Autonomous Data Platform Market Report Scope & Overview:

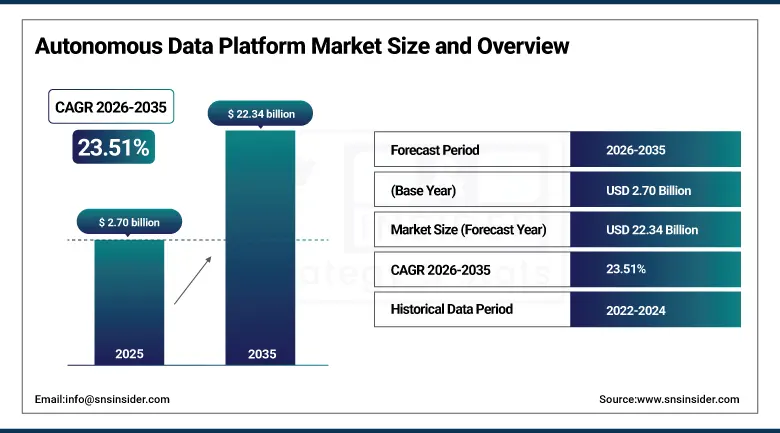

The Autonomous Data Platform Market size was USD 2.70 Billion in 2025 and is expected to reach USD 22.34 Billion by 2035, growing at a CAGR of 23.51% from 2026–2035.

Autonomous Data Platforms carry out data processing, analysis, and management tasks with minimal involvement of people. The need for such solutions will only grow due to the desire of enterprises for faster and scalable data infrastructures. Integration between multiple data platforms helps in easy manipulation of data from all sources. Increasing investments and funds will continue to spur innovation within this fast-growing sector. AI-based insights will be used to boost decision-making skills among organizations. Innovations and patents will continue to drive growth with technological developments. Cost reductions can be achieved using automation in data platforms. Companies realize that they need to have such data platforms as part of their infrastructure for their digital transformations projects.

AWS unveiled major advancements during AWS Pi Day, including Amazon Bedrock updates for generative AI workloads. SageMaker Unified Studio and Amazon S3 Tables were also introduced to enhance data integration. These updates support multi-agent collaboration for analytics and AI workloads specifically. This kind of platform expansion reflects how quickly cloud providers are adding autonomous capabilities. Competing platforms are likely to respond with similar integrated analytics and AI feature releases.

Market Size and Forecast:

-

Market Size in 2026E: USD 3.34 Billion

-

Market Size by 2035: USD 22.34 Billion

-

CAGR: 23.51% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Autonomous Data Platform Market - Request Free Sample Report

Autonomous Data Platform Market Trends:

-

Real-time analytics adoption is accelerating as enterprises seek faster, data-driven decision-making capabilities.

-

AI and machine learning integration is improving predictive analytics and automated decision-making across platforms.

-

Cloud-based deployment is gaining ground due to lower upfront costs and greater scalability.

-

Growing SME adoption is being driven by more affordable, accessible autonomous platform offerings.

-

Industry-specific platform solutions tailored to healthcare, retail, and manufacturing are gaining traction.

-

Generative AI copilots are increasingly being embedded directly into core data platform interfaces.

-

Consolidation through acquisitions is reshaping the competitive landscape among major data platform vendors.

-

Open table format standards like Apache Iceberg are gaining adoption across competing platform vendors.

U.S. Autonomous Data Platform Market Outlook:

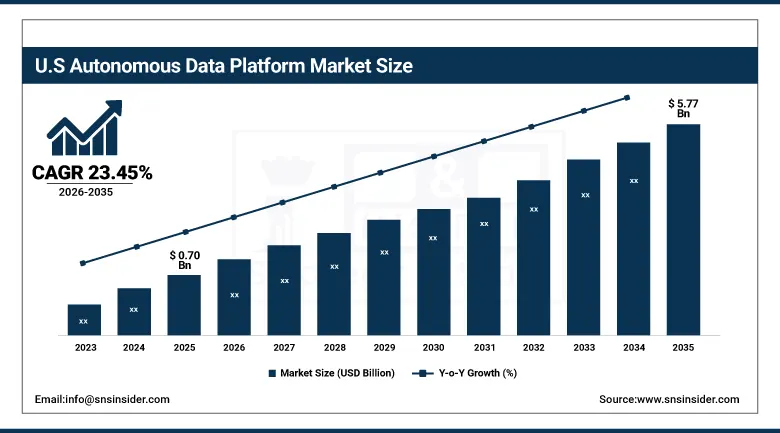

The U.S. Autonomous Data Platform Market was valued at approximately USD 0.70 Billion in 2025. It is expected to reach approximately USD 5.77 Billion by 2035. The market is growing at a CAGR of approximately 23.45%.

