billion cases of illness and 2.7 million deaths annually in humans, with vector-borne and soil-transmitted helminths representing a substantial fraction of this burden. The American Pet Products Association's 2023 pet ownership survey documents that U.S. pet owners spent USD 38.3 billion on veterinary care with parasiticide products as one of the highest-value pharmaceutical categories reflecting the deep commercial market that companion animal health consciousness creates.

Animal Parasiticides Market Size and Forecast

-

Market Size in 2025: USD 12.24 Billion

-

Market Size by 2035: USD 22.6 Billion

-

CAGR: 6.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Animal Parasiticides Market - Request Free Sample Report

Animal Parasiticides Market Trends

-

Isoxazoline class compounds including afoxolaner (NexGard), fluralaner (Bravecto), sarolaner (Simparica), and lotilaner (Credelio) — have transformed the companion animal flea and tick market with oral chewable formats providing 1-3 months of systemic protection from a single monthly or quarterly dose.

-

Long-acting injectable parasiticide formulations providing 4-12 months of protection from a single subcutaneous injection are improving parasiticide compliance in livestock and companion animals whose owner medication adherence with daily or weekly oral treatments is notoriously poor.

-

Combination parasiticides addressing multiple parasite types simultaneously combining heartworm prevention, flea treatment, tick control, and gastrointestinal worm coverage in a single monthly product are the fastest-growing market segment as pet owners adopt simplified single-product parasite protection protocols.

-

Resistance monitoring programs are becoming standard across the livestock sector as anthelmintic resistance in gastrointestinal parasites of sheep and cattle documented across all major anthelmintic drug classes including benzimidazoles, levamisole, and macrocyclic lactones requires diagnostic-guided rotation strategies.

-

Digital veterinary platforms are integrating parasite risk assessment — using geographic parasite prevalence data, weather-based seasonal activity predictions, and individual animal history to generate personalized parasiticide recommendations that improve both clinical outcomes and product compliance.

-

Premium topical spot-on formulations for companion animals — particularly those addressing multiple parasite categories including fleas, ticks, mites, and gastrointestinal parasites in a monthly topical application — are sustaining product innovation investment despite oral chewable competition.

-

Aquaculture parasiticides — for salmon lice (Lepeophtheirus salmonis) control in Atlantic salmon farming — represent a rapidly growing market segment whose product development urgency reflects the industry's substantial economic losses from parasite infestation.

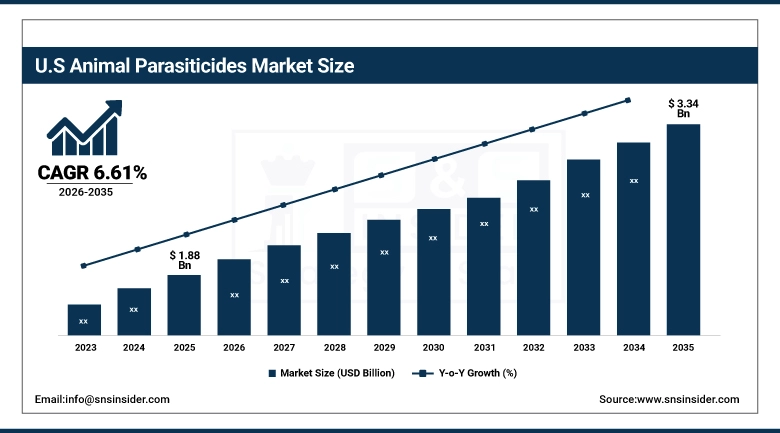

U.S. Animal Parasiticides Market was valued at USD 1.88 billion in 2025 and is expected to reach USD 3.34 billion by 2035, growing at a CAGR of 6.61% from 2026-2035.

North America is expected to register the fastest growth in the Animal Parasiticides Market through the forecast period, driven by the United States' extraordinarily high pet ownership with over 90 million cats and 69 million dogs representing the world's largest companion animal population combined with the high veterinary care expenditure that U.S. pet humanization sustains. The U.S. companion animal parasiticide market's commercial sophistication is reflected in the rapid adoption of premium oral isoxazoline products: NexGard, Bravecto, Simparica, and Credelio collectively generated over USD 3 billion in U.S. companion animal parasiticide revenue in 2025 demonstrating the commercial scale that innovation in parasiticide formulation and convenience achieves in a health-conscious pet owning market. The U.S.'s sophisticated veterinary prescription system where companion animal parasiticides are predominantly prescribed by licensed veterinarians who maintain regular client-patient relationships sustains premium product adoption at rates that over-the-counter markets cannot approach.

