Anime Market Report Scope & Overview:

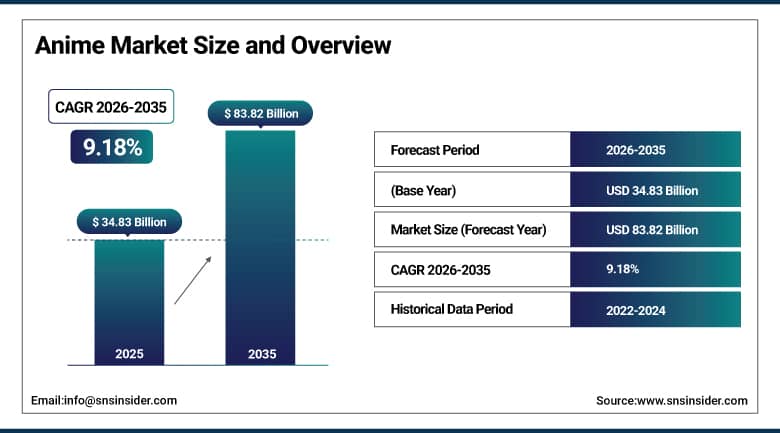

The Anime Market was valued at USD 34.83 billion in 2025 and is expected to reach USD 83.82 billion by 2035, growing at a CAGR of 9.18% from 2026–2035.

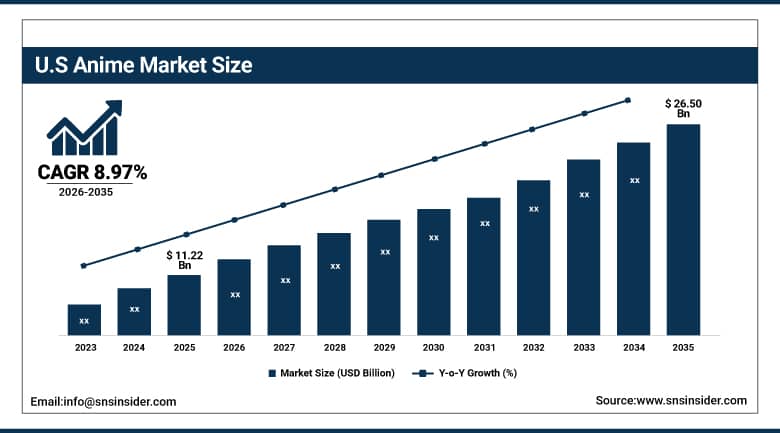

Anime has firmly crossed from cultural export to global entertainment mainstream. Streaming giants including Netflix, Crunchyroll, and Disney+ now compete actively for exclusive licences, funding original productions and delivering simultaneous multi-language releases to fans on every continent. Japan's revised Cool Japan strategy targets quadrupling overseas content revenue to JPY 20 trillion by 2033, giving studios strong government backing to scale global operations. U.S. revenue alone stood at USD 11.22 billion in 2025 and is projected to reach USD 26.50 billion by 2035. Merchandise, theatrical events, and immersive fan experiences are amplifying the revenue base well beyond subscriptions.

Anime Market Size and Forecast

-

Market Size in 2025: USD 34.83 Billion

-

Market Size by 2035: USD 83.82 Billion

-

CAGR: 9.18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Anime Market - Request Free Sample Report

Anime Market Trends

-

Simultaneous world premieres, helping fans in over 190 countries enjoy new episodes within hours of their first broadcast in Japan.

-

AI-powered animation production systems alleviating staffing problems and letting smaller studios compete with the big leagues in terms of quality and output schedule.

-

Anime movie theatres becoming huge money makers around the world, with Sony identifying Demon Slayer as one of its top revenue generators for Q2 2025.

-

High-end merchandise and collectible figures as well as a fan convention business model generating varied sources of income and decreasing dependence on subscribers.

-

The VR and AR technologies allowing fans to become part of the storylines and thus providing an entirely new format of anime content creation.