Growing demand for data insights, AI-powered analytics, and automation continues to propel the growth of the U.S. market. Business organizations seek improved decision-making skills and affordable data management systems. Autonomous platforms provide more efficient means of doing so compared to existing data infrastructures. Substantial investment into AI and cross-platform innovation continues to facilitate this trend among U.S. businesses. The rising need for real-time analysis makes these platforms a requirement for digital transformation. State and federal government agencies have also started piloting autonomous data platforms.

In June 2024, Databricks purchased Tabular, the company behind the development of Apache Iceberg. It is estimated that this USD 1 billion acquisition allowed for solving the problem of competing data format standards in the industry. As a result, Databricks introduced its Delta Lake UniForm solution, enabling access to data via Delta and Iceberg formats at the same time. Such acquisitions demonstrate an increasing level of competitive pressure to own standard data infrastructure technologies. Platform companies are increasingly buying specialized technologies rather than developing all of them independently.

Autonomous Data Platform Market Segment Analysis:

-

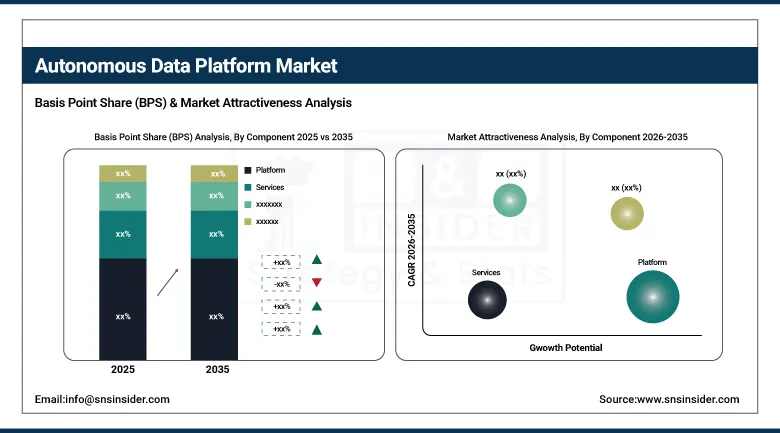

By Component, the platform segment dominated the autonomous data platform market with approximately 70% share in 2025. The services segment is growing fastest, at a CAGR of 24.93%.

-

By Deployment, the on-premise segment dominated the autonomous data platform market with approximately 54% share in 2025. The cloud segment is growing fastest, at a CAGR of 24.45%.

-

By Enterprise Size, the large enterprises segment dominated the autonomous data platform market with approximately 62% share in 2025. The SMES segment is growing fastest, at a CAGR of 24.86%.

-

By End Use, the BFSI segment dominated the autonomous data platform market with approximately 22% share in 2025. The retail segment is growing fastest, at a CAGR of 26.28%.

By Component, platforms dominate, services grow fastest

In the component category, the platform segment had the highest market share in 2025, accounting for around 70%. The need for scalable and robust data processing platforms is growing in virtually every sector. Features like real-time analytics, artificial intelligence, and automation offered by such platforms enable organizations to be highly efficient and make quick decisions. Such benefits make these platforms more popular and hence the segment to be highly dominant. There is an increasing trend of incorporating AI functionalities directly into platform offerings. As companies collect large amounts of data, the need for platforms is expected to grow consistently.

The services segment is experiencing the highest rate of growth of all other component segments, at 24.93% CAGR. Increasing demands for consultative and implementation services are making this market segment grow rapidly. Organizations adopting these platforms find themselves in need of professional assistance to deploy and integrate these platforms. The need for maintenance and support services ensures that they operate efficiently and without any issues in the long run.

