High Heat Foam Market Report Scope & Overview

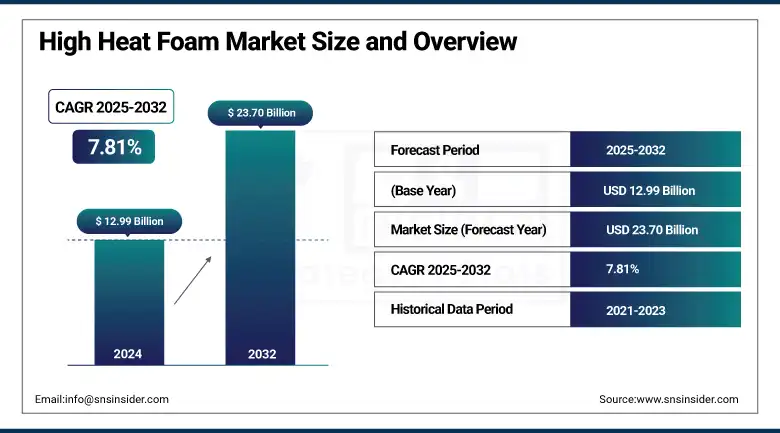

The High Heat Foam Market size was USD 12.99 billion in 2024 and is expected to reach USD 23.70 billion by 2032, growing at a CAGR of 7.81% over the forecast period of 2025-2032.

High heat foam market analysis highlights the growing application of high heat foam in electronics and electrical insulation. Due to shrinking sizes and increasing power of electronic devices and components, efficient thermal management solutions have become even more important. High heat foams with high thermal resistance, high dielectric strength, and flame-retardant capabilities are widely used to protect heat-sensitive components from overheating and electrical interference. Applications for these materials increasingly include circuit boards, insulation for batteries and wires, and electronic equipment housings. Furthermore, as the consumer electronics and electric vehicle industries are growing at a significant pace, high heat foam is expected to witness continuous demand for stable and long-lasting insulation materials.

To Get more information On High Heat Foam Market - Request Free Sample Report

The IIP for electrical equipment manufacturing increased by 108.0 in April 2023 and is expected to jump to 128.2 in March 2024, which indicates that higher production activities can generate demand for high heat foam as an insulation component.

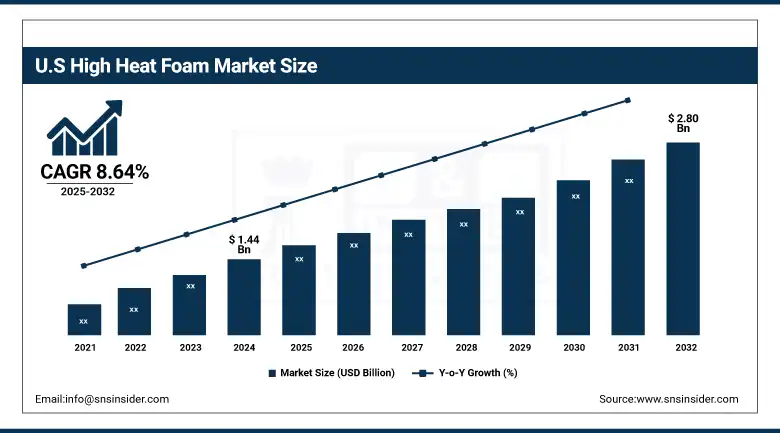

The U.S. high heat foam market size was USD 1.44 billion in 2024 and is expected to reach USD 2.80 billion by 2032 and grow at a CAGR of 8.64% over the forecast period of 2025-2032. It is owing to its advanced industrial infrastructure and high demand in the primary sectors identified above, along with a focus on innovation and product performance; this attribute combined with its wide acceptance across various industries paves way for the growth of the High Heat Foam Market in the U.S. Major automotive and aerospace manufacturers and high heat foam companies stimulate demand for materials with excellent thermal insulation, fire resistance, and lightweight properties. In addition, the strict government regulations regarding energy efficiency and fire safety traction have led for the extensive utilization of high heat foam in building and industrial machinery.

