Artificial Blood Vessels Market Report Scope & Overview:

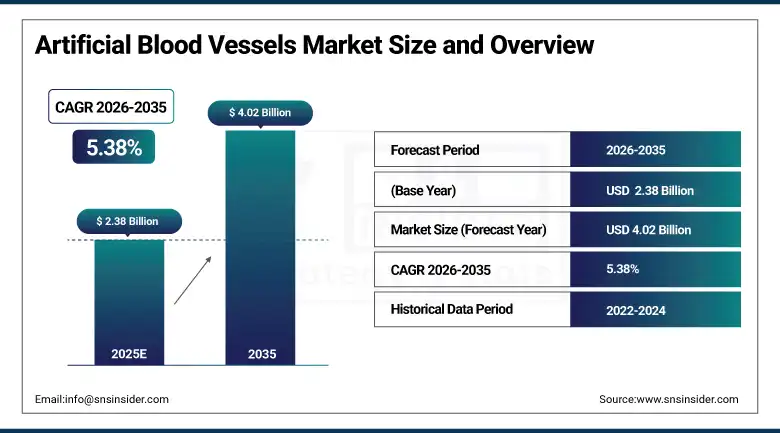

The Artificial Blood Vessels Market was valued at USD 2.38 Billion in 2025 and is expected to reach USD 4.02 Billion by 2035, growing at a CAGR of 5.38% over the forecast period of 2026–2035.

Artificial blood vessels synthetic or bioengineered conduits used to replace or bypass diseased or damaged native vessels occupy a well-defined and durable niche within the broader medical device landscape. Their clinical rationale is clear: when a patient's own vessels are unsuitable for grafting due to prior harvesting, disease, or inadequate diameter synthetic alternatives fill the gap. That has been true for decades, and the clinical case for them has not weakened. What has changed is the patient population size and the complexity of the procedures being performed. Cardiovascular and peripheral vascular disease burdens are rising globally, driven by ageing demographics and the sustained prevalence of obesity, type 2 diabetes, and hypertension all of which are independent risk factors for arterial disease. Each of those patients who reaches the point of needing bypass surgery or vascular reconstruction represents a potential demand event for an artificial graft.

In February 2025, cardiovascular research institutes published data showing that next-generation polymer-based vascular grafts achieved long-term patency rates exceeding 85% in peripheral artery bypass procedures a result that, if replicated at scale, would materially strengthen the case for synthetic grafts over autologous vein alternatives in a broader range of patients.

Artificial Blood Vessels Market Size and Forecast:

-

Market Size in 2025: USD 2.38 Billion

-

Market Size by 2035: USD 4.02 Billion

-

CAGR: 5.38% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Artificial Blood Vessels Market - Request Free Sample Report

Artificial Blood Vessels Market Trends:

-

Bioengineered and polymer-based vascular grafts with anti-thrombogenic surface coatings are gaining clinical traction, particularly in small-diameter applications where conventional ePTFE and polyester grafts have historically underperformed.

-

Tissue-engineered vascular grafts combining decellularised biological matrices with synthetic polymers are advancing through clinical and preclinical evaluation, offering the prospect of grafts that actively recruit host cells and reduce long-term immunological complications.

-

Hemodialysis access is emerging as one of the faster-growing application areas, as the global dialysis population expands and the limitations of native arteriovenous fistulas in certain patient groups make synthetic grafts a more practical default choice.

-

Nanotechnology-enabled surface treatments are being applied to graft materials to reduce bacterial adhesion and mitigate infection risk historically one of the most serious complications of synthetic vascular implants.

-

Regenerative medicine approaches using autologous stem cells seeded onto biodegradable scaffolds are moving from academic proof-of-concept studies toward early-stage clinical investigation in select patient populations.

-

Minimally invasive vascular reconstruction techniques are increasing the volume of procedures performed in outpatient and ambulatory settings, expanding the distribution channels through which artificial grafts reach patients.

-

Cardiovascular surgical capacity is expanding in Southeast Asia, the Middle East, and parts of Latin America, creating new market access points that were not commercially significant for graft manufacturers five years ago.