By Deployment, on-premise dominates, cloud grows fastest

The on-premise deployment accounted for the biggest market share in 2025, capturing about 54% of the overall revenue share. Large corporations working in heavily regulated industries prefer to be completely in charge of their infrastructure and data. In comparison to cloud-based solutions, on-premise deployment ensures higher levels of protection, customization, and compliance with regulations. It further offers higher data privacy and better performance for organizations that deal with extremely sensitive data. These characteristics ensure that the deployment type retains some relevance.

Cloud deployment shows the highest rate of growth when compared to other types of deployment, demonstrating a CAGR of 24.45%. Increased popularity of such platforms results from their versatility, flexibility, and low costs. Businesses no longer have to spend money on costly and large-scale infrastructures as they will not have to manage data locally. Trends related to remote working, digital transformation, and analytics drive increased demand for cloud platforms.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Autonomous Data Platform Market Insights

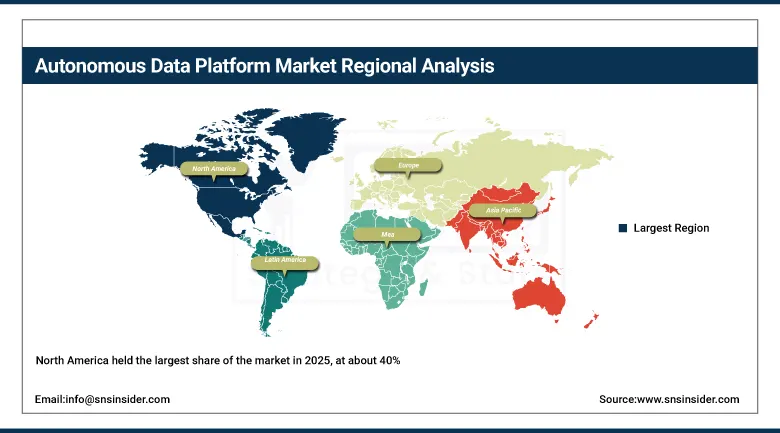

North America held the largest share of the market in 2025, at about 40%. Early adoption of cutting-edge technology and a powerful presence of leading vendors both support this lead. Growing automation demand across BFSI, healthcare, and retail keeps reinforcing this regional position. A well-established IT infrastructure and favorable regulatory environment add further reinforcement.

The United States accounts for approximately 82.5% of North American revenue. High R&D investment keeps driving continued innovation across major American technology vendors. This combination of infrastructure and innovation keeps North America firmly in the lead.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Autonomous Data Platform Market Insights

Europe represents a steady, established market for autonomous data platforms across regulated industries. Germany leads the regional market, supported by strong industrial digitization and enterprise IT investment. France and the UK contribute meaningful demand through their own expanding financial services sectors. Manufacturing digitization across the broader region is also adding fresh demand for these platforms.

Germany accounts for approximately 24.6% of European revenue. Strict data protection regulations across the EU continue shaping platform design and deployment choices. This regulatory environment should keep supporting steady European market growth.

Asia Pacific Autonomous Data Platform Market Insights

Asia Pacific is growing fastest in this market, at a CAGR of approximately 25.20%. Expanding digital transformation projects and rising cloud technology adoption both drive this growth. Mounting demand for data-driven decision-making across manufacturing, retail, and healthcare reinforces this trend. The emergence of new SMEs and government technology infrastructure initiatives further support rapid adoption.

China accounts for approximately 40.6% of Asia Pacific revenue. Growing enterprise digitization across the region keeps fueling continued platform adoption. As digital transformation initiatives keep expanding, this regional growth should keep accelerating.

MEA & Latin America Autonomous Data Platform Market Insights

The UAE leads MEA revenue, growing government technology investment and rising enterprise digitization both support this position. Saudi Arabia is also expanding its digital infrastructure across major industry sectors. Smart city initiatives across the Gulf region are also generating fresh platform demand.

Brazil leads Latin American revenue, expanding enterprise digitization and rising cloud adoption both drive this regional lead. Mexico and Argentina contribute secondary demand through their own expanding technology sectors.