-

Fan networks on social media contributing to the spread of word-of-mouth advertising, with franchise-related hashtags trending globally on release dates without any need for paid advertising campaigns.

-

Earnings from overseas markets becoming higher than in Japan itself in 2024 based on figures from the Association of Japanese Animations.

U.S. Anime Market Size Outlook:

The U.S. Anime Market was valued at USD 11.22 billion in 2025 and is expected to reach USD 26.50 billion by 2035 at a CAGR of 8.97%, driven by subscription-based streaming growth, exclusive content deals, immersive fan events, and accelerating adoption across younger demographics who consume anime as primary entertainment.

Anime Market Segment Insights

-

By Format, Television Anime has the highest market share with approximately 28%, owing to episodic formats and the commitment of the audience on television channels; Internet Distribution is the rapidly growing format with an annual growth rate of more than 13%. The new mode of consumption, i.e., Internet distribution, has replaced the traditional consumption method of television viewing.

-

By Genre, Action & Adventure is the most profitable genre owing to its high market share and storyline based on universal concepts, including combat, as well as franchise extension; Sci-Fi & Fantasy is the fast-growing genre with a high degree of engagement with its fictional universe.

-

By Revenue Source, Merchandise is the largest revenue source for anime, accounting for approximately 31% in 2025, as it uses IP rights by means of apparel, figures, and merchandise; Subscription Services is the fastest-growing revenue source due to competitive streaming services.

By Type: Television Anime dominates, Internet Distribution grows fastest

Television anime retains its position at the top of the type table because it produced the medium's foundational franchises, commands dedicated broadcast slots backed by advertising revenue, and maintains cultural prestige in Japan that influences production decisions globally. Strategic programming blocks such as Nippon TV's Friday Anime Night reinforce television's ongoing commercial relevance. Internet distribution is the segment changing the market's structural shape. When a new season drops on Crunchyroll or Netflix simultaneously across dozens of countries, audience figures and social conversation volumes dwarf anything broadcast television can achieve. Platforms are funding original productions directly, bypassing traditional studio broadcast cycles entirely, which is reshaping how anime content gets commissioned, budgeted, and released.

By Genre: Action and Adventure dominates, Sci-Fi and Fantasy grows fastest

Action and adventure anime travels exceptionally well across cultural borders. The narrative appeal of characters overcoming adversity through strength, strategy, and personal growth translates with minimal localisation effort, which is why studios and platforms consistently back large-scale action franchises as commercial anchors. Sci-fi and fantasy is growing fastest because streaming platforms are investing in complex universe-building projects that reward long-term viewer commitment. When a platform delivers an original sci-fi anime series, subscribers who invest in multi-season arcs churn far less than casual viewers. Producers are responding with increasingly ambitious world-building projects featuring artificial intelligence, space exploration, and supernatural ecosystems designed specifically to sustain subscriber engagement over multiple years.

By Revenue Stream: Merchandise dominates, Streaming Subscriptions grow fastest

Character-based merchandise turns audience love into purchase decisions across apparel, collectible figures, stationery, home goods, and accessories in ways that scale with franchise popularity rather than content release schedules. A popular character generates merchandise revenue continuously rather than only during broadcast windows. Streaming subscription revenue is growing fastest because the number of paying anime streaming subscribers is rising rapidly across North America, Europe, and Southeast Asia, and platforms are demonstrating willingness to increase subscription prices as content libraries improve. Exclusive original anime productions are a key subscription retention tool, making platform investment in anime content a compounding commercial strategy.

