Augmented Intelligence Market Report Scope & Overview:

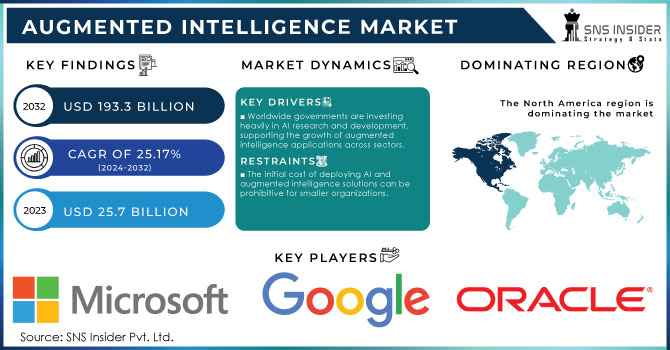

The Augmented Intelligence Market Size was valued at USD 25.7 Billion in 2023 and is expected to reach USD 193.3 Billion by 2032, growing at a CAGR of 25.17% over the forecast period 2024-2032. The augmented intelligence market has experienced considerable growth on a global scale as a result of the governments’ increased focus on digitalization. As of the recent statistics provided by the U.S. Department of Commerce, the federal agencies are planning to allocate approximately $7.5 billion to AI and other technologies in 2023, which marks a 12% increase from 2022 level. The significant investments are aimed at increasing the country’s economy by creating the environment in which artificial intelligence and its augmented variation can flourish. In Europe, the European Union allocated €10 billion to R&D in AI in the framework of the Horizon Europe plan, showing that the union is willing to concentrate on responsible use of AI technologies as one of the leading players globally.

Get More Information on augmented intelligence market - Request Sample Report

Increased investments in AI training programs, regulations, and public-private partnerships in such industries as healthcare, automotive, and finance that are the most regulated are likely to encourage businesses to expand the use of advanced AI-assisted solutions. AI-based virtual assistants help organizations in enhancing the productivity of their customer service specialists and allow them to concentrate on complicated inquiries. As hybrid workforce models are becoming more widespread, the use of AI in combination with human involvement can boost productivity and improve decision-making. Another example of the usage of real-time data processing by AI is the retail sector, which uses this method for management of supplies and understanding of customer needs. Therefore, when artificial and human capacities are combined, innovative solutions can be developed and used to improve business operation in the digital environment. Augmented intelligence described as the collaboration between a computer and a human to produce effective and efficient results. For example, AI will play a critical role in banks and financial institutions, since this human-machine pairing will enable them to process business intelligence and improve employee-customer contact.

Market dynamics

Drivers

-

Worldwide governments are investing heavily in AI research and development, supporting the growth of augmented intelligence applications across sectors.

-

AI-driven solutions improve diagnostics, treatment planning, and operational efficiencies, making augmented intelligence crucial in healthcare.

-

Augmented intelligence enhances collaboration between AI tools and human workers, boosting productivity in hybrid work environments.

-

Businesses are increasingly using sophisticated analytics, smart contracts, machine intelligence, and the Internet of things.

The increased use of AI in healthcare is one of the key factors advancing the growth of the augmented intelligence market. As more and more healthcare organizations are opting for AI solutions to improve patient care, streamline operations, and reduce diagnostic mistakes, the adoption of such solutions should rise. AI algorithms help interpret medical images, patient records, and genetic sequencing to provide more accurate medical diagnostics and personalized treatment plans. For example, it was reported in 2023 by the U.S. Food and Drug Administration that there was a 30% increase in medical devices powered by AI approved for use, compared to the previous year. Such devices help detect different diseases, such as cancer, heart, or neurodegenerative diseases, at an early stage, and with higher accuracy. The use of AI in healthcare also reduces errors made by humans in decisions concerning treatment. According to a study published in 2023 by the British Medical Journal, AI microscopy, whole-slide imaging, and PCR systems helped cut diagnostic errors by 15-20%, particularly in the fields of radiology and pathology. Additionally, the government’s interest in AI solutions for healthcare has been growing, with the European Union having announced to invest over €1.5 billion in 2023 to fund AI research and innovation, where the focus is mostly on healthcare. All these factors help drive the market for augmented intelligence, reflective of the growing adoption of AI in healthcare.

Restraints:

-

The initial cost of deploying AI and augmented intelligence solutions can be prohibitive for smaller organizations.

-

The increased use of AI for processing sensitive data raises concerns about privacy breaches and cybersecurity risks.

-

There is a shortage of professionals with the necessary expertise to implement and manage augmented intelligence systems.

