Barrier Films Market Report Scope & Overview:

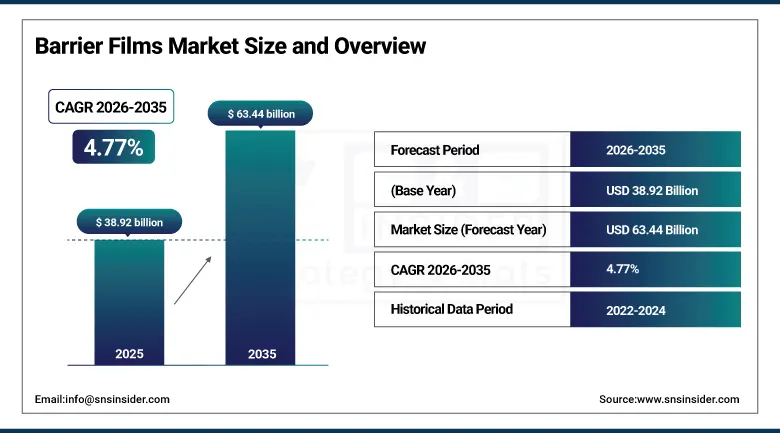

The Barrier Films Market was valued at USD 38.92 Billion in 2025 and is expected to reach USD 63.44 Billion by 2035, growing at a CAGR of 4.77% from 2026–2035.

The global barrier films market is growing at a steady and commercially broad-based pace. Barrier films are specialized polymer films engineered to prevent the permeation of gases, water vapor, aromas, and other environmental factors that would compromise packaged product quality, safety, and shelf life. This multi-layer or mono-layer films deploy barrier polymers including EVOH, PVDC, polyamide, and aluminum foil in their structure to create transmission resistance that standard polyethylene and polypropylene films cannot achieve. The market is driven by technology upgrades and the growing preference for sustainable packaging, with the food and beverage industry’s need to extend product shelf life creating consistent demand.

In March 2024, Toppan and Toppan Specialty Films (TSF) launched GL-SP, a new barrier film using a biaxially oriented polypropylene (BOPP) substrate to strengthen its GL Barrier series. The GL-SP film’s advanced inorganic barrier coating on BOPP substrate creates recyclable high-barrier packaging whose mono-material compatible structure enables plastic film recycling without the multi-material separation requirement that conventional EVOH barrier laminates create, addressing the fundamental recycling challenge that high-barrier flexible packaging faces in sustainable packaging transition programs.

Market Size and Forecast:

-

Market Size in 2026E: USD 40.78 Billion

-

Market Size by 2035: USD 63.44 Billion

-

CAGR: 4.77% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Barrier Films Market - Request Free Sample Report

Barrier Films Market Trends:

-

Development of recyclable mono-material barrier films is accelerating as sustainability goals and packaging regulations drive demand for environmentally friendly packaging solutions

-

High-barrier transparent films are increasingly replacing aluminum foil in food and pharmaceutical packaging due to their visibility, lightweight properties, and strong barrier performance

-

Growing adoption of biaxially oriented nylon (BOPA) films is supporting advanced food packaging applications that require superior oxygen barrier protection and durability

-

Demand for digitally printable barrier films is increasing as brands seek flexible packaging solutions that support customization, shorter production runs, and reduced inventory costs

-

Active barrier film technologies incorporating oxygen scavengers, moisture absorbers, and antimicrobial agents are creating premium packaging solutions that enhance product protection and extend shelf life