Zoetis's 2024 annual report documents that its companion animal parasiticide portfolio — led by Simparica Trio (sarolaner + moxidectin + pyrantel) — generated over USD 1.5 billion in companion animal parasiticide revenue in the U.S. alone, making it the world's leading animal health company by companion animal pharmaceutical revenue. The Companion Animal Parasite Council's 2024 guidelines recommend year-round parasite prevention for dogs and cats in all U.S. climate zones a protocol recommendation whose compliance creates 12-month-per-year companion animal parasiticide market demand rather than the seasonal purchasing patterns that historically characterized flea and tick markets.

Animal Parasiticides Market Segment Analysis

-

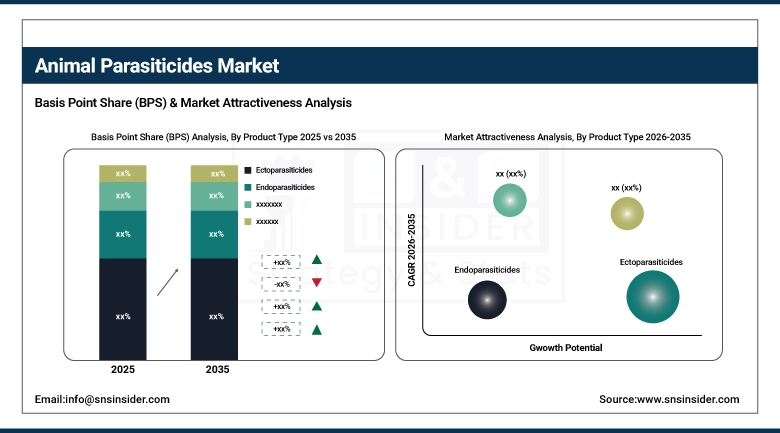

By Product Type, Ectoparasiticides dominated with 43.26% share in 2025; Anthelmintics and Combined Formulations growing rapidly.

-

By Animal Type, Companion Animals significant share; Livestock dominated historically driven by agricultural volume.

-

By Distribution Channel, Veterinary Hospitals & Clinics dominated with 58.30% share in 2025; Online Channels growing fastest.

By Product Type: Ectoparasiticides dominate at 43.26%, Combination growing rapidly

Ectoparasiticides held approximately 43.26% of the Animal Parasiticides Market in 2025, reflecting the clinical and commercial priority that external parasite control — targeting fleas, ticks, mites, lice, and flies commands across both companion animal and livestock applications. The companion animal ectoparasiticide segment's extraordinary commercial dynamism where the isoxazoline revolution created a USD 5+ billion global market categories in less than a decade from NexGard's first approval in 2013 — sustains ectoparasiticide segment dominance through both unit volume and per-unit revenue premium that oral systemic flea and tick products command over traditional topical alternatives. In livestock, ectoparasiticide demand is driven by cattle flies — horn flies, face flies, stable flies whose production impact in beef cattle and dairy operations creates year-round parasiticide program investment on commercial farms.

Anthelmintics drugs targeting internal parasites including roundworms, tapeworms, hookworms, and lungworms sustain significant market share as the pharmacological class addressing the internal parasite burden that companion animal wellness protocols and livestock herd health programs must control. Macrocyclic lactones including ivermectin, doramectin, and moxidectin serve both companion animal heartworm prevention and livestock gastrointestinal nematode control creating dual-market products whose commercial versatility sustains manufacturing scale investment. Combined Formulations — single products simultaneously addressing ectoparasites and endoparasites — are the fastest-growing product type, driven by companion animal owners' preference for monthly single-product parasite protection that eliminates the need to manage separate flea, tick, and heartworm prevention products.

By Animal Type, Companion Animals significant share; Livestock dominated historically driven by agricultural volume.