-

Integrating AI into existing systems can be complex and time-consuming, posing challenges for businesses with limited technical capabilities.

One of the significant restraints in the augmented intelligence market is the lack of a competent workforce required to properly run and implement AI-based systems. As AI is developing and becoming more advanced, it creates an increased demand for personnel qualified in artificial intelligence, machine learning, data science etc. However, such specialized personnel is scarce in the job market. According to the World Economic Forum’s 2023 Future of Jobs Report, half of the companies across the globe already deal with the AI skill gaps. In addition, in 2024 recent survey over 57% of organizations reported facing a difficulty in finding a qualified AI talent required to support advanced technology implementation. The issue results in many companies implementing augmented intelligence solutions, not being technically skilled and armed enough to manage them effectively. The need for skilled professionals not only increases operational costs but also slows down the adoption of AI-driven tools, limiting the potential for augmented intelligence to be fully realized in many industries.

Segment analysis

By Component

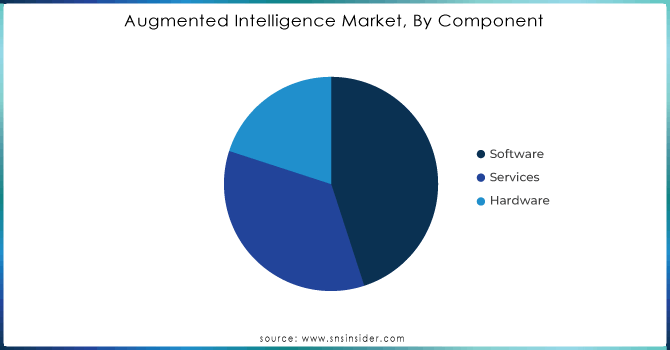

The software segment led the market and held largest share and accounted more than 43% of the revenue share in 2023. The prevalence of software as the major component of augmented intelligence can be attributed to the rapid increase in the demand for more advanced AI-empowered platforms that could enhance human decision-making. Global governments prioritize the integration of AI in their industries, resulting in the increased pace of AI-based software development innovation. Notably, the China Ministry of Industry and Information Technology reported that AI software solutions allowed manufacturers in China to heighten their sector’s efficiency by 20% in 2023 by enabling them to automate sophisticated tasks, improve operational efficiency, and gain the ability to draw data-based insights.

The service segment is projected to grow at the fastest growth rate from 2024 to 2032. The major driving force for the rapid growth of the service share will be the ever-increasing need for consulting, implementation, and training services as companies and organizations struggle with the effective deployment of the new AI solutions. Governments are also playing a crucial role here; the U.K. government’s 2023 AI White Paper emphasizes the need for a skilled workforce and AI literacy to ensure successful implementation, leading to a surge in demand for service providers who offer specialized AI training and support. Therefore, the tendency to high demand for the service providers that offer specialized training along with multifaceted AI solutions will influence the exponential growth of the service segment over the projection period.

Need any customization research on Augmented Intelligence Market - Enquiry Now

By vertical

In 2023, the IT and telecom segment dominated the augmented intelligence market in the based on vertical. This sector accounted for a significant portion of the global market share, driven by its pivotal role in the digital infrastructure and the increased emphasis on AI-driven analytics. According to FCC, in the U.S. telecom industry, the adoption of AI increased by 15% in 2023, specifically in network optimization, customer service automation, and cybersecurity. The telecom companies are utilizing augmented intelligence for operational functions, which allows them to navigate diverse and immense datasets provided by the launch of IoT and 5G networks. The local government’s pressure on the implementation of 5G infrastructure, accompanied by extensive spending on AI-adjunct for network solutions, are the strongest boost for the IT & Telecom vertical. The sector’s ability to adapt quickly to technological advancements further solidifies its position as a key driver in the augmented intelligence market.

