Bakelite Market Size & Trends

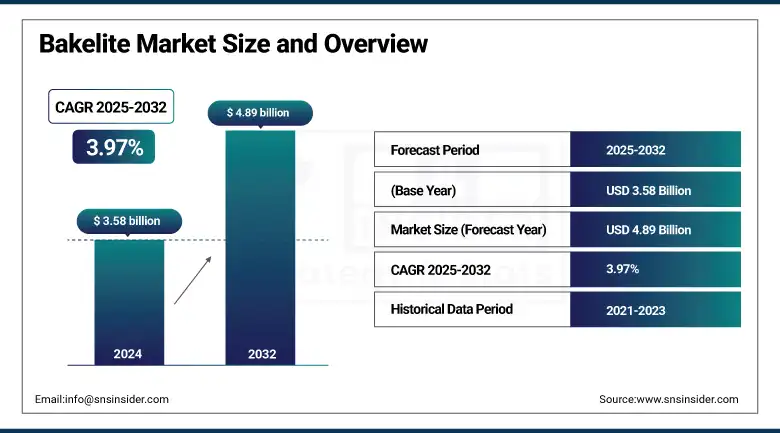

The Bakelite Market Size was valued at USD 3.58 billion in 2024 and is expected to reach USD 4.89 billion by 2032 and grow at a CAGR of 3.97% over the forecast period 2025-2032.

Bakelite market analysis indicates the soaring requirement from the electrical and electronics industry as one of the prime factors driving market growth. Bakelite, a thermosetting plastic with good electrical insulating and heat resistance, as well as good mechanical strength, is commonly used as a material for circuit breakers, switches, sockets, insulators, and housing of electrical equipment. With the worldwide advancement of electrification, development of smart grid, and popularization of consumer electronics, manufacturers are looking for durable and reliable materials such as Bakelite to satisfy performance and safety requirements. Moreover, as electronic components become smaller and as circuits become more complex, the importance of heat resistance and dimensional stability of materials is felt, and attention is focused on the need for Bakelite in this area, also, which also drives the bakelite market growth.

To Get more information On Bakelite Market - Request Free Sample Report

The U.S. government investments in electrification infrastructure. Under IIJA, USDOT is allocating USD 5billion to National Electric Vehicle Infrastructure (NEVI) Formula Program (2022–2026) and an additional USD 2.5billion in discretionary funding for charging infrastructure enabled by $\NEVI Formula Program (statutory required, as per IIJA) to advance nationwide EV networks.

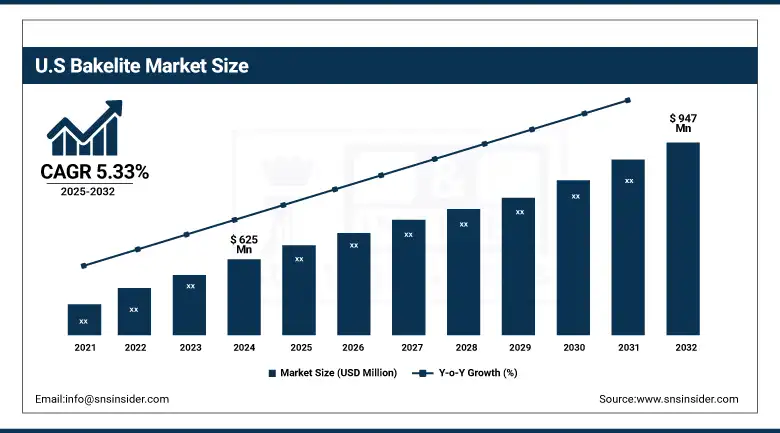

The U.S Bakelite market size was USD 625 million in 2024 and is expected to reach USD 947 million by 2032 and grow at a CAGR of 5.33% over the forecast period of 2025-2032. It is owing to its advanced automotive manufacturing and stringent healthcare standards. Synthetic polyisoprene is widely used in producing medical gloves, electrical insulation material tubing, and device seals as an alternative to natural rubber. In the automotive sector, the material is essential in producing tire components, hoses, and suspension systems for both ICE and electric vehicles. In 2023, Toyota and Mazda expanded their joint manufacturing facility in Alabama, increasing the demand for auto-grade elastomers like polyisoprene used in interior and performance parts.

Bakelite Market Dynamics

Key Drivers:

-

Increasing Automotive Applications Drive the Market Growth

Bakelite’s excellent thermal resistance, mechanical durability, and dimensional stability make it a highly suitable material for a wide range of automotive components such as brake pads, clutch plates, distributor caps, and ignition systems. As the global automotive industry shifts toward electric vehicles (EVs) and high-performance internal combustion engine (ICE) components, there is a growing demand for materials that can endure elevated temperatures and harsh mechanical environments. Bakelite’s lightweight and heat-resistant properties contribute to improved fuel efficiency and safety, aligning with industry trends like emissions reduction and vehicle weight optimization. Additionally, its compatibility with compression and injection molding ensures high-volume, cost-effective production—critical for the automotive supply chain.

