Automotive finance Market Report Scope & Overview:

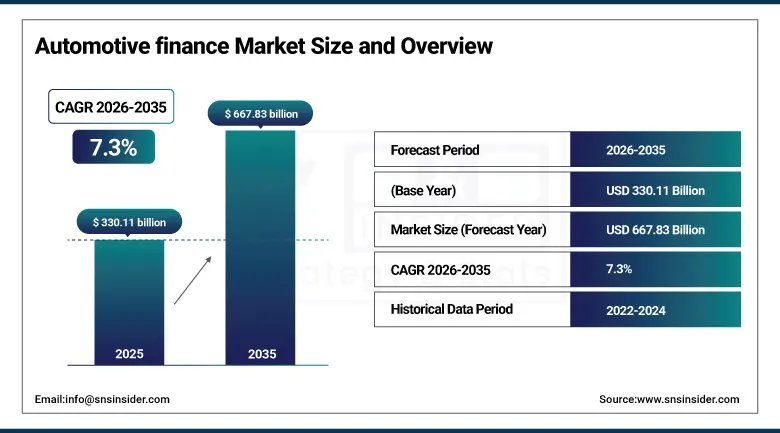

The Automotive Finance Market was valued at USD 330.11 billion in 2025 and is expected to reach USD 667.83 billion by 2035, growing at a CAGR of 7.3% from 2026-2035.

In the automotive financing industry, there is rapid growth being witnessed owing to growth in automobile ownership, high demand for luxury cars and electric cars, and the widespread adoption of digital financing solutions. The car manufacturers and banks are offering flexible terms of loans and leases to the customers, thereby enhancing their convenience and presence in the market. The application of AI in credit scoring, online loan services, and real-time valuation of automobiles is transforming the automotive finance space.

More than 80% of new vehicles added to the road in the United States were financed with a lease or a loan and OEM financial services divisions, commercial banks, and rapidly growing fintech auto lenders are intensifying competition to capture this vast financing opportunity across both new and used vehicle segments through 2035.

Market Size and Forecast

-

Market Size in 2025: USD 330.11 Billion

-

Market Size by 2035: USD 667.83 Billion

-

CAGR: 7.3% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Automotive Finance Market - Request Free Sample Report

Automotive Finance Market Trends

-

Rapid adoption of AI-powered credit scoring, real-time vehicle valuation, and automated underwriting platforms enabling lenders to approve automotive loans faster, with greater accuracy, and to a broader credit spectrum of borrowers.

-

Growing shift toward subscription-based vehicle ownership models and flexible short-term leases, particularly among younger consumers who prioritize access to mobility over traditional vehicle ownership.

-

Increasing development of specialized EV financing products including battery residual value guarantees, charging infrastructure financing bundles, and software subscription integration within EV loan and lease agreements.

-

Rising adoption of online and mobile-first automotive finance platforms enabling fully digital loan origination, e-signature, vehicle delivery, and payment management without dealership or branch visits.

-

Growing integration of fintech-driven buy-now-pay-later (BNPL) and embedded finance models into automotive retail platforms, enabling seamless point-of-purchase vehicle financing across dealer networks and online marketplaces.

-

Increasing demand for commercial vehicle financing solutions driven by fleet electrification, logistics expansion, and e-commerce growth creating sustained demand for EV fleet leases and commercial vehicle loan products.

-

Growing adoption of used vehicle financing platforms enabled by AI-driven vehicle condition assessment, digital title transfer, and blockchain-based vehicle history verification improving lender confidence in used asset quality.

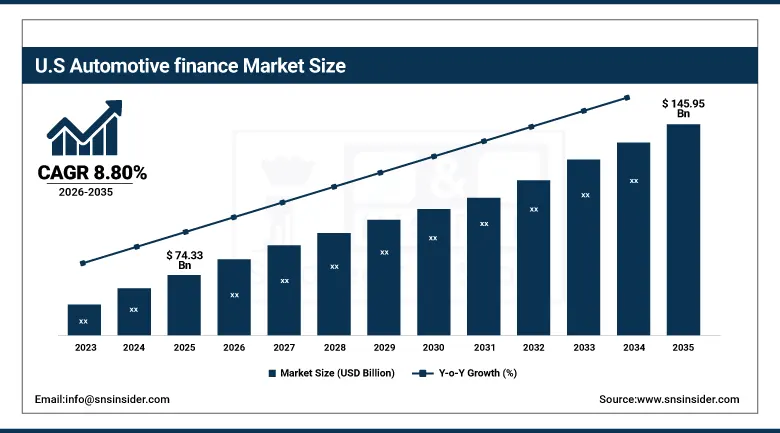

U.S. Automotive Finance Market was valued at USD 74.33 billion in 2025 and is expected to reach USD 145.95 billion by 2035, growing at a CAGR of 8.80% from 2026-2035.