High Heat Foam Market Drivers

-

Rising infrastructure and railway projects drive the market growth.

The high heat foam market is primarily driven by growing infrastructure and satellite projects globally. Transportation infrastructure expansion and modernization efforts around the world have been majorly funded by governments and the private sector alike, resulting in an increased need for advanced materials that provide thermal insulation, fire resistance, and durability. High heat foam is an automotive material extensively employed in railway coaches and infrastructure for acoustic insulation, thermal protection, and vibration dampening. Due to its lightweight and thermal-resistant properties, it will help in improving safety and comfort for the passengers. In addition, the massive-scale high-speed rail system and smart city development drive the demand for this type of reliable and high-performance material, which in turn enables high heat foam market growth.

As of January 2024, Indian Railways has attained 94% of electrification works on its network and aims to complete the remaining 06% by mid-2024. The goal of this is to decrease carbon emissions and enhance energy efficiency.

High Heat Foam Market Restrain

-

Technical challenges related to foam durability under extreme conditions may hamper the market growth.

The growth of the High Heat Foam Market can be hindered by the high technical challenges foam durability due to perturbed conditions. Foams used in high-heat settings are typically subjected to extreme environments that can involve prolonged exposure to elevated temperatures, mechanical stress, and chemical agents. Such deterioration eventually deteriorates the foam structure, which in turn reduces performance in insulation, cushioning, or protection. These durability challenges can lead to higher maintenance expenses, reduced product life cycles, and safety risks, in turn limiting their penetration in essential applications such as aerospace, automotive, and industrial segments.

High Heat Foam Market Opportunities

-

Increasing government incentives for domestic manufacturing and green technologies.

Growth of government incentives for domestic manufacturing and green technologies is one of the high heat foam market opportunities. Governments worldwide are seeking to pivot away from imports, offering subsidies, tax incentives, and policy support to encourage local production and manufacturing. Moreover, because of the increasing focus on sustainability and environmental responsibility across the globe, there is a severe demand for the use of biobased, biodegradable materials and sustainable technologies. These initiatives lend themselves to high heat foams that are recyclable, have or lower environmental impact, or assist with energy efficiency. Such a conducive regulatory framework is prompting manufacturers to leverage innovative, sustainable foam alternatives, which are creating growth opportunities in the market and driving the high heat foam market trends.

Mission of Hydrogen in National Green with an aim to make India a global hub for producing green hydrogen, the mission also includes provisioning for pilot projects in the steel, transport, and shipping sectors. The initiative incentivizes the utilization of renewable energy and encourages the use of green technologies (which resonates well within the High Heat Foam Market).

National Action Plan For Cooling Foundation (NCAP) The NCAP seeks to promote energy-efficient cooling solutions while ensuring sustainable, comfortable atmospheric and thermal conditions for all. This strategy would promote the use of sophisticated insulation materials, including high-heat foams, across multiple sectors for increased energy efficiency and reduced environmental footprint.