Companion Animals held a significant share of the Animal Parasiticides Market in 2025, reflecting the rapid expansion of pet ownership, increasing veterinary expenditure, and the growing clinical emphasis on preventive parasite care for dogs and cats across developed and emerging markets. The companion animal segment benefits from strong consumer willingness to spend on premium parasiticide products including oral chewables, spot-on formulations, long-acting collars, and combination therapies targeting fleas, ticks, mites, heartworms, and intestinal parasites. The commercial success of premium companion animal parasiticides such as Zoetis’ Simparica, Boehringer Ingelheim’s NexGard, and Elanco’s Seresto collar continues to drive high per-animal treatment spending and recurring monthly preventive care adoption. Increasing humanization of pets, rising awareness regarding zoonotic diseases, and the expansion of veterinary healthcare infrastructure further support strong companion animal segment growth globally.

Livestock historically dominated the Animal Parasiticides Market due to the enormous treatment volume generated by cattle, poultry, swine, sheep, and aquaculture industries where parasite management directly impacts meat yield, milk production, reproductive performance, and overall farm profitability. Commercial livestock operations maintain large-scale parasiticide treatment programs to control gastrointestinal worms, ticks, lice, mites, and flies that can significantly reduce productivity and increase disease transmission risk. Macrocyclic lactones including ivermectin, doramectin, and moxidectin remain widely utilized across cattle and sheep operations due to their broad-spectrum efficacy and cost efficiency in large herds. The livestock segment’s historical dominance reflects the agricultural scale of parasite control programs where millions of production animals require routine preventive treatment across intensive farming systems globally.

By Distribution Channel: Vet Clinics dominate, Online growing fastest

Veterinary Hospitals and Clinics held approximately 58.30% of the Animal Parasiticides Market in 2025, reflecting the prescription and recommendation-driven purchase pattern that companion animal parasiticides follow in well-developed veterinary markets. Veterinary prescription parasiticides — including the isoxazoline class oral chewables that require veterinary prescription in the U.S. and EU — are exclusively available through veterinary channels, sustaining clinic distribution dominance for the highest-value companion animal product categories. The veterinary clinic's role as the primary point of parasiticide recommendation creates commercial value beyond mere distribution: veterinarians who recommend specific brands sustain brand loyalty through the trust relationship with pet owners that peer review, product trial experience, and professional credibility create. Online channels are growing at the fastest distribution CAGR, driven by the expansion of online veterinary pharmacy platforms and direct-to-consumer parasiticide brands whose convenience and price competition with clinic pricing create growing online share particularly for OTC parasiticide categories.

Animal Parasiticides Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

42% |

|

North America |

United States |

88% |

|

Europe |

Germany |

27% |

|

Middle East & Africa |

South Africa |

38% |

|

Latin America |

Brazil |

52% |

Asia Pacific Animal Parasiticides Market Insights

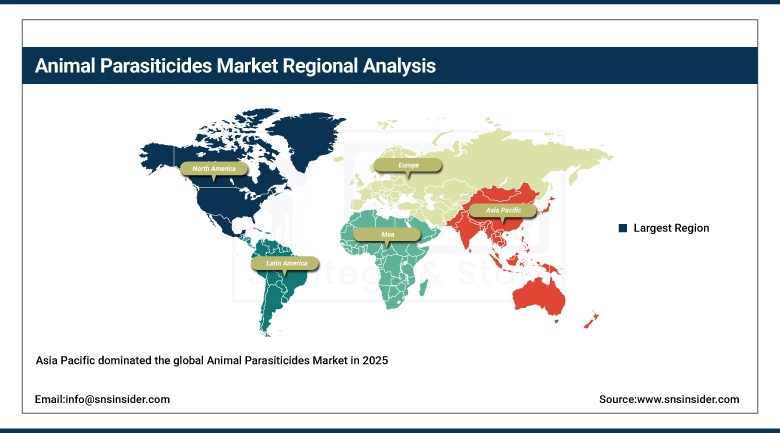

Asia Pacific dominated the global Animal Parasiticides Market in 2025, driven by the region's extraordinary livestock population China, India, and Southeast Asia collectively account for the majority of global cattle, pig, poultry, and sheep populations whose parasite control requirements create the world's largest livestock parasiticide demand. China's pig industry the world's largest by production volume, recovering from ASF losses requires comprehensive parasite control programs across 400+ million pig placements annually. India's cattle population of approximately 300 million animals creates massive anthelmintic demand from veterinary health programs, private livestock producers, and government animal husbandry programs whose parasiticide procurement sustains domestic and imported product demand. Asia Pacific's growing companion animal market particularly in China, Japan, and South Korea where pet humanization is accelerating rapidly is additionally creating premium companion animal parasiticide demand that is the region's fastest-growing parasiticide sub-segment.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Animal Parasiticides Market Insights