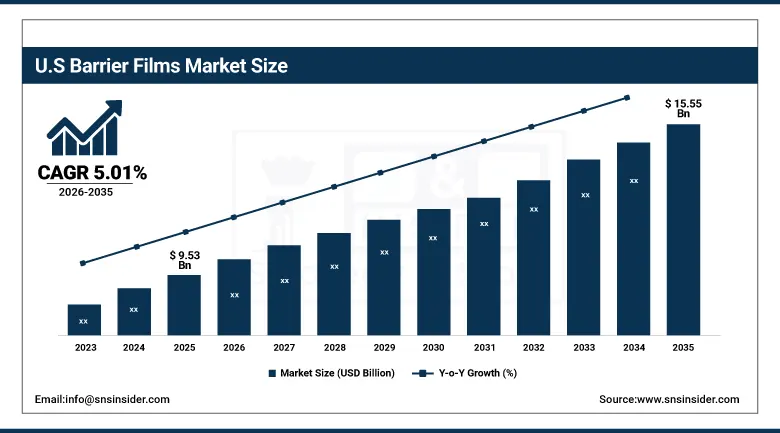

U.S. Barrier Films Market Outlook:

The U.S. Barrier Films Market was valued at approximately USD 9.53 Billion in 2025 and is expected to reach approximately USD 15.55 Billion by 2035, growing at a CAGR of approximately 5.01%.

The U.S. is the most commercially sophisticated barrier films market within North America’s fastest-growing regional position. Amcor’s U.S. operations, Berry Global, Sealed Air, Printpack, and Mondi’s North American commercial presence collectively define the domestic barrier films commercial landscape. FDA’s pharmaceutical packaging regulation, USDA FSIS’s food packaging safety standards, and the EPA’s sustainable packaging guidelines create structured compliance investment motivation whose aggregate sustains U.S. market development. The extraordinary pace of U.S. flexible packaging adoption driven by e-commerce, food delivery, and retail sustainability mandates creates growing barrier film procurement.

Amcor launched AmLite Ultra Recyclable barrier film in 2024, a high-barrier flexible packaging solution designed to achieve supermarket-grade recyclability while maintaining the oxygen and moisture barrier performance that food brand owners require for fresh food, snacking, and dairy applications. The launch represents the commercial breakthrough that the sustainable flexible packaging transition requires, demonstrating that recyclable mono-material structures can achieve barrier performance previously only available from non-recyclable multi-layer laminates containing EVOH or PVDC barrier layers.

Barrier Films Market Segment Analysis:

-

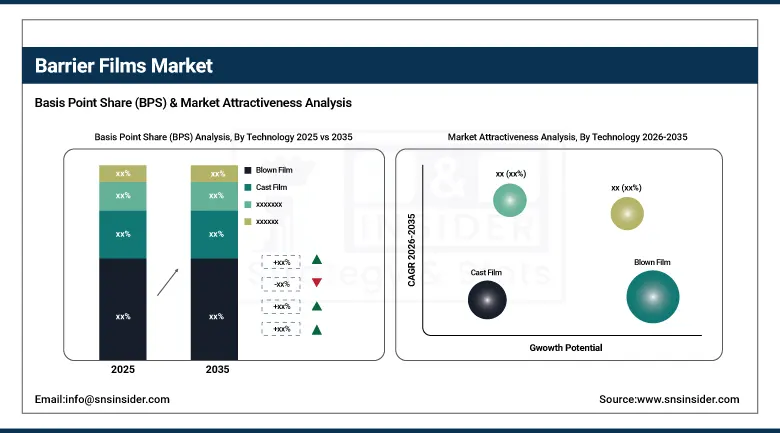

By Technology, the Blown Film segment dominated the Barrier Films Market with 55% share in 2025, while the Cast Film segment is the fastest growing.

-

By Material, the Polyethylene segment dominated the Barrier Films Market with approximately 38% share in 2025, while the EVOH segment is the fastest growing.

-

By Application, the Food & Beverage segment dominated the Barrier Films Market with approximately 42% share in, while the Pharmaceutical & Healthcare segment is the fastest growing.

By Technology, blown film dominates, cast film grows fastest

Blown film retained the dominant technology position with 55% of the barrier films market in 2025. The blown film extrusion process’s commercial primacy reflects its ability to produce multi-layer co-extruded barrier films incorporating EVOH, polyamide, and tie-layer resins in a single extrusion pass whose manufacturing efficiency creates competitive barrier film economics at commercial production scales. The blown film process’s orientation in both machine and transverse directions during bubble expansion creates balanced film mechanical properties whose biaxial orientation creates superior dart drop impact and puncture resistance that cast film alternatives cannot achieve at equivalent gauge. Each food packaging application whose barrier requirement and mechanical performance specification is satisfied by blown film co-extrusion creates procurement that sustains the technology’s dominant market position.