High Heat Foam Market Segmentation Analysis

By Raw Material

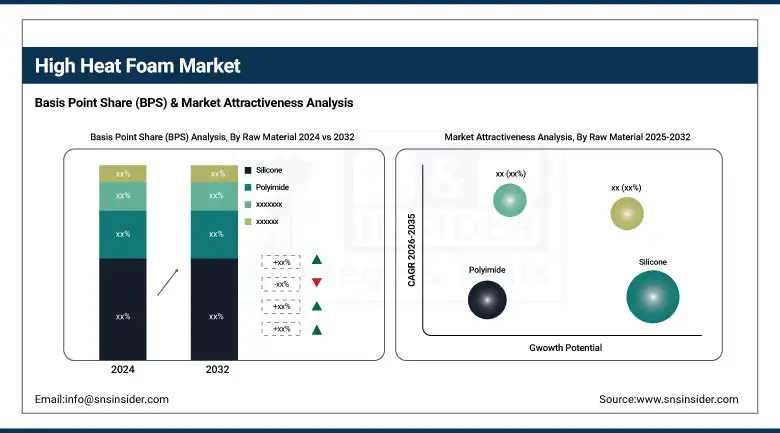

Silicon held the largest high heat foam market share, around 58%, in 2024. It is due to its high thermal stability, ease of processing, durability, and versatility in a wide range of applications. Silicone foams, unlike other foam materials, are also capable of withstanding extremely high temperatures without degrading, which is why they find great application in automotive, aerospace, electronics, and industrial sectors where heat resistance is a key requirement. And with its chemical resistance, flexibility, and high electrical insulation, silicone foam becomes a more attractive solution for harsh environments.

Polyimide held a significant high heat foam market share, which is owing to its high thermal resistance and mechanical stability, which makes it an ideal candidate for high-temperature applications. Withstanding direct exposure of up to 400°C long term, polyimide foam is also a proven material of choice for aerospace, electronics and other industrial applications that value durability and reliability in extreme performance environments. Also, polyimide has a unique combination of mechanical and chemical stability, low dielectric constant, and flame-retardant properties that are often used in electrical insulation and low-density thermal barriers.

By Application

The automotive segment held the largest market share, around 36%, in 2024. It is owing to a rise in demand for lightweight, heat-resistant, and durable materials in vehicle construction. High heat foams are being extensively used in automotive applications, including engine components, thermal and acoustic insulation, seating, and interior parts, solutions that enhance overall fuel economy by lowering the weight of the vehicle, and protection against high temperatures. The increasing use of electric vehicles (EVs) is another factor contributing to the demand for advanced thermal management solutions because high heat foams serve as battery insulation and heat-dispersing mechanisms.

The industrial segment holds a significant market share in the high heat foam market. It is due to a large amount of extreme temperature materials demand that require thermal insulation, fire resistance, and durability in one material. High heat foams are widely used in industries like manufacturing, chemical processing, oil and gas, and power generation to protect equipment, machinery, and infrastructure from heat damage and to increase operational safety. These foams also contribute to the improvement of energy efficiency by reducing heat loss, which is an important aspect of industrial processes. Chemical resistance and the ability of high heat foam to perform well in harsh environments, as well as to keep equipment up and running and workers safe, add greatly to the product's position as the most dominant in the industrial segment.

High Heat Foam Market Regional Outlook

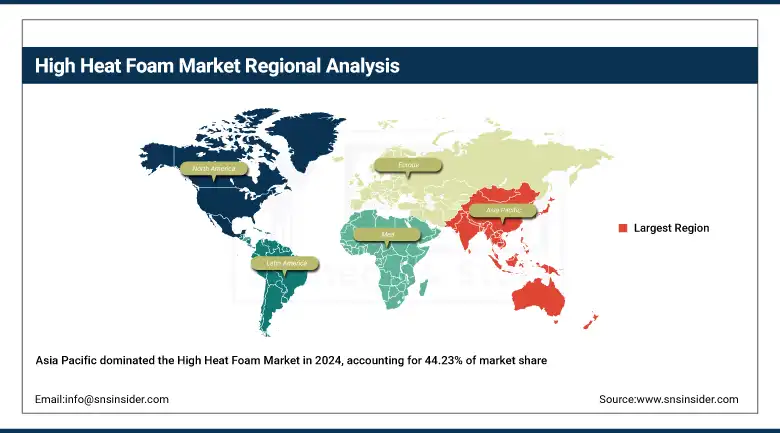

Asia Pacific held the largest market share, around 44.23%, in 2024. It is due to witnessing rapid industrialization, followed by revolutionary urbanization and burgeoning investment opportunities in growing sectors like automotive, electronics, aerospace, and infrastructure. The manufacturing industry in these countries is booming, in turn increasing the demand for advanced materials such as high heat foam for insulation, thermal management, and fire resistance. Moreover, the growing market for electric vehicles and increasing railway modernization projects are major factors boosting the growth of the market. Asia Pacific continues to dominate the market with easy access to raw materials, a large, skilled workforce, and government support for domestic manufacturing and green technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