In 2023, Sumitomo Bakelite Co., Ltd. announced the expansion of its phenolic molding compound production facility in the U.S. to cater to increasing demand from automotive OEMs for heat-resistant components in EVs and hybrid vehicles.

Restrain:

-

Environmental and Disposal Concerns, which may hamper the Market Growth

Despite its functional advantages, Bakelite faces environmental scrutiny due to its thermosetting nature, which prevents it from being remolded or recycled like thermoplastics. This characteristic leads to challenges in disposal and limits its use in applications where recyclability is a priority. In an era of rising environmental awareness and stringent regulations around plastic waste, Bakelite’s non-recyclability is a growing concern. Regulatory bodies in Europe and North America are pushing for greater circularity and sustainability in material usage, which could result in reduced adoption of Bakelite in consumer goods and automotive interiors where sustainable alternatives are available.

Opportunities:

-

Strategic Use in Green Energy & EV Infrastructure Create an Opportunity for the Market

The global push toward decarbonization, electrification, and sustainable energy systems is creating new growth avenues for high-performance insulating materials. Bakelite’s ability to withstand high temperatures and electrical loads makes it an ideal candidate for use in electric vehicle connectors, battery casings, and renewable energy systems such as solar inverters and wind turbine components. With the rapid buildout of EV charging infrastructure and renewable power generation facilities, demand for materials with proven thermal and electrical reliability is increasing. The market can capitalize on this shift by offering tailored Bakelite grades for green energy applications, which drive the bakelite market trends.

The U.S. Department of Transportation, under the National Electric Vehicle Infrastructure (NEVI) Program, allocated USD 5 billion through 2026 to build out the national EV charging network, driving demand for robust insulation materials like Bakelite in EV chargers and related components.

Bakelite Market Segmentation Analysis

By Type

Alcohol-based Bakelite holds the largest market share, around 42% in 2024. It is owing to its long-standing use in electrical insulation, molded parts, and coatings. It offers strong thermal stability, high mechanical strength, and efficient curing properties, making it cost-effective and widely compatible with legacy manufacturing systems. It remains the preferred choice in large-scale industrial applications, especially in circuit breakers, heat shields, and automotive clutch components.

Ether-based Bakelite is the fastest-growing segment, primarily due to increasing regulatory pressure to reduce VOCs (volatile organic compounds) and formaldehyde emissions. These resins offer greater flexibility and safer handling during manufacturing. Their growth is supported by demand in safer consumer electronics, low-emission coatings, and eco-conscious construction applications.

By Form

Molding powder continues to dominate the market, particularly in high-volume production processes such as compression and transfer molding. It is widely used for making small-to-medium-sized parts with high mechanical and thermal performance requirements. Applications in electrical housings, appliance handles, and industrial panels support its ongoing dominance. Its easy flow, fast curing time, and dimensional accuracy make it a staple in OEM manufacturing.

Laminates are witnessing the fastest growth due to their expanding role in the electrical, construction, and aerospace sectors. High-pressure Bakelite laminates provide outstanding fire resistance, chemical resistance, and mechanical durability, making them suitable for demanding insulation boards, wall linings, and high-performance industrial panels.

By Manufacturing Process

Compression molding is the most widely adopted process in the Bakelite industry, favored for its ability to produce large volumes of durable parts at a low cost. This process is particularly effective for manufacturing dense, solid parts such as brake pads, switchgear, and tool handles. Its simplicity and long-standing infrastructure in many production facilities reinforce its dominance in the market.

Injection molding is rapidly emerging as the fastest-growing process, particularly as demand grows for precision parts with complex geometries. In electronics and automotive sectors, manufacturers increasingly prefer injection molding for its capability to produce lightweight, miniaturized components with excellent repeatability and fine detailing.

By Application

The electrical & electronics industry remains the dominant Bakelite applications segment due to Bakelite’s insulating properties, flame resistance, and mechanical durability. It is widely used in switchboards, sockets, insulators, and circuit protectors. The reliability of Bakelite under high-voltage and high-temperature conditions makes it a staple material in both industrial and household electrical systems.

Automotive is the fastest-growing segment, especially driven by the rise of electric vehicles (EVs) and hybrid systems that demand materials with high heat resistance and electrical insulation. Bakelite is used in EV battery modules, motor insulation, and under-the-hood components. OEMs are increasingly investing in thermoset-based materials to improve durability, reduce weight, and enhance thermal management, all of which favor Bakelite adoption.