Cast film is the fastest-growing technology because pharmaceutical, electronics, and precision industrial barrier applications whose optical clarity, tight gauge uniformity, and superior surface smoothness requirements create specification preference for cast film’s superior dimensional and optical characteristics. Each pharmaceutical blister packaging specification whose pin-hole freedom and precise gauge tolerance requirements create cast barrier film procurement, and each electronics component barrier packaging whose electrostatic discharge protection and clarity requirements sustain cast film’s above-average adoption in premium application categories.

By Application, food & beverage dominates, pharma grows fastest

Food and beverage retained the dominant application position with approximately 42% of the barrier films market in 2025. Food packaging’s universal requirement for moisture, oxygen, and aroma barrier protection creates the most commercially consistent and highest-volume barrier film procurement category. Each new food product introduction creates barrier packaging specification whose aggregate across the global food industry’s extraordinary product innovation pace sustains barrier film demand. Fresh meat packaging’s modified atmosphere requirement, snack food packaging’s moisture and oxygen sensitivity, and dairy packaging’s extended shelf-life requirement collectively create diverse barrier film specification categories whose combined volume defines the application category’s commercial dominance.

Pharmaceutical and healthcare is the fastest-growing application because the pharmaceutical industry’s extraordinary production growth, the medical device sector’s sterile barrier packaging requirement, and the healthcare sector’s infection control packaging investment create structured above-average barrier film procurement. Each new drug formulation that requires blister packaging or pouch barrier protection creates pharmaceutical-grade barrier film procurement whose regulatory quality requirements sustain premium pricing above commodity food packaging film alternatives.

By Material, polyethylene dominates, EVOH grows fastest

Polyethylene retained the dominant material position with approximately 38% of the barrier films market in 2025. Polyethylene’s commercial primacy reflects its position as the most commercially versatile and cost-effective polymer for barrier film substrate and seal layer applications whose LDPE, LLDPE, HDPE, and mLLDPE variants collectively serve the broadest range of barrier packaging applications. PE’s moisture barrier performance, heat sealability, and chemical inertness create specification suitability for the majority of food, industrial, and agricultural barrier packaging whose performance requirements do not demand the premium gas barrier that specialty barrier resins provide. The polyethylene-based recyclable barrier film innovation that Amcor’s AmLite Ultra demonstrates creates additional PE market development that sustains polyethylene’s dominant material position as sustainable packaging transition progresses.

EVOH is the fastest-growing material because its unparalleled oxygen barrier performance, whose oxygen transmission rate substantially below alternative barrier resins at equivalent gauge creates fresh food shelf-life extension that no alternative material achieves at comparable film thickness, creates specification preference in premium fresh food, modified atmosphere, and pharmaceutical barrier packaging. Each fresh food packaging programme that migrates from conventional packaging toward modified atmosphere preservation creates EVOH co-extruded barrier film procurement whose per-unit performance justification sustains premium pricing above standard polyethylene or polypropylene alternatives.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