U.S. Artificial Blood Vessels Market Insights:

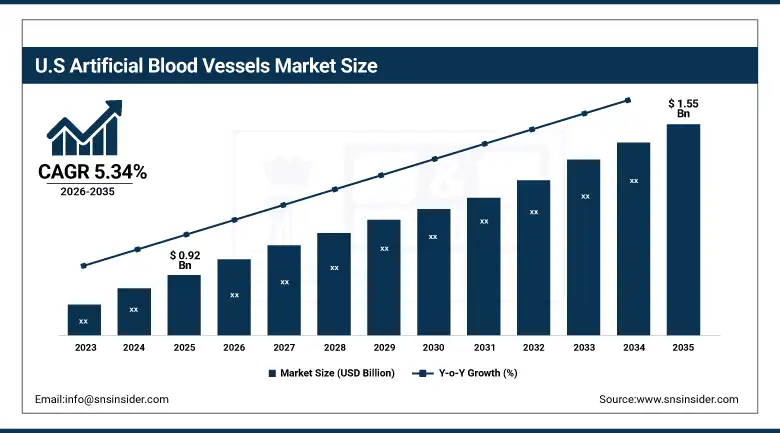

The U.S. Artificial Blood Vessels Market was estimated at USD 0.92 Billion in 2025 and is expected to reach USD 1.55 Billion by 2035, growing at a CAGR of 5.34% from 2026 to 2035.

The United States holds the largest individual country share of the global artificial blood vessels market, and the reasons are not complicated. The U.S. performs more cardiovascular procedures per capita than virtually any other country, supported by a healthcare system that maintains broad access to surgical intervention for vascular disease. Reimbursement for coronary artery bypass grafting, peripheral artery bypass, and aortic repair is well-established within Medicare, Medicaid, and major private insurance frameworks, which keeps procedure volumes from being constrained by payer resistance. The domestic presence of companies like W. L. Gore, Medtronic, and LeMaitre Vascular ensures that the latest graft technologies reach U.S. hospital systems ahead of most other markets.

Artificial Blood Vessels Market Growth Drivers:

Rising Cardiovascular and Peripheral Artery Disease Burden as the Primary Demand Driver

Cardiovascular disease remains the leading cause of death globally, and the numbers have not been moving in a favourable direction. The global burden measured in procedure volumes, hospital admissions, and mortality has grown as populations in developing economies adopt risk-factor-laden lifestyles faster than healthcare systems can respond with preventive care. Peripheral artery disease, in particular, tends to be underdiagnosed until it reaches a severity requiring surgical intervention. By the time a patient reaches a vascular surgeon for bypass consideration, the native vessels are often in poor enough condition that synthetic grafts are the more practical option.

In April 2025, cardiovascular surgery centres reported a 28% increase in peripheral artery bypass procedures using synthetic vascular grafts compared to the prior year a jump that reflects both growing disease burden and improving surgeon confidence in the reliability of current synthetic graft materials.

Artificial Blood Vessels Market Growth Restraints:

Thrombosis, Infection Risk, and the Regulatory Hurdle for Implantable Devices

Artificial blood vessels have a well-documented Achilles heel: the smaller the diameter, the harder it is to maintain long-term patency without thrombosis. In large-diameter aortic applications, synthetic grafts perform very well. In small-diameter peripheral bypass, particularly below the knee, thrombosis rates with standard synthetic materials have historically been high enough that surgeons prefer autologous saphenous vein when it is available. This limitation is well-known and is the central target of current material science and surface treatment R&D, but it has not yet been solved to a degree that eliminates the clinical preference for native tissue in those settings.

Artificial Blood Vessels Market Growth Opportunities:

Tissue-Engineered and Biohybrid Grafts as the Next Clinical Frontier

The most compelling opportunity in this market sits at the intersection of materials science, cell biology, and vascular surgery. Tissue-engineered vascular grafts constructs that combine a synthetic or biological scaffold with living cells to produce a graft that behaves more like native tissue than a passive synthetic conduit have been in development for two decades. What is different now is that the enabling science has matured to a point where clinical translation looks genuinely achievable in the medium term. Decellularisation techniques that strip donor tissue of its immunogenic components while preserving the structural extracellular matrix, combined with improved cell seeding protocols, are producing graft constructs that animal and early human studies show can support endothelial cell colonization and functional integration with host tissue.