North America is expected to grow at the fastest Animal Parasiticides Market CAGR, led by the United States where the combination of the world's highest companion animal parasiticide spending per pet, the most advanced isoxazoline oral product penetration, and the growing awareness of zoonotic disease risk from companion animal parasites create uniquely favorable commercial conditions. The U.S. Companion Animal Parasite Council's year-round prevention recommendation adopted by a growing proportion of U.S. veterinarians is converting the historically seasonal flea, tick, and heartworm market into a 12-month continuous purchasing pattern that sustains higher annual per-pet parasiticide spend. Canada's large livestock sector and strong companion animal parasiticide market contribute to North America's combined market leadership.

Europe Animal Parasiticides Market Insights

Europe's Animal Parasiticides Market is characterized by sophisticated companion animal parasite prevention protocols — including the European Scientific Counsel Companion Animal Parasites (ESCCAP) guidelines that are widely adopted by European veterinary practices — and extensive livestock parasite control programs across the EU's substantial sheep, cattle, and pig industries. European approval of isoxazoline companion animal parasiticides — including EU approval for NexGard, Bravecto, Simparica, and Credelio — has converted European companion animal parasiticide purchasing toward premium oral systemic products that sustain higher per-pet annual expenditure than previous-generation topical products. The UK's Sheep Scab control program and EU cattle herd health programs sustain consistent livestock parasiticide demand.

MEA and Latin America Animal Parasiticides Market Insights

The Middle East and Africa's Animal Parasiticides Market is growing with improving veterinary infrastructure and expanding livestock industry investment. Sub-Saharan Africa's substantial livestock sector whose cattle population exceeds 230 million animals represents an enormous potential parasiticide market whose realized demand is constrained by limited veterinary services access, purchasing power constraints, and distribution infrastructure gaps that global animal health companies are progressively addressing through strategic partnerships with local distributors and government animal health programs. Latin America's market is driven by Brazil's world-leading beef cattle industry whose Nelore cattle breed's resistance to tropical parasites creates a specialized parasiticide market for the tick species and internal parasites adapted to Brazilian conditions and the region's large pig, poultry, and sheep industries.

Animal Parasiticides Market Growth Drivers:

Rising pet ownership and zoonotic disease awareness driving sustained animal parasiticides market growth globally

The Animal Parasiticides Market is driven by the convergence of companion animal market premiumization and livestock production intensification that are each independently strong and mutually reinforcing at the global animal health industry level. Companion animal humanization where pet owners increasingly adopt human-equivalent healthcare standards for their animals creates consistent willingness-to-pay for premium parasiticide products whose efficacy, convenience, and safety profiles justify substantial price premiums over generic alternatives. Zoonotic disease awareness accelerated by demonstration of animal-to-human pathogen transmission risk is creating policy and consumer motivation for rigorous companion animal parasite control that sustains parasiticide program compliance. Livestock intensification in emerging markets where the productivity pressure of feeding growing urban populations requires efficient, healthy animal production is driving systematic parasite control program adoption in farming systems that previously relied on traditional or no treatment approaches.

Animal Parasiticides Market Restraints:

Anthelmintic resistance development and regulatory burden creating animal parasiticides market challenges globally

The Animal Parasiticides Market faces a fundamental biological challenge that no commercial strategy can fully resolve parasites evolve resistance to the drugs used against them. Anthelmintic resistance — documented across all major drug classes (benzimidazoles, levamisole, macrocyclic lactones) in sheep and cattle gastrointestinal nematodes across virtually every livestock-producing country — is reducing the efficacy of established parasiticide programs and demanding rotation strategies, reduced-treatment approaches, and investment in novel drug classes whose development pipeline is limited. Companion animal flea resistance to older pyrethroid and organophosphate compounds has already created the commercial opening for isoxazoline innovation — demonstrating the market disruption that resistance creates for established products while sustaining innovation investment that resistance pressure incentivizes.