The US market for financing the automobile industry has an advantage over other financial industries because of its enormous size in terms of the volume of cars being purchased in both markets (used and new). The regulation of financing consumer automobiles is very efficient in the market, and technology is extensively used in the automobile finance industry. Among the leading players in the market are Ally Financial, Bank of America, Capital One, and Chase Auto Finance, while the fintech start-ups disrupting the traditional model of lending include AutoFi, Carvana, and Upstart.

In April 2025, AutoFinIQ launched a finance engine incorporating AI to assess vehicle value depreciation, credit risk, and payment behavior in real-time enabling customized loan offerings with dynamic risk scoring, allowing financial institutions to serve significantly more customers while maintaining portfolio health and profitability.

Automotive Finance Market Segment Insights

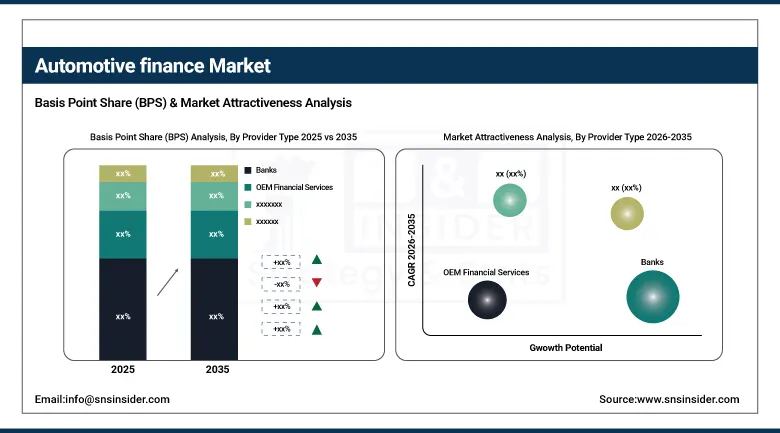

Based on Provider Type, Banks accounted for the largest market share in 2025; NBFCs & Fintech Lenders expected to be the fastest-growing segment (CAGR of 8.18%).

Based on Finance Type, Loans accounted for the largest market share (>75%) in 2025; Leasing expected to be the fastest-growing segment driven by EV adoption and subscription models.

Based on Vehicle Type, Passenger Vehicles accounted for the largest market share in 2025; Commercial Vehicles expected to grow fastest driven by fleet electrification and logistics expansion.

Automotive Finance Market Segment Analysis

By Provider Type, Banks dominate, NBFCs & Fintech Lenders expected to grow fastest

Commercial banks continued to hold supremacy in the automotive financing market in 2025 owing to customer trust built through years, extensive distribution channels, favorable interest rates, and diversification of financial portfolios. Bank of America, Chase, Wells Fargo, and other foreign banks remained the leaders in processing maximum automotive loans worldwide using both direct and indirect methods for issuing automotive loans.

Lenders belonging to the fintech category and NBFCs will witness a higher CAGR of 8.18% between 2026 and 2035. This can be attributed to the growing adoption of NBFCs and fintech lenders in the automotive finance market owing to flexible financing options catering to subprime consumers. Automotive fintech firms such as AutoFin, Carvana, and Upstart have developed artificial intelligence-powered platforms offering customized auto loans by assessing credit scores and consumer purchasing behavior. Firms including Capital Float and Upstart have expanded their operations in tier II and tier III cities, providing fast loan approvals with minimal paperwork.

By Finance Type, Loans dominate, Leasing growing rapidly

Market share was held strongly by the loan segment, where more than 75% market share was achieved in 2025. Auto loans account for the most mature and widely used form of financing automobiles in the world. It helps customers acquire ownership of an automobile through periodic payments for a mutually agreed period. The increasing trend of zero-interest promotional financing provided by captive finance wings of OEMs has ensured a steady flow of loans.

The leasing segment has been estimated to experience the fastest growth CAGR for 2026-2035 owing to consumer preference for flexibility in accessing a vehicle over ownership, increase in EV purchases requiring leases that help upgrade technologies and OEM subscriptions including insurance and other aspects in one single monthly payment.