Anime Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~82% |

|

Europe |

United Kingdom |

~28% |

|

Asia Pacific |

Japan |

~65% |

|

Middle East & Africa |

UAE |

~27% |

|

Latin America |

Brazil |

~44% |

Asia Pacific Anime Market Insights

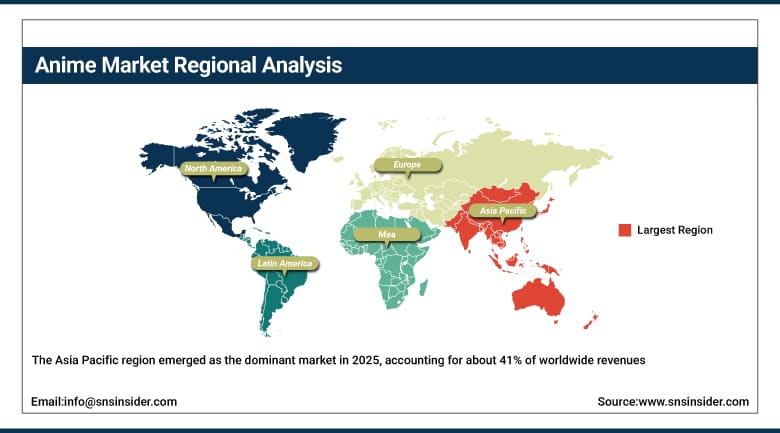

The Asia Pacific region emerged as the dominant market in 2025, accounting for about 41% of worldwide revenues, thanks to its sophisticated production system and rapidly increasing demand in China, South Korea, and India. The Japanese animation studios and IP have no equals, while China has built an extensive digital platform infrastructure, enabling it to become a strong second market for Japanese anime and domestically produced animation.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Anime Market Insights

North America is growing at the fastest regional CAGR, projected at approximately 15.6% through 2035 by multiple analysts. The U.S. market benefits from mature streaming infrastructure, high willingness to pay for premium content subscriptions, and mainstream cultural acceptance of anime across demographics previously considered outside the core fan base.

Europe Anime Market Insights

Europe is a large and ever-growing market that boasts strong communities of fans especially in France, Germany, United Kingdom, and Spain. Anime on Crunchyroll and Netflix services have been increased in Europe, while the localized license holders produce dubbed versions of anime in other European languages.

Latin America and MEA Anime Market Insights

Latin America and MEA are emerging high-growth regions. Brazil leads Latin American revenues at approximately 44% of the regional share, supported by a passionate fan community and growing convention culture. Streaming platform availability in Spanish, Portuguese, and Arabic is converting previously underserved audiences into paying subscribers.

Anime Market Growth Drivers:

-

Global streaming platform competition for exclusive anime licences driving production investment and audience expansion simultaneously across all major markets.

With competition among Netflix, Crunchyroll, and Disney+ for the same shows, licence prices become very expensive and, therefore, lead to a larger profit margin for the studios, allowing them to produce high-quality animations. With more money involved in the production, the animation quality gets improved and new customers attracted, further raising the prices charged for licences. Over the years, this process has only been speeding up and there are no signs of it slowing down because of anime being considered a high-retention form of entertainment compared to live-action films.

In October 2025, the Association of Japanese Animations said that overseas anime revenues had increased by 26% year-over-year to reach JPY 2.17 trillion in 2024, indicating the fact that international sales became greater than sales within Japan. The success comes as proof of the efforts put into developing international strategies over the last ten years and shows that anime has a long way to go internationally in Asia, Americas, Europe, and the Middle East.

Anime Market Restraints

-

Production pipeline bottlenecks in Japan straining the industry's ability to meet accelerating global demand without compromising animation quality standards.

Professional animators, directors, and voice actors are still found mostly in Japan, where it has taken decades for their production chain to evolve. There is increasing global demand for their expertise, but training schools have not been able to keep up with the growing demand, resulting in some scheduling and quality problems.

Anime Market Opportunities

-

AI-assisted production tooling, global co-productions, and emerging market platform expansion presenting three converging growth opportunities for the industry.