In January 2025, researchers reported the successful development of a bioengineered vascular graft capable of supporting natural endothelial cell growth within weeks of implantation an early but meaningful indication that the cell-seeded scaffold approach is producing results that may support regulatory pathway conversations in the near term.

Artificial Blood Vessels Market Segment Analysis:

-

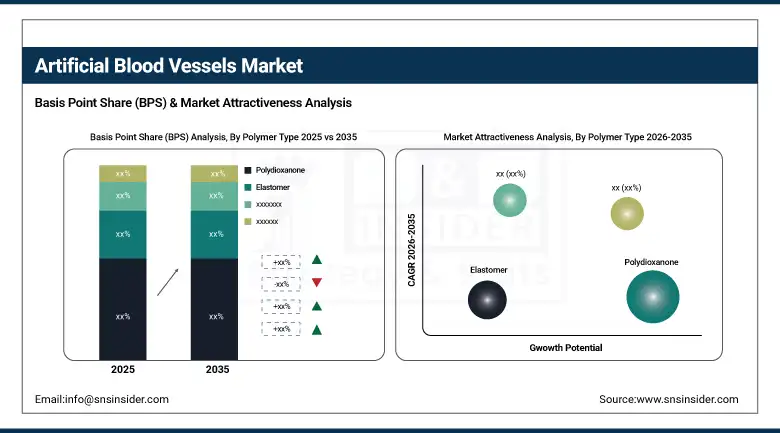

By Polymer Type: Polyethylene terephthalate held the largest share of 39.42% in 2025; elastomer-based grafts are anticipated to exhibit the fastest growth at a CAGR of 6.12%.

-

By Application: Peripheral artery disease held the largest market share of approximately 41.35% in 2025; the hemodialysis segment is expected to register the highest CAGR of 6.48%.

-

By End-User: Hospitals dominated with a share of nearly 54.27% in 2025; ambulatory surgical centres are expected to witness the fastest growth at a CAGR of 6.05%.

By Application: Peripheral Artery Disease Leads; Hemodialysis Grows Fastest

Peripheral artery disease held a 41.35% revenue share in 2025, and the structural reasons for that concentration are straightforward. Peripheral bypass is one of the highest-volume vascular surgical procedures globally, and synthetic grafts are routinely used when the saphenous vein is unavailable, has been previously harvested, or is of inadequate quality. The patient population driving this demand is large and growing: diabetes and obesity independently accelerate peripheral arterial disease, and both conditions are increasing in prevalence across essentially every major market. The hemodialysis segment is forecast at a 6.48% CAGR the fastest of any application category. Chronic kidney disease prevalence is rising globally, and dialysis is a long-term treatment for a substantial and growing patient population.

By Polymer Type: Polyethylene Terephthalate Leads; Elastomers Gain Ground

Polyethylene terephthalate marketed under brand names including Dacron captured 39.42% of the polymer-type segment in 2025. PET has earned its market position through decades of reliable clinical performance in large-diameter aortic and iliac applications. Its mechanical properties are well-characterised, surgeons are experienced in handling and implanting it, and its long-term durability record gives clinicians confidence in its use in patients expected to live for many years post-procedure. Elastomer-based grafts are the fastest-growing polymer category at 6.12% CAGR, driven by the logic that a graft material whose mechanical behaviour more closely matches native arterial wall compliance should produce better haemodynamic outcomes.

By End-User: Hospitals Lead; Ambulatory Surgical Centres Grow Fastest

Hospitals held a 54.27% end-user share in 2025, which reflects the complexity of the procedures that dominate current artificial graft utilisation. Aortic aneurysm repair, complex peripheral bypass involving multiple anastomoses, and haemodialysis graft placement in high-comorbidity patients all require the surgical infrastructure, anesthetic capabilities, intensive care backup, and specialist nursing that only hospital settings can reliably provide. Ambulatory surgical centres are forecast to grow at 6.05% CAGR, the fastest of the end-user categories. The driver is the ongoing migration of lower-complexity vascular procedures to outpatient settings a trend that is part clinical, part economic. For straightforward haemodialysis access placements, certain peripheral angioplasty procedures, and some secondary graft revisions, ambulatory centres can deliver equivalent clinical outcomes at substantially lower cost per procedure.