By Vehicle Type, Passenger Vehicles dominate, Commercial Vehicles growing fast

In 2025, passenger cars accounted for the biggest share in the automotive finance industry, attributed to the large number of personal car sales globally, the increasing purchasing power of middle classes in developing countries, urbanization, and the desire among consumers for personal transportation. The trend towards higher-value luxury and electric passenger cars is elevating transaction volumes and financing amounts per unit, enabling healthy revenue growth despite slowing unit growth.

Commercial vehicles offer a high-growth opportunity, thanks to the logistics growth facilitated by online shopping, electrification initiatives for commercial vehicle fleets in businesses and transport authorities, and the rise of connected vehicle technology in commercial vehicles that help lenders understand asset utilization and manage risks.

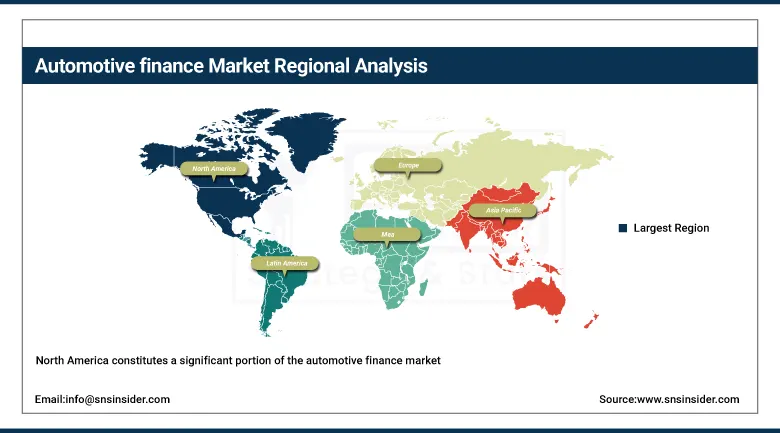

Automotive Finance Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

72% |

|

Europe |

Germany |

32% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

UAE |

28% |

|

Latin America |

Brazil |

44% |

North America Automotive Finance Market Insights

North America constitutes a significant portion of the automotive finance market, with the United States being the driving force behind it. As per statistics, the U.S. ranks among the biggest automotive finance markets in the world. High automobile penetration rates, increased consumer dependency on automobile financing schemes such as auto loan financing and leasing arrangements, and rising demand for luxury and electric automobiles have been responsible for the growth of the market. Over 80% of the purchase of new automobiles in the United States is done through auto loan financing provided by commercial banks, credit unions, OEM captive finance firms, and fintech companies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Automotive Finance Market Insights

The Asia Pacific region is anticipated to record the highest growth rate in the automotive finance market on account of increased vehicle ownership, an increase in the middle class population, and higher levels of financial inclusion in nations like China, India, Japan, South Korea, and ASEAN member states. China is currently dominating the market on account of its massive automotive sector and a growing network of digital auto lenders and OEM-affiliated finance providers. India is another country poised for significant growth on account of growing demands from passenger vehicles and greater ease of getting loans via FinTech firms.

Europe Automotive Finance Market Insights

In 2025, the market in Europe was one of the largest globally, owing to the high cost of automobiles, a robust leasing environment, and effective OEM captive finance companies. Countries like Germany, France, the UK, Italy, and Spain remain the key drivers of financing in both passenger and commercial automobiles. The rising popularity of electric vehicles has been contributing immensely to the growing demand for leasing and subscribing to ownership, as well as green financing programs. Banks and carmakers have been increasingly providing flexible payment plans and digital finance platforms to customers. Moreover, favorable policies by the government on electric vehicles have further bolstered the automotive finance market in Europe.

Middle East & Africa and Latin America Automotive Finance Market Insights

Markets in the Middle East and Africa and Latin America regions have shown consistent growth owing to the increased requirement for cars, enhanced banking presence, and greater availability of automotive loans to consumers. In the Middle East, countries like Saudi Arabia and UAE are registering an increase in the acceptance of Islamic car financing options, which comply with Sharia laws, along with the growing popularity of luxury and electric cars. The Latin American region, spearheaded by countries like Brazil and Mexico, is reaping benefits of growing middle-income groups and digital lending options.

Market Growth Drivers:

Rising Global Vehicle Ownership and Expanding Consumer Credit Availability Driving Automotive Finance Market Growth: The automotive finance industry continues to grow consistently because of factors such as high penetration levels, increased interest from consumers on automotive finance solutions, as well as global growth within credit agencies. The finance solutions, including loans, leases, and subscriptions, continue to be relied upon by consumers to ensure that their initial costs remain low during the purchase of vehicles. Moreover, the growth in the use of electric vehicles, digital financing methods, and automotive finance programs ensures continued growth in the industry. The rivalry between banks, OEM finance companies, financial technology providers, and credit unions in the banking sector also fuels growth.