Animal Parasiticides Market Opportunities:

Novel drug class development and aquaculture parasiticide demand creating significant animal parasiticides market growth opportunities globally

Novel parasiticide drug class development addressing antiparasitic resistance through mechanisms of action distinct from existing chemical classes represents the animal health industry's most strategically important pipeline opportunity. Merial's (Boehringer Ingelheim) isoxazoline discovery fundamentally changed the companion animal ectoparasiticide market by introducing a new mechanism GABA-gated chloride channel modulation that parasites had not previously encountered and therefore lacked resistance mechanisms against. The next novel mechanism discovery will similarly create a premium market position for the innovating company while sustaining clinical efficacy for the generation of products following the initial launch. Aquaculture parasiticide development particularly for Atlantic salmon sea lice represents a rapidly growing market segment whose combination of animal welfare, food safety, environmental regulatory, and producer economic pressures creates premium willingness-to-pay for effective treatments.

Recent Developments:

-

2026: Zoetis launched Simparica Trio Plus — a next-generation combination parasiticide combining sarolaner, moxidectin, and pyrantel with an expanded gastrointestinal parasite spectrum covering whipworm, hookworm, and roundworm species that the original Simparica Trio's pyrantel component missed in some clinical presentations — achieving FDA approval and targeting the premium end of the U.S. companion animal combination parasiticide market where comprehensive gastrointestinal coverage alongside flea, tick, and heartworm protection commands the highest per-dose pricing.

-

2025: Elanco Animal Health received European Medicines Agency approval for Credelio Plus — a combination lotilaner and milbemycin oxime oral chewable providing flea, tick, and heartworm prevention alongside gastrointestinal parasite control in a monthly chewable for dogs — completing the major isoxazoline companies' introduction of combination oral parasiticide products and triggering a competitive response from Zoetis and MSD Animal Health in the European companion animal parasiticide market.

-

2025: MSD Animal Health (Merck) launched Bravecto Long-Acting Injectable — a fluralaner injectable formulation providing 4-month flea and tick protection from a single veterinary-administered injection — targeting companion animal owners whose oral product compliance is inconsistent due to pet non-acceptance of oral chewables, introducing an alternative delivery route that extends Bravecto's reach to the compliance-challenged segment of the companion animal parasite prevention market.

Animal Parasiticides Market Key Players

Some of the Animal Parasiticides Market Companies

-

Zoetis Inc.

-

Merck & Co. Inc. (MSD Animal Health)

-

Boehringer Ingelheim Animal Health GmbH

-

Elanco Animal Health Inc.

-

Virbac SA

-

Vetoquinol SA

-

Ceva Santé Animale

-

Bayer AG (now Elanco)

-

Phibro Animal Health Corporation

-

Norbrook Laboratories Ltd.

-

Bimeda Inc.

-

SeQuent Scientific Ltd.

-

Chanelle Pharma Group

-

Dechra Pharmaceuticals plc

-

Ecuphar NV

-

Hester Biosciences Ltd.

-

Kyoritsu Seiyaku Corp.

-

Ourofino Saúde Animal

-

Lallemand Animal Nutrition

-

ICB Pharma Ltd.

Animal Parasiticides Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.24 Billion |

| Market Size by 2035 | USD 22.6 Billion |

| CAGR | CAGR of 6.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Ectoparasiticides, Endoparasiticides, Endectocides) • By Animal Type (Companion, Livestock) • By Distribution Channel (Veterinary Hospitals & Clinics, Pharmacies, E-commerce, Others [pet stores, etc.]) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zoetis Inc., Merck & Co. Inc. (MSD Animal Health), Boehringer Ingelheim Animal Health GmbH, Elanco Animal Health Inc., Virbac SA, Vetoquinol SA, Ceva Santé Animale, Bayer AG (now Elanco), Phibro Animal Health Corporation, Norbrook Laboratories Ltd., Bimeda Inc., SeQuent Scientific Ltd., Chanelle Pharma Group, Dechra Pharmaceuticals plc, Ecuphar NV, Hester Biosciences Ltd., Kyoritsu Seiyaku Corp., Ourofino Saúde Animal, Lallemand Animal Nutrition, ICB Pharma Ltd. |

Frequently Asked Questions

Ans: The Animal Parasiticides Market was valued at USD 12.24 billion in 2025.

Ans: Asia Pacific dominated; North America is expected to register the fastest CAGR through 2035.

Ans: Veterinary Hospitals & Clinics dominated with approximately 58.30% share; Online Channels growing fastest.

Ans: Ectoparasiticides dominated with approximately 43.26% share in 2025.

Ans: The Animal Parasiticides Market is expected to grow at a CAGR of 6.32% from 2026 to 2035.

Get in Touch