Artificial Blood Vessels Market Regional Highlights:

North America Artificial Blood Vessels Market Insights:

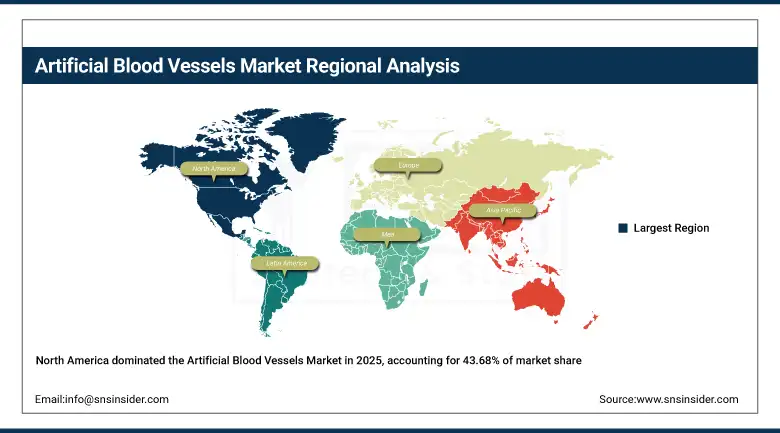

North America accounted for approximately 43.68% of global market revenue in 2025 the largest regional share by a clear margin. The U.S. contribution dominates: high cardiovascular procedure volumes, favourable reimbursement for surgical vascular intervention, and the domestic presence of most of the world's leading vascular graft manufacturers combine to create a procurement environment with few parallels. FDA 510(k) and PMA pathways for vascular devices, while demanding, are well-understood by incumbent manufacturers, which maintains a structured but functional innovation pipeline. Canada adds a complementary demand stream through its publicly funded cardiovascular surgery system, though at considerably smaller absolute volumes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Artificial Blood Vessels Market Insights:

Asia Pacific is forecast to be the fastest-growing regional market at a CAGR of 6.21% through 2035. The growth mechanics are distinct from North America's. In China, cardiovascular disease incidence has risen sharply as dietary and lifestyle patterns have shifted over two generations, and the healthcare system is expanding surgical capacity to meet that demand. Japan has an older population than almost any other country globally, creating substantial and consistent vascular surgery volumes. India's market is earlier-stage but developing a large unmet need, a growing private hospital sector with cardiovascular surgical capability, and improving medical device import and regulatory pathways are all moving in the right direction for international graft manufacturers looking to establish commercial footholds.

Europe Artificial Blood Vessels Market Insights:

Europe is the second-largest regional market, characterised by relatively high per-capita procedure volumes in western European countries and a strong domestic biomedical engineering research base. Germany, France, the UK, and the Netherlands are the primary markets within the region. European academic medical centres have been active contributors to clinical evaluation of next-generation graft technologies, and several tissue-engineering programmes with clinical-stage ambitions are based in European universities. The MDR regulatory framework for medical devices which replaced the older MDD has raised the bar for clinical evidence requirements, which has created short-term friction for some device manufacturers but should improve the long-term quality and credibility of the evidence base for devices reaching European markets.

Latin America (LATAM) and Middle East & Africa (MEA) Artificial Blood Vessels Market Insights:

Latin America and MEA are smaller markets currently but represent genuine longer-term growth opportunities as healthcare infrastructure investment continues. Brazil leads in Latin America, with a public healthcare system that performs a meaningful volume of cardiovascular surgeries and a private hospital sector that is actively upgrading surgical capabilities. Mexico, Colombia, and Argentina are secondary markets with growing private cardiovascular surgical infrastructure. In the Middle East, the UAE and Saudi Arabia are investing heavily in tertiary medical centre development that includes cardiovascular surgical capability, and international medical device manufacturers are establishing commercial presence in those markets. South Africa and Egypt lead the MEA region outside the Gulf. In both Latin America and MEA, cost sensitivity is a real purchasing consideration, which favours established PET and ePTFE graft products over premium next-generation options in many procurement decisions.