Market Restraints

High Interest Rates and Increased Defaulting on Loans Constricting Automotive Financing Market Growth Around the Globe: While there are numerous opportunities for expansion within the automotive financing industry, there are certain concerns it needs to address. Some of the obstacles could include higher interest rates, rising prices, and loan payment defaults. During times of economic volatility, as well as any shift in consumer purchasing power, car prices could become too expensive for individuals to purchase, thus influencing their demand for financing services, especially within developing nations. Problems such as credit risk, regulations, and depreciation in used car financing are some examples of other issues facing the industry.

Market Opportunities

Digital Lending Innovations and Electric Vehicle Financing Creating New Automotive Finance Market Opportunities Globally: The fast shift towards digitalization, along with the adoption of more electric cars, is generating many business opportunities for the auto financing sector. There is an increasingly evident trend of using fintech organizations and conventional loan disbursing institutions that utilize artificial intelligence and big data analysis to automate the loan processing procedures in order to streamline the whole process of issuing loans. With more specialized loan programs being demanded by consumers, such as battery lease options and subscription services, along with other green measures, lenders can earn extra income from auto manufacturers.

Recent Developments:

-

2025 (October): Volkswagen Financial Services introduced a subscription-based financing model for its electric vehicles, bundling maintenance, insurance, and charging to capture younger consumers valuing flexibility and sustainability.

-

2025 (September): Toyota Financial Services launched a digital platform for seamless online financing applications, improving accessibility and reducing friction in the vehicle financing process for retail customers.

-

2025 (August): Ford Credit announced a partnership with a major technology firm to develop an AI-driven platform to streamline electric vehicle financing, improving customer experience and positioning Ford Credit as a leader in EV finance.

Automotive Finance Market Key Players

-

Ally Financial Inc.

-

Bank of America Corporation

-

Capital One Financial Corporation

-

Chase Auto Finance (JPMorgan Chase)

-

Toyota Financial Services

-

GM Financial Inc.

-

Ford Motor Credit Company

-

Volkswagen Financial Services

-

Mercedes-Benz Financial Services

-

BMW Financial Services

-

Daimler Financial Services

-

Hitachi Capital

-

Wells Fargo Auto

-

Santander Consumer USA

-

TD Auto Finance

-

Westlake Financial

-

Carvana

-

AutoFi

-

Upstart Holdings

-

Capital Float

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 330.11 Billion |

| Market Size by 2035 | USD 667.83 Billion |

| CAGR | CAGR of 7.3% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Provider Type (Banks, OEM Financial Services, Credit Unions, NBFCs & Fintech Lenders) • By Finance Type (Loan, Leasing) • By Vehicle Type (Passenger Vehicles, Commercial Vehicles) • By Vehicle Condition (New, Used) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ally Financial Inc.; Bank of America Corporation; Capital One Financial Corporation; Chase Auto Finance (JPMorgan Chase); Toyota Financial Services; GM Financial Inc.; Ford Motor Credit Company; Volkswagen Financial Services; Mercedes-Benz Financial Services; BMW Financial Services; Daimler Financial Services; Hitachi Capital; Wells Fargo Auto; Santander Consumer USA; TD Auto Finance; Westlake Financial; Carvana; AutoFi; Upstart Holdings; Capital Float |

Frequently Asked Questions

Ans: Europe held a leading regional share of approximately 32% in 2025, supported by high vehicle transaction values, well-established OEM captive finance operations, and growing EV leasing and subscription product adoption across Germany, France, the United Kingdom, and other major European automotive markets.

Ans: The Loans segment dominated the Automotive Finance Market in 2025 with greater than 75% market share, reflecting automotive loans as the most established vehicle financing mechanism globally, widely adopted across new and used vehicle segments.

Ans: The Banks segment dominated the Automotive Finance Market in 2025, leveraging their established customer trust, broad distribution networks, competitive interest rate structures, and large direct and indirect automotive loan portfolios.

Ans: Rising global vehicle ownership rates, increasing vehicle transaction values driven by electrification and premiumization, growing demand for EV-specific financing products, and the rapid adoption of AI-powered digital auto lending platforms are the primary drivers of sustained market growth through 2035.

Ans: The Automotive Finance Market was valued at USD 330.11 billion in 2025.

Ans: The Automotive Finance Market is expected to grow at a CAGR of 7.3% from 2026 to 2035.

Get in Touch