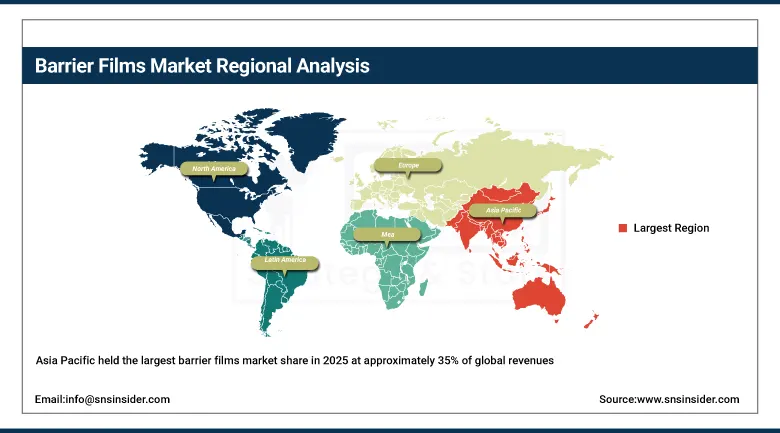

Asia Pacific Barrier Films Market Insights

Asia Pacific held the largest barrier films market share in 2025 at approximately 35% of global revenues. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary food packaging industry scale, the pharmaceutical manufacturing sector’s barrier packaging procurement, and the domestic barrier film manufacturer development. The region’s rapid urbanization, growing middle-class demand for packaged food and beverages, and expanding pharmaceutical production create the world’s largest aggregate barrier film consumption.

Japan, South Korea, and India are significant secondary markets where advanced food packaging technology, pharmaceutical manufacturing, and electronics production create consistent above-average barrier film specification procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Barrier Films Market Insights

North America is the fastest-growing regional barrier films market, driven by the extraordinary pace of sustainable packaging transition creating barrier film reformulation investment, FDA’s pharmaceutical packaging standards, and the food retail sector’s extended shelf-life requirement. The United States accounts for approximately 87.4% of North American revenues through Amcor, Berry Global, Sealed Air, and Printpack’s commercial operations.

Canada contributes approximately 12.6% of North American revenues through its food processing industry’s barrier packaging procurement, pharmaceutical manufacturing, and the retail sector’s sustainable packaging transition investment.

Europe Barrier Films Market Insights

Europe is a technically sophisticated barrier films market where EU Packaging and Packaging Waste Regulation’s recyclability mandates, REACH regulation’s material safety standards, and the food industry’s above-average fresh food packaging culture create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its food and pharmaceutical manufacturing sectors’ barrier packaging procurement, Toppan’s European sales, and the sustainable packaging innovation investment that EU regulatory pressure sustains.

France, the Netherlands, and Italy are significant secondary markets whose food manufacturing, pharmaceutical production, and agricultural film application create consistent barrier film procurement.

MEA & Latin America Barrier Films Market Insights

UAE leads MEA revenues at approximately 38.4% through its food retail sector’s premium barrier packaging, the pharmaceutical manufacturing investment, and the industrial sector’s protective film procurement. Brazil leads Latin American revenues at approximately 44.2% through its large food processing industry’s barrier packaging procurement, agricultural film application, and pharmaceutical manufacturing barrier packaging requirement.

Saudi Arabia’s food processing investment and South Africa’s retail food packaging sector create significant MEA secondary markets whose barrier film procurement reflects the progressive adoption of extended shelf-life packaging technologies.

Market Dynamics:

Growth Drivers: Food shelf-life extension demand and sustainable recyclable barrier film transition

Food shelf-life extension demand is the barrier films market’s most commercially consistent growth driver. The global trend toward reducing food waste, minimizing supply chain losses, and meeting the extended shelf-life requirements of modern retail distribution creates consistent procurement motivation for barrier packaging whose oxygen and moisture transmission resistance creates measurable commercial value in reduced spoilage and extended distribution reach. Each new ready-to-eat, modified atmosphere, or extended shelf-life food product introduction creates barrier film procurement whose aggregate across the global food industry’s extraordinary product innovation pace sustains market demand.

Sustainable recyclable barrier film transition represents the most commercially transformative product development direction whose regulatory mandate under EU PPWR creates structured reformulation procurement from the European food and consumer goods packaging sector. Each brand owner whose sustainability commitment requires mono-material recyclable barrier packaging creates procurement demand for recyclable barrier film alternatives whose innovation investment sustains above-average product development commercial activity.

Restraints: Raw material price volatility and environmental concerns about non-biodegradable barrier materials

Petrochemical raw material price volatility creates barrier film production cost uncertainty whose impact on margin predictability limits manufacturer investment confidence. Each crude oil and naphtha price spike creates downstream polyethylene, polypropylene, and specialty barrier resin cost variation that moderates commercial stability for barrier film producers whose pricing power is limited by competitive market dynamics.