Market Dynamics:

Growth Drivers: Demand for real-time analytics driving faster, data-driven decision-making

Rising necessity for fast and data-based decisions from the enterprises drives the adoption of real-time analytics. Autonomous data platforms provide real-time analysis capabilities without any human intervention. Enterprises require fast processing of huge amounts of data to respond to market and operational dynamics. Such platforms enhance data processing capabilities through automatic detection of trends and patterns. Automatic detection of patterns makes it possible to make quicker decisions in different organizational processes.

Transformation projects that incorporate digitization are rapidly gaining momentum across almost all sizes of organizations across industries. It has become necessary for enterprises to have real-time analysis capabilities due to rapid competition in different industries. Automation enables organizations to benefit from their data resources in an efficient way without engaging in time-consuming manual analysis activities. Adoption of generative artificial intelligence will further accelerate this trend.

Restraints: High implementation costs limiting adoption among smaller organizations

The deployment of autonomous data platforms always entails considerable costs associated with setup and integration. Small companies tend to feel overwhelmed by the price of such complex software since it exceeds the capabilities of their budgets. The integration with current IT infrastructure and systems is often complicated and time-consuming.

Vendor lock-in issues also serve as another reason for avoiding commitment to just one particular platform vendor. This procedure demands unique resources, which adds even more costs. Such technology might be hard to invest in due to cost sustainability issues.

Opportunities: AI and machine learning integration enhancing data insights and decision-making

The use of AI and machine learning can give corporations more insights into their current data. This is because such technologies allow platforms to analyze big amounts of data better, while at the same time detecting any patterns. Prediction analysis allows making better business decisions faster and with higher precision. Machine learning also helps prediction become even more accurate through learning from any additional information received in the process.

The ability to make such sophisticated predictions is valuable for business success since it is possible to make the right decision before competitors. The number of enterprises that choose to employ AI-powered autonomous platforms in order to get better data insights continues to grow. There is a chance that it will only get easier with the further evolution of AI.

Recent Developments:

-

2025: AWS announced new advancements during AWS Pi Day, including Amazon Bedrock for generative AI, SageMaker Unified Studio, and Amazon S3 Tables.

-

2024: Oracle announced its upcoming Intelligent Data Lake as part of the Oracle Data Intelligence Platform, offering a unified developer experience integrating orchestration, analytics, and AI.

-

2024: Databricks acquired Tabular, the company founded by the creators of Apache Iceberg, for approximately USD 1 billion to resolve competing data format standards.

Autonomous Data Platform Market Key Players are:

-

Oracle Corporation

-

Teradata

-

IBM Corporation

-

Amazon Web Services, Inc.

-

Hewlett Packard Enterprise Development LP

-

Qubole, Inc.

-

Cloudera, Inc.

-

Gemini Data

-

Denodo Technologies

-

Alteryx, Inc.

-

Snowflake Inc.

-

Microsoft Corporation

-

Google LLC

-

SAP SE

-

Databricks

-

Vertica

-

Informatica

-

Hitachi Vantara

-

Domo, Inc.

-

Qlik

Autonomous Data Platform Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.70 Billion |

| Market Size by 2035 | USD 22.34 Billion |

| CAGR | CAGR of 23.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platform, Services) • By Deployment (On-premise, Cloud) • By Enterprise Size (Large Enterprises, SMEs) • By End Use (BFSI, Healthcare, Retail, Manufacturing, IT and Telecom, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Oracle Corporation, Teradata, IBM Corporation, Amazon Web Services, Inc., Hewlett Packard Enterprise Development LP, Qubole, Inc., Cloudera, Inc., Gemini Data, Denodo Technologies, Alteryx, Inc., Snowflake Inc., Microsoft Corporation, Google LLC, SAP SE, Databricks, Vertica, Informatica, Hitachi Vantara, Domo, Inc., and Qlik |

Frequently Asked Questions

The Autonomous Data Platform Market is expected to grow at a CAGR of 23.51% from 2026 to 2035.

The Autonomous Data Platform Market was valued at USD 2.70 Billion in 2025, with the United States accounting for roughly a quarter of that global total.

Rising demand for real-time analytics, growing AI and machine learning integration, and expanding cloud adoption are the primary growth factors.

The Platform segment dominated the Autonomous Data Platform Market with approximately 70% share in 2025.

North America dominated the Autonomous Data Platform Market with approximately 40% revenue share in 2025.

Get in Touch