Bakelite Market Regional Outlook

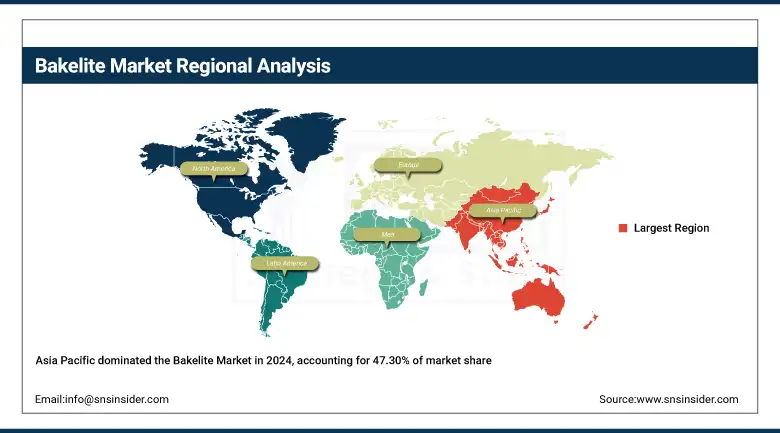

Asia Pacific held the bakelite market share largest market share, around 47.30%, in 2024. It is owing to rising industrialization and the presence of low-cost manufacturing hubs. Countries like China, India, and Japan lead tire production and export, heavily consuming polyisoprene in inner liners, treads, and anti-vibration components. The region also benefits from growing investments in EVs and medical supplies, which utilize synthetic polyisoprene due to its durability and flexibility.

Get Customized Report as per Your Business Requirement - Enquiry Now

A recent development includes Kuraray expanding its isoprene production plant in Thailand in 2023 to meet regional demand, particularly from the tire and medical device industries.

The North America region is the fastest-growing market. It is driven by robust demand from the automotive and medical sectors. The region's mature manufacturing infrastructure supports widespread use of polyisoprene in tires, industrial bakelite, belts, gaskets, and medical gloves. The shift toward synthetic variants, especially in healthcare, is accelerating due to rising concerns about latex allergies and the need for high-purity alternatives. Additionally, infrastructure development is fueling demand for polyisoprene-based seals and vibration-dampening materials.

In a recent development, U.S. infrastructure investment under the Bipartisan Infrastructure Law is boosting automotive and construction-related consumption of elastomeric materials, indirectly supporting polyisoprene demand across North America.

Europe holds a substantial share in the global Bakelite market; it is due to its advanced automotive and medical industries and strict environmental regulations. Countries such as Germany and France lead in automotive innovation, using polyisoprene in tire systems, suspension parts, and sealing applications. The region also favors synthetic polyisoprene in healthcare for its hypoallergenic properties, especially in surgical gloves and pharmaceutical packaging. Recently, several European manufacturers have invested in R&D to develop bio-based and eco-friendly synthetic polyisoprene variants, aligning with the EU Green Deal and increasing sustainability demands.

Bakelite Market Key Players

Major Bakelites companies are Hexion Inc., Sumitomo Bakelite Co., Ltd., DIC Corporation, BASF SE, Akrochem Corporation, Ashland Global Holdings Inc., Georgia-Pacific Chemicals, SI Group, Momentive Performance Materials, Mitsui Chemicals, Inc., Kolon Industries, Inc., Hexcel Corporation, Prefere Resins Holding GmbH, Plenco (Plastic Engineering Company), Dynea AS, Chang Chun Group, Arclin Inc., Altex Coatings Ltd., Fenolit d.d., Rotres Group.

Recent Development in the Bakelite Market

-

In April 2024, Sumitomo Bakelite Co., Ltd. announced the completion of new phenolic molding compounds plant at its subsidiary Nantong in China, doubling capacity (~25,000t/year) with AI/IoT-driven automation and energy-efficient, emissions‑compliant processes.

-

In January 2025, Kolon Industries Inc. launched new phenolic composite material for EV battery housings and interior parts, which has excellent heat resistance and reduced weight performance for EV car manufacturers.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.58 Billion |

| Market Size by 2032 | USD 4.89 Billion |

| CAGR | CAGR of 3.97% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type: Alcohol-based, Ether-based, Others (e.g., Phenol-based, Cresol-based) • By Form: Molding Powder, Laminates, Sheets, Rods, Tubes • By Manufacturing Process: Compression Molding, Injection Molding, Extrusion, Transfer Molding, Others (e.g., Casting, Blow Molding) • By Application: Electrical & Electronics, Automotive, Aerospace, Construction, Consumer Goods, Industrial Equipment, Others (e.g., Marine, Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Hexion Inc., Sumitomo Bakelite Co., Ltd., DIC Corporation, BASF SE, Akrochem Corporation, Ashland Global Holdings Inc., Georgia-Pacific Chemicals, SI Group, Momentive Performance Materials, Mitsui Chemicals, Inc., Kolon Industries, Inc., Hexcel Corporation, Prefere Resins Holding GmbH, Plenco (Plastic Engineering Company), Dynea AS, Chang Chun Group, Arclin Inc., Altex Coatings Ltd., Fenolit d.d., Rotres Group |

Frequently Asked Questions

Ans The market is regionally segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with Asia Pacific dominating in production and demand.

Ans.Bakelite production can lead to formaldehyde emissions, energy-intensive processing, and challenges in recyclability and biodegradability.

Ans. Major trends include bio-based phenolic resin development, automation in molding processes, and increased use in EV applications.

Ans Key growth drivers include rising demand in automotive and electrical industries, thermal resistance properties, and growing infrastructure development.

Ans Leading Bakelite manufacturers include Sumitomo Bakelite Co. Ltd., Hexion Inc., BASF SE, Kolon Industries, and Prefere Resins Holding GmbH.

Get in Touch