Artificial Blood Vessels Market Competitive Landscape:

W. L. Gore & Associates is a global medical technology company known for developing advanced implantable medical devices and biomaterial-based solutions. The company is widely recognized for its vascular graft products used in cardiovascular surgery and dialysis access procedures. Its artificial blood vessels, primarily made from expanded polytetrafluoroethylene (ePTFE), are designed to provide durability, biocompatibility, and long-term patency. Gore focuses on continuous innovation in biomaterials and vascular technologies to support improved outcomes in cardiovascular and peripheral vascular treatments worldwide.

-

2022: L. Gore & Associates expanded its vascular graft product portfolio to support advanced cardiovascular and peripheral vascular surgical procedures.

Terumo Corporation is a global healthcare company specializing in cardiovascular systems, medical devices, and vascular graft technologies. The company develops synthetic and bioengineered artificial blood vessels used in cardiovascular and endovascular procedures such as bypass surgery and vascular repair. Terumo focuses on innovation in polymer-based materials and minimally invasive vascular technologies to enhance surgical precision and patient outcomes across global healthcare markets.

-

2023: Terumo Corporation strengthened its cardiovascular product portfolio by advancing the development and global distribution of its vascular graft and interventional systems.

Getinge AB is a leading medical technology company that provides advanced solutions for surgical procedures, intensive care, and cardiovascular treatment. The company offers vascular grafts and surgical implants used in complex cardiovascular and vascular reconstruction procedures. Getinge focuses on delivering high-quality biomaterials and innovative surgical technologies that enhance patient safety and improve treatment outcomes in hospitals and healthcare facilities worldwide.

-

2023: Getinge AB continued investing in research and development to enhance its cardiovascular surgical solutions, including advanced vascular graft technologies.

Artificial Blood Vessels Market Key Players:

-

L. Gore & Associates

-

Terumo Corporation

-

Getinge AB

-

Braun Melsungen AG

-

Medtronic

-

Becton Dickinson (BD)

-

Abbott Laboratories

-

Cook Medical

-

Artivion Inc.

-

Edwards Lifesciences

-

Baxter International

-

Cardinal Health

-

Endologix

-

MicroPort Scientific Corporation

-

Meril Life Sciences

-

Lombard Medical

-

Vascutek Ltd.

-

JOTEC GmbH

-

Shanghai MicroPort Endovascular MedTech

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.38 Billion |

| Market Size by 2035 | USD 4.02 Billion |

| CAGR | CAGR of 5.38% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Polymer Type (Polydioxanone, Elastomer, Polyethylene Terephthalate, and Others) • By Application (Aortic Disease, Peripheral Artery Disease, and Hemodialysis) • By End-users (Hospitals, Cardiac Catheterization Laboratories, Ambulatory Surgical Centers, Specialty Clinics, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | L. Gore & Associates, Terumo Corporation, Getinge AB, Braun Melsungen AG, LeMaitre Vascular, Medtronic, Becton Dickinson (BD), Abbott Laboratories, Cook Medical, Artivion Inc., Edwards Lifesciences, Baxter International, Cardinal Health, Endologix, MicroPort Scientific Corporation, Meril Life Sciences, Lombard Medical, Vascutek Ltd., JOTEC GmbH, Shanghai MicroPort Endovascular MedTech |

Frequently Asked Questions

The Artificial Blood Vessels Market was valued at USD 2.38 billion in 2025 and is projected to reach USD 4.02 billion by 2035, growing at a CAGR of 5.38% from 2026 to 2035.

Artificial blood vessels, also called synthetic vascular grafts, are used to restore blood flow in patients with arterial blockages, aneurysms, peripheral artery disease, and for hemodialysis access procedures.

Market growth is driven by the rising prevalence of cardiovascular diseases, increasing vascular surgeries, growing aging population, and technological advancements in biomaterials and polymer-based vascular grafts.

North America holds the largest market share due to advanced healthcare infrastructure, high cardiovascular surgery rates, and the strong presence of leading medical device manufacturers.

The hospitals segment dominates the market, accounting for about 54.27% share in 2025, as most complex vascular surgeries and graft implantation procedures are performed in hospital settings.

Get in Touch