Environmental concerns about the biodegradability and recyclability of conventional barrier film structures whose multi-layer laminate design prevents straightforward mechanical recycling create growing regulatory and consumer pressure whose commercial consequence is mandatory reformulation investment that creates transition cost and timeline uncertainty.

Opportunities: Recyclable mono-material barrier structures and pharmaceutical-grade specialty film

Recyclable mono-material barrier film represents the most commercially transformative near-term opportunity whose EU PPWR mandate creates structured procurement from European brand owners with 2030 packaging recyclability compliance deadlines. Each mono-material recyclable barrier film launch that achieves commercial barrier performance parity with conventional multi-layer laminates creates market access whose sustainable credential commands premium pricing.

Pharmaceutical-grade specialty barrier film represents a premium commercial opportunity whose sterile barrier packaging, blister film, and cold-form foil applications create above-commodity pricing relationships whose pharmaceutical industry growth sustains procurement expansion.

Recent Developments:

-

2024: Toppan and Toppan Specialty Films launched GL-SP barrier film in March 2024, using a biaxially oriented polypropylene (BOPP) substrate with advanced inorganic barrier coating creating recyclable high-barrier packaging compatible with plastic film recycling infrastructure.

-

2024: Amcor launched AmLite Ultra Recyclable barrier film in 2024, achieving supermarket-grade recyclability with oxygen and moisture barrier performance for fresh food, snacking, and dairy flexible packaging applications requiring sustainable mono-material structure.

-

2023: Amcor introduced a new line of recyclable barrier films in 2023 designed to meet growing demand for sustainable packaging solutions, offering enhanced barrier properties while maintaining compatibility with existing recycling infrastructure.

Barrier Films Market Key Players:

-

Amcor Plc

-

Berry Global Inc.

-

Sealed Air Corporation

-

Toppan Holdings Inc.

-

Mondi Group

-

Cosmo Films Ltd.

-

Uflex Limited

-

Huhtamaki Oyj

-

Innovia Films Ltd. (CCL Industries)

-

Toray Plastics Inc.

-

Treofan Group

-

Bemis Company (Amcor)

-

Printpack Inc.

-

Wipak GmbH

-

Constantia Flexibles

-

Klöckner Pentaplast Group

-

SKC Co., Ltd.

-

Transcontinental Inc.

-

Winpak Ltd.

-

ProAmpac LLC

Barrier Films Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.92 Billion |

| Market Size by 2035 | USD 63.44 Billion |

| CAGR | CAGR of 4.77% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Blown Film, Cast Film, Biaxially Oriented Film/BOPET/BOPP/BOPA) • By Material (Polyethylene/PE, Polypropylene/PP, Polyester/PET, EVOH, Polyamide/Nylon, Aluminum Foil, PVDC/Saran, Others) • By Application (Food & Beverage, Pharmaceutical & Healthcare, Agriculture, Electronics, Industrial & Chemical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amcor Plc, Berry Global Inc., Sealed Air Corporation, Toppan Holdings Inc., Mondi Group, Cosmo Films Ltd., Uflex Limited, Huhtamaki Oyj, Innovia Films Ltd. (CCL Industries), Toray Plastics Inc., Treofan Group, Bemis Company (Amcor), Printpack Inc., Wipak GmbH, Constantia Flexibles, Klöckner Pentaplast Group, SKC Co., Ltd., Transcontinental Inc., Winpak Ltd., ProAmpac LLC |

Frequently Asked Questions

The Barrier Films Market is expected to grow at a CAGR of 4.77% from 2026 to 2035.

The Barrier Films Market was valued at USD 38.92 Billion in 2025.

Technology upgrades and growing preference for sustainable packaging, combined with rising demand for food shelf-life extension creating consistent barrier film procurement across the global food and beverage packaging sector.

Blown Film dominated the Barrier Films Market with 55% share in 2025 (confirmed by SNS Insider), while Cast Film is the fastest growing segment.

Asia Pacific held the largest market share at approximately 35% in 2025, while North America is the fastest-growing region.

Get in Touch