Regional Analysis | North America Leads the Market

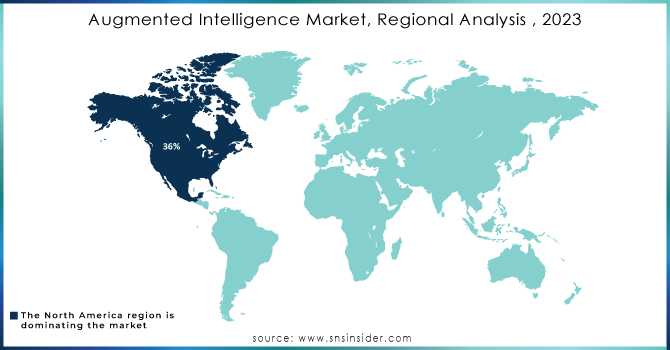

North America dominated the augmented intelligence market, accounted more than 36% share of the global market. The United States government is the main factor for the leading position of North America in the augmented intelligence industry. The National Artificial Intelligence Initiative Office sates that, the U.S. government budgeted a record $13 billion for its efforts in AI research in 2023. Furthermore, North America is a home for various giants like Google, Facebook, IBM, and several independent research institutions supported by the country’s government. The region has one of the best regulations on AI that ensures no misuse of the technology, thus providing a conducive environment for stakeholders to invest in augmented intelligence to public and private sectors. The North American region has also been dominant in augmented intelligence because of the current MG workforce and availability of exposure to the most advanced research in the world. North America’s leading position in this market will continue owing to adequate support from the government and the current high adoption rates in the healthcare, manufacturing, and retail markets.

Asia-Pacific’s market is expected to grow with the higher CAGR in the forecast period of 2024-2032. AI is widely employed in the fintech sector to strengthen digital banking, enhance financial inclusion and manage risk. Furthermore, AI algorithms are employed to evaluate consumer behaviour, credit quality, and transaction history. Through analyzing consumer data, the fintech sector has been able to improve fraud detection, credit ratings, and personalized financial products and services. In Singapore, Hong Kong, and Mumbai, the main financial hubs, banks, startups, and authorities are employing AI to create safe and streamlined financial systems.

KEY PLAYERS:

-

IBM (IBM Watson, IBM Watson Discovery)

-

Microsoft (Microsoft Azure AI, Microsoft Cognitive Services)

-

Google (Google Cloud AI, Google Assistant)

-

Amazon Web Services (AWS) (AWS SageMaker, AWS Lex)

-

Salesforce (Salesforce Einstein, Salesforce Service Cloud)

-

Oracle (Oracle AI Platform, Oracle Autonomous Database)

-

SAP (SAP Leonardo, SAP AI Core)

-

Intel (Intel Nervana, Intel Movidius)

-

NVIDIA (NVIDIA DGX Systems, NVIDIA Clara)

-

Palantir Technologies (Palantir Foundry, Palantir Gotham)

-

Hewlett Packard Enterprise (HPE) (HPE Ezmeral, HPE Nimble Storage)

-

UiPath (UiPath Studio, UiPath Orchestrator)

-

Qualcomm (Qualcomm Snapdragon AI, Qualcomm AI Engine)

-

Cerner Corporation (Cerner Millennium, Cerner HealtheDataLab)

-

OpenText (OpenText Magellan, OpenText Business Network)

-

Adobe (Adobe Sensei, Adobe Experience Cloud)

-

Baidu (Baidu Apollo, Baidu DuerOS)

-

SAS Institute (SAS Viya, SAS Analytics Cloud)

-

Nexar (Nexar AI Dashcams, Nexar Fleet)

and others in final Report.

Salesforce -Company Financial Analysis

| Report Attributes | Details |

| Market Size in 2023 | USD 25.7 Bn |

| Market Size by 2032 | USD 193.3 Bn |

| CAGR | CAGR of 25.17% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Technology (Machine Learning, Natural Language Processing, Context-Aware Computing, Computer Vision, Others) • By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises) • By Vertical (IT and Telecom, BFSI, Healthcare, Manufacturing, Automotive, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amazon Web Services, Inc., International Business Machines Corporation, SAS Institute, Microsoft Corporation, QlikTech International AB, Salesforce.com, Inc., Samsung, SAP SE, Sisense Inc., Adobe, NVIDIA |

| Key Drivers | • Businesses are increasingly using sophisticated analytics, smart contracts, machine intelligence, and the internet of things. |

| Market Opportunities | • The usage of augmented intelligence solutions by large corporations is on the rise. • An increase in the quantity and variety of data inside an automated system. |

Frequently Asked Questions

Ans:- Key Stakeholders Considered in the study are Raw material vendors, Distributors/traders/wholesalers/suppliers, Regulatory authorities, including government agencies and NGO, Importers and exporters etc

Ans:- The major key players are Amazon Web Services, Inc., International Business Machines Corporation, Micron Technology, Inc., Microsoft Corporation, QlikTech International AB, Salesforce.com, Inc., Samsung, SAP SE, Sisense Inc., TIBCO Software Inc.

Ans:- The segments covered in the Augmented Intelligence market report for study are On The Basis of Component, Technology, Organization Size, Industry Vertical etc

Ans:- Businesses are increasingly using sophisticated analytics, smart contracts, machine intelligence, and the internet of things and Increasing usage of digital media in order to satisfy client expectations.

Ans:- The estimated market size for the Augmented Intelligence market for the year 2032 is USD 193.3 Bn.

Get in Touch