The government of India is offering several initiatives for increasing the productivity of the country, like the Production-Linked Incentive (PLI) schemes, which are providing USD 26.3 billion to 14 sectors, including electronics, automotive, textiles, etc. Approximately 8 lakh people are expected to get employment through these initiatives, which will also boost the call for high-performance materials.

North America high heat foam market held a significant market share and is the fastest-growing segment in the forecast period. It is owing to a well-established industrial base, high automotive and aerospace manufacturing, and high investment in advanced infrastructure and technologies. High heat foam used as an insulating material is required in many parts of the world due to the stringent regulatory standards imposed in the region concerning energy efficiency, fire safety, and environmental protection. Moreover, growing adoption of electric vehicles and expansion of the electronics sector also contribute to the growth of the market. Both Canada and the United States have substantial investments in R&D and innovation that allow for the development of more sophisticated foams that can hold up in high-temperature applications.

In April 2024, BASF, together with SABIC and Linde, launched the first demonstration facility for electrically heating steam cracking furnaces at BASF's Verbund site in Ludwigshafen, Germany. This plant, three years in the making, will convert renewable electricity into olefins, ethylene, and propylene, reducing CO₂ emissions by more than 90% compared to the traditional production process.

Europe held a significant market share in the forecast period. It is due to the high-tech industry with stringent regulations and high demand for energy-efficient, fire-retardant and even highly liquid materials used across industries and sectors. Manufacturers in automotive and aerospace rely on high-performance foams for thermal insulation, lightweighting, and safety; many leading manufacturers are based in the region. The drive towards sustainable, non-toxic, and thermally stable materials that respond to the stricter building and construction codes in Europe is also expected to drive the demand accordingly. Meanwhile, the move from the European Union towards carbon neutrality, alongside green building initiatives, also speeds the progress of high heat foams in construction and infrastructure applications.

High Heat Foam Market Companies are:

BASF SE, Rogers Corporation, Evonik Industries AG, SABIC, Sekisui Chemical Co., Ltd., Armacell International S.A., Ube Industries Ltd., Zotefoams Plc, JSP Corporation, Sinoyqx

Recent Development:

-

In June 2024, Wacker Chemie AG announced plans to build its second silicone specialty factory in Karlovy Vary, complementing its existing production. This site will also produce high-performance silicones that cure at ambient temperature, as well as high-consistency silicone rubber (from 2028) to further consolidate Wacker as a solutions provider.

-

In July 2023, Solvay and Zotefoams have established a strategic partnership for aerospace applications, to supply polyvinylidene fluoride (PVDF) foam. This partnership is to create closed-cell, crosslinked foams to save weight and vibration and noise control of aircraft interiors.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 12.99 Billion |

| Market Size by 2032 | USD23.70 Billion |

| CAGR | CAGR of 7.81% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Raw Material (Silicone, Polyimide, Melamine, Polyethylene, Others) • By Application (Automotive, Railway, Industrial, Aerospace, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Rogers Corporation, Evonik Industries AG, SABIC, Sekisui Chemical Co., Ltd., Armacell International S.A., Ube Industries Ltd., Zotefoams Plc, JSP Corporation, Sinoyqx |

Frequently Asked Questions

Asia Pacific led the High Heat Foam Market in the region with the highest revenue share in 2024.

Rising infrastructure and railway projects drive the market growth.

Automotive will grow rapidly in the High Heat Foam Market from 2025 to 2032.

The expected CAGR of the global High Heat Foam Market during the forecast period is 7.81%

The High Heat Foam Market was valued at USD 12.99 billion in 2024.

Get in Touch