AI-driven composition, in-betweening, and background creation are already saving per-episode costs at progressive studios, freeing up budget for the design of characters and storytelling. Joint production among Japanese studios and their Western or Korean counterparts is broadening creative perspectives as well as tapping new sources of manpower. In developing countries where smart phones are spreading fast and anime content was previously unavailable due to linguistic or cost-related issues, localization efforts for the various platforms are turning large dormant audiences into paying customers at increasing speeds.

Recent Developments:

-

April 2025: Sunrise debuted Maebashi Witches on Tokyo MX and licensed the series worldwide through Crunchyroll, expanding its global pipeline of international licenses for its original properties.

-

March 2025: Studio Ghibli restored Princess Mononoke in 4K and IMAX quality for global release, illustrating the value proposition in restoring classic anime movies to generate global theatrical events with existing international fan bases.

-

Second quarter 2025: Sony identified the theatrical launch of Demon Slayer: Infinity Castle as an important revenue source, confirming anime movies as viable global box office events equivalent to live action movies.

-

February 2025: The Japanese government updated its Cool Japan policy with the objective of quadrupling overseas content sales to JPY 20 trillion by 2033, indicating that structural government policy will back up global anime distribution growth.

-

2024: Toei Animation enhanced consumer interaction programs in China, recording increased merchandising revenues with the implementation of an event and e-commerce-focused anime distribution model targeting the Chinese market.

Anime Market Key Players

-

Toei Animation Co. Ltd.

-

Studio Ghibli Inc.

-

MAPPA Co. Ltd.

-

Kyoto Animation Co. Ltd.

-

Sunrise Inc. (Bandai Namco Filmworks)

-

Production I.G Inc.

-

MADHOUSE Inc.

-

A-1 Pictures Inc. (Aniplex)

-

Bones Inc.

-

Pierrot Co. Ltd.

-

TMS Entertainment Co. Ltd.

-

David Production Co. Ltd.

-

CloverWorks Inc.

-

Wit Studio Co. Ltd.

-

Crunchyroll LLC (Sony)

-

Netflix Inc.

-

Aniplex Inc.

-

Kadokawa Corporation

-

Bandai Namco Entertainment Inc.

-

OLM Inc.

Anime Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 34.83 Billion |

| Market Size by 2035 | USD 83.82 Billion |

| CAGR | CAGR of 9.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Television Anime, Movie, Streaming/Internet Distribution, Video/OVA, Music, Live Entertainment, Others) • By Genre (Action and Adventure, Sci-Fi and Fantasy, Romance and Drama, Sports, Others) • By Revenue Stream (Merchandise, Streaming Subscriptions, Licensing, Home Video, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Toei Animation Co. Ltd., Studio Ghibli Inc., MAPPA Co. Ltd., Kyoto Animation Co. Ltd., Sunrise Inc. (Bandai Namco Filmworks), Production I.G Inc., MADHOUSE Inc., A-1 Pictures Inc. (Aniplex), Bones Inc., Pierrot Co. Ltd., TMS Entertainment Co. Ltd. OLM Inc., David Production Co. Ltd., CloverWrks Inc., Wit Studio Co. Ltd., Crunchyroll LLC (Sony), Netflix Inc., Aniplex Inc., Kadokawa Corporation Bandai Namco Entertainment Inc |

Frequently Asked Questions

The Anime Market is expected to grow at a CAGR of 9.18% from 2026 to 2035.

The Anime Market was valued at USD 34.83 billion in 2025.

Television Anime dominated the market in 2025 with approximately 28% of global revenues, sustained by its legacy of foundational franchises, consistent episodic storytelling, and dedicated broadcast loyalty across Japan and East Asia.

Streaming Subscriptions are the fastest-growing revenue stream as platform competition for exclusive anime content drives investment in original productions, simultaneous global releases, and multi-language localisation that convert new audiences into paying subscribers.

Asia Pacific dominated the Anime Market in 2025 with approximately 41% of global revenues, anchored by Japan's unparalleled studio ecosystem and supported by rapidly rising consumption across China, South Korea, and India